Inventory turnover ratio is a measure of the efficiency of inventory management by a company. It tells us whether the company is using its inventory in the best possible manner or not.

Inventory management is one of the most essential functions of the company. It covers all the stages right from the purchase of raw material to its conversion into finished goods and then transporting the finished goods to the customers. Any lapse by the company at any stage can lead to a significant financial impact on the company.

An investor may understand the importance of inventory management and its financial impact on the company by the following example of a car manufacturer.

Suppose a car manufacturer having its factory in Delhi sells cars in Chennai. Assume that the customers in Chennai buy 100 cars every day. Therefore, the car manufacturer sends 100 cars every day from Delhi to Chennai by loading them in trucks. Assume that the trucks take 4 days to reach from Delhi to Chennai. Therefore, at any point of time 400 cars (=100 cars * 4 days travel time) will be on the road in transit from Delhi to Chennai. Every day one truck will reach Chennai with 100 cars and a new truck will start from Delhi with 100 cars for Chennai. The cost of these 400 cars, which are always in the transit is the money permanently stuck in inventory for the car manufacturer.

Now imagine if the car manufacturer sells in all the major 100 cities in India and delivers cars from its plant in Delhi, then how many cars will be permanently in transit. How much money of the car manufacturer will be stuck in this finished goods inventory permanently in transit? For a large company, it may be hundreds to thousands of crores of rupees.

Calculate the cost of financing this money and if by better strategic management, the car manufacturer can reduce this cost, then how much money can be freed up for other uses or to return to shareholders. How much value it will create for the shareholders?

Therefore, an investor would appreciate that inventory management is one of the crucial aspects of business management in any company. As a result, companies like the car manufacturer mentioned above, keep implementing strategies like manufacturing plants spread across the country near their customers, cheaper and faster modes of transporting cars to customers etc.

The companies aim to have the least possible amount of inventory stuck in different phases of manufacturing like from raw material to finished good and then transport of finished goods to the customer. Car manufacturers attempt to reduce the money stuck in raw material by asking their suppliers to send them material just-in-time i.e. just before it is needed in the manufacturing of cars. They might further reduce the inventory expenses by asking their customers i.e. dealers to take delivery of the cars at the factory gates and then transport the cars at their own cost to their respective cities.

Such strategies will change from one industry to another. However, an investor would appreciate that it might not be easy for any company to reduce the requirement of inventory below a certain limit. If for a company, the conversion of raw material into finished goods takes two months, then at any point of time a stock of two months’ worth of sales would be present with the company at different stages of processing. A company would not be able to reduce this level of inventory further unless it develops a new technology, which reduces the processing time of raw material into finished goods from 2 months to say 1 month. If it can develop such technology, then the inventory requirement of the company will automatically reduce by half as it would need to keep only 1 months’ worth of sales as inventory with it.

Looking at the importance of the efficiency of inventory management and its impact on the financial health of a company, an investor would appreciate that it becomes important that she assess inventory turnover ratio of every company that she analyses.

Formula to calculate Inventory Turnover Ratio:

We calculate the inventory turnover ratio (ITR) as:

Sales / average of inventory at the start of the year and the end of the year

If a company has sales of ₹100 and it has an average inventory of ₹20, then its inventory turnover ratio would be 5 (=100/20). It means that the company can rotate/churn its inventory 5 times during the year. It can also be interpreted by converting it into “days of inventory”.

Days of inventory = (365 / inventory turnover ratio)

In the above example, the company has days of inventory as 73 (= 365/5), which means that at any point of time, the company has to keep a stock of about 73 days of sales with itself as inventory. In other words, the money of about 2.5 months’ worth of sales is tied up in inventory for the company.

Higher the inventory turnover i.e. lower the days of inventory means that the company needs a lower amount of inventory to run its business smoothly.

Lower the inventory turnover i.e. higher the days of inventory means that the company needs a higher amount of inventory to run its business smoothly.

Please note that sometimes, investors use the cost of raw material instead of sales in the formula to calculate ITR. We believe that an investor may use either of them; however, she should make sure that while analysing any company and comparing it with other companies, she keeps in mind that she uses one formula consistently for all the companies. Using sales to calculate ITR of one company and then comparing it with ITR of another company whose ITR is calculated by using the cost of raw material may not lead to a correct decision.

An investor can use the inventory turnover ratio to assess a company from different aspects:

- She may look at the absolute value of inventory turnover ratio of the company and judge whether its business model would require a large amount of money for growth. A company with a higher inventory turnover ratio would need lesser investment in its inventory when it grows whereas a company with lower inventory turnover ratio would need higher investment.

- She can analyse the trend of inventory turnover ratio of a company over the years to see if it has become better or poor at inventory management.

- She can compare inventory turnover ratio of a company with other companies within the same industry to see whether the company is better than its peers. Lower inventory turnover ratio of a company than its peers may indicate inefficient management or inferior production technology.

Over the years, we have analysed hundreds of companies and have come across companies with different levels of inventory turnover ratios. Many companies had a very low inventory turnover ratio whereas other companies had very high inventory turnover ratio. Many companies improved their inventory turnover ratio over the years whereas other companies saw deterioration in their inventory turnover ratio over the years. Within the same industry, we could see that some companies had a higher inventory turnover ratio indicating better inventory management where other companies had a lower inventory turnover ratio indicating scope for improvement in their inventory management.

Advised reading: What I learnt from analysis of 2,800 Companies

The current article is our attempt to share with all the readers our learning about inventory turnover ratio after analysing hundreds of companies. The article contains examples of real-life companies to understand different usages of inventory turnover ratio to analyse any company.

How to use Inventory Turnover Ratio in stock analysis

Let us discuss how an investor can use the inventory turnover ratio to understand the business of any company and then make her opinion.

A) Absolute level of Inventory Turnover Ratio:

As discussed earlier in this article, an investor can ascertain whether a company’s business is capital-consuming by looking at the inventory turnover ratio of the company.

A company with a low inventory turnover ratio would need a higher investment in inventory when it grows its business whereas another company with a higher inventory turnover ratio would need a lower amount of investment.

Before an investor can make an opinion whether the inventory turnover ratio of a company is low or high, she needs to ascertain what the normal level of inventory turnover ratio is. As mentioned earlier, one of the key determinants of inventory turnover ratio is the time taken by the company to convert its raw material into finished goods.

If a company takes about 1 month to convert its raw material into finished goods, then it may have an inventory turnover ratio of 12. On the contrary, if a company takes 3-months to convert its raw material into finished goods, then it would have an inventory turnover ratio of 4.

The amount of time that any company would take to convert its raw material into finished good cannot be generalised across the companies. It will differ from one product to another; therefore, inventory turnover ratios will differ a lot from one industry to another.

However, still, to work with some form of rough benchmark, and based on our observations from analysing multiple companies, we find that on an average, manufacturing companies tend to have an inventory turnover ratio of 6 to 8. This corresponds to raw material to finished goods conversion time of about 1.5 to 2-months.

An investor would find that companies present on a wide range of inventory turnover ratio. Therefore, the benchmark of average inventory turnover ratio of 6 to 8 should not be considered very strict criteria for the assessment of companies. Nevertheless, if an investor comes across companies with inventory turnover ratio much lower or higher than 6 to 8, then she may believe that such companies have a low or a high inventory turnover ratio.

Let us now see examples of companies with low inventory turnover ratio as well as the companies with a high inventory turnover ratio and understand this aspect further.

1) Companies with a low inventory turnover ratio:

A low inventory turnover ratio means that the company is able to rotate/churn its inventory slowly. It indicates that the company either takes a lot of time to make finished goods from its raw material or it takes a lot of time in transportation from the factory to the customer. Long transport time forces the company to bear the cost of the inventory even after it has produced the finished good.

While analysing companies with a low inventory turnover, an investor would come across instances of both the above situations.

a) KRBL Ltd:

KRBL Ltd is the world’s largest basmati rice producer-and-exporter company owning the well-known brand of basmati rice “India Gate”.

While analysing KRBL Ltd, an investor notices that the company has an inventory turnover ratio in the range of 1.3 to 1.8. An investor would appreciate that this is very low inventory turnover and it indicates that KRBL Ltd takes a lot of time to convert its raw material (rice) into finished good (packaged rice ready for sale).

While reading about the business of KRBL Ltd, an investor realizes that the company has to buy the requirement of rice for the entire year within a short paddy season of October to December every year. Also, KRBL Ltd needs to store the rice for 12-18 months for aging it to command better realizations.

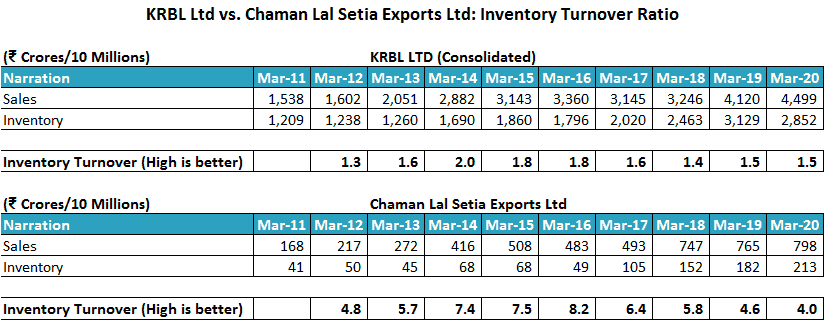

An investor would notice that due to the low inventory turnover ratio, as the business of KRBL Ltd grew, it had to invest a lot of money in its inventory. From FY2011 to FY2020, the inventory of the company increased from ₹1,209 cr to ₹2,852 cr indicating that the company had to invest an additional ₹1,643 cr in its inventory in the last 10 years.

Such a large amount of investment in the inventory resulted in a large portion of KRBL Ltd getting stuck in its inventory (working capital). As a result, the company could not convert its profits into cash flow from operations.

When we analyse the cumulative profits and cash flow data for last 10 years (FY2011-2020), then we realize that during these years, KRBL Ltd had a profit after tax (PAT) of ₹3,088 cr. whereas the CFO over the same was ₹1,937 cr indicating that a significant amount of money has been stuck in the working capital of the company.

The credit rating agency, ICRA, has also highlighted such working capital intensive nature of the business of KRBL in its rating rationale for KRBL Ltd:

The raw material intensity of the business is high on account of procurement of the entire year’s paddy requirement during the period from October to December coupled with the ageing requirement of basmati rice for a period of 12-18 months (to improve the realisation). This leads to high working capital borrowings, at the same time exposing the company to volatility in paddy prices, which are determined by demand and supply forces.

From the above discussion, an investor would appreciate that KRBL Ltd has a low inventory turnover ratio due to the long processing time taken to convert raw rice into packaged ready-for-sale rice.

An investor may read our detailed analysis of KRBL Ltd in the following article: Analysis: KRBL Ltd

Let us now look at another company where the transportation of the finished good from the factory to the customer takes a lot of time and as a result, leads to lower inventory turnover ratio for the company.

b) HEG Ltd:

HEG Ltd is one of the leading graphite electrode manufacturers in India.

While analysing HEG Ltd, an investor notices that the inventory turnover ratio of the company has been at low levels of 2 to 2.5 over the years.

While analysing the business model of HEG Ltd, an investor gets to know that the company keeps finished graphite electrodes in its warehouses around the world so that it can supply them to the customers “just-in-time”. It means that HEG Ltd bears the cost of transporting graphite electrodes from its factory in India to its warehouses around the world where it stores them until it receives orders from the customers and it immediately delivers the electrodes to the customer without any delay.

As per the website of HEG Ltd:

Warehousing: HEG has warehouses throughout world. We are able to hold inventory and deliver just in time.

An investor would appreciate the decision of the company to hold inventory in its warehouses near customer locations increases the needs for investment in inventory as it has to hold the finished electrodes for a longer time, transport them to foreign warehouses and store them there at its own cost. This, in turn, decreases the inventory turnover of the company.

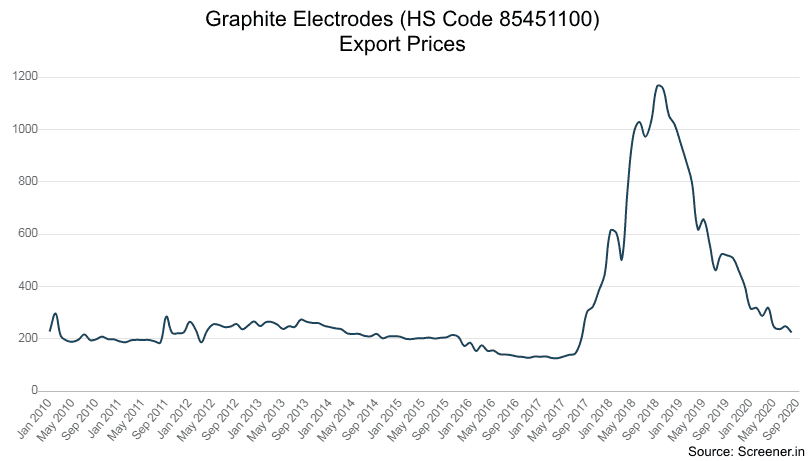

During FY2018 and FY2019, the inventory turnover ratio of HEG Ltd increased to 7. However, this improvement was not a result of any technological advance, which might have decreased the manufacturing time drastically. This improvement in the inventory turnover ratio was a result of a sharp increase in the sales price of graphite electrodes, which resulted in a significant increase in the numerator in the inventory turnover ratio formula used by us (Sales/average inventory for the year).

Advised reading: How to do Business Analysis of a Company

The below chart taken from Screener showing the trend of export prices (in ₹ per Kg) of graphite electrodes from India from Jan-2010 to Sept-2020 shows how sharply the prices increased during FY2018-FY2019 and then declined to historical levels in FY2020.

As the graphite electrodes prices declined to their normal levels in FY2020 onwards, the inventory turnover ratio of HEG Ltd also declined from 7 in FY2018-FY2019 to 1.9 in FY2020.

Therefore, an investor would appreciate that in the case of HEG Ltd, the decision of the company to transport the graphite electrodes to warehouses near the customers in foreign countries and store them there waiting for customers’ order has led to a lower inventory turnover ratio.

An investor can read our detailed analysis of HEG Ltd, which is a good case study of a company operating in a cyclical industry, in the following article: Analysis: HEG Ltd

2) Companies with a high inventory turnover ratio:

An investor would note that a manufacturing company has to procure its raw material, process it into finished goods, transport them near the customers’ location and then store them until they are sold and delivered to the customer. All these phases take time and holding inventory during these phases requires investment.

If a company has to reduce its investments in the inventory and increase its efficiency, then it has to reduce the time each of these phases takes. Many companies reduce the time and thereby investment by outsourcing some of these phases.

For example, if a company outsources the manufacturing of goods and only focuses on selling goods, then it can avoid blocking time and money in the purchase of raw material and its processing into finished goods. The company can directly purchase finished goods from its suppliers and sell it within a short time to its customers.

Such kind of outsourcing of manufacturing process helps the company to reduce its investment in inventory as the company can order goods from its suppliers a short-time before it intends to sell them. Therefore, the time for which it has to hold inventory with itself can be reduced. Such business decisions of outsourcing reduce investment in inventory, increase inventory turnover ratio and improve the business efficiency of the company.

Let us see an example of a company that has used outsourcing to increase its inventory turnover ratio.

a) Sreeleathers Ltd:

Sreeleathers Ltd is one of the leading footwear companies in India based out of Kolkata. It deals in the formal and casual footwear of men, women and kids as well as in leather accessories.

While analysing Sreeleathers Ltd, an investor notices that the company has an inventory turnover ratio over 11 throughout the last 10 years (FY2011-2020).

When an investor studies the business model of Sreeleathers Ltd to understand the reasons for a high inventory turnover ratio, then she notices that the company outsources the manufacturing of shoes.

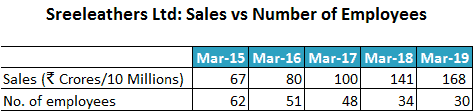

An investor notices that from FY2011 to FY2020, the company has increased its sales from ₹40 cr to ₹173 cr. However, the company has done a capital expenditure (capex) of only ₹1 cr during these 10 years (FY2011-2020). It indicates that instead of creating shoe manufacturing capacities in-house, the company is relying on outsourcing/other suppliers to produce shoes for it, which it then sells in its showrooms spread across India.

While reading the annual reports of the company, an investor gets more information, which indicates that the company is relying on outsourcing to manufacture shoes.

FY2012 annual report, page 5:

Your company continues to procure a part of its total footwear sold in the market from small scale and cottage industries, so that these industries continue to upgrade their machines and manpower.

Advised reading: How to read the Annual Report of a Company

FY2013 annual report, page 6:

Your company continues to procure a part of its total footwear sold in the market from small scale and cottage industries, so that these industries continue to upgrade their machines and manpower. This is a social obligation which your Company fulfills to support the employment given by these small scale and cottage industries.

Moreover, when an investor analyses the increase in the number of employees of the company, then she notices that over FY2015 to FY2019, the sales of the company increased from ₹67 cr to ₹168 cr. However, during the same period, the number of employees in the company declined from 62 to 30.

From the above discussion, an investor would appreciate that Sreeleathers Ltd has increased its sales significantly without any capital expenditure and with a reduction in the number of employees by outsourcing its shoe-manufacturing operations. As a result, the company could save on investments in its inventory to finished goods conversion stages and in turn operate efficiently. This is reflected in the high inventory turnover ratio of the company.

An investor may read our detailed analysis of Sreeleathers Ltd in the following article: Analysis: Sreeleathers Ltd

Until now, we have discussed how an investor can look at the absolute level of inventory turnover ratio (ITR) of a company and analyse its business model for requirements of investments in the inventory/working capital of the company.

A low ITR indicates that a company would need a large amount of investment in inventory when its business grows. Whereas a high ITR indicates that the requirements of investments in inventory would be lower. A company can take steps like outsourcing and better usage of the supply chain to improve its inventory management efficiency and achieve a higher inventory turnover ratio.

Let us now look at another aspect of inventory turnover ratio (ITR) where an investor can analyse the trend of ITR of the company over the years to understand whether the company is getting better or worse in its inventory management.

B) Analysing trend of Inventory Turnover Ratio:

When an investor analyses the past financial performance of a company, then looking at the trend of its inventory turnover ratio over the years can give her important business insights about the operations of the company. She can get to know whether the strategic working-capital decisions of the management are working in its favour or not.

If the inventory turnover ratio is increasing over the years, then it means that the company is becoming better at the utilization of its inventory and may generate more value on investments by shareholders. Whereas if the inventory turnover ratio is decreasing, then it may indicate that the company’s inventory management processes are becoming inefficient, which may reduce the returns generated by the company for its shareholders.

Let us see different examples of real-life companies with increasing as well as decreasing inventory turnover ratio.

1) Increasing inventory turnover ratio:

When an investor comes across any company whose inventory turnover ratio is increasing over the years, then she should analyse the company in-depth to understand the strategic business decisions of the company that have led to the improved efficiency in the inventory management. In many such instances, the investor would notice that:

- The company might have changed its sourcing strategy of its raw material leading to saving in the inventory costs.

- The company might have updated its technology leading to the usage of lower-cost raw material to produce finished goods or

- The company might have negotiated contracts with the customers where the company could avoid the uncertainty of orders and thereby work with lower inventory as the production plans are now certain.

These are some of the steps that lead to an improvement in the efficiency of inventory utilization by any company. While analysing companies, an investor may come across many other decisions, which have worked for companies. She should take note of all those steps as their knowledge would help her in stock analysis.

Let us now see examples of some of the companies that could improve their inventory turnover ratio over the years.

a) Filatex India Ltd:

Filatex India Ltd is an Indian manufacturer of polyester, nylon & polypropylene multifilament yarn.

While analysing Filatex India Ltd, an investor notices that the inventory turnover ratio of the company has improved from 9.5 in FY2012 to 16.2 in FY2020. This improvement reflects efficient inventory management by the company.

An investor gets to understand some of the steps taken by the company for efficient inventory management in the FY2019 annual report, page 25-26:

The two basic raw materials viz. PTA & MEG are purchased from both domestic and foreign suppliers. This year the company decreased its imports and purchased a majority from domestic players. This allowed the company to maintain less stock as lead time decreased. Therefore, holding levels were lower as compared to previous year and Inventory Turnover ratio improved from 32 days to 23 days.

An investor notices that in FY2019, Filatex India Ltd focused on purchasing its raw material from domestic suppliers instead of importing it from overseas. As a result, it had to keep less inventory with itself as it could buy additional raw material from domestic suppliers at a short notice (lower lead time). This has improved the inventory utilization efficiency and hence improved the inventory turnover ratio.

Please note that in its annual report, the company has mentioned the inventory turnover ratio in the number of days, which represents “days of inventory” parameter discussed at the start of this article. When an investor measures the efficiency of inventory management in “days of inventory”, then a decrease in the days of inventory indicates better management. On the contrary, if an investor measures the efficiency of inventory management in “inventory turnover ratio”, then an increase in the inventory turnover ratio indicates better management.

Irrespective of the parameter for the efficiency of inventory management, an investor may appreciate that Filatex India Ltd has improved its inventory management by shifting its raw material purchases from international suppliers to domestic suppliers.

An investor may read our detailed analysis of Filatex India Ltd in the following article: Analysis: Filatex India Ltd

b) Associated Alcohols and Breweries Ltd:

Associated Alcohols and Breweries Ltd is an Indian distillery based in Madhya Pradesh dealing in country liquor, extra neutral alcohol, rectified spirit and Indian made foreign liquor (IMFL).

While analysing Associated Alcohols and Breweries Ltd, an investor notices that over the years, the inventory turnover ratio (ITR) of the Associated Alcohols and Breweries Ltd has increased from 7.5 in FY2012 to 9.2 in FY2020. An increasing ITR indicates that Associated Alcohols and Breweries Ltd has been able to manage its inventory efficiently over the years.

On analysing the business model of Associated Alcohols and Breweries Ltd, an investor notices that the company has invested in a multi-grain processing facility, which can process different grains as raw material. This multi-grain processing facility provides the benefit of shifting from one food grain to another to produce alcohol whenever the prices of one of the food grains increase.

FY2017 annual report, page 27:

Multi-feed security: The AABL management selected to invest in equipment that would accommodate multi-grain feedstock as opposed to relying on molasses. This decision widened the company’s flexibility in being able to draw on diverse grain sources and moderate the impact of unforeseen cost increases by shifting from one grain source to another, particularly relevant in a business marked by a high raw material cost

As a result, the company can control its raw material costs by using cheaper food grains to produce alcohol. Such initiatives of the company contribute to efficient inventory management by the company and as a result, the inventory turnover has improved over the years.

An investor may read our detailed analysis of Associated Alcohols and Breweries Ltd in the following article: Analysis: Associated Alcohols and Breweries Ltd

c) Nile Ltd:

Nile Ltd is an Indian manufacturer of Lead and its alloys, supplying primarily to battery manufacturer Amara Raja Batteries Ltd.

While analysing Nile Ltd, an investor notices that Nile Ltd has improved its inventory turnover ratio over the years from the levels of 6 in FY2012 to 8 in FY2020.

To analyse the reasons for the improvement in inventory management, an investor would need to refer to the credit rating rationale of April 2014 for Nile Ltd prepared by India Ratings and Research, which highlights some of the features of the contract that it has signed with Amara Raja Batteries Ltd:

- Page 1): Amara Raja Batteries Ltd contributes 80% to the overall sales of Nile Ltd:

Strong Counterparty: The ratings are constrained by significant customer concentration. Amara Raja Batteries Limited continues to be the major contributor (FY16: 80%, FY15: 81.8%) to Nile’s revenue. However, Amara Raja Batteries’ leading industry positioning mitigates such concerns.

Advised reading: Credit Rating Reports: A Complete Guide for Stock Investors

- Page 3): The contract with Amara Raja Batteries Ltd has a minimum offtake clause i.e. Amara Raja will buy at least a minimum agreed quantity and therefore, Nile Ltd can plan its inventory purchases accordingly:

Nile has a yearly supply contract with Amara Raja Batteries Limited. The terms of the contract include minimum offtake by the client. The offtake price is based on average previous month London Metal Exchange (LME) price plus a pre-determined premium. Contractual revenue allows Nile to tie up its raw material requirements and procurement price, ensuring profit booking while protecting against loss from a sharp rise in raw material prices.

The above two observations when seen together would lead to the conclusion that there is high visibility of the amount of product demand for Nile Ltd and therefore, it can easily assess its inventory requirements and plan its inventory purchases well.

This business characteristic of the ability to do advance inventory planning helps in improving the management of inventory by any company, which increases the inventory turnover ratio of the company.

An investor may read our detailed analysis of Nile Ltd in the following article: Analysis: Nile Ltd

Until now, we have discussed the cases that have increased their inventory turnover ratio over the years. Let us now discusses cases where the inventory turnover ratio decreased over the years.

2) Decreasing inventory turnover ratio:

When an investor notices that a company’s inventory turnover ratio is declining over the years, then she may find that either the technology used by the company to produce the goods is getting old and inefficient or the company is facing weakness in its competitive position i.e. bargaining power on its customers. The weakening competitive position may force the company to hold more inventory due to the following reasons:

- The inventory is not selling and therefore, it is getting accumulated in the warehouses/dealer network.

- The customer is asking more choices/options; therefore, the company has to produce more kind of goods and many of them remain unsold.

- The customer is asking “just-in-time” delivery; therefore, the company has to store the goods in its warehouses near the customer’s locations while it waits for the order.

Similarly, there can be many reasons for a decline in the inventory turnover ratio, which needs to be analysed by the investor by doing an in-depth analysis.

Let us see examples of such companies:

a) Supreme Industries Ltd:

Supreme Industries Ltd is a plastic goods manufacturer in India. The company manufactures plastic pipes, plastic furniture, cross-laminated films, protective packaging, composite LPG cylinders etc.

While analysing Supreme Industries Ltd, an investor notices that over the years, the inventory turnover of the company has declined from 8.9 in FY2012 to 6.7 in FY2020.

A decline in the inventory turnover ratio highlights that the operations of the company have become more working capital intensive. It indicates that the company’s efficiency in managing its inventory is declining.

Moreover, in the case of Supreme Industries Ltd, an investor finds that in the initial years of the previous decade, Supreme Industries Ltd had classified a significant portion of the commercial real estate building (Supreme Chambers), which was unsold, in the inventory. Gradually, over the years, as the area in the Supreme Chambers was sold, it was removed from the inventory. In FY2020, the entire area in the Supreme Chambers was sold and it was completely removed from the inventory.

The impact of the addition of the unsold real estate area in the inventory tends to bring down the inventory turnover ratio (ITR). An investor notices that in the initial part of the decade, the inventory had a large part of real estate (₹109 cr in FY2011 and ₹98 cr in FY2012), whereas in FY2020 when the real estate inventory was nil.

Also read: How to do Business Analysis of Real Estate Companies

Therefore, an investor may observe that if she excludes the real estate inventory, then the decline in the ITR representing only the core plastic business, would be even higher.

The credit rating agency, CRISIL has highlighted in its report in February 2017 that Supreme Industries Ltd has to maintain a large amount of inventory of its products.

Furthermore, Supreme also has to maintain large raw material inventory (raw materials constitute around 63% of operating income as of December 2016); hence, volatility in input prices also impacts working capital intensity.

Moreover, when an investor analyses the business performance of Supreme Industries ltd over the last 10 years, then she notices that some of the business initiatives taken by the company as the development of composite cylinders, cross-plastic films as well as manholes did not give results within the desired period. As a result, the company had to produce these goods, whereas it did not find ready buyers because the customers took their own sweet time to try and test the products. In cases like composite cylinders, the products of the company did not meet the customers’ expectations and the company had to pay damages to the customers in Bangladesh.

Such instances of delays in product development also add to the inefficiency in the inventory management as the company has to produce the goods; however, it does not get continuous orders from customers and in turn, the money gets stuck in the inventory in the plants.

Also, the intense competition faced by Supreme Industries Ltd from competitors in the organized as well as the unorganized sector has added to the pressures on the business of the company. The company has to frequently introduce new products, ship them to the warehouses, dealers and retailers and has to phase-out non-selling products, which leads to inventory losses.

All the above factors lead to a decline in the inventory turnover ratio for any company.

An investor may read our detailed analysis of Supreme Industries Ltd in the following article: Analysis: Supreme Industries Ltd

Until now in this article, we have discussed how an investor can use the inventory turnover ratio to analyse companies by either looking at its absolute value or its trend over the years.

Now, let us discuss another aspect of inventory turnover ratio (ITR) analysis where an investor can compare the ITR of one company with other companies from its industry to assess how efficient the company is in its inventory management when compared to its peers.

C) Comparing inventory turnover ratio with peers/competitors:

An investor would appreciate that companies in the same industry mostly face similar challenges in their production processes. Like all the rice-sellers would require to buy raw-rice and then process it to convert it into finished-packages ready-to-sell rice. Similarly, all of the steel manufacturers would require to buy raw material like iron ore, coal etc. and then convert these into steel.

However, after analysing a few companies from any industry, an investor would notice that all the companies approach these seemingly similar tasks differently. They solve similar challenges differently and take different strategic decisions to manage their production processes efficiently.

These differences between companies within the same industry allow investors to prefer one company over another from the industry.

In the case of efficiency in inventory management as well, when an investor would compare many companies from the same industry, then she will notice that different companies show different levels of inventory management. Some show a higher inventory turnover ratio whereas others show a lower inventory turnover ratio.

Therefore, it becomes essential for an investor to compare any company with its peers to understand where it stands in the terms of efficiency of its business operations before she makes any final investing decision about the company.

Advised reading: Operating Performance Analysis: A Simple & Complete Guide

Let us take a couple of examples where we compare the companies discussed above in this article with their industry-peers to understand where they stand in the terms of efficiency in inventory management.

1) Sreeleathers Ltd vs. Mirza International Ltd:

In the article above, we discussed the example of Sreeleathers Ltd, which is a footwear manufacturer and has a high inventory turnover ratio exceeding 11 for the last 10 years. We noticed that the reason for a high inventory turnover for Sreeleathers Ltd was the outsourcing of shoe-manufacturing done by it to small & medium enterprises.

Other pieces of information indicating outsourcing of manufacturing activities by Sreeleathers Ltd are minimal capital expenditure done by the company in the last 10 years and a reduction in the number of employees over FY2015-FY2019 despite a significant increase in the revenues during the same period.

To understand how the business decisions of Sreeleathers Ltd stand in comparison to its peers, an investor may compare its inventory turnover ratio with another footwear manufacturer, Mirza International Ltd that owns the Redtape brand of shoes.

While analysing Mirza International Ltd, an investor notices that it had an inventory turnover ratio in the range of 3 to 4.5 over the last 10 years, which his much lower than the inventory turnover ratio of exceeding 11 for Sreeleathers Ltd.

On further analysis, an investor notices that Mirza International Ltd has done a capital expenditure of ₹659 cr in the last 10 years (FY2011-FY2020) in its business instead of relying on outsourcing without doing capital expenditure as done by Sreeleathers Ltd. The fallout of such an approach is that Mirza International Ltd has a debt of ₹288 cr in FY2020, which has increased from ₹131 cr in FY2011. On the other hand, Sreeleathers Ltd has been almost debt-free throughout the last 10 years (FY2011-2020).

Therefore, an investor would notice that within the same industry, different companies may follow completely different approaches towards the management of the production process. Some companies may choose to manufacture the products in-house and as a result, face challenges of inventory management like procurement of raw material and then its conversion into finished goods. Whereas other companies may choose to outsource the production of goods and directly buy finished goods from suppliers and focus more on selling the goods to customers.

Such different business approaches have different implications on the business outcomes and expose the companies as well as their shareholders to different kinds of risk. Therefore, it is advisable that whenever an investor analyses a company, then she should compare it with its industry peers on all the parameters including the inventory turnover ratio. From the above example of Sreeleathers Ltd and Mirza International Ltd, an investor would appreciate that two companies involved in a seemingly similar business of selling shoes may have entirely different business models and the inventory turnover ratio may become one of the tools for the investor to identify it.

An investor may read our detailed analysis of Mirza International Ltd in the following article: Analysis: Mirza International Ltd

Let us now see a comparison of inventory turnover ratio of another company discussed earlier, KRBL Ltd with its industry peer Chaman Lal Setia Exports Ltd.

2) KRBL Ltd vs. Chaman Lal Setia Exports Ltd:

We discussed the case of KRBL Ltd, the largest basmati rice producer of India and the owner of brand “India Gate” of basmati rice. We noticed that the inventory turnover ratio of KRBL Ltd was low in the range of 1.3 to 1.8. The major reasons for the low inventory turnover of the company were two; first, it had to buy rice for the whole year within a short paddy season from October to December and second, it had to store and age the rice for 12-18 months so that it can get a good price for the rice.

Let us compare the inventory turnover of KRBL Ltd with another rice-producer, Chaman Lal Setia Exports Ltd, which owns the brand “Maharani” of basmati rice.

An investor may expect that Chaman Lal Setia Exports Ltd will also face the same challenges like procuring the rice for the whole year during the paddy season of October to December and then storing the rice to age it so that it can sell at a higher price. Therefore, an investor would expect that the inventory turnover ratio of Chaman Lal Setia Exports Ltd would be similar to KRBL Ltd.

However, when an investor compares the inventory turnover ratio of KRBL Ltd with Chaman Lal Setia Exports Ltd, then she notices the Chaman Lal Setia Exports Ltd has an inventory turnover ratio ranging from 4 to 8.

An investor would appreciate that the inventory turnover ratio of Chaman Lal Setia Exports Ltd, which is more than double of KRBL Ltd indicates that the company is doing something different than KRBL Ltd. Therefore, before making any final opinion about KRBL Ltd, an investor should analyse the business strategies of both KRBL Ltd as well as Chaman Lal Setia Exports Ltd to understand what are the factors leading to this significant difference in seemingly similar businesses.

An investor may read our detailed analysis of Chaman Lal Setia Exports Ltd in the following article: Analysis: Chaman Lal Setia Exports Ltd

Summary

Inventory management is one of the most essential functions of the company. Efficient inventory management can ensure that the raw material is available to the manufacturing unit as and when needed without impacting the continuity of operations due to lack of it and without impacting the financial health of the company by having an excess of it. The inventory management ensures that the finished goods are sold at the earliest to the customers without spending a lot of money on their transportation or storage.

Inventory management is important because buying excess raw material that may become obsolete and unusable whereas long-stored finished goods may become obsolete and non-saleable. All these may lead to inventory write-off, which can cause a significant impact on the financial health of the company.

An investor may use the inventory turnover ratio to measure the efficiency of inventory management of any company. Inventory turnover ratio can be assessed from different aspects to gain different insights about a company.

The investor can assess the efficiency of inventory management of a company along with the nature of its business model when she assesses the absolute value of inventory turnover ratio. A company with a low inventory turnover ratio would require a larger investment in its inventory (and working capital) when its business grows. Such companies may find it difficult to convert their profits into free cash flow for shareholders. On the contrary companies with a high inventory turnover ratio can manage their business growth without a lot of investment in their inventory and working capital.

An investor should also analyse the trend of inventory turnover ratio of any company over the past. If the inventory turnover ratio is increasing over the years, then it may indicate that the company is doing something fruitful in its business strategy, which is lowering its cost of raw material like alternate sources of suppliers or alternate cheaper options as raw material. In addition, it may also indicate that the company is able to negotiate better business terms with its customers like minimum offtake or take-or-pay contracts that help the company to plan its inventory requirement in a better manner. On the contrary, if an investor notices that the inventory turnover ratio of a company is declining over the years, then it may indicate that company is facing obsoletion of production technology or is losing its competitive strength and the customers are demanding better terms like “just-in-time” delivery, which increases the warehousing & transportation costs for the company leading to increased investment in the inventory and working capital.

An investor should always compare the inventory turnover ratio of any company with its peers from the same industry. This is essential because different companies resolve different business challenges differently. The companies may choose completely different business strategies for seemingly similar production processes. As a result, different companies from the same industry may perform very differently on key parameters of inventory management, capital expenditure, and debt etc. All these factors would impact the business outcome differently and therefore, would impact the value that the companies would generate for their shareholders. Therefore, before making a final opinion about any company, an investor should always compare its parameters like inventory turnover ratio with its industry peers.

With this, we have come to the end of this article in which we focused on inventory turnover ratio and its importance in stock analysis. We discussed how an investor can make informed judgements about companies when she gets the data of inventory turnover ratio of any company.

Now it is your turn. Do you use inventory turnover ratio in the stock analysis? If yes, then how do you interpret it? What has been your experience in using inventory turnover ratio? Do you find that it can help to differentiate a good company from a poor one? What are the other factors you look at while assessing the efficiency of inventory management of any company?

You may share your views in the comments to this article. Your inputs would be very beneficial for us as well as other readers of our website.

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

This article was originally written and published during the period when I, Vijay Malik, was registered with SEBI as an Investment Adviser. I am currently registered with SEBI as a Research Analyst (Regn. No. INH100008364).

This article is for educational purposes only and should not be construed as investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.

12 thoughts on “Inventory Turnover Ratio: A Complete Guide”

Dear Sir,

Thank you so much for your critical comments.

Regards,

Nihal

You are welcome, Nihal.

Hi Sir,

I have been reading your articles for a month and have been fascinated by the way you have approached teaching the skill of stock analysis. I was reading about the inventory days and was mesmerized by the way you explained it.

As you had given the exercise of analyzing the Chaman Lal Setia Exports Ltd in the above-mentioned article i.e. Inventory Turnover. I went through reading annual reports of the company for past years and yet could not make the absolute conclusion about their business model that differentiates them from other peers in the Industry.

There is some point I want to highlight which I noticed and also got the confirmation from Faisal and you in the analysis of the company.

*The company has high realizations per/kg for their product which is clearly visible when we calculate the same with actual productions.

2021- ₹851 Cr For 29123.6 MT — Realization ₹292/Kg

2020- ₹798 Cr For 23909.1 MT — ₹333/Kg

2019- ₹765 Cr For 23978.8 MT– ₹319/Kg

2018- ₹747 Cr For 20826.2 MT– ₹365/Kg

2017- ₹493 Cr For 29807.4 MT– ₹165/Kg

This is quite confusing that the average realizations when we calculate in accordance with their product pricing listed on the different e-commerce sites are around 150 per Kg. Also, fluctuations in realizations can be understood for the commoditized nature of their business but with this huge fluctuation, my knowledge fails to understand the same. So if going by Faisal’s explanation of their Inventory Turnover being the result of realizations seems conflicting to me. Can you please shed some light on it?

Dear Nihal,

Thanks for writing to us!

If you look at the formula for inventory turnover ratio (ITR), then you would notice that it has sales in the numerator:

Sales / average of inventory at the start of the year and the end of the year

Therefore, if the value of sales of any company increase, then its ITR will increase. Sales can increase either due to an increase in the volume of sales or an increase in the realization i.e. the price of goods. Therefore, an increase in realization is expected to increase the ITR for any company.

Regarding the difference in the average realization of products of the company as calculated from the annual report and as observed on the e-commerce websites, an investor may contact the company directly to understand if the data in the annual report needs any change or if the company is funding discounts for sales on e-commerce websites.

Regards,

Dr Vijay Malik

Dear Sir,

You have explained it in such a simple way that it looks very simple now. Sir, I have just found that KRBL inventory days are 400+. How can it be so high? Is the ratio in the negative? Kindly let me know.

Regards

Dear Krishan,

We request that before asking queries, readers should read the annual reports and credit rating reports of companies in order to find the answers to their queries themselves. This is because, in almost all of the cases, the annual reports and credit rating reports have the answers to their queries. We request you also to do the same.

In addition to reading the annual reports and credit rating reports, you may also read the following article, which will also help you: Analysis: KRBL Ltd

Regards,

Dr Vijay Malik

I have never come across such a text, which explains everything so nicely. It gave me lots of confidence as my concept of ITR is now very much clear. It is much better than what any book can teach. Thanks, Dr Malik

Thanks for your feedback, Vishal.

All the best.

– Dr Vijay Malik

This is how ratios should be taught. Learnt ITR during graduation and post-graduation as well, but this article gave me a different perspective. Nicely explained. Many thanks, Sir.. 🙂

Dear Ganesh,

Thanks for sharing your feedback. All the best.

–

Dr Vijay Malik

Please share an article on ROIC and how this can be calculated basis screener data. Nowadays ROIC is a parameter that is widely used in MNCs. So a detailed sharing like inventory turnover ratio will help.

Dear Shiva,

Thanks for your suggestion. We may write an article on ROIC in future; however, it may take some time.

Regards,

Dr Vijay Malik