It is a hard truth that the management of a company stands between the profits of the business and its public shareholders. The management decides how much of the profits it wants to share with the public shareholders. The corporate world has many examples where the management/promoters of the company siphoned off money from the company instead of giving it to the public shareholders.

In light of such instances, it is said that instead of promoter-owned-and-managed companies, the professionally-owned-and-managed companies are better for the public/minority shareholders. However, over time, we have noticed that companies without any promoter-family are also not risk-free for the minority shareholders. There have been many instances where professional managers of companies benefited at the cost of public shareholders whether these companies were promoter-owned or professionally-owned.

The current article is an attempt to look at some of the examples where the professionals when in charge of the companies seemed to benefit at the cost of public shareholders. The examples include instances of both types of companies, which were owned by promoter-families as well as companies that did not have any promoter i.e. were institutionally-owned or professionally-owned.

The current article aims to highlight the possible pitfalls that an investor may come across when she analyses companies where instead of promoter-family-members, the professional managers have a lot of say in the company matters.

An investor should note that the actions and the companies highlighted in the article may not be against the law. The companies and the professionals might have complied with all the legal requirements. Nevertheless, a minority/public shareholder needs to assess whether these actions are in her interest or not.

Therefore, we advise that instead of looking at specific cases of these companies and labelling them good or bad, an investor should try to understand how these aspects of management are identified and the resources/parts of annual reports that are used to analyse them. Focusing on the conceptual aspects of the discussion and illustrations would help the investor in including these as a part of her stock analysis process, which will help her throughout her investing journey!

How professional managers disproportionately benefit themselves

In our experience of analysing hundreds of companies, we have noticed that in professionally-managed companies, wherever professional managers have attempted to disproportionately benefit themselves, then it has happened mainly via the following means:

- High remuneration, which includes both the salary as well as employee stock options (ESOPs). In such cases, we noticed that the salary of the managers was not linked to the performance of the company. The salary of the managers increased even though the business performance of the company declined.

- ESOPs is one of the most common areas where professional managers disproportionately benefit themselves. Managers very frequently use very low priced restricted stock units (RSUs), which they may get for a nominal price of even ₹1 per RSU. In both the cases of routine ESOPs as well as RSUs, the managers avoid decisions that may hurt the stock price in the short-term even though such decisions might be beneficial to the company in the long-run. These instances occur in both promoter-owned as well as professionally-owned companies. In the promoter-owned companies, an investor would notice that the promoters also tend to benefit themselves irrespective of the performance of the business.

- Frauds: there are many instances of professional managers doing frauds on the companies to benefit themselves at the cost of shareholders.

- Related party transactions: even in the cases of professionally-owned and professionally managed companies, the management may transfer economic benefits from one company to another company in the group, which may not be beneficial to the public shareholders.

- In the extreme scenarios, an investor may notice that professional managers attempt to become promoters of a professionally-owned company and try to convert it into a promoter-owned company.

Let us see real-life examples of such situations where professional managers attempt to benefit themselves at the cost of public/minority shareholders. An investor should always keep in mind that such instances occur in both promoter-owned as well as professionally/institution-owned companies.

A) Remuneration not linked to the performance of the company:

In such cases, the professional managers are able to exercise their influence on the board/key shareholders and as a result, they enjoy increasing salaries and perks irrespective of the business performance of the company. This is true for both promoter-owned as well as professionally-owned companies.

Let us see an example of a company where the remuneration of the professional managers increased even during the period when the company was making losses.

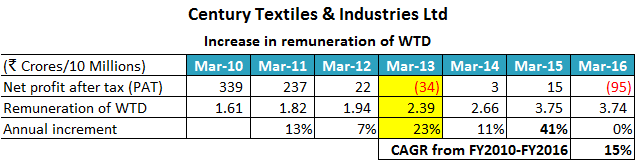

1) Century Textiles & Industries Ltd:

Century Textiles & Industries Ltd is a B.K. Birla group company currently involved in the production of paper and textiles products, and real estate activities. The company has recently sold its large cement division.

While analysing Century Textiles & Industries Ltd, an investor notices multiple decisions that indicate suboptimal capital allocation like:

- execution of the projects is being delayed year after year

- cost of the projects is increasing year after year

- heavily debt-funded capital expenditure is not earning sufficient return

- cement assets are earning less than half the EBITDA per tonne than the competitors

However, when an investor analyses the compensation of the professional managers (whole-time director, WTD), then she notices that during FY2010-FY2016, the net profit after tax (PAT) of the company had declined from net profits of ₹339 cr in FY2010 to a net loss of (₹95) cr in FY2016. However, during the same period, the remuneration of the highest-paid employee of the company, its whole-time director (WTD), increased from ₹1.61 cr (FY2010 annual report, page 26) to ₹3.74 cr (FY2016 annual report, page 40).

An investor would notice that the remuneration of the WTD increased by 132% (3.74/1.61 = 2.32) during the period when the performance of the company declined from reasonable profits in FY2010 (₹339 cr, 8% net profit margin) to net losses of (₹95) cr in FY2016.

An investor is surprised to see that during FY2013 when Century Textiles & Industries Ltd made a net loss of (₹34) cr, the remuneration of the WTD increased by 23% from ₹1.94 cr (FY2012 annual report, page 29) to ₹2.39 cr (FY2013 annual report, page 30).

From the above disclosures, an investor may feel that the remuneration of the management of Century Textiles & Industries Ltd is not linked to the business performance of the company. Whether the company makes profits or losses, the interests of the management of the company are intact. The increase in the remuneration of the WTD from ₹1.60 cr in FY2010 to ₹3.74 cr in FY2016 amounts to about a 15% increase every year even when the performance of the company was going down. In FY2013, when the company reported losses, then the remuneration of WTD increased by even more i.e. 23%.

An investor may fear that in such remuneration structures, the management may not be much bothered about the financial performance of the company as their monetary interests are intact.

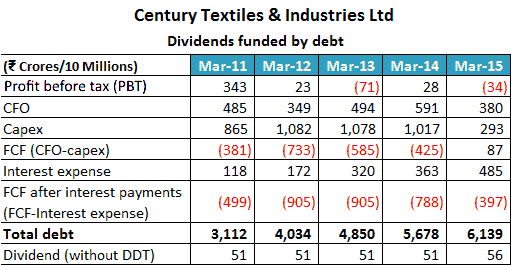

In such a situation, an investor would doubt why the promoters of the company have permitted such a remuneration hike to professional managers when the performance of the business had declined. Upon analysis, the investor notices that the company paid out dividends during FY2011-FY2015 even when it was not making any surplus free cash flow. Most of the time, the promoters of the company i.e. the largest shareholders are the biggest beneficiaries of dividends.

An investor notices that during the phase of FY2011 to FY2015, Century Textiles & Industries Ltd was continuously doing debt-funded capital expenditure. During this period, the company was not making sufficient profits and the cash flow from operations to meet its investment requirements. Further, during FY2013, the company reported a net loss as well of ₹34 cr.

Therefore, during FY2011-FY2015, the investment requirements of the company exceeded its operating cash flows. As a result, the debt of the company was continuously on a rise every year. The debt increased from ₹2,369 at the start of FY2011 to ₹6,139 at the end of FY2015.

However, when an investor notices the dividend payout by the company during this phase (FY2011-FY2015), then she notices that the company continued to declare dividends. The dividend payout (excluding distribution tax) continued at ₹51 cr per year from FY2011 to FY2014 and it increased to ₹56 cr in FY2015. The company declared a dividend (excluding distribution tax) of ₹51 cr even in FY2013 when it had a net loss of ₹34 cr.

An investor would appreciate that during FY2011 to FY2015, the company was investing all the money that it made from operations and more money raised from debt into its capital expansion projects. The debt of the company was continuously increasing. As a result, an investor may infer that the money to be paid to shareholders as dividends is effectively the debt taken by the company from lenders to transfer to the bank accounts of the shareholders of the company.

Century Textiles & Industries Ltd presents a peculiar case where the remuneration of the management is unlinked to the company’s performance and the dividends to the shareholders are unlinked to the company’s performance.

Such a situation has a high probability of creating conditions leading to inefficient allocation of capital. This is because, in the short term, no one is getting impacted due to poor capital allocation. The management keeps getting a significant hike in remuneration even when the company makes losses. The shareholders keep getting their dividends even if the company makes losses even if the company raises more debt to pay money to the accounts of shareholders.

In such a situation, it is usually very long before everyone realizes that the company is in a debt trap where it cannot service its debt from its cash flows. It is then that the companies have to sell assets to repay debt.

Century Textiles & Industries Ltd suffered the same fate and it had to sell its assets and business divisions to repay debt.

An investor may read our detailed analysis of Century Textiles & Industries Ltd in the following article: Analysis: Century Textiles & Industries Ltd

B) Employee stock options (ESOPs) and restricted stock units (RSUs):

ESOPs and RSUs are other key instruments that professional managers use to benefit themselves. It is usually seen that professional managers are able to influence the board/key shareholders to agree to their disproportionately large compensation plans.

Let us see instances where the professional managers received a large proportion of the overall ESOPs portion of the company and its impacts.

1) Ashok Leyland Ltd:

Ashok Leyland Ltd is a part of the Hinduja Group, is one of the leading manufacturers of commercial vehicles in India. Ashok Leyland Ltd specializes in medium & heavy commercial vehicles and buses. The company is run by professional managers and the member of the promoters, the Hinduja family, is the non-executive Chairman of the company.

While analysing Ashok Leyland Ltd, an investor notices that the company has treated its professional manager, the CEO & MD very generously. While reading the FY2019 annual report, an investor notices that the CEO & MD of the company took home a total remuneration of about ₹137 cr. (= 131.21 + 5.81).

FY2019 annual report, page 64:

An investor notices that the biggest part of the remuneration is stock options of about ₹110 cr. Among the stock options, an investor notices that the maximum number of the stock options (7,454,000) is priced extremely generously at an exercise price of ₹1/- per option.

Stock options at an exercise price of ₹1/- per option, is almost the most generous proposition that can be offered by any company to its employees next only to handing over free shares to them.

In addition, when an investor analyses the details of the options available to the employees of Ashok Leyland Ltd, then she gets to know the total number of options and their respective exercise prices.

FY2019 annual report, page 70:

Further advised reading: Understanding the Annual Report Of A Company

From the above table, an investor notices that in the ESOPs plan of Ashok Leyland Ltd, the different tranches of options are put at different exercise prices. There are a total of 13,299,875 options available to all the employees of Ashok Leyland Ltd, 5,845,875 options (44%) are available to employees for exercise prices of ₹80/-, ₹83.5, and ₹109/-. However, a very large portion of options, (7,454,000, 56% of all the options) are available at an exercise price of ₹1/-.

Moreover, an investor notices that all the generously priced options (7,454,000 at ₹1/-) are allotted to one single person, the CEO & MD of the company. Whereas all the remaining employees of the company have been competing for the balance 44% of options that too priced at ₹80/- to ₹109/-.

Then, the investor realizes that the company has treated its CEO exceptionally generously.

From one perspective, it does not come as a surprise to the investor when she notices that in 2019, many of the minority shareholders had voted against the remuneration of the CEO & MD when the proposal was put to the vote of the shareholders. In total, 14.16% of shareholders had rejected the proposed remuneration of the CEO for FY2019.

FY2019 annual report, page 36:

While reading about the senior management of Ashok Leyland Ltd, an investor notices that the CEO & MD of the company, Mr. Vinod Dasari, was in this position from April 2011 to March 2019 after which he left Ashok Leyland Ltd to join Royal Enfield.

While doing a detailed analysis of Ashok Leyland Ltd and focusing on the capital allocation, merger, amalgamation, buyout, investment decision and business performance of the company during FY2011 to FY2019, an investor comes across quite a few decisions that leave room for improvement like:

i) Investments in Optare Plc. UK:

Ashok Leyland Ltd started its investments in Optare Plc. in FY2011 as a small investment of ₹50 cr for taking a 26% stake. However, by FY2019, this investment led to losses of about ₹1,000 cr for the shareholders of Ashok Leyland Ltd. The shareholders have lost almost all the money put by Ashok Leyland Ltd in Optare Plc by way of equity or loans and are now holding 99.08% of the company.

ii) Investments in Albonair GmbH:

In the case of Albonair companies, it may seem to an investor that the management of Ashok Leyland Ltd is continuing with a loss-making acquisition where it has invested hundreds of crores of rupees and about 12 years of management time. However, even after all these investments, the company is not able to generate any return to the shareholders of Ashok Leyland Ltd and is making losses. It tried to sell Albonair by keeping it in “held for sale” for two years in FY2014 and FY2015. However, it could not find any buyer for Albonair. Nevertheless, instead of cutting its losses, Ashok Leyland Ltd threw good money after bad money every year.

iii) Investment in a joint venture with John Deere, USA:

The joint venture proved a failure from the start as the JV could never make money and finally, after losing hundreds of crores of rupees of the shareholders, Ashok Leyland Ltd decided to wind it up.

iv) Joint venture with Nissan for light commercial vehicles:

The LCV JV lost hundreds of crores of rupees and as a result, Ashok Leyland Ltd recognized a loss of 42% of its investments in the JV, whereas Nissan took a complete 100% loss on its equal investments (it was an equal investment JV). Nissan thought it better to cut its losses and sold its entire stake in the JV to Ashok Leyland Ltd for ₹1 (ONE RUPEE).

In the light of these sub-optimal capital allocation decisions, it does not come as a surprise to the investors that many public shareholders voted against the remuneration proposal of the CEO & MD.

An investor may read our detailed analysis of Ashok Leyland Ltd in the following article: Analysis: Ashok Leyland Ltd

2) DCB Bank Ltd.:

DCB Bank has its origins in the merger of many cooperative banks in the 1930s. It was granted the scheduled bank license by the Reserve Bank of India in 1995. Renowned Tata group bought 4.6% in DCB Bank in 2007.

On October 13, 2015, DCB Bank came up with its future business strategy and informed the public through stock exchange filings:

In the above filing, DCB Bank stated that:

- It plans to increase the branch expansion speed from earlier 25-30 branches per year to about 150 branches within next one year along with various other technology initiatives

- It had done detailed planning for this business strategy and expects that the cost ratios and in turn profits would be negatively impacted in the short term horizon of about 2-3 years but these decisions would create long term wealth for the shareholders from FY2019 onwards.

The Bank has done in-depth planning by assessing various parameters like probable break-even, payback, return on equity, return on assets etc. and the management seemed to be in the know of the steps that they are taking. The management seemed an ideal one, which prioritizes the long term interests of the business over the short term incentives. I find that such bold managements are in rarity nowadays and appreciate such managements.

However, the markets were spooked by this announcement. The share price of DCB Bank tumbled 30% in two days from ₹133.45 on October 13, 2015, to ₹92.35 on October 15, 2015.

The reaction of the stock market started with the report of Kotak Securities, which downgraded DCB Bank to “Sell”:

Kotak labelled the management strategy as “very dangerous…..disappointing shift in their strategy”

In quick succession, Edelweiss downgraded DCB Bank to sell.

Soon thereafter, DCB Bank filed another announcement to stock exchanges on October 15, 2015:

We recently announced our intention to install 150+ additional branches within 12 months so as to have more than 300 branches by December 2016. This was part of a new approach which has also other elements mentioned in General Q and A dated October 13, 2015.

Post the above announcement we have received feedback on our branch expansion plans from investors, analysts and other stakeholders. We sincerely thank them for taking time to express their feedback

In view of the feedback received, and in close consultation with our Chairman, the management team has decided to install 150+ branches in a cautious. prudent and calibrated manner over a period of 24 months (instead of 12 months).

This announcement meant that the business plan, which seemed to have been devised well after detailed background work, proper research with possible challenges in execution and their responses in place, was changed based on feedback from analysts. To stress, this was the feedback from investors and analysts who might not have worked in a bank branch and would have hardly done the research and hard work that DCB Bank staff might have done to devise the business strategy.

This was a complete “U” turn from the earlier strength and boldness expressed by the management. This demanded a deeper assessment.

One possible answer seemed to lie in the annual report for FY2015 on the page detailing the employee stock options outstanding for the Bank.

It showed that at the end of FY2015, DCB Bank employees had about 1.1 cr. (11 million) options outstanding, which were exercisable at a weighted price of ₹47.29.

On October 13, 2015, when DCB Bank’s share price was ₹133, these options (ESOPs) had a value of about ₹95 cr. to their holders. And as per the prevalent corporate culture, a huge majority of these ESOPs are expected to be in the hand of top very few senior management employees.

On October 15, 2015, when the DCB Bank’s share price fell to ₹92, the value of these 1.1 cr. options had declined from ₹95 cr to ₹50 cr. That is a decline in value of a whopping ₹45 cr. and that too primarily from the hands of the top very few senior management employees.

A decline of ₹45 cr. in wealth (whether real or notional) is very significant for any salaried employee. This significant decline in value of ESOPs presents one probable explanation for the almost U-turn that the DCB Bank management did on its business strategy based on apparent “Analyst” feedback.

Read: How to do Management Analysis of Companies?

C) Frauds:

In the corporate world, there have been many instances where professional managers did fraud on the companies and as a result, the shareholders of the company suffered.

Let us see a couple of examples where senior professional managers attempted to benefit themselves by way of fraud.

1) National Peroxide Ltd:

National Peroxide Ltd is a Wadia Group company and the largest manufacturer of hydrogen peroxide (H2O2) in India.

While analysing National Peroxide Ltd, an investor notices that in FY2018, the company came across a financial fraud of about ₹37 cr conducted by its employees including senior management employees. The company terminated the services of these employees and filed criminal complaints with the police.

FY2018 annual report, page 116:

Embezzlement of funds of the Parent Company: 1. During the current financial year, the Parent Company’s management has identified instances of embezzlement of its funds by certain employees of the Parent Company, including senior management employees, whose services have since been terminated. Based on the management’s scrutiny and the forensic investigation report, the amount of the embezzlement is ₹3,702.98 lakhs. The Parent Company has initiated criminal proceedings against these employees including filing of FIR and application for other appropriate action with the Joint Commissioner of Police, Economic Offences Wing.

Later on, from media reports, an investor gets to know that the police had arrested Mr. Suhas Lohokare (ex. MD) and an accountant of the company, Mr. Nipul Trivedi. The media report mentioned that these suspects siphoned off money, which was for the payments of sales tax and value-added tax (VAT) for over 10 years, from 2008-2017 (Source: Times of India)

Suhas Lohkare, who was brought from Pune and arrested

EOW had earlier arrested Nipul Trivedi (40), an accountant with the firm

The suspects siphoned off money for payment as sales tax and Vat over 10 years, from 2008. They claimed the ST receipts were pending with the government and they would get them later,” added an officer

After this fraud, National Peroxide Ltd acknowledged that its internal processes needed strengthening. As a result, the company changed its senior management team including the MD and the VP-Finance as well as its internal auditors. The company mentioned that it is revisiting its key contracts as well as customer and vendor prices.

An investor may read our detailed analysis of National Peroxide Ltd in the following article: Analysis: National Peroxide Ltd

2) Quick Heal Technologies Ltd:

Quick Heal Technologies Ltd is an Indian company providing security software solutions like antivirus, antispyware, antimalware etc. to retail consumers under the brand Quick Heal and to enterprises and the govt. segment under brand Seqrite.

While analysing Quick Heal Technologies Ltd, an investor notices a case where a General Manager of the company was conducting fraud on it by selling its products through companies owned by him.

Quick Heal ex-GM arrested for fraud (Source: Pune Mirror)

A former general manager of leading anti-virus solution provider Quick Heal has been arrested for allegedly duping the firm to the tune of Rs 1.24 crore over the last 10 years by selling its products through companies owned by him.

Many times, such cases of fraud by employees seem to be a result of weak internal control processes. However, it also indicates that investors should be cautious while assuming that handing over the control of the company to professional managers is a solution to all the problems of promoter-owned companies.

An investor may read our detailed analysis of Quick Heal Technologies Ltd in the following article: Analysis: Quick Heal Technologies Ltd

D) MNC-owned, professionally managed companies shifting economic benefits away from minority shareholders:

When an investor comes across incidences of promoters siphoning off funds from listed entities, then a thought comes to her mind that she should prefer institutionally-owned and professionally-run companies. The underlying thought process is that in the institutional shareholders, there is not a single family who controls the company and as a result, the instances of promoters shifting economic benefits away from minority shareholders would be less. However, the truth is not such straightforward.

This is because there have been instances where institutionally-owned and professionally-run companies have shifted economic benefits from the listed entity to other group companies, which impacts the minority shareholders of the listed company.

Let us see a few examples where institutionally-owned and professionally-run companies have shifted economic benefits from listed entities.

1) Honeywell Automation India Ltd:

Honeywell Automation India Ltd is a part of Honeywell group, USA, is its Indian subsidiary working in automation and control systems in industries, buildings, automobiles etc.

While analysing Honeywell Automation India Ltd, an investor comes across many situations where it looks that the company has utilized resources belonging to the listed company for the benefit of its other group companies, which is equivalent to shifting the economic benefits from the minority shareholders of the listed company to its group companies.

i) Usage of funds of Honeywell Automation India Ltd by other group companies:

While reading the past annual reports of the company, an investor notices that at multiple instances Honeywell Automation India Ltd gave inter-corporate loans to other Honeywell group entities.

In FY2007, Honeywell Automation India Ltd gave inter-corporate deposits of ₹32.5 cr to group companies (FY2007 annual report, page 30):

- Honeywell Turbo Technologies (I) Pvt. Ltd: ₹18.5 cr

- Honeywell Turbo (India) Pvt. Ltd: ₹14 cr.

In FY2008, Honeywell Automation India Ltd gave inter-corporate deposits of ₹509 cr to group companies (FY2008 annual report, page 28):

- Honeywell Turbo Technologies (I) Pvt. Ltd: ₹505 cr

- Honeywell Turbo (India) Pvt. Ltd: ₹4 cr.

In FY2009, Honeywell Automation India Ltd gave inter-corporate deposits of ₹55.4 cr to group companies (FY2009 annual report, page 28):

- Honeywell Turbo Technologies (I) Pvt. Ltd: ₹45.9 cr

- Callidus Technologies India Pvt. Ltd: ₹9.5 cr.

In FY2010, Honeywell Automation India Ltd gave inter-corporate deposits of ₹78.7 cr to group companies (FY2010 annual report, page 28):

- Honeywell Turbo Technologies (I) Pvt. Ltd: ₹78.7 cr

In FY2011, Honeywell Automation India Ltd gave inter-corporate deposits of ₹3.8 cr to group companies (FY2011 annual report, page 27):

- Honeywell Controls and Automation India Pvt. Ltd.: ₹3.5 cr

- Matrikon Industrial Solutions India Pvt. Ltd: ₹0.3 cr.

An investor would appreciate that these transactions where the money of Honeywell Automation India Ltd has been given to the group companies, is equivalent to the economic benefits are being transferred from one company to another.

Further advised reading: How Promoters benefit themselves using Related Party Transactions

ii) Global corporate overheads of Honeywell group:

While analysing the expenses of Honeywell Automation India Ltd, an investor notices that over time a significant amount of expenses have been charged as “corporate overhead allocations”. The following table shows that during FY2009-2020, the company has charged about ₹873 cr as corporate overhead allocations.

According to the company, these expenses pertain to the services of Honeywell group companies used by Honeywell Automation India Ltd.

FY2009 annual report, page 38:

With effect from previous year, the Company has accounted for corporate overhead allocation, in respect of various services rendered by Honeywell group companies.

An investor would notice that in the absence of break-up/details of the services charged under “corporate overhead allocations”, this expense becomes a black box. There is no means for an investor to assess whether these expenses are justified. It looks like a case similar to transfer pricing, where companies use products and services provided by their global entities in different regions.

Transfer pricing has always invited disputes because many times instead of fair market value, many other considerations enter into the picture when companies allocate values to the products & services of one region utilized by other regions.

Under transfer pricing, companies may allocate a higher share of expenses to companies that are profitable so that the other loss-making entities of the group may also show good financial performance. Other similar considerations might go into deciding how much “corporate overhead” would be charged to Honeywell Automation India Ltd.

An investor may read our detailed analysis of Honeywell Automation India Ltd in the following article: Analysis: Honeywell Automation India Ltd

2) Stovec Industries Ltd:

Stovec Industries Ltd is a leading producer of printing machines & consumables for textile printing, graphics printing. The company is a part of the SPGPrints group of the Netherlands.

While analysing Stovec Industries Ltd, an investor comes across an incidence related to the acquisition & sale of a subsidiary company, Atul Sugar Screens Pvt. Ltd (ASSPL). In this transaction, it seemed that the company paid significantly for acquiring ASSPL; however, it later sold it off along with other sugar-screen assets to a group company for a seemingly cheaper valuation. In addition, the company continued to manufacture sugar screens in the same plant and started to pay rentals to the group company.

The investor may read full details of this transaction in our detailed analysis of Stovec Industries Ltd in the following article: Analysis: Stovec Industries Ltd

Let us understand this transaction in a short detail below.

In FY2014, Stovec Industries Ltd acquired a 100% stake in Atul Sugar Screens Pvt. Ltd (ASSPL) from Atul Electro Formers Ltd for about ₹8 cr. At the time of the acquisition, ASSPL did not have any significant assets. Its net worth was only about ₹3.50 lac. It did not have any meaningful fixed assets. All its current assets (trade receivables, inventory, cash & bank balance of ₹42 lac) were to be set off against the trade payables of ₹53 lac.

Therefore, almost the entire amount of about ₹8 cr. paid by Stovec Industries Ltd to the seller (Atul Electro Formers Ltd) was a consideration for the trademark, technical know-how, and non-compete fee.

In FY2018, Stovec Industries Ltd sold the entire sugar screens business (including the one purchased with ASSPL) to one of its group companies, Veco B.V. for about ₹20 cr.

- Sale of entire equity stake with all the assets of Atul Sugar Screens Pvt. Ltd (ASSPL) for ₹10.4 cr.

- Sale of assets of Stovec Industries Ltd related to the sugar screen business along with the associated trademarks for ₹9.96 cr.

Upon analysis, an investor notices that the disclosure made by the company to BSE on April 5, 2018, indicates that the sugar screens business owned by Stovec Industries Ltd (outside of ASSPL) had a net worth of ₹19.96 cr. In addition, the net worth of ASSPL was about ₹6.3 cr, which was held as cash in the bank account.

Therefore, if an investor looks at the sale transaction in its entirety, then she notices that while selling the sugar screens business along with all the trademarks to the group company, Veco B.V., for consideration of ₹20 cr., Stovec Industries Ltd has given away a total net worth of more than ₹26 cr. (6.3 + 19.96).

Therefore, an investor would appreciate that in this sale transaction, the shareholders of Stovec Industries Ltd did not receive even the full consideration for the net worth given away by them. It is anybody’s guess what valuation has been assigned to the trademarks and intangible benefits, which were purchased by Stovec Industries Ltd in about ₹8 cr. when it bought Atul Sugar Screens Pvt. Ltd (ASSPL). If an investor assumes that these trademarks were at the same value of ₹8 cr, then the total value of assets given away comes to near ₹34 cr (=26+8).

Therefore, it looks like the sale transaction might have got a higher valuation if it was sold by Stovec Industries Ltd to an independent third-party instead of a group company.

Moreover, as per the disclosures made by Stovec Industries Ltd with the results of the June 30, 2018 quarter, even though the company has sold its assets of sugar screens, it is still manufacturing the sugar screens in those assets/plants.

June 2018 quarterly results, page 4:

During the quarter, the Company has sold certain identified assets of galvanic business. Resultant gain on such sale of assets of INR 37.441 Million has been shown as exceptional items in the results for the quarter ended June 30, 2018. However, the operations of galvanic business is continued by the Company after entering into the Contract Manufacturing Agreement.

An investor would appreciate that in this arrangement, the company (Stovec Industries Ltd) has sold the assets of the manufacturing plant but is still using it to manufacture the goods.

In such a situation, in addition to the manufacturing costs like raw material, labour costs etc., the company (Stovec Industries Ltd) will have to additionally pay for the rent to use the plant for manufacturing goods. Whereas the entity who bought the manufacturing plant (Veco B.V.) is assured of a usually fixed rental income from Stovec Industries Ltd for giving the plant on lease to it.

In addition to the above transaction, while analysing Stovec Industries Ltd in detail, an investor also notices the following:

- The company had given its building on lease to a third-party where the lease rent had not increased during the reported period of FY2012-FY2017 whereas normally, in commercial agreements, lease rentals increase after every period of 3-years.

- The company had paid remuneration to its managing directors over 5% of net profit after tax (PAT) whereas our assessment of multiple companies indicates that the remuneration of key management personnel of most of the companies stays within 2-4% of PAT. Therefore, a payment of 5% of PAT in salary may not be higher than legal limits but it seems higher than the norm that we had noticed in the companies that we have analysed.

An investor may read our detailed analysis of Stovec Industries Ltd here: Analysis: Stovec Industries Ltd

E) When professionals attempt to become promoters of the company:

When an investor prefers an institutionally/professionally-owned and professionally-managed company over a promoter-owned-managed company, then she assumes that the shareholders’ interests would be better protected. One of the reasons for this belief is that the professionally-owned companies lack an identifiable promoter-family as owner. Therefore, shareholders believe that the probability of one person controlling the resources of the company and siphoning it off is low.

However, at times, investors come across situations where the key employees who control the decision-making powers in a professionally-owned company, start to take steps to increase their control of the company. In turn, they attempt to become the promoters of the company by taking control of voting rights of a large portion of shareholding by various means including preferential allotments etc.

In such companies, an investor notices that over time, the nature of the company changes from professionally-owned & managed to promoter-owned & managed. This change nullifies the underlying assumption of the investor to invest in the professionally-owned company in the first place.

Let us see the example of a company where the professional managers seem to increase control over the voting rights and in turn, effectively attempt to convert it into a promoter-owned company.

1) Ion Exchange (India) Ltd:

Ion Exchange (India) Ltd is an Indian company involved in water treatment plants, wastewater processing, sewage treatment, packaged drinking water, and seawater desalination etc.

While analysing Ion Exchange (India) Ltd in detail, an investor can identify the change in the management culture of the company over the years.

While reading the FY2013 annual report of Ion Exchange (India) Ltd, an investor gets to know about the history of the company.

- Investor notices that the water treatment company of the UK, Permutit, was represented in India by another UK company, J. Stone. (1930s)

- In 1952, Permutit decided to leave India due to falling business, but J. Stone convinced them to keep India business alive.

- G. Shankar Ranganathan, an employee of J. Stone worked hard and could improve the business significantly.

- Because of the improving business, Permutit formed an Indian subsidiary, Ion Exchange (India) Ltd, with 60% foreign holding in 1964.

- In 1984, when Permutit decided to leave India, then Ion Exchange (India) Ltd formed many employee welfare trusts, which bought the shares held by Permutit and the company became a wholly Indian owned entity.

FY2013 annual report, page 2:

Shankar Ranganathan, Founder and Chairman Emeritus

From small beginnings, with pioneering and entrepreneurial spirit, Mr. Ranganathan created the strong Ion Exchange edifice and raised it into a global player with a vision. In the 1930s J. Stone, a Calcutta based British Company, was Permutit’s agent in India. Their main business was from the Indian railways and textile mills. In 1952, because of dwindling sales, Permutit planned to shut shop in India but were persuaded by J. Stone to give it a lost chance. A young Ranganathan joined J. Stone – with a staff of just two commissioning engineers and a steno-typist. Business picked up and Permutit accepted Ranganathan’s recommendation to form a subsidiary company and in 1964 Ion Exchange (India) Ltd., was registered with 60% equity by Permutit, 40% Indian. In 1984 when Permutit divested their holding, he advocated and set up employee welfare trusts, a pioneering concept for India and Ion Exchange become a wholly Indian company.

While reading additional aspects via annual reports of the company, an investor notices that effectively the trust got the money to buy the shares from Permutit from Ion Exchange (India) Ltd in the form of loans. As per the FY2017 annual report, page 97, Ion Exchange (India) Ltd disclosed that the purpose of its loans to the trust is to create a corpus for these trusts. The trusts own 2,662,914 shares of the company (FY2017 annual report, page 97).

The trusts receive dividends of about ₹75-80 lac every year for the shares held by them and utilize this dividend amount to repay the loans to the company for about ₹60 lac every year (FY2017 annual report, page 96).

By the understanding received until now, an investor understands that originally, Ion Exchange (India) Ltd was led by Mr. G. Shankar Ranganathan and the employee welfare trusts owned a significant stake in the company. This seems like a professional corporate setup.

When an investor looks at the current Chairman & Managing Director of the company, Mr. Rajesh Sharma, then it looks like that he is not a blood relative of Mr. G. Shankar Ranganathan.

Moreover, as per the FY2014 annual report, page 9, Mr. Rajesh Sharma joined the company in 1974 and then worked across various positions in his career with the company before becoming the current Chairman & Managing Director.

This seems like a leadership change where the leadership baton was passed from one professional to another professional of the company.

However, if an investor looks at the current senior leadership, then she notices that Executive Director, Mr. Dinesh Sharma, is the brother of current CMD, Mr. Rajesh Sharma. Moreover, among the other directors of the company are Executive Director, Mr. Aankur Patni and his father Mr. M. P. Patni. Therefore, it seems that now family relations are making their presence in the board of directors.

In addition, if an investor notices the change of shareholding of the senior management over the years, then she notices that the current leadership is increasing its stake in the company consistently by various means.

a) FY2011: Share allotment via exercise of employee stock options and private placement:

In FY2011, Ion Exchange (India) Ltd disclosed in its annual report that it has allotted 950,000 shares to key management personnel (KMP) and their relatives on the exercise of employee stock options and private placement.

FY2011 annual report, page 94:

While reading the details of related parties, an investor finds that the relatives of key management personnel are the father, mother, wife and daughter of Mr. Rajesh Sharma, Mr. Dinesh Sharma and Mr. Aankur Patni.

FY2011 annual report, page 93:

Relatives of Key Management Personnel:

- Mr. Mahabir Patni – Father of Mr. Aankur Patni

- Mrs. Nirmala Patni – Mother of Mr. Aankur Patni

- Mrs. Aruna Sharma – Wife of Mr. Rajesh Sharma

- Mrs. Poonam Sharma – Wife of Mr. Dinesh Sharma

- Mrs. Nidhi Patni – Wife of Mr. Aankur Patni

- Ms. Pallavi Sharma – Daughter of Mr. Rajesh Sharma

Therefore, in FY2011, the current senior leadership of the company increased its stake by 950,000 shares via the exercise of employee stock options and private placement.

At the end of FY2011, the company reported a total number of 13,098,011 shares including the 950,000 shares issued to KMP and their relatives.

FY2011 annual report, page 74:

Therefore, in FY2011, the KMP and their relatives increased their stake in the company by 7.25% (= 950,000/13,098,011) in FY2011 by way of exercise of employee stock options and private placement.

Also read: How Promoters use Loopholes to Inflate their Shareholding

b) FY2014: Increase in stake of promoters of Ion Exchange (India) Ltd:

In FY2014, an investor notices that the shareholding of promoters in the company increased from 40.6% at the end of FY2013 to 44.44% at the end of FY2014.

FY2013 annual report, page 28:

FY2014 annual report, page 40:

In absolute terms, in FY2014, the promoters’ shareholding increased by 941,334 shares (= 6,458,727 shares at FY2014 – 5,517,393 shares at FY2013)

While analysing further details, an investor finds that the shareholding of CMD, Mr. Rajesh Sharma, and shareholding of Mr. M. P. Patni, the father of Executive Director, Mr. Aankur Patni, have increased in FY2014.

FY2014 annual report, page 108:

Further, in the FY2014 annual report, there is no mention of allotment of shares to KMP by way of exercise of employee stock options.

However, in FY2014, the share capital of the company increased significantly due to the issuance of 1,070,282 new shares as a part of an amalgamation of one of the associate companies, Ion Exchange Services Ltd (IESL).

FY2014 annual report, page 108:

While reading about the amalgamation of Ion Exchange Services Ltd (IESL), in the FY2013 annual report, an investor notes that Ion Exchange (India) Ltd held a 41.58% stake in IESL and the remaining stake was owned by other parties.

FY2013 annual report, page 89:

As in FY2014, there is no allotment under the exercise of stock options to KMP; therefore, an investor can assume two possible situations leading to an increase in stake of promoters by 941,334 shares:

- The promoters bought 941,334 shares from the open market and increased their shareholding.

- The promoters are the significant other parties in Ion Exchange Services Ltd (IESL) holding 58.42% stake (= 100 – 41.58) who are allotted most of the 1,070,282 new shares issued by Ion Exchange (India) Ltd in FY2014.

An investor may contact the company directly to get clarification about the other counterparties in Ion Exchange Services Ltd (IESL) who were allotted shares on amalgamation and whether the KMP constituted these counterparties.

Further advised reading: How Promoters use Loopholes to Inflate their Shareholding

c) FY2020: increase in stake of promoters:

From FY2014, until Sept 2019, the number of shares owned by the promoters of Ion Exchange (India) Ltd stayed constant at 6,458,727. Even though, the percentage shareholding declined from 44.44% in FY2014 to 44.04% in FY2019 because of the allotment of new shares on exercise of stock options to employees other than key management personnel (KMP).

Sept 2019 shareholding pattern as per the BSE website:

Even among the promoters, the number of shares owned by the KMP and their relatives seems to stay constant until Sept 2019 (Source BSE, March 2014, and Sept. 2019):

- Rajesh Sharma: 781,218 shares,

- Dinesh Sharma: 588,521 shares,

- Aankur Patni: 254,668 shares,

- M. P. Patni: 711,747 shares

However, in the current financial year, in Oct. 2019 and Dec. 2019, there have been certain transactions where the employee welfare trusts have sold shares and the KMP, their relatives, Independent Directors and other major shareholders have picked up the majority of those shares. These transactions have been reported under section BSE > Disclosures > Insider Trading 2015 at the BSE website.

BOARD OF DIRECTORS:

- Mr. Rajesh Sharma Chairman & Managing Director

- Mr. Dinesh Sharma Executive Director

- Mr. Aankur Patni Executive Director

- Dr. V. N. Gupchup Director

- Mr. M. P. Patni Director

- Mr. T. M. M. Nambiar Director

- Mr. P. Sampath Kumar Director

- Mr. Abhiram Seth Director

- Mr. Shishir Tamotia Director

- Ms. Kishori J. Udeshi Director

- On Oct. 31, 2019, out of 175,000 shares sold by the trusts, 171,875 shares have been bought by the key management personnel and their relatives and 3,125 shares have been picked by Mr. Bimal Jain who owns 2.82% stake (414,098 shares) in the company at Sept 30, 2019 (Source: BSE).

- On Dec. 20, 2019, out of 94,000 shares sold by the trusts, 90,500 shares have been bought by the Independent Directors and 3,500 shares have been picked by Mr. Anil Manocha, and Mr. Harminder Mohan Bareja.

- On Dec. 23, 2019, 2,900 shares were sold by the trusts, which have been bought by Parthasarathy Sampath Kumar (Independent Director).

As per the BSE website, the mode of disposal/acquisition of these 271,900 (= 175,000 + 94,000 + 2,900) shares is “Market Sale”/”Market Purchase”. Therefore, an investor may assume that these transactions indicate that the shares until now owned by the employee welfare trusts are now owned by individuals, which are primarily existing KMP and directors of the company.

An investor would note that the changes in the management and shareholding structure of the company over the last decade indicate that Ion Exchange (India) Ltd may be changing its character from an “Employee-owned, Employee-run” company to a “Promoter-owned, Promoter-run” company. The current increase in stake of key management personnel and directors in the company along with the presence of blood relatives in the senior management and board of directors indicates that the nature of management succession in the company in future may be different from the last management succession when the leadership baton changed from one professional employee to another professional employee.

In addition, an investor notices that the key management personnel who are in charge of Ion Exchange (India) Ltd have been taking a remuneration higher than the legal limits.

Remuneration availed by the Promoters over statutory limits:

While reading the past financial performance of Ion Exchange (India) Ltd, an investor comes across certain instances where the promoters/key management personnel have taken remuneration, which exceeded the statutory limit stipulated under the Companies Act. As a result, the company had to apply for special approval from the central govt. to regularize the excess remuneration paid by the company to the promoters.

- In FY2011, the Executive Directors took a remuneration, which was ₹2.50 cr in excess to the statutory limits.

FY2011 annual report, page 28:

The remuneration paid to the Executive Directors is in excess of the limits specified in Schedule XIII of the Act by Rs. 2,50,66,516 for which steps have been taken by the Company to obtain Central Government approval.

- In FY2015, the Directors took a remuneration, which was ₹0.74 cr in excess to the statutory limits.

FY2015 annual report, page 100:

The company has paid remuneration to the directors as per the terms of their respective service contracts with the company which were approved by the board of directors and shareholders. In view of inadequacy of profit in the current year, pursuant to provision of section 197 read with section II of part II of Schedule V of the Companies Act 2013. the company has made an application with the Central Government for payment of the excess remuneration amounting to Rs. 73,74,532 to the said directors, which is pending approval.

An investor may read our detailed analysis of Ion Exchange (India) Ltd in the following article: Analysis: Ion Exchange (India) Ltd

Summary

By looking at the above examples, an investor would appreciate that labelling professional-control-and-management as shareholder-friendly and promoter-control-and-management as shareholder-unfriendly without analysing each case, may not be a wise decision.

Even though the popular belief is that professional ownership and professional management are shareholder-friendly; however, the above examples, as well as many other instances in the corporate world, indicate that even professional managers have at times done acts that were not shareholder-friendly. These actions included:

- Taking a high remuneration where the managers were not held accountable for poor outcome of their decision; instead, they kept on receiving substantial salary hikes despite losses in business operations.

- Lucrative ESOPs/RSUs: At times, the professional-managers could influence the board/key shareholders to grant them extremely lucrative stock options (ESOPs)/restricted stock units (RSUs) whereas the minority shareholders voted against it. However, the small voting share of minority shareholders could not change the outcome.

- Frauds: At other occasions, the professional managers also resorted to outright fraud to benefit themselves at the cost of company and shareholders.

- Related party transactions with group companies: We also witnessed instances where the professionally-owned-and-managed companies indulged into similar related party transactions like promoter-owned-and-managed companies where the economic benefits were transferred from the listed company to other group companies.

- Attempts to fully control the professionally-owned company: At times, the employees tried to fully control the professionally-owned company by appointing their friends and relatives on the board of directors as well as in senior management positions. Also, the professional managers-in-control resorted to preferential allotment of warrants and other means to increase their control on the voting rights of the company, which tends to convert the company in a promoter-owned-and-managed company with the managers-in-control becoming the new promoters.

Therefore, we believe that whenever an investor analyses a company, then she should analyse the management of the company on a case-to-case basis without getting influenced by any prejudices related to professional-control-and-management being shareholder-friendly and promoter-control-and-management being shareholder-unfriendly.

A promoter-manager may turn out to be an extremely shareholder-friendly person and a professional manager may hurt shareholders’ interest by prioritizing her interest above everything else.

There is no general rule that works in management analysis. Every company and its management needs to be seen in exclusivity. The same analysis guidelines apply to both professional management as well as promoter-management.

An investor may take guidance from the following article for management analysis: How to do Management Analysis of Companies

With this, we have come to an end of the current article where we looked at various instances where the professional managers seem to have prioritized their interests ahead of shareholders’ interest.

Now, it is your turn. What has been your experience of analysing and investing in professionally-owned and managed companies? How do you look at professional-management vis-à-vis promoter-management? What parameters do you use to analyse professional management? Are these parameters different from the analysis of promoter management?

It would be great if you could share your inputs as comments. It would be very useful for us as well as other readers of the website.

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

This article was originally written and published during the period when I, Vijay Malik, was registered with SEBI as an Investment Adviser. I am currently registered with SEBI as a Research Analyst (Regn. No. INH100008364).

This article is for educational purposes only and should not be construed as investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.

8 thoughts on “Are professionally managed companies safer for shareholders?”

Insightful article. Thanks for sharing the article.

Thanks for your feedback, Anup.

An eye-opener article. Thanks for the efforts.

You’re welcome. Wish you the best.

Sad that you changed the old comment layout I mean Disqus one.

Thanks for sharing your feedback.

Thank you so much for your detailed report on Esops. I kindly request you to deliver the prospects of Concor Corporation of India, MPS LTD, ITC, for the short term. Thank you, sir.

Dear G. Jaganmohan,

Thanks. We do not have any views on any company for the short-term. You may share your detailed analysis of these stocks with us. We will be happy to provide our inputs to your analysis.

Regards,

Dr Vijay Malik