The current section of the “Analysis” series covers Safari Industries (India) Ltd, a company selling luggage, backpacks etc. under brands like Safari, Genius, Genie, Magnum etc.

“Analysis” series is an attempt to share with all the readers, our inputs to the company analysis submitted by readers on the “Ask Your Queries” section of our website.

Please note that to benefit the maximum from this article; an investor should focus on the process of analysis instead of looking for good or bad aspects of the company. She should learn the interpretation of different types of data and transactions and pay attention to the parts of annual reports etc. used to get the information. This will help her in improving her stock analysis skills.

Safari Industries (India) Ltd: Detailed Fundamental Analysis

Safari Industries (India) Ltd published both standalone as well as consolidated financials because, on March 31, 2022, it has two wholly-owned subsidiaries (WOS), Safari Lifestyles Limited and Safari Manufacturing Limited. The company started publishing consolidated financials for the first time in FY2015 after it formed its first WOS, Safari Lifestyles Ltd.

FY2015 annual report, page 10:

The wholly owned subsidiary of the Company, Safari Lifestyles Ltd., was incorporated on 30th October 2014

As a result, Safari Industries used to publish only standalone financials until FY2014 and from FY2015 onwards, it started publishing both standalone as well as consolidated financials.

We believe that while analysing any company, an investor should always look at the company as a whole and focus on financials, which represent the business picture of the entire company including its subsidiaries, joint ventures etc. The consolidated financials of a company present such a picture.

Further advised reading: Standalone vs Consolidated Financials: A Complete Guide

Therefore, in the case of Safari Industries (India) Ltd, during the last 10 years (FY2013-FY2022), we have analysed standalone financials for FY2013-FY2014 and consolidated financials from FY2015 onwards.

With this background, let us analyse the financial performance of Safari Industries (India) Ltd.

Financial and Business Analysis of Safari Industries (India) Ltd:

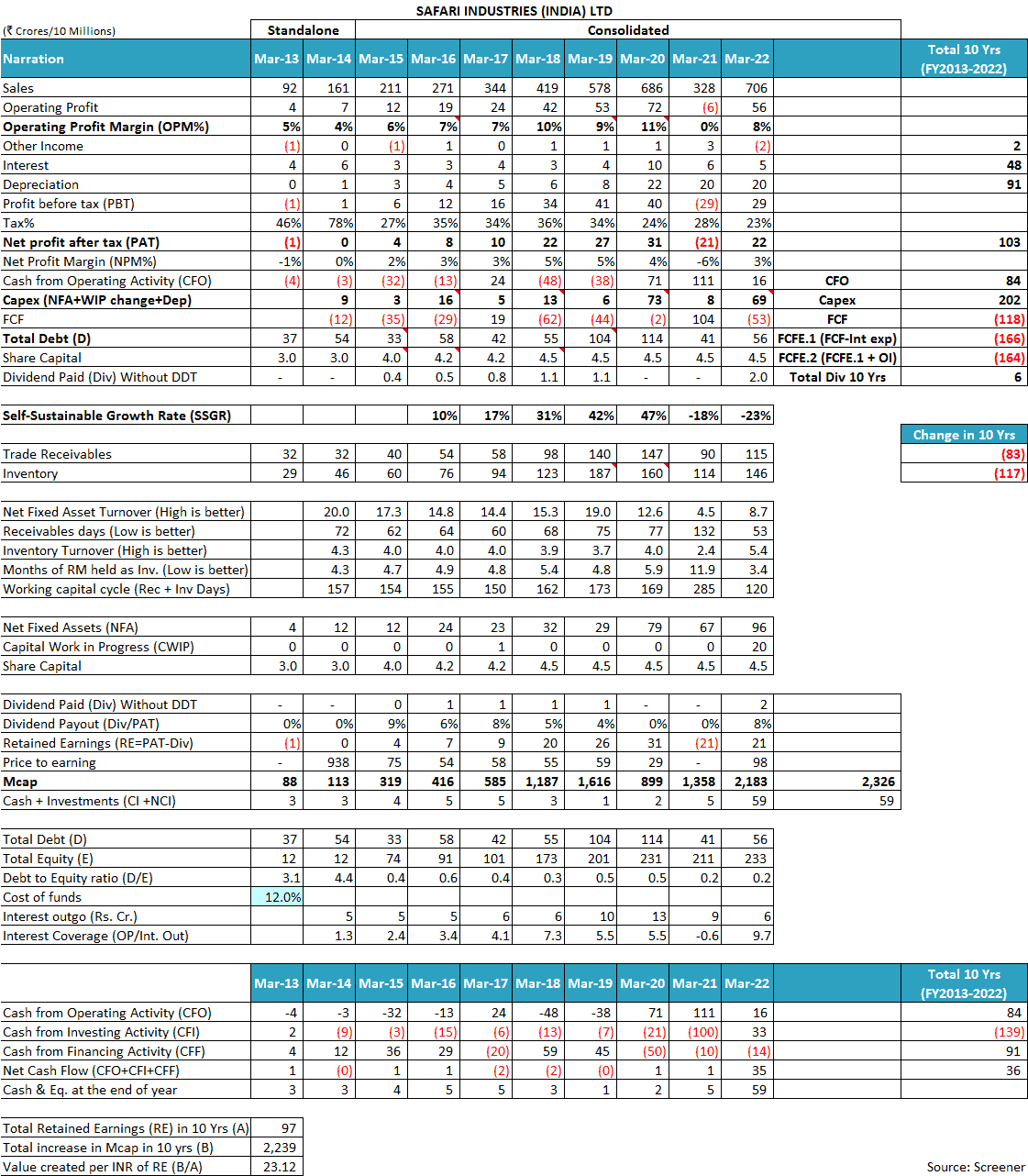

Sales of Safari Industries (India) Ltd have grown at a pace of 25% year on year from ₹92 cr in FY2013 to ₹706 cr in FY2022. The sales of the company have increased every year since FY2013 except FY2021 when the sales declined to ₹328 cr from ₹686 cr in FY2020. However, in the next year, FY2022, the sales of the company increased sharply to ₹706 cr.

On an overall basis, the operating profit margin (OPM) of the company has improved from 5% in FY2013 to 8% in FY2022. However, the OPM has seen a fluctuating pattern with periods of decline in FY2014, FY2019 and FY2021. The company reported net losses in FY2013 and FY2021.

To understand the reasons for the financial performance of Safari Industries (India) Ltd, an investor needs to read the publicly available documents of the company like its annual reports from FY1997 onwards, credit rating reports, corporate announcements as well as other public documents. Then she would understand the factors leading to an overall increase in its sales and profit margins over the years with fluctuations in between.

After going through the above-mentioned documents, an investor notices the following key factors, which influenced the business of Safari Industries (India) Ltd, which she needs to keep in her mind before making any predictions about the performance of the company.

1) Change of management of Safari Industries (India) Ltd in 2012:

The management of Safari Industries changed in April 2012 when Mr Sudhir Jatia purchased a majority stake in the company from its founding promoters, the Mehta family.

FY2012 annual report, page 10:

Mr. Sudhir M. Jatia (Promoter) and Mrs. Neeti S. Jatia (PAC) have directly and indirectly acquired, on 18th April, 2012, 22,95,933 equity shares of the company, aggregating to 76.79% of the paid up capital of the Company.

This change in the management of the company has been the single biggest factor, which led to sharp improvements in the sales and profits of the company.

Data on the financial performance of Safari Industries since FY1993 is present in the public domain (FY1997 annual report, page 2). From FY1993 to FY2012, the company was in the control of the Mehta family and thereafter, Mr Jatia controlled it.

Under the Mehta family (FY1993 to FY2012), the net sales of the company increased from ₹26 cr to ₹62 cr at compounded annual growth rate (CAGR) of 4.7% whereas, under Mr Jatia (from FY2012 to FY2022), the sales increased from ₹62 cr to ₹706 cr at a CAGR of 27.5%.

Let us see some of the steps taken by Mr Jatia to increase the growth of Safari Industries.

1.1) Expanding sales channels, focus on advertising and discounts by Safari Industries:

It seems that the Mehta family did not push the company for growth. They relied mainly on one customer, the canteen stores department (CSD) for sales. The dependence of the company on CSD was so much that any factor influencing sales of CSD items had a significant impact on the performance of Safari Industries.

In FY2006, the company witnessed a decline in revenue and a net loss. The company intimated to its shareholders that the poor performance including losses was due to lower sales from CSD due to the introduction of taxes (value-added tax, VAT) on sales at CSD.

FY2006 annual report, page 7:

Sales and other income have been more or less stagnant…as sales to Canteen Stores Department were significantly affected due to imposition of VAT on their sales, which were hitherto exempted from Sales Tax, which has also affected profitability.

Sales of Safari Industries were so much concentrated in CSD that even under the new management, in FY2015, CSD constituted 55% of its sales.

Credit rating report by India Ratings, June 2015:

The ratings are constrained by demand off-take risks with a large concentration of sales to a single counterparty (CSD)…In FY15, sales to CSD accounted for around 55% of the turnover

Nevertheless, the moment Mr Jatia took over Safari Industries, he focused on expanding the sales channels. Immediately after the management change, in FY2013, Safari Industries started focusing on alternate channels like hypermarkets.

FY2013 annual report, page 5:

The Company is also exploring various new channels of marketing and retail and has tied up with renowned hypermarket chains such as D’mart, Reliance Retail, Big Bazaar, Bharti Walmart, etc.

For the first time, in FY2014, Safari Industries opened its exclusive showrooms.

FY2014 annual report, page 10:

The Company has also opened almost 50 exclusive retail stores and plans to add further in the years to come.

In FY2015, the company began selling its products on various online portals like Amazon, Flipkart etc.

FY2015 annual report, page 11:

Company has also begun its ecommerce play with listing & selling the products in marketplace websites such as amazon.in, snapdeal.com, myntra.com, jabong.com & flipkart.com

The company began spending aggressively on advertising including offering discounts to increase its sales. In the first full year under Mr Jatia, in FY2014, the advertising spending of the company increased to about 2.5 times from ₹2.8 cr in FY2013 to ₹6.9 cr in FY2014. Similarly, the discounts given by the company increased in FY2014 to 3.5 times from ₹1.5 cr in FY2013 to ₹5.1 cr in FY2014.

Advised reading: How to do Business Analysis of Organised Retail Companies

1.2) Expanding product range and brands of Safari Industries:

In addition, Mr Jatia expanded the product range of Safari Industries from luggage to other related categories like backpacks, laptop bags etc., which were low-ticket items but needed frequent replacements than traditional luggage bags.

FY2014 annual report, page 10:

The Company also introduced new product lines such as laptop bags, back packs, etc. which are fast selling items

A timely entry into the backpacks segment led to a significant increase in the market share of Safari Industries.

Credit rating report by CRISIL, October 2017, page 1:

improvement in market share is backed by the company’s foray into the backpack segment in fiscal 2017.

In FY2016, the company acquired many brands like Genius, Genie, Magnum, Gscape etc. to offer products to different sub-segments of consumers.

Corporate presentation, August 2021, page 8:

FY2016: Acquired Genius, Activa, Magnum, Orthofit, DBH, Egonauts, Gscape and Genie brands

It also acquired distribution rights of a UK brand, Antler to target the premium luggage segment.

FY2016 annual report, page 56:

Company is becoming multi brand as during the year it acquired brands like Genius & Magnum and also signed a distribution agreement for India with ANTLER, a popular luggage brand in UK.

In addition, Mr Jatia led Safari Industries to introduce polycarbonate-based hard luggage, which was the consumers’ preference by creating a manufacturing unit for polycarbonate-based luggage at Halol.

FY2013 annual report, page 5:

Company is currently in the process of setting up a Poly Carbonate Plastic luggage project at its factory at Halol, Gujarat, which will facilitate manufacturing of Poly Carbonate Plastic luggage. Poly Carbonate Plastic luggage is the new trend in the luggage industry and is increasingly gaining popularity.

FY2014 annual report, page 10:

Company has successfully launched the poly carbonate luggage range in the month of March, 2014.

Therefore, an investor would note that under the founder-promoters, the Mehta family, Safari Industries was a slow-moving company with a limited product range focusing solely on CSD sales. No wonder it grew only at an annual rate of 4.7% over 20 years (FY1993-FY2012).

However, the moment, Mr Jatia took over the company in April 2012, he expanded the focus of the company in all aspects like new trendy luggage types (polycarbonate), new product categories (backpacks, laptop bags), sales channels (exclusive stores, hypermarkets, online stores) and also did aggressive marketing combined with discounts.

Such an aggressive growth strategy by the new management increased the annual sales growth of Safari Industries to more than 25% every year.

After understanding the huge impact created by Mr Jatia on Safari Industries, an investor would want to know about what skills Mr Jatia brought with him that he could bring massive changes in the business performance of Safari Industries.

When Mr Jatia took over Safari Industries, he was already an industry veteran and had worked as the managing director of VIP Industries Ltd, a Dilip Piramal Group company, which is the market leader in the luggage industry in India. He had to leave VIP Industries to vacate the leadership position for Radhika Piramal, a member of the Piramal family. (Source: Former VIP Industries MD Sudhir Jatia Buying 56.55% In Safari Inds: VCCircle, Sept 7, 2011)

Therefore, when Mr Jatia left VIP Industries, then he took over a small player in the industry, Safari Industries and applied his leadership skills to refine its business model to grow it at a brisk pace. In FY2022, Safari Industries managed to acquire about a 20% share of the luggage market in India.

Credit rating report by CRISIL, January 2022, page 1:

Safari has also gained in market share within the organized segment by around 800 bps in the past three fiscals, strengthening its market share to over 20-22%.

Therefore, over the last decade, the single biggest factor that has led to a change in the business fortunes of Safari Industries is the change in management of the company from the Mehta family to Mr Jatia.

Advised reading: Why Management Assessment is the Most Critical Factor in Stock Investing?

2) Intense competition in the luggage industry:

The luggage industry in India faces severe competition both from the unorganized sector as well as within the organized sector.

The unorganized sector constitutes a major portion of the luggage sales where many traders import bags from China, Bangladesh etc. and sell them in Indian markets. These bags are priced cheaper than the products of the organized sector. As a result, they put strong pricing pressure on the organized players.

One of the reasons for the large presence of the unorganized sector in the luggage industry is a very low requirement for research and development (R&D). In fact, even organized players like Safari Industries do not spend any money on R&D.

FY2022 annual report, page 41:

The expenditure incurred on Research and Development: Nil

Because of low R&D and simple manufacturing processes, many players from the unorganized sector are able to establish luggage bag manufacturing units or import readymade bags from countries like China, Bangladesh etc. and sell them in the market at low prices.

Among the organized sector, the Indian luggage industry is dominated by three players: VIP, Samsonite and Safari. Among the organized sector players as well, there is intense competition with aggressive marketing and discounts to gain market share. Recently, VIP Industries Ltd ran an offer where it announced a free stay at a 5-star hotel for one night on purchasing luggage bags of ₹5,999/- and above (Source: VIP Impossible Offer. It is Impossible. And it is back).

Safari Industries has highlighted unfair competition among luggage manufacturers as one of the key risks that it faces.

FY2016 annual report, page 57:

The major risks as identified by the Company are overdependence on China for purchase of soft luggage, risk of exchange loss associated with imports, unfair competition, brand positioning, etc.

Such industry dynamics where numerous unorganized players compete with low-priced offerings, as well as intense competition among organized players, creates a tough situation for players in a price-value-conscious consumer market.

The direct result of such intense competition is a lack of pricing power in the hands of luggage players.

3) Low pricing power of Safari Industries (India) Ltd:

Due to intense competition, Safari Industries (India) Ltd is not able to freely increase its product prices when it faces an increase in its raw material costs. As a result, on numerous occasions in the past, Safari Industries has to take a hit on its profit margins, which, at times, has even resulted in net losses for the company.

In FY2001, Safari Industries suffered a net loss and intimated to its shareholders that it could not pass on the increase in raw material costs to its customers.

FY2001 annual report, page 4:

The profitability was further adversely affected due to cost escalation of major inputs like plastic and aluminium during the year, which could not be passed on due to drop in demand for moulded luggage.

In FY2004 as well, Safari Industries highlighted that it suffered, as it could not pass on the increase in input costs to its customers.

FY2004 annual report, page 5:

The year under review has been a difficult one with profitability being adversely affected due to cost escalation of all major raw materials like Plastic, Aluminium and other inputs during the year, which had been absorbed by the Company due to sluggish demand for Moulded luggage.

In FY2007, the company worked hard to increase its sales; however, its profits declined as it could not pass on the increase in raw material costs to its customers.

FY2007 annual report, page 7:

Despite substantial improvement in sales, the margins remained under pressure due to unabated increase in the cost of all raw materials on the back of increase in crude oil and commodity prices.

In FY2012, Safari Industries suffered losses. It intimated to its investors that one of the reasons leading to losses was an increase in raw material costs.

FY2012 annual report, page 10:

The loss for the year is mainly on account of exchange loss of Rs.130.87 lacs and significant increase in raw material cost due to rising commodity prices.

In FY2017, Safari Industries highlighted that due to intense competition it had to absorb a part of the cost increases, as it could not fully pass on the increase in input costs. The company also highlighted that the intense competition in the luggage industry would continue to put pressure on its profit margins.

FY2017 annual report, pages 53-54:

Further, due to intense competition, only some increases were passed on to customer through price increases which partially but not fully offset these increased costs….margins may continue to experience pressure on account of intense competition

In FY2019, when the profit margins of the company declined, then it highlighted the increase in the cost of purchases from China as the reason why these increased costs could not be passed on to the customers.

FY2019 annual report, page 45:

During the year, there was increased upwards pressure on buying costs of imported products from China

Therefore, an investor would note that over the last 20 years, the business of Safari Industries has continuously faced challenges in passing on the increase in input costs to its customers. At times, it had to suffer and face losses. Intense competition in the luggage industry is the primary reason for the low pricing power of Safari Industries.

Advised reading: How to do Business Analysis of a Company

4) Foreign exchange fluctuation risk is significant for Safari Industries (India) Ltd:

A significant part of the overall costs of Safari Industries is influenced by fluctuations in the foreign exchange (forex) i.e. movement of the Indian Rupee (INR) against foreign currencies especially the US Dollar (USD). Foreign exchange fluctuations influence its business in two aspects.

First, Safari Industries imports most of its soft luggage bags from either China or Bangladesh, which are priced in USD. Any fall in the value of the Indian Rupee against the USD increases the cost of these bags for Safari Industries in INR.

In FY2017 when INR depreciated against USD, the profit margins of Safari Industries were impacted as the cost of imports increased for the company.

FY2017 annual report, page 53:

Imported Soft luggage across product categories is the major contributor to the sales of the Company. During the year, rupee remained weak and the Company’s buying costs of imported products remained high in rupee terms due to depreciation of rupee against USD which has put pressure on margins.

Similarly, in FY2019, Safari Industries faced margin pressure due to INR depreciation against USD.

FY2019 annual report, page 45:

During the year, there was increased upwards pressure on buying costs of imported products from China due to increase in import duty and adverse exchange rate movements.

Second, the company makes hard luggage from plastic like polycarbonate or polypropylene whose prices are linked to crude oil prices. Prices of these products are based on import parity and whenever the value of INR declines against USD, then the cost in INR for all these raw materials derived from crude oil increases.

FY2007 annual report, page 7:

Despite substantial improvement in sales, the margins remained under pressure due to unabated increase in the cost of all raw materials on the back of increase in crude oil and commodity prices.

Therefore, the profit margins of Safari Industries remain vulnerable to adverse movements of INR against USD.

Credit rating report by CRISIL, January 2017, page 1:

Exposure to volatility in raw material prices and foreign exchange rates: Profitability is susceptible to prices of imported raw material, which account for over 45% of operating cost.

Advised Reading: Credit Rating Reports: A Complete Guide for Stock Investors

On multiple occasions, Safari Industries has suffered significant losses due to foreign exchange fluctuations.

In FY2012, the company reported losses when it suffered a large foreign exchange fluctuation loss.

FY2012 annual report, page 10:

The loss for the year is mainly on account of exchange loss of Rs.130.87 lacs

In FY2014, Safar Industries reported forex losses of ₹3.75 cr (FY2014 annual report, page 10). In FY2020, it suffered a forex loss of ₹2.1 cr (FY2020 annual report, page 146).

Safari Industries has identified forex/currency risk as one of the key risks to its business.

FY2022 annual report, page 43:

The major risks as identified by the Company are demand-risks due to any resurgence in the COVID 19 pandemic, currency risk associated with imports, unfair competition, etc.

5) Adjustment of product mix as per markets’ preferences:

Over the years, Safari Industries has changed its product mix in line with ongoing customer preferences. For example, previously, it used to make primarily hard luggage that too without wheels. However, the customers started preferring wheeled luggage bags with a preference for soft luggage.

As a result, in FY2012, the company’s business performance suffered and the company reported losses when the demand for hard luggage declined sharply.

FY2012 annual report, page 10:

The drop in sales is mainly on account of 30% degrowth in sales of Hard Luggage due to falling demand.

Credit rating report by India Ratings, February 2013:

Operating profits declined to INR39m in FY12 (FY11: INR61m) on account of a rise in input costs due to INR depreciation and a revenue decline in the hard luggage segment which contributed over 50% of the turnover in FY12.

In FY2012, despite a 30% decline in sales of hard luggage, it still constituted more than 50% of revenue. However, the company quickly changed its product mix and within the next 3 years, by FY2015, soft luggage contributed 80% of its sales and hard luggage was reduced to 20% of sales.

Credit rating report by India Ratings, June 2015:

sale of soft luggage accounts for around 80% of the company’s turnover, followed by hard luggage which accounts for the remaining sales

This major change was led by changing consumer preferences in the market.

FY2016 annual report, page 56:

Major growth is observed in soft luggage uprights and polycarbonate uprights, whereas traditional hard luggage, made of Poly Propylene saw a steep drop in Sales. This shift is due to change in consumer preferences towards the convenience of light and wheeled travel products and away from heavier products without wheels

The rise in the share of soft luggage also added to the profitability of Safari Industries.

Credit rating report by India Ratings, June 2015:

increased contribution of soft luggage sales to overall sales volumes led to a sustained improvement in the EBITDAR margins (FY15: 7.6%, FY14: 5.9%, FY13: 4.4%).

Another key change effected by Safari Industries was the start of manufacturing of polycarbonate zipped luggage bags immediately after the takeover by Mr Jatia. It was also in line with the upcoming consumer preferences.

Investors noticed that over FY2012-FY2015, consumer preferences changed from hard luggage to soft luggage. Once again, over the next 4 years, consumer preferences changed again and now instead of soft luggage, the market started preferring trendy-looking lightweight polycarbonate hard luggage.

FY2019 annual report, page 46:

Major growth was observed in Polycarbonate Uprights, due to shifting consumer preference from Soft Luggage to more durable and premium looking hard luggage.

Therefore, the product mix of Safari Industries shifted from 20% soft luggage in FY2015 to 33% soft luggage in FY2020 (FY2020 annual report, page 38).

Moreover, the company continued to invest to increase the manufacturing capacity of zippered polycarbonate hard luggage.

FY2018 annual report, page 50:

To meet the overall growth objectives, the Company has increased its manufacturing capacity of polycarbonate luggage at its Halol Plant

The company increased its manufacturing capacity for polycarbonate luggage in FY2021 and then again in FY2022.

FY2021 annual report, page 44:

Company continued to invest in Zippered Hard Luggage by continuing to expand its range of Polycarbonate zippered cases as well as enhancing production capacity at its manufacturing plant in Halol, Gujarat.

In 2022, the company further expanded its manufacturing capacity of polypropylene zippered hard luggage by creating a new manufacturing unit in a newly bought property.

FY2022 annual report, page 41:

Company is also setting up a new manufacturing plant through its wholly owned subsidiary in Halol, Gujarat for additional capacity for polypropylene zippered hard luggage.

The plant was completed in June 2022. The corporate announcement, BSE, June 17, 2022:

Safari Manufacturing Limited, the wholly owned subsidiary of the Company has successfully commenced its commercial production/manufacturing of luggage today i.e. 17th June 2022 at its newly set up factory situated at Halol, Gujarat

The company has continued to invest as per the changing preferences of the consumers.

FY2022 annual report, page 43:

The trend of rising consumer preference for zippered hard luggage category continued as it is perceived to be more premium and durable. This trend was also accelerated by relatively higher availability and lower pricing for zippered hard luggage compared to soft luggage.

The company has also discontinued its products, which did not get sufficient consumer attention. For example, it stopped the production of non-wheeled-framed hard luggage.

FY2020 annual report, page 50:

Company discontinued its product ranges of framed hard luggage, made of Polypropylene given the lack of consumer demand in this category.

Advised Reading: How to study the Annual Report of a Company

Therefore, the ability of the company to switch from hard luggage to soft luggage during FY2012-FY2015 and then again to hard luggage in line with the market’s preference has helped Safari Industries to grow its business significantly during the last 10 years.

6) Shifting of sourcing of soft luggage by Safari Industries:

Safari Industries manufactures only hard luggage in its production units. It sources all of its soft luggage products including backpacks and laptop bags etc. from third parties, primarily from imports. Previously, it used to rely solely on China to meet its requirements for soft luggage.

Credit rating report by India Ratings, June 2015:

Soft luggage is imported from Chinese manufacturers and is sold by the company under its own brand name, while hard luggage is manufactured in-house at the company’s facility located at Halol, Gujarat.

The company had identified its overdependence on China for soft luggage, which constituted a majority of its sales, as a major risk.

FY2016 annual report, page 57:

The major risks as identified by the Company are overdependence on China for purchase of soft luggage

This risk materialized later on when the Chinese govt. started a crackdown on polluting units. In addition, the Govt. of India imposed a customs duty on the import of soft luggage from China.

FY2019 annual report, page 45:

During the year, there was increased upwards pressure on buying costs of imported products from China due to increase in import duty

Safari Industries started diversifying its sourcing for soft luggage from China to India and Bangladesh.

FY2020 annual report, page 50:

Company is also increasing its outsourcing of soft luggage and backpacks from India and Bangladesh.

By FY2022, the company had tied up with manufacturing units in Bangladesh for production exclusively for Safari Industries.

Corporate presentation, August 2021, page 16:

Captive 3rd party capacity in Bangladesh

As a result, of this shift, the company could diversify its supply chain, make it more secure as well as achieve cost benefits.

FY2022 annual report, page 42:

The Company has significantly enhanced its sourcing from manufacturing bases in India and Bangladesh reducing its dependence on Chinese imports. This shift has helped improve supply security as well as relative cost savings given the continued global supply chain disruptions.

The ability of the company to change its sourcing model in light of challenges faced from China has helped it to grow its business profitably.

7) Risk of recessions, reduced travel and wedding expenditure:

The demand for luggage products made by Safari Industries is primarily dependent on travel undertaken by the public. Therefore, during recessions when companies, as well as public, cut down their travels, then the sales of Safari Industries suffer.

For example, during the dot com bubble in FY2001-FY2002, the recession coupled with reduced travel following the 9/11 attacks, the Indian parliament attack (December 13, 2001) led to a sharp decline in the sales and losses for Safari Industries.

FY2001 annual report, page 4:

Production and sales were significantly affected as demand for consumer durable goods has been sluggish due to recessionary conditions in the economy.

FY2002 annual report, page 4:

The events of the 11th September, 2001 and 13th December, 2001 adversly affected Travel and many other industries…Sales and other income decreased from Rs. 5393.13 lakhs to Rs. 3912.58 lakhs. The net loss of Rs. 111.08 lakhs

Once again, in FY2009, the sales of the company declined due to the global recession.

FY2009 annual report, page 5:

Net Sales and other income has been stagnant at Rs.61,06 crores compared to Rs.62.45 crores in the previous year mainly due to slow down in the economy.

Similarly, in FY2021, when there was a lockdown in India due to coronavirus and travel as well as wedding spending declined, then the business of Safari Industries suffered significantly. Its sales declined by more than 50% over FY2020 and it reported operating losses.

However, in FY2022 when the lockdown was lifted and travel resumed, then the business of the company revived and it reported all-time high sales of ₹706 cr in FY2022.

FY2022 annual report, page 41:

travel industry is seeing an unprecedented boom with consumers looking to get out of their houses after long period of lock-downs. Marriage demand has also been strong led by the opening of the economy and easing of restrictions

Similarly, in FY2016 when the travel industry recovered as well as the wedding season did well, then the business performance of Safari Industries improved.

FY2016 annual report, page 56:

Company witnessed a good growth in the topline during the year under review, owing to good wedding season and increase in domestic and international travel.

Therefore, an investor should note that any event affecting travel, holidaying, and social gatherings like weddings etc. would have a significant impact on the business of Safari Industries.

Advised reading: How to do Financial Analysis of a Company

Going ahead, an investor should keep a close watch on the profit margins of Safari Industries to understand how it is managing the increase in raw material costs and competition as well as monitor forex losses. She should track the changing product mix of the company to understand whether it is able to utilize its manufacturing capacities well.

In recent years (FY2016 onwards), the tax payout ratio of Safari Industries (India) Ltd has been in line with the standard corporate tax rate prevalent in India. The tax payout ratio has declined since FY2020 in line with the new corporate tax regime implemented in India.

Operating Efficiency Analysis of Safari Industries (India) Ltd:

a) Net fixed asset turnover (NFAT) of Safari Industries (India) Ltd:

Over the years, the NFAT of the company has declined from 20.0 in FY2014 to 8.7 in FY2022. Moreover, during this period, the NFAT of the company has fluctuated significantly.

First, NFAT declined sharply to 14.4 in FY2017, which coincided with the investments done by Safari Industries in the acquisition of brands like Genius, Genie, Magnum etc. as well as the expansion of hard luggage manufacturing capacity. As these investments took some time to contribute to the revenue of the company; therefore, in the interim, the NFAT of the company decreased.

As these investments started adding to the revenue, then the NFAT increased to 19.0 by FY2019. In FY2021, the NFAT declined to its lowest level of 4.5, which is due to a decline in the business of the company because of Covid-lockdowns.

In FY2022, the NFAT of the company recovered to 8.7; however, it is still lower than the historical levels due to two factors. First, in recent years, the sale of zippered hard luggage made of polycarbonate is increasing, which is made by Safari Industries in-house at Halol. Previously, almost 80% of sales were soft luggage, which was imported/traded. An increase in the share of trading/imported items in the sales increases the NFAT of the company whereas an increase in the in-house manufactured items decreases the NFAT.

Secondly, in FY2022, Safari Industries India Ltd created a new manufacturing unit by buying out a land parcel with the existing structure. This new plant became operational in June 2022. This new investment, which is yet to contribute to sales, has also led to a decline in the NFAT in FY2022.

Going ahead, an investor should keep a close watch on the NFAT of the company to assess whether it is able to use its newly created manufacturing capacity in an optimal manner.

Further advised reading: Asset Turnover Ratio: A Complete Guide for Investors

b) Inventory turnover ratio (ITR) of Safari Industries (India) Ltd:

Over the years, the inventory turnover ratio (ITR) of the company has increased from 4.3 in FY2014 to 5.4 in FY2022. However, before improving to 5.4 in FY2022, the ITR of Safari Industries declined significantly to 3.7 in FY2019 and then to 2.4 in FY2021.

The consistent decline of ITR from 4.3 in FY2014 to 3.7 in FY2019 is mainly linked to the expansion of sales channels by the company during this period along with a wide product range consisting of multiple brands. The inventory needs of the company increased as it opened exclusive showrooms as well as in the hypermarkets. The company had to keep more inventory in its warehouses to meet demand from e-commerce websites.

FY2019 annual report, page 45:

Company continued its focus on building the Safari brand via launches of innovative new products and a new advertising campaign to drive visibility. The Magnum brand was strengthened with a larger product portfolio and wider channel availability.

In order to ensure that the sales channel has sufficient stock of its products, Safari Industries increased its inventory levels. In FY2019, the company was carrying an inventory of ₹187 cr up from ₹29 cr in FY2013.

In addition, the sales of the company show some seasonality with sales increasing in the first quarter of the financial year in line with the wedding season. The company needs to keep a high inventory to meet the seasonal demand.

Credit rating report by CRISIL, October 2017, page 1:

inventory holding is high at 103 days since the company needs to maintain higher inventory due to seasonality of sales, especially for the first quarter of the fiscal.

Moreover, the company used to import almost all of its soft luggage/backpacks etc. from China. It opened two offices in China starting 2015 to meet its demand for soft luggage. In the import process, a large amount of inventory is consumed in the supply chain/transit, which lowers the inventory turnover ratio.

As a result, when in recent years, Safari Industries diversified its sourcing of soft luggage from China to India and Bangladesh as well as increased the sales of hard luggage, which it makes in-house, and its inventory requirements declined.

Credit rating report by CRISIL, March 2020, page 2:

The improvement in inventory is backed by lower import of luggage from China and higher revenue contribution from hard luggage, which is manufactured in India and has lower inventory levels.

Going ahead, an investor should keep a close watch on the inventory levels of the company. This is because, as discussed earlier, the luggage industry faces frequent changes in consumer preferences. As a result, current inventory may become unsaleable in the future.

In the past, there have been instances when Safari Industries had to write down its existing stock of luggage bags, as it could not sell them in the market.

In FY2013, Safari Industries wrote down stock/inventory of about ₹2.8 cr (FY2013 annual report, page 24). Again, in the next year, FY2014, the company further wrote down stock/inventory of ₹0.27 cr (FY2014 annual report, page 30).

Therefore, going ahead, an investor should keep a close watch on the ITR of the company to assess whether it is using its inventory efficiently.

Further advised reading: Inventory Turnover Ratio: A Complete Guide

c) Analysis of receivables days of Safari Industries (India) Ltd:

Over the years, the receivables days of Safari Industries (India) Ltd have improved from 72 days in FY2014 to 53 days in FY2022.

One of the major reasons for this improvement seems to be diversification of sales channel from an earlier focus solely on canteen stores department, which is run by army/govt. to now a broad-based sales channel including exclusive stores, hypermarkets, e-commerce websites etc.

Most of the time, businesses face delays in receiving money from govt. agencies. However, with increasing sales from other channels, the recovery of money by Safari Industries seems to have improved.

In FY2021, the company reported receivables days of 132 days, which is primarily due to Covid-lockdown-related difficulties faced by businesses. As a result, the company had to provide for/write off a significant amount of receivables.

In FY2022, Safari Industries wrote off receivables of about ₹10.5 cr and further provided for ₹5 cr worth of receivables (FY2022 annual report, page 146).

While assessing the receivables position of Safari Industries on March 31, 2022, an investor notes that it has impaired about ₹14.4 cr of receivables, which includes more than ₹9 cr of receivables due for more than one year. It also impaired receivables, which are less than 6 months old. These might be due from customers, which suffered a lot during Covid restrictions.

FY2022 annual report, page 149:

Going ahead, an investor should monitor the trend of receivables days of Safari Industries (India) Ltd to assess whether it is able to collect its overdue receivables and keep its receivables position under control.

Further advised reading: Receivable Days: A Complete Guide

When an investor compares the cumulative net profit after tax (cPAT) and cumulative cash flow from operations (cCFO) of Safari Industries (India) Ltd for FY2013-2022, then she notices that over the years (FY2013-FY2022), the company is not able to convert its profit into cash flow from operations.

Over FY2013-22, Safari Industries (India) Ltd reported a total net profit after tax (cPAT) of ₹103 cr. During the same period, it reported cumulative cash flow from operations (cCFO) of ₹84 cr.

It is advised that investors should read the article on CFO calculation, which would help them understand the situations in which companies tend to have the CFO lower than their PAT. In addition, the investors would also understand the situations when the companies would have their CFO higher than the PAT.

Further advised reading: Understanding Cash Flow from Operations (CFO)

In the case of Safari Industries, the cCFO is less than cPAT because of its working capital-intensive business operations. Due to its higher inventory requirements, a lot of cash generated by the company from its operations is stuck in additional inventory required for business growth.

Credit rating report by India Ratings, June 2015:

The ratings are also constrained by the working capital intensive nature of SIIL’s operations. The firm has a long cash conversion cycle (FY15: 179 days), primarily due to its large inventory holding requirement. Furthermore, cash flow from operations has remained negative (FY15: negative INR342.6m, FY14: negative INR80m) due to the incremental working capital requirements arising from the high growth in scale.

Therefore, going ahead, an investor should keep a close watch on the working capital position of the company to understand whether it is able to manage its inventory and receivables position well.

The Margin of Safety in the Business of Safari Industries (India) Ltd:

a) Self-Sustainable Growth Rate (SSGR):

Read: Self Sustainable Growth Rate: a measure of Inherent Growth Potential of a Company

Upon reading the SSGR article, an investor would appreciate that if a company is growing at a rate equal to or less than the SSGR and it can convert its profits into cash flow from operations, then it would be able to fund its growth from its internal resources without the need of external sources of funds.

Conversely, if any company attempts to grow its sales at a rate higher than its SSGR, then its internal resources would not be sufficient to fund its growth aspirations. As a result, the company would have to rely on additional sources of funds like debt or equity dilution to meet the cash requirements to generate its target growth.

An investor may calculate the SSGR using the following formula:

SSGR = NFAT * NPM * (1-DPR) – Dep

Where,

- SSGR = Self Sustainable Growth Rate in %

- Dep = Depreciation rate as a % of net fixed assets

- NFAT = Net fixed asset turnover (Sales/average net fixed assets over the year)

- NPM = Net profit margin as % of sales

- DPR = Dividend paid as % of net profit after tax

(For systematic algebraic calculation of SSGR formula: Click Here)

While analysing the formula of SSGR, an investor would note that it is dependent on NFAT, which indicates the efficiency with which a company is able to manage its plants & machinery. In the case of Safari Industries, a major portion of sales is achieved by soft luggage, where production is fully outsourced.

As a result, in the case of Safari Industries, SSGR may not provide the best results and we have to rely on the assessment of free cash flow to assess the margin of safety in the business model of the company.

b) Free Cash Flow (FCF) Analysis of Safari Industries (India) Ltd:

While looking at the cash flow performance of Safari Industries (India) Ltd, an investor notices that during FY2013-FY2022, it generated cash flow from operations of ₹84 cr. During the same period, it did a capital expenditure of about ₹202 cr.

Therefore, during this period (FY2013-FY2022), Safari Industries (India) Ltd had a negative free cash flow (FCF) of (₹118) cr (=84 – 202).

In addition, during this period, the company had a non-operating income of ₹2 cr and an interest expense of ₹48 cr. As a result, the company had a total negative free cash flow of (₹164) cr (= -118 + 2 – 48). Please note that any capitalized interest is already factored in as a part of the capex deducted earlier.

To meet this shortfall of ₹164 cr, Safari Industries (India) Ltd had to raise debt as well as additional equity. The company primarily relied on equity dilution as the total debt of the company increased only by ₹19 cr during FY2013-FY2022 from ₹37 cr to ₹56 cr.

In the past, the company had the following instances of equity dilution:

- FY2021: ₹75 cr by issuing Compulsorily Convertible Debentures (CCDs) to Investcorp Private Equity Fund II (FY2021 annual report, page 16)

- FY2018: ₹50 cr by allotting shares to two Malabar Funds (FY2018 annual report, page 36)

- FY2015: about ₹70 cr by issuing shares to Tano India Pvt Equity Fund II (₹49.8 cr) and warrants to the promoter Mr Jatia (₹19.8 cr) (FY2015 annual report, pages 11-12)

Moreover, the requirement for additional money is not a recent phenomenon for Safari Industries. Even in the previous decade, in FY2007, under the founder-family, Mehtas, the company had to dilute its equity to raise ₹1.4 cr to meet its business requirements (FY2007 annual report, page 8).

Therefore, an investor would note that the business of Safari Industries is capital intensive, which needs a significant investment in working capital. The funds’ requirement of the company is much more than what it is able to generate through its operations. As a result, the business looks like a cash-guzzling machine.

At times, Safari Industries had to raise equity by issuing shares at a discount to the ongoing market price.

- In March 2021, Safari Industries raised ₹75 cr by issuing CCDs at a price of ₹570 whereas the prevalent market price was in the range of about ₹650.

- On October 31, 2017, the company raised ₹50 cr at a price of ₹340 per share whereas the market price then was about ₹410.

- In FY2015, the company raised about ₹70 cr at a price of ₹600 per share (FV ₹10, pre-split) whereas the market price was in the range of ₹750-800 per share (FV ₹10, pre-split).

Therefore, an investor would note that the company was in urgent need of equity dilution and had to incentivize the investors by offering them shares at a discount to the ongoing price in the market.

It seems that in FY2014, the company’s need for funds to an urgent situation and it had to raise ₹14.75 cr via intercorporate deposits.

FY2014 annual report, page 26:

The company had to dilute its equity the next year, FY2015, to repay these intercorporate deposits.

FY2015 annual report, page 52:

Credit rating report by India Ratings, June 2015:

reduction in debt levels was achieved through the part use of equity funds (INR621.7m) received in FY15 from the issuance of shares to a private equity fund and the conversion of warrants issued to SIIL’s sponsor.

This shows that the business growth of the company had been highly dependent on the additional money infused by investors and is difficult to sustain from the cash generated by the company from its operations. Such a situation indicates that the business model of Safari Industries India Ltd does not have a great margin of safety.

Going ahead, an investor should keep a close watch on the free cash flow generation by Safari Industries (India) Ltd to understand whether the company continues to consume cash from outside sources or it starts to generate surplus cash from its business.

Further advised reading: Free Cash Flow: A Complete Guide to Understanding FCF

Self-Sustainable Growth Rate (SSGR) and free cash flow (FCF) are the main pillars of assessing the margin of safety in the business model of any company.

Further advised reading: 3 Simple Ways to Assess “Margin of Safety”: The Cornerstone of Stock Investing

Additional aspects of Safari Industries (India) Ltd:

On analysing Safari Industries (India) Ltd and after reading annual reports, credit rating reports and other public documents, an investor comes across certain other aspects of the company, which are important for any investor to know while making an investment decision.

1) Management Succession of Safari Industries (India) Ltd:

Safari Industries (India) Ltd is run by Mr Sudhir Jatia (age 53 years), Chairman & Managing Director of the company.

As per the disclosures by the company under related party transactions, currently, two daughters of Mr Jatia, Ms Shivani Jatia and Ms Tanisha Jatia draw remuneration from the company indicating that they work for the company.

As per related party transactions disclosure for H2-FY2022, from Oct. 2021 to March 2022, Ms Shivani Jatia took home a salary of ₹10.6 lac indicating an annual remuneration of about ₹21 lac. During the same period, Ms Tanisha Jatia took home a salary of ₹8.1 lac indicating an annual remuneration of about ₹16 lac.

An investor may contact the company directly to understand more about the role played by Ms Shivani and Ms Tanisha in the company. Thereafter, she may make an opinion about the succession planning of the company.

The presence of the next generation of Mr Sudhir Jatia in the company in an active role when he is still handling active responsibilities might indicate a good succession plan. It allows the next generation to learn the nuances of the business under the guidance of senior members who are still actively involved in the business.

An investor should look for signs of any ownership-related differences between the two daughters or sons-in-law either currently or in the future as it might have a significant impact on the affairs of the company.

Further advised reading: How to do Management Analysis of Companies?

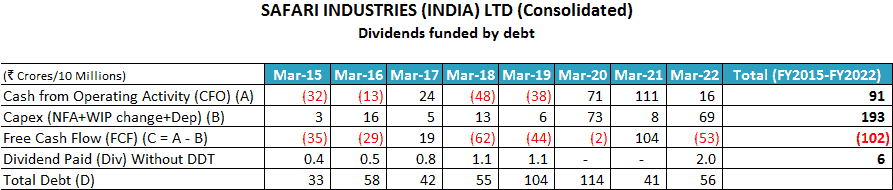

2) Dividends funded by debt:

In the last 10 years, Safari Industries has paid dividends from FY2015 to FY2022, totalling about ₹6 cr excluding dividend distribution tax (DDT). During this period, the company had a negative free cash flow of (₹102) cr (FY2015-FY2022). This is because, during FY2015-FY2022, it generated a total cash flow from operations (CFO) of ₹91 cr whereas it made a capital expenditure of ₹193 cr.

Therefore, it consumed its entire CFO during FY2015-FY2022 for making capital expenditures and still was short of funds (negative free cash flow). As a result, it had to raise funds from additional sources like equity dilution (₹195 cr: FY2015: ₹70 cr, FY2018: ₹50 cr and FY2021: ₹75 cr) and incremental debt of ₹23 cr (FY2015 debt: ₹33 cr and FY2022 debt: ₹56 cr).

If a company has a negative free cash flow and is using debt and equity dilution to meet its capital expenditure, then if it payout out dividends to its shareholders, then the dividends are funded by debt. This is because money is a fungible commodity.

We believe that companies should use their resources for capital expenditure and if any surplus is left then should repay debt. In the situation of deficit (i.e. negative free cash flow), the companies should raise only that much debt, which is needed to meet its business requirements and avoid raising extra debt in order to enable it to pay dividends. Such dividend outflows put an extra burden of interest payments on the company, which could have been avoided.

Further advised reading: Steps to Assess Management Quality before Buying Stocks

3) Warrants to the promoters of Safari Industries India Ltd:

In FY2015, Safari Industries allotted 330,000 warrants to the promoter of the company at ₹600/- per warrant, which could be converted into one equity share each within a period of 18 months.

As per the terms, the promoter paid 25% of the total consideration i.e. 25% of ₹19.8 cr = ₹4.95 cr on the allotment of warrants. The remaining 75% of the amount, ₹14.85 cr was to be paid any time within the next 18 months when the promoter decides to convert the warrants into equity shares. Irrespective of the market price on the date of the promoters choosing, the company would issue him shares at a fixed price of ₹600 per share whenever he decides to convert these warrants into shares.

On March 31, 2015, the promoter converted half of the total warrants i.e. 165,000 warrants into equity shares.

FY2015 annual report, page 12:

The Company has also issued 3,30,000 convertible share warrants to Mr. Sudhir Jatia, the Promoter of the Company. Each share warrant is convertible into one equity share of ₹10/- each at a premium of ₹590/- per share. As on 31st March 2015, out of the above share warrants, 1,65,000 share warrants have been converted into fully paid equity shares.

On March 31, 2015, the market price of shares at BSE was ₹ 801.50 (closing price).

The promoter converted the remaining 165,000 warrants into equity shares in FY2016 at ₹600 per share. During the entire FY2016, the share price of Safari Industries had been almost above ₹750 and at times, exceeded ₹1,000.

Therefore, an investor would notice that even though the promoters got the warrants at a price of ₹600, they could convert them into shares at times when the share price was higher than the conversion price. This is almost always true because the promoters usually convert warrants only when they make money on conversion otherwise they let the warrants expire.

Stock warrants are like call options where the holder has paid a premium of 25% of the value. She would convert the warrants into equity shares by paying the balance 75% only if at the time of conversion the price of the equity share of the company is such that the holder of the warrants makes money over her warrant allotment price.

We believe that the warrants are 25% beneficial to the company and 75% beneficial to the promoters. Before February 2009, this ratio was 10% beneficial to the company and 90% beneficial to the promoters because; then the promoter had to pay only 10% of the total money upfront.

The key reason that led SEBI to increase the upfront payment for warrants was that the promoters used warrants to enrich themselves when the stock markets rose while their loss was limited to only 10% if the markets fell. (Source)

There were complaints that promoters allotted warrants to themselves and select investors at a pre-determined price, but didn’t buy them when the due date came if the prevailing stock prices were lower than the decided price. If the prices were higher, they would convert those warrants and at least make a paper profit, and in some cases encash the gains.

It is to discourage promoters from trading profits. Warrants are seen as an instrument that gives an advantage to promoters above retail investors, who have all other rights equal to company founders.

When the markets melted during 2008 and early 2009, promoters of many companies such as Hindalco Industries, Tata Power, GE Shipping and Pantaloon Retail did not convert those warrants, regulatory filings show.

After similar complaints, in February 2009, the regulator had raised the up-front margin to be paid by warrant subscribers to 25% from 10% since the payment lost was insignificant compared with the losses one would have made if forced to buy.

Common logic says that no one holding stock warrants would exercise them to get shares at a price, which is higher than the price at which he/she can get shares from the market.

More so, if the promoters intend to infuse money into the company, then they should simply get all the shares at the current market price and give the entire money to the company upfront so that the company may use it for the purpose for which it needs money.

If the promoters pay 25% now and let the stock warrants expire due to the market price being consistently lower than the exercise price in future, then it effectively means that the promoters did not have the true intention of infusing 100% of the money or that the company did not need 100% of the money.

Moreover, warrants also allow a promoter to increase her shareholding in the company without facing the market impact i.e. the cost of increasing her stake at a higher price when the market gets to know that the promoter is increasing her stake in the company by buying them from the market.

In the case of warrants, the promoter is able to increase her stake in the company at the fixed price of warrant allotment.

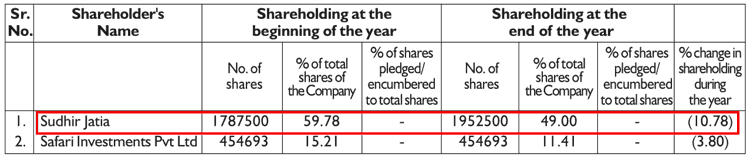

In the case of Safari Industries, in FY2014, the shareholding of Mr Jatia was 59.78%, which fell to 49.00% on March 31, 2015. The primary reason was the allotment of new shares to Tano India Pvt Equity Fund II which got about a 20% stake in the company for its investment. The shareholding of 49.00% of Mr Jatia in FY2015 was despite the conversion of 165,000 warrants on March 31, 2015, i.e. the entry of Tano India fund had brought the stake of Mr Jatia in Safari Industries below the majority mark.

FY2015 annual report, page 28:

Please note that the company “Safari Investments Pvt Ltd” is a part of the original founder-promoter family, Mehta and not a part of Mr Jatia’s family.

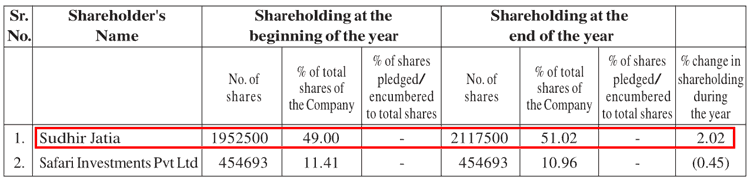

In FY2016, Mr Jatia exercised the remaining 165,000 shares and could increase his stake in the company above the majority mark.

Therefore, after the complete conversion of warrants, Mr Jatia could retain his majority shareholding in the company and for it; he could get additional shares at a fixed price of ₹600 and not face the market cost of buying shares from the open market.

It might be a situation where the number of warrants allotted to Mr Jatia was arrived at after doing all the calculations that only that many warrants should be allotted so that he could achieve his targeted 51% stake. That is why the stake after warrants conversion increased to 51.02%. In addition, no warrants were allotted to the original founder promoters Mehta family who own a stake in the company via Safari Investments Pvt Ltd, classified under promoters.

Therefore, we believe that investor should increase their due diligence whenever they come across a case of allotment of warrants to the promoters. For any further clarifications, an investor may contact the company directly.

Further Reading: Stock Warrants to Promoters: How to Analyse

4) Scope for improvement in internal controls and processes at Safari Industries India Ltd:

An investor notices many instances, which indicate that internal controls could have been improved.

In FY2021, the company did not comply with required guidelines while holding its board meeting. As a result, the Bombay Stock Exchange (BSE), as well as National Stock Exchange (NSE), imposed a fine on the company. Later on, BSE agreed to waive the fine. However, NSE has not waived the fine until now.

FY2022 annual report, page 33:

During the preceding Financial Year i.e. 2020-21, BSE limited and National Stock Exchange of India Limited had issued notice to the Company for non-compliance with Regulation 29 of the Listing Regulations with respect to its Board Meeting held on 12th February 2021 and subsequently both stock exchanges had levied fine of ` 10,000/- each exclusive of taxes. The Company had applied for waiver of fine before both the Stock Exchanges, however only BSE Limited has approved the waiver application.

Previously, in FY2011, the company had raised deposits from the public; however, it did not comply with the RBI requirement of maintaining sufficient liquid assets within stipulated time limits.

FY2011 annual report, page 11:

The Company has complied with the provisions …and directives issued by the Reserve Bank of India…with regard to the deposits accepted from the public, save and except maintaining liquid assets

In the past, there had been two instances of fire at the company’s premises, which led to losses. First, in FY2003, the company faced a fire in its depot.

FY2003 annual report, page 21:

Insurance Claim of Rs.17.85 Lacs represents settlement of claim in respect of loss of goods due to fire at the Company’s depot.

Thereafter, in FY2016, the company faced another fire in its manufacturing unit at Halol.

FY2016 annual report, page 16:

During the year, there was a fire at the Halol plant of the Company and Properties & Inventories lying there were damaged.

An investor should be cautious if such instances of fire are repeated because these can lead to a significant loss of life and business.

In FY2013, Safari Industries did not pay its undisputed due for service tax to govt. authorities within the stipulated time. The same was outstanding for more than 6 months from the due date for payment.

FY2013 annual report, page 11:

There are undisputed arrears of Service tax amounting to ₹46,831 outstanding as at March 31, 2013 for a period of more than six months from the date they became payable.

Delays in depositing undisputed service tax dues continued in FY2014 as well.

FY2014 annual report, page 17:

There are undisputed arrears of Service tax amounting to ₹1.75 lacs outstanding as at March 31, 2014 for a period of more than six months from the date they became payable.

In FY2015, when the company initially sent its annual report to shareholders on July 10, 2015, then it did not include companies auditor’s report order (CARO) in its annual report, which is an important part of the auditor’s observations of the company’s financial statements. Later on, the company had to revise its annual report on July 15, 2015, to include CARO and publish it in newspapers. (Source: FY2015 annual report, pages 1-2).

In FY2009, while reappointing the managing director of the company, it did not file the required information with the authorities.

FY2009 annual report, page 9:

The company has during the year under review re-appointed the Managing Director. Save and Except filing of form 23, 32 and filing of Agreement defining terms of re-appointment…has complied with the provisions of the Act in respect of the same

In FY2018, the company diluted its equity when it raised ₹50 cr from Malabar Funds by issuing new shares. As a result, the shareholding of all the existing shareholders declined even though they did not sell any shares. However, while disclosing the change in shareholding of promoters during the year, the company made an error and did not consider the impact of equity dilution on their holding at the end of FY2018.

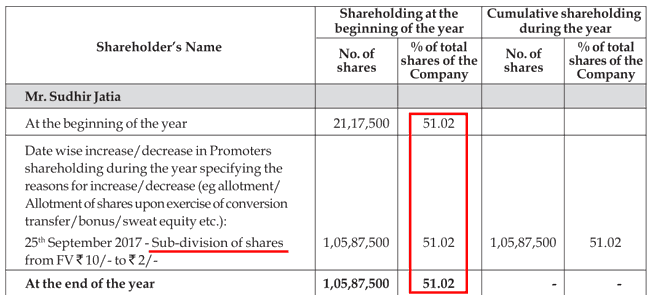

The following table from the FY2018 annual report, page 40 indicates that the shareholding of Mr Jatia did not go down during FY2018 and stayed constant at 51.02%. The only change is the increase in the number of shares due to the split of shares from face value (FV) of ₹10 to FV of ₹2.

However, at the same time, in a different table, Safari Industries has correctly mentioned the decline in the shareholding of Mr Jatia in FY2018 by 3.44% from 51.02% at the start of the year to 47.58% at the end of the year.

FY2018 annual report, page 40:

Such instances of errors indicate weakness in the processes like lack of oversight/maker-check mechanisms.

In FY2009, the company disclosed that it had many tax-related disputes with govt. authorities going back to the years FY2003 to FY2006. However, it had not disclosed these disputes in any of the previous annual reports until FY2008.

FY2008 annual report, page 11:

According to the information and explanations given to us, there were no disputed dues of sales tax, income- tax, customs duty, wealth-tax, service tax, excise duty and cess

An investor may contact the company directly to understand the reasons for nondisclosure of the tax disputes in the annual reports until FY2008. Was it because these disputes arose in FY2009 only? However, some of the disputes were already at the appeal stage indicating that they had been continuing for a while.

In FY2010, Safari Industries published an advertisement in the English language whereas it needed to publish it in the Marathi language.

FY2010 annual report, page 10:

The Company closed its Register of Members and Share Transfer of Register from 10.07.2009 to 25.07.2009…However, Advertisement in Navshakti edition dt. 15th June, 2009 in English Language instead of Marathi Language.

On one occasion, Safari Industries disclosed that the resignation of a professional was effective from a date different from the date mentioned in the letter of resignation.

FY2010 annual report, page 12:

The Company has accepted the resignation of Mr. Y. P. Trivedi vide Resignation letter dt. 31.01.2009 in the Board Meeting held on 25.04.2009 and mentioned that the said resignation is effective with close of business hours on 25.04.2009, however the resignation letter mentions the resignation is effective with close of business hours on 31.01.2009.

Therefore, it is advised that investors should pay enhanced attention while going through the disclosures of Safari Industries India Ltd.

Advised Reading: How to study the Annual Report of a Company

The Margin of Safety in the market price of Safari Industries (India) Ltd:

Currently (July 27, 2022), Safari Industries (India) Ltd is available at a price-to-earnings (PE) ratio of about 82 based on consolidated earnings of FY2022.

However, we recommend that an investor may read the following articles to assess the PE ratio to be paid for any stock, which takes into account the strength of the business model of the company as well. The strength in the business model of any company is measured by way of its self-sustainable growth rate and the free cash flow generating the ability of the company.

In the absence of any strength in the business model of the company, even a low PE ratio of the company’s stock may be a sign of a value trap where instead of being a bargain; the low valuation of the stock price may represent the poor business dynamics of the company.

- 3 Principles to Decide the Ideal P/E Ratio of a Stock for Value Investors

- How to Earn High Returns at Low Risk – Invest in Low P/E Stocks

- Hidden Risk of Investing in High P/E Stocks

Analysis Summary

Overall, Safari Industries (India) Ltd seems a company, which has grown its sales almost consistently at a rate of 25% year on year for the last 10 years. Sales declined only in FY2021 due to Covid-related restrictions. Over the last 10 years, profit margins have also seen significant improvements; however, the profit margins have seen fluctuations as well.

The business of the company started growing fast, in both sales and profits, after 2012 when Mr Sudhir Jatia, an industry veteran and ex-MD of the industry leader, VIP Industries Ltd, took over Safari Industries from the Mehta family. Sales of the company that were growing at a slow rate of about 5% year on year in the last 20 years (FY1993-FY2012) started growing at 25% year on year after Mr Jatia took over.

Using his experience, Mr Jatia expanded the sales channel of the company from primarily CSD to exclusive showrooms, hypermarkets, eCommerce sites etc. He added many other brands as well as new products like backpacks, laptop bags, and polycarbonate zippered hard luggage to meet changing customer preferences. As a result, Safari Industries increased its market share in the intensely competitive luggage bags industry.

However, despite significant sales growth, the company has low pricing power over its customers, as there is intense competition from the unorganized sector as well as an oligopolistic organized sector dominated by VIP, Samsonite and Safari. As a result, whenever the inputs costs increase whether due to commodity price increase or due to Rupee depreciation, then the company has to take a partial hit on its profit margins.

Nevertheless, recently when the company was hit due to problems of Rupee depreciation as well as supply chain problems from China, then it diversified its sourcing of soft luggage from China to India and Bangladesh. This resulted in cost savings as well as lower inventory requirements.

All these strategies have helped the company grow its business at a brisk pace; however, still, its business is highly dependent on the spending on travel by corporates and individuals as well as wedding season. In FY2021, the Covid restriction led to a decline in spending on all these aspects leading to a sharp decline in sales for the company and it reported losses.

Safari Industries’ business is highly capital intensive as it needs a large amount of inventory to make its product available to the customer across different sales outlets like exclusive showrooms, hypermarkets and CSD etc. In addition, as its business has grown, more and more money is stuck in receivables. In fact, the working capital of Safari Industries has consumed cash much more than what it generated by its operations in the last 10 years. This is even though its operations are not fixed-capital intensive as it completely outsources the production of soft luggage, which is more than half of its sales.

The company has faced significant negative free cash flow and has to raise additional money by equity dilution and debt to meet its funds’ shortfall. Equity dilution is a regular affair for the company and after every 2-3 years, it comes up with a preferential issue of shares, which dilutes the holding of existing shareholders. In FY2015, when the shareholding of its key promoter fell below the majority mark after issuing shares to the private equity investor, then the company issued warrants to the promoter to bring his shareholding above the majority mark.

However, despite the situation of a continuous cash shortfall, Safari Industries has declared dividends for many years, which seem to be funded by debt or the proceeds from equity dilution.

The current promoter of the company, Mr Sudhir Jatia is young at 52 years of age and has also introduced his two daughters as employees in the company. It seems a step toward management succession planning.

There have been many instances, which indicate scope for improvement in the internal controls and processes of Safari Industries.

Going ahead, an investor should keep a close watch on its profit margins, product mix, forex losses, sourcing for soft luggage, and utilization levels of the newly completed hard luggage-manufacturing unit as well as its inventory levels. The investor should also keep a check on the receivables level of the company and monitor any write-offs of receivables as well as any provisions towards bad/doubtful debt. The investor should monitor whether the company starts generating free cash flow or it goes for further equity dilution to fund its growth in the future and whether it goes for any further rounds of warrants issuance to promoters.

All these aspects should be monitored by an investor to keep a continuous check on the financial performance of Safari Industries.

Further advised reading: How to Monitor Stocks in your Portfolio

These are our views on Safari Industries (India) Ltd. However, investors should do their own analysis before making any investment-related decisions about the company.

You may use the following steps to analyse the company: “Selecting Top Stocks to Buy – A Step by Step Process of Finding Multibagger Stocks”

I hope it helps!

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

I, Vijay Malik, am a SEBI-registered Research Analyst (Regn. No. INH100008364). This article is for educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.

{kind=link}

4 thoughts on “Analysis: Safari Industries (India) Ltd”

Dear Sir,

Reading this again after a gap of two years, it is noteworthy that the company raised funds via “Proceeds from the preferential issue of equity shares” amounting to Rs. 229 crores in FY24. The 10-year cumulative Capex is still higher than the cash generated from operations, resulting in no FCF generation. Additionally, the company resorted to taking on more debt apart from equity dilution. This reiterates that there is no margin of safety in the business model.

Thanks & Regards,

Omkar Ranjan

Thanks for sharing your input, Omkar.

Dear Sir,

Insightful reading as always. Thanks for your hard and diligent work. Just one typographical error in the following sentence “The sales of the company have increased every year since FY2013 except FY2021 when the sales declined to ₹328 cr from ₹686 cr in FY2012. However, in the next year, FY2022, the sales of the company increased sharply to ₹706 cr.”

FY2012 should be FY2020.

Regards,

Omkar Ranjan

Dear Omkar,

Thanks for your feedback and for pointing out the error. We have rectified the same in the article.

Regards,

Dr Vijay Malik