Transformers and Rectifiers (India) Ltd (TRIL) is one of India’s largest transformer manufacturers, producing multiple types of transformers like power, distribution, furnace and rectifier transformers as well as shunt reactors, focusing on power transmission & distribution and industrial sectors.

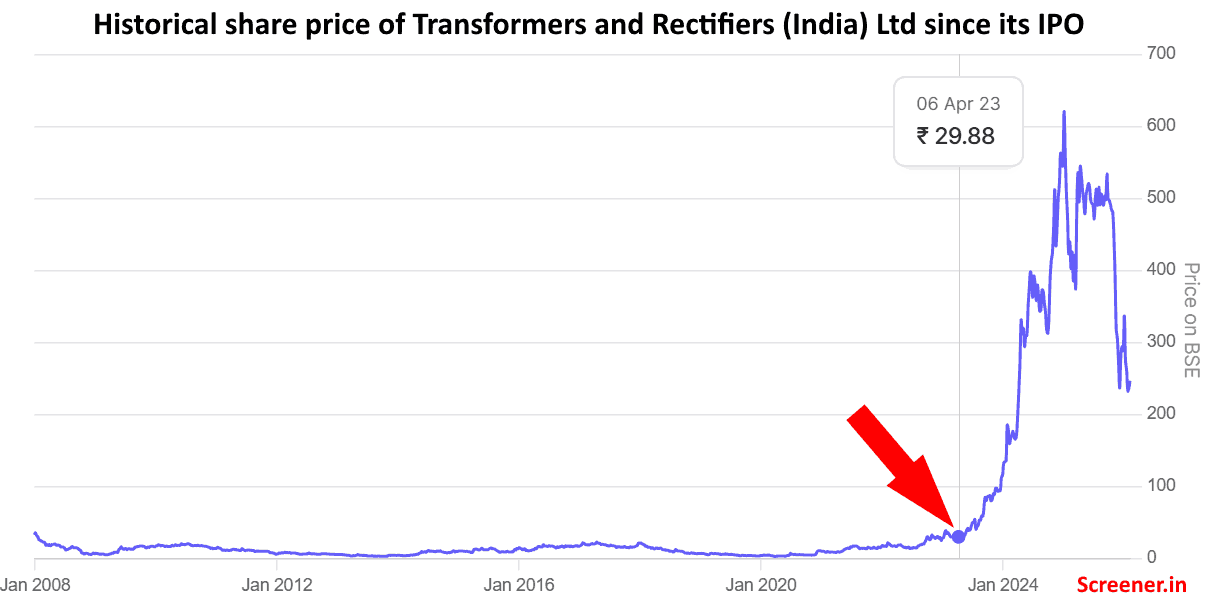

In recent years, the company has witnessed a strong revival in its financial performance, attracting significant interest from investors. As a result, its share price has increased from about ₹9 in Feb. 2021 to a peak of ₹650 in January 2025 before correcting to about ₹250 now.

Our experience shows that during the times of euphoria of increasing sales and profits, at times, investors might overlook and underestimate key risks that might be of concern to long-term investors. Therefore, in the current article, instead of arriving at a buy or sell conclusion, we highlight some of the risks that a long-term investor should keep in mind and conduct enhanced due diligence before making any opinion and investment decision about the company.

Key aspects long-term investors should examine carefully

Key risk areas that require closer examination:

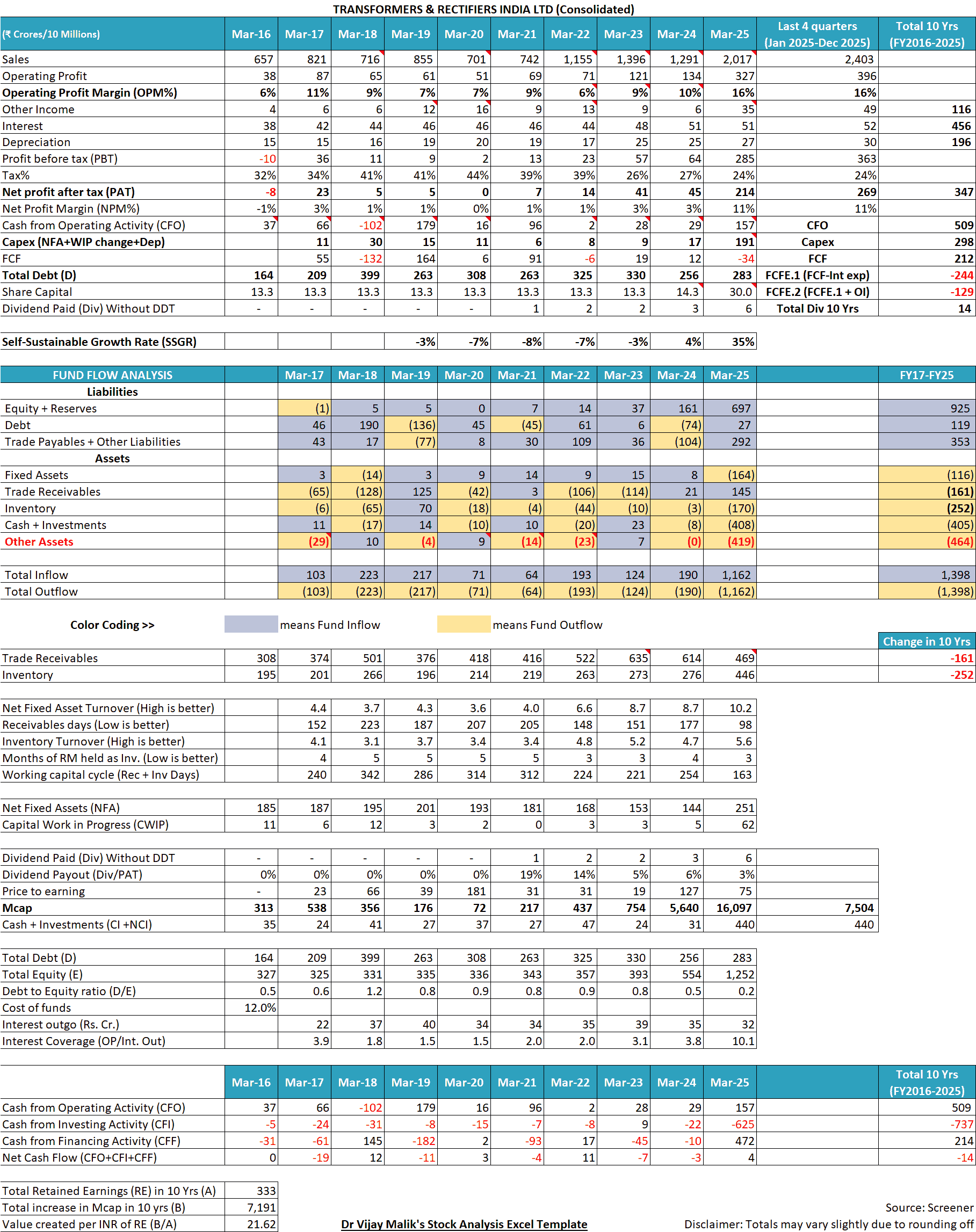

A snapshot of the financial performance of Transformers and Rectifiers (India) Ltd over the last 10 years is provided below to set the context for the discussion that follows:

1) Cyclical profit swings at Transformers and Rectifiers (India) Ltd:

In the last 5 years (FY20-FY25), sales and profits of the company have increased at a very fast pace. Its sales increased 24% year on year (YoY) from about ₹700 to over ₹2,000 cr. In the same period, its net profit after tax (PAT) has increased 251% YoY, from about ₹0.4 cr to ₹214 cr.

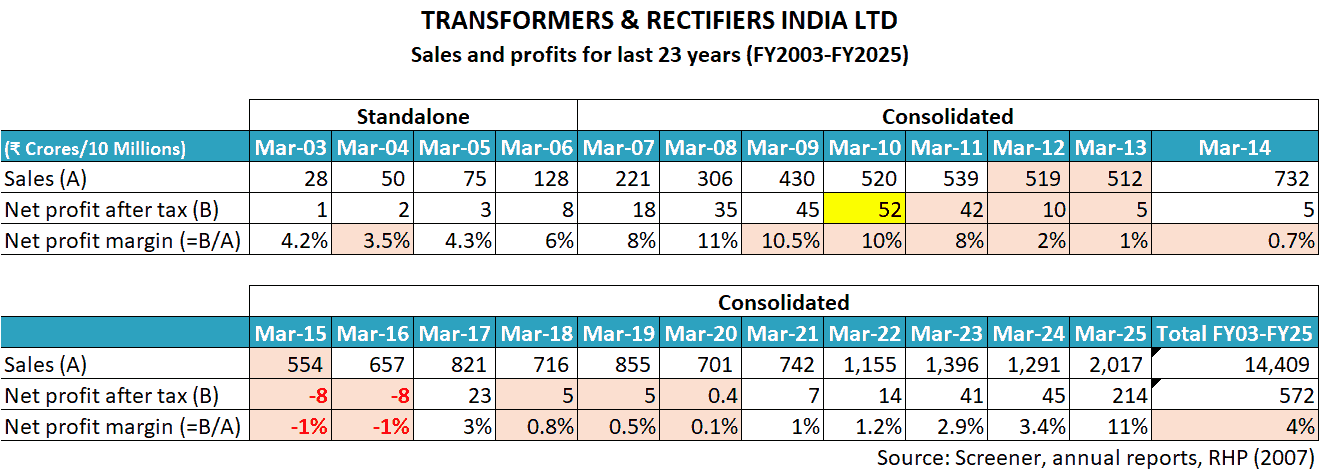

However, the moment an investor broadens her horizon and analyses the long-term financial performance of Transformers and Rectifiers (India) Ltd over the last 23 years (FY07-FY25), she notices the cyclical nature of its business. The table below shows the sales, profits (PAT) and net profit margin (NPM) of the company over the last 23 years.

TRIL used to have an NPM of about 4% in FY2003, and it increased to 11% in FY2008. Thereafter, the NPM started declining continuously, and the company reported net losses in FY2015 and FY2016. Thereafter, for most of the next 4 years, the company barely avoided losses with an NPM of 0.1% in FY2020. Thereafter, its NPM increased to 11%, a level that was previously seen 17 years back in FY2008. In FY2010, the company had reported a profit of ₹52 cr; however, due to a long downcycle, it took nearly 15 years to surpass it in FY2025.

Even now, the company reminisces about the profit margins that it had at the time of its IPO in FY2008. (Conference call transcript (CC), Jan-2024, p.7):

Jitendra Mamtora: See, I tell you, when we came out with the IPO, our EBITDA margin was 18% to 20%, approximately. And the kind of market now or the kind of demand which has come now, we have started looking at that kind of EBIT margin.

There are many reasons leading to cyclicity in the business performance of Transformers and Rectifiers (India) Ltd. Let us see a few of them.

1.1) Cyclicality of customer industries and its impact on the company:

The biggest consumer of TRIL, the power sector, undergoes significant challenges every few years.

Power generation is highly capital-intensive with very little margin of error in business performance. Any disruption in business assumptions can damage the entire business model. For example, a scarcity of natural gas led to the failure of multiple gas-based power plants in India (Source: Lack of gas, high cost ‘stranded’ more than half of India’s gas-based power plants: January 17, 2019)

Transformers and Rectifiers (India) Ltd also had to write off ₹12.5 cr from one of its customers, a gas-based power plant. (Annual report (AR) FY16: p.67; AR FY17: p.68).

Another problem for the power sector is the continued losses made by distribution companies (discoms). Every few years, discoms accumulate large losses and are unable to pay for power, leading to financial stress in the entire power production ecosystem. In FY2015 and FY2016, Transformers and Rectifiers (India) Ltd reported losses due to the poor financial health of discoms. (AR FY15: p.9; AR FY16: p.50)

Other key consumers of Transformers and Rectifiers (India) Ltd, like steel etc., also have investment cycles. They rely heavily on the phase of the economic cycle and commodity prices for their financial performance and, thereby, capital expenditure.

As a result, every few years, troubles faced by its consumers get passed on to transformer manufacturers, impacting their performance. For example, just before the start of the recent upcycle in FY2021, the industry saw many players close down their plants as survival became impossible.

Credit rating report (CR) by India Ratings (IndRa), Mar-21:

Also, capacity closures have been witnessed in the sub-220 Kilovolt (KV) segment, given low margins and high working capital requirements

The recent improved financial performance of Transformers and Rectifiers (India) Ltd is due to the up-phase in the cyclical transformer industry, leading to demand outpacing their supply. (AR FY24: p.12)

Advised reading: How to do Business Analysis of a Company

1.2) Tender-driven competition and the absence of sustained pricing power:

Over the years, the company has highlighted that its contracts with its customers have price variation clauses, i.e. it can pass on any increase in raw material costs (e.g. cold-rolled grain-oriented (CRGO) steel, copper etc.) to its customers and protect its profit margins. (CR IndRa, Jun-25)

However, despite the supposed protection from adverse raw material price movements, we have seen that TRIL’s profit margins have been very volatile and even declining to losses in FY2015 and FY2016 and barely avoiding losses in many other years.

One of the major reasons it is not able to maintain its profit margins and sees such wide fluctuation is that it does not have a sustained pricing power over its customers.

This is because it faces intense competition from both domestic and international players, who, at times, are ready to supply transformers at below cost to gain market share, which, when combined with the tender-based ordering system of its major customers, takes away any sustained pricing power from the company. (AR FY12: p20; CR CARE, Oct-07).

Therefore, during the downcycle, TRIL has to bid at very low/aggressive prices, leading to a sharp decline in profit margins. As a result, profit margins of the company suffer despite price variation clauses in its customer contracts. (CR IndRa, Jun-22).

As the industry is cyclical, during the up-phase, when demand is more than supply, the company gains negotiating power and resorts to picking and choosing orders. (CC Aug-25, p.9).

Chanchal Rajora:…now we have become pick and choose in terms of the order. We are choosing the order considering what is the revenue margins we are making as well as what is the delivery time is there. So we are not going after every order

Therefore, long-term investors should keep in mind that Transformers and Rectifiers (India) Ltd operates in a cyclical business, where periods of strong demand and margin expansion are often followed by phases of sharp deterioration. Therefore, investors should be cautious while projecting the company’s recent financial performance into the future.

If the entire 23-year period from FY2003 to FY2025 is viewed as a single cycle, then TRIL generated cumulative sales of ₹14,409 crore and a cumulative net profit of ₹572 crore, translating into a long-term net profit margin of about 4%. This highlights how much short-term upcycles can distort the perception of underlying profitability.

As a result, before extrapolating the improved performance of recent years, investors should recognise that the company’s products are inputs into capital expenditure cycles of larger sectors such as power and steel, which themselves are highly cyclical. Strong profit growth during favourable industry phases can easily be mistaken for structural improvement. Long-term investors must distinguish between temporary benefits of demand upcycles and businesses with sustained pricing power, as cyclical recoveries often reverse sharply when industry conditions weaken.

Advised reading: How to analyse New Companies in Unknown Industries?

2) Capital intensity and dependence on external funding across cycles:

The business of TRIL is capital-intensive, both from the perspective of fixed assets and working capital. Creating transformer manufacturing and testing facilities (e.g. short-circuit testing) as well as running them requires significant capital.

For example, in H1-FY2024, the company had to retest about 10 transformers for one of its clients, Gujarat Energy Transmission Corporation Ltd (GETCO), whose costs significantly impacted its profit margins. (CR IndRa, May-24).

In the past, internal accruals of Transformers and Rectifiers (India) Ltd have always fallen short of meeting the costs of creating new capacities. Therefore, all its major expansions are funded fully by public investors’ money, i.e. equity dilution.

For example, in the major expansion of its Moraiya plant in FY2008-FY2010, the entire cost of ₹102 cr was fully funded by the proceeds from its IPO (₹139 cr) in FY2008. (RHP, Dec-07: p.18).

The current ongoing capacity expansion (to 75,000 MVA) as well as backward integration projects, are to be fully funded out of the QIP issue of ₹500 cr done in June 2024 (prospectus for QIP (P-QIP), Jun-24, pp.76, 79).

Advised reading: Asset Turnover Ratio: A Complete Guide for Investors

2.1) Working capital intensity and execution vulnerability:

Business of Transformers and Rectifiers (India) Ltd is highly working capital intensive, with a large amount of money always stuck in inventory and trade receivables.

Some of the reasons for a large requirement of working capital are a long lead time for imported raw material as one of its key inputs, CRGO steel is not produced in India, a long inventory holding time as it needs to customise transformers to clients’ needs, leading to long designing and manufacturing time as well as long transportation time, as transformers are bulky. Moreover, clients pay only a part of the money (about 80%) on delivery and hold the balance as retention money. (Sources: CC IndRa, May- 24, May-25)

These large working capital requirements have created big challenges for Transformers and Rectifiers (India) Ltd. For example, in FY2024, due to a lack of timely payments from customers, it suffered a loss of ₹150 cr in sales and had to delay its capital expenditure plans. (CC Aug-23, pp.5, 7).

Abhishek Sirohiya: major instance is due to the delay in receipt of funds from GETCO…it could have enabled us to build further revenue of around 150 Crores because this has reduced my capacity to procure the material from the market and convert it into the finished goods.

Advised reading: Operating Performance Analysis: A Simple & Complete Guide

2.2) Liquidity stress, promoter support, and repeated equity dilution:

TRIL primarily relies on bank borrowings to meet its working capital needs. However, its requirements are so large that frequently, its banks’ funding limits are 100% utilized. The resulting cash flow crunch threatened its operations and forced it to look for equity infusion.

For example, during losses of FY2015 and FY2016, it took shareholders’ approval for a qualified institutional placement (QIP) of ₹125 cr in its 2016 AGM to fund its working capital and capital expenditure. (AR FY16, p.13)

However, TRIL could not raise money from the market despite renewing the QIP approval from shareholders for multiple subsequent years.

Then, again, in FY2021, utilisation of its funding limits reached 100%, which disturbed its lenders, who, instead of giving more working capital limits to TRIL, reduced their funding. (CR CARE, Jul-20, Oct-20).

As a last resort, the promoters of the company had to infuse unsecured loans and give their personal property as security to the lenders to convince them to give a loan to the company. (CR CARE, Oct-20).

Therefore, during the downcycle of FY2013-FY2022, no one was willing to give money to the company, neither the lenders nor the market.

However, this support from promoters could suffice only for about 3 years before the company again hit a liquidity crisis in 2023. (CC Nov-23, pp.4, 10)

Chanchal Rajora: we have fund-based limit of Rs. 163 crore and presently it’s almost 100% utilized

The company experienced short-term mismatch in working capital that caused delay in execution of certain jobs.

However, from FY2023 onwards, the industry upcycle had begun, and investors became interested in its stock.

Therefore, in 2023, the company capitalised on the positive investors’ sentiment and raised ₹120 cr. from equity investors to repay some of its debt to get some breathing space. (CR IndRA, May-24).

Since then, the company took benefit of the positive investor sentiment and has repeatedly raised large sums of money from the market. Within 9-months of the last QIP, it came with another much larger QIP issue in June 2024 and raised ₹500 cr.

Thereafter, within 10-months of its second QIP, in early 2025, when its share price was at a lifetime peak of ₹650, it took another QIP approval to raise another ₹750 cr. Nevertheless, since then, the share price has declined more than 60% to about ₹250 on Feb. 4, 2026.

Availability of capital to Transformers and Rectifiers (India) Ltd depends on the phase of its industry cycle. Therefore, an investor should monitor whether in this upcycle, the company is able to raise the required money before the cycle turns, because in the downcycle, no one gives it money easily, be it lenders or the market.

Long-term investors should note that capital intensity is not only about fixed assets but also about the cash that gets locked into receivables and inventories. Investors should always assess whether growth creates free cash flows or merely expands the balance sheet. Businesses that require frequent equity dilution or high leverage to fund working capital put shareholders at significant risk when business conditions weaken.

Advised reading: Free Cash Flow: A Complete Guide to Understanding FCF

3) Governance, compliance lapses, and minority shareholder risks:

Over the years, multiple instances draw focus of investors on the corporate governance and compliance culture at the company.

The most notable incident is an ongoing issue with the World Bank (WB), where initially, the WB banned TRIL for 4 years under allegations of payment of bribes to govt. officials in Nigeria to win a contract in Nigeria, as an initial investigation by the World Bank Integrity Vice Presidency (INT) found “sanctionable misconduct” by TRIL (Source).

according to the INT, T&R made improper payments to public officials during the bidding and execution phases of a World Bank-funded contract and failed to disclose commission payments made to two agents to influence the award and execution of the contract

The proceedings about this case are currently going on.

Previously, in 2023, the company was sanctioned by Gujarat Energy Transmission Corporation Limited (GETCO) with a stop deal notice for 3 years, stating that TRIL forged documents for the transformers supplied to it. During its internal investigation, TRIL suspended two of its employees (Source: BSE, BSE). Later on, the company found weaknesses in its internal controls, which it apparently strengthened after this incident (CC Jan-24, p.5).

In this case, TRIL could limit the damages by retesting the said transformers and later on, GETCO lifted the stop deal sanction.

Earlier, at the time of its IPO, Transformers and Rectifiers (India) Ltd disclosed that the Gujarat Pollution Control Board (GPCB) had rejected its application for no objection certificate (NOC) for its Changodar plant as the company was running the plant without the approval of GPCB. (RHP, Dec-07, pp.xii).

3.1) Short tenures of external CEOs and leadership stability concerns:

In the history of Transformers and Rectifiers (India) Ltd, only two non-promoter/outside professionals joined as chief executive officers (CEOs); however, both of them resigned within a short period of joining the company.

First, Mr Mathew Kurian was appointed as CEO on February 6, 2023 (Source: NSE), and he resigned within 3 months from May 4, 2023, citing ill health. On his LinkedIn profile, Mr Mathew Kurian shows his latest ongoing experience as CEO in the capital goods industry from Sept 2022 to present without referring to his tenure at Transformers and Rectifiers (India) Ltd.

Then, after a gap of more than 2 years, on July 8, 2025, Transformers and Rectifiers (India) Ltd appointed Mr Mukul Srivastava as CEO. However, he only stayed for about 6 months and resigned on January 7, 2026, citing personal reasons.

A long-term investor may analyse why external professionals are resigning from leadership positions of the company within a few months.

3.2) Absence of independent validation of funding requirements:

Over the years, while raising money from equity investors, Transformers and Rectifiers (India) Ltd has not provided an assessment of its funds’ requirements by any independent financial institutions etc.

For example, while raising ₹500 cr in QIP (June 2024), it provided, as proof of funds’ requirement, quotations from its own subsidiaries and not from any bank or financial institution.

Prospectus for QIP, June 2024, page 57:

Our funding requirements and the proposed deployment of Net Proceeds have not been appraised by a public financial institution or a scheduled commercial bank…majority of the quotations…have been procured from two of its subsidiaries…we cannot assure you that we could not have achieved more favourable terms had the current quotations been procured from unrelated parties.

Even during its IPO in FY2008, when it funded the entire cost of the Moraiya plant from IPO proceeds, the requirement of funds for the expansion was not assessed/verified by any institution. (RHP, Dec-07, p.xvii).

An investor would note that a lack of independent assessment of the estimated costs by any bank or financial institution increases the risk in proper utilization of funds raised from the public.

Advised reading: Why Management Assessment is the Most Critical Factor in Stock Investing?

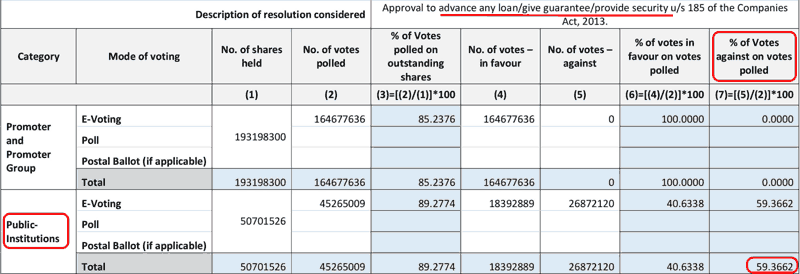

3.3) Related-party transactions and divergence between promoter and public shareholders:

In the AGM held on May 13, 2025, more than 59% of public institutional shareholders voted against the proposal to give loans/guarantees for up to ₹100 cr to related parties. However, the resolution was passed as the promoters, who are majority shareholders (64.36%) in the company, voted in favour of it.

Results, 31st AGM, May 13, 2025, page 12:

In the same AGM, more than 35% of public institutional shareholders voted against the reappointment of the founder-promoter, Mr Jitendra U. Mamtora, as the Chairman and Whole Time Director of the company. (Results, 31st AGM, May-25, p.8)

One of the public institutional shareholders, Invesco India Manufacturing Fund, cited high remuneration, performance incentive/commission and reimbursement of expenses by the company incurred by his spouse and attendant while on business trips as reasons to vote against the appointment of Mr Jitendra U. Mamtora (Source: Invesco Mutual Fund):

Long-term investors should note that governance quality shows itself not through promoters’ statements but through actions taken during periods of financial stress. Frequent leadership changes, related-party transaction proposals, and misjudgment of funding needs might be early warning signs. Investors must pay close attention to how promoters treat minority shareholders when the business is facing tough times, as such behaviour often determines long-term wealth creation more than reported earnings growth.

Advised reading: How Promoters benefit from Related Party Transactions

Conclusion: Learning for Long-Term Investors

This analysis shows that financial recoveries/turnarounds, especially in cyclical manufacturing businesses, can hide structural weaknesses that only reveal themselves over a full business cycle. It shows that revenue growth, margin expansion, and rising order books are necessary for value creation; however, long-term investors must assess whether such growth is supported by pricing power and cash generation.

The case of Transformers and Rectifiers (India) Ltd highlights how working-capital intensity, funding decisions, and governance behaviour play a key role in long-term shareholder outcomes. Many times, investors usually ignore such factors during business upcycles; however, during downcycles, these factors become very critical for shareholders.

For long-term investors, the key lesson is not about this company alone, but about developing a framework to identify early warning signs in similar businesses. We believe that sustainable wealth creation depends as much on avoiding structurally weak businesses as it does on identifying growth opportunities.

Further recommended reading: How to Monitor Stocks in your Portfolio

In our premium services, this kind of analysis is used primarily as a filtering tool to eliminate businesses where long-term risks outweigh the benefits of growth. Only companies that demonstrate sustainable cash flows, prudent capital allocation, and aligned promoter incentives eventually qualify for inclusion in my long-term portfolio.

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

I, Vijay Malik, am a SEBI-registered Research Analyst (Regn. No. INH100008364). This article is for educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.

2 thoughts on “Transformers and Rectifiers (India) Ltd: When Cyclical Recovery Masks Deeper Risks”

This approach is called as Investing by looking the rare mirror .

Investing should always be done by looking forward , just like driving the car.

Now let’s see – what lies ahead for TARIL

Green Energy corridor Phase 3 and 4 will be announced soon – creating big opportunity for the company

Rectifiers orders for Green Hydrogen are yet to start in

Every bit of MW added in Generation , needs transformation capacity

Listen to CG powers earnings call , Q3 FY 26 – even if all the planned expansions for transformers manufacturing comes online , still there will be enough room for everyone to do Business , since demand supply gap is huge

Don’t look in rare mirror while Investing , look what lies ahead

Hi Gaurav,

Thank you for taking the time to read the analysis and for sharing your perspective in such detail.

Markets naturally consist of participants with different time horizons, assumptions, and analytical frameworks, and such diversity of views is what ultimately enables trading and price discovery.

The intent of this article was not to comment on near-term or medium-term demand visibility, but to highlight how factors such as cyclicality, cash-flow behaviour, capital intensity, and governance can influence outcomes for long-term investors across full business cycles.

I appreciate you engaging with the article and contributing your thoughts.

Regards,

Dr Vijay Malik