Kirloskar Brothers Ltd (KBL), a part of the Sanjay Kirloskar Group, is one of India’s leading manufacturers of pumps and fluid management systems, catering to sectors such as water supply, irrigation, power, and oil & gas. In recent years, the company has reported a sharp improvement in its sales and profitability, which has attracted a lot of investor interest.

Our experience shows that during the periods of improving business performance, investors may, at times, underestimate key risks that can become important from a long-term perspective. As a result, the current article focuses on some of the aspects that a long-term investor should examine closely before making any opinion about the company.

Please note that this analysis is not intended to arrive at a buy or sell conclusion. Instead, it aims to highlight factors that tend to get ignored during periods of strong business growth.

Key Aspects Long-Term Investors Should Examine Carefully

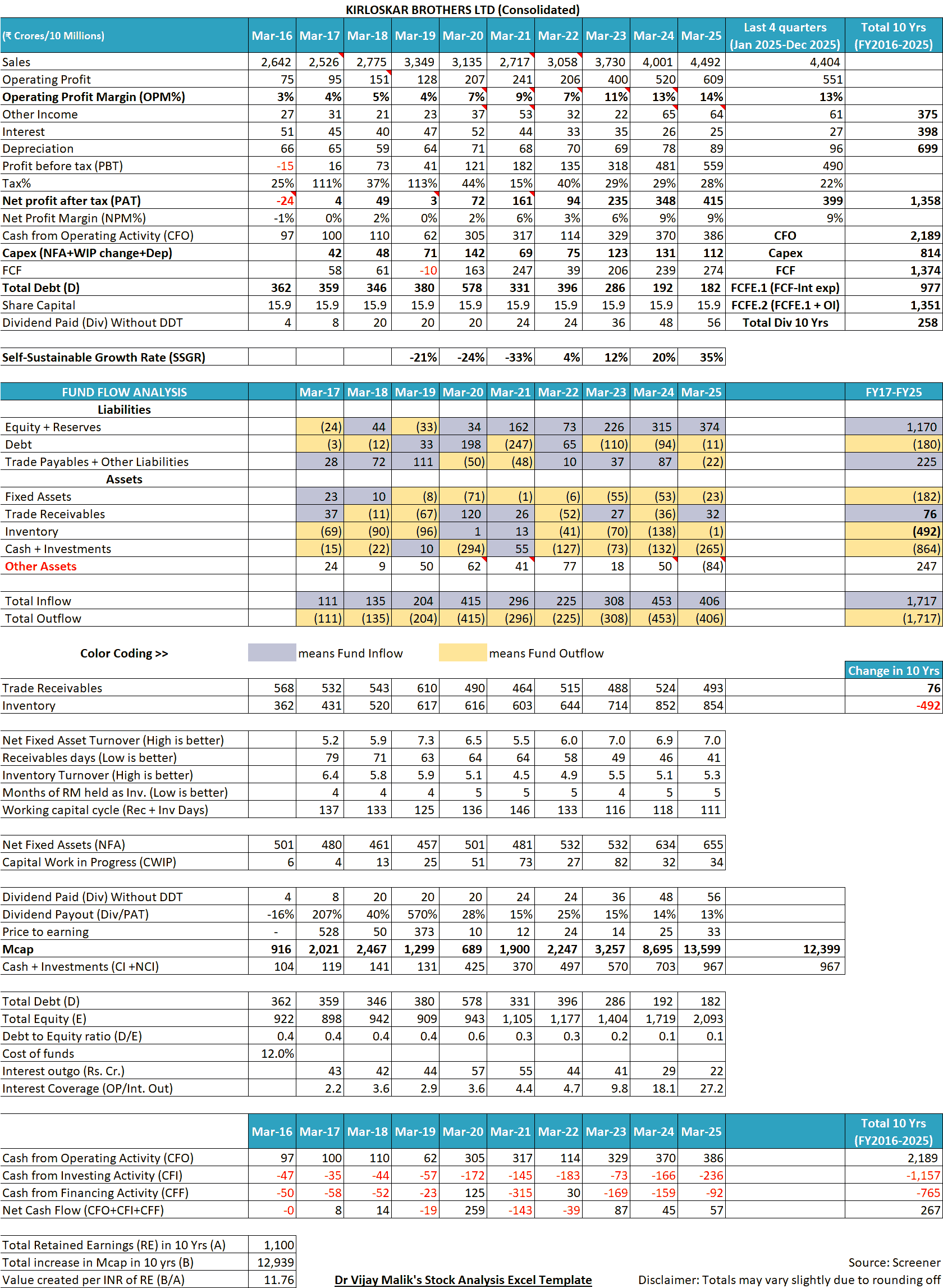

A snapshot of the financial performance of Kirloskar Brothers Ltd over the last 10 years is provided below to give you the context for the discussion that follows:

1. Promoter Dynamics and Their Impact on Business Stability:

Mr Chandrakant Shantanu Kirloskar, father of Mr Sanjay Kirloskar, died in 1987. However, the division of family assets between four remaining key family members, wife: Ms Suman Kirloskar and three sons: Atul, Sanjay and Rahul, has not been clean. As a result, every now and then, promoter family disputes keep appearing, threatening the interests of public companies and shareholders.

At times, disputes start from seemingly petty incidents like the construction of a gate at their family home, and end up in full-blown legal battles or when one son (Sanjay) tries to demolish an ancestral property wall by bringing in bulldozers, the entire family reaches the police station (Source: Pune Mirror).

Apart from the inharmonious division of personal property assets, the division of business assets among family members is also fraught with issues. Due to intricate crossholdings of group companies, brothers Atul, Sanjay and Rahul are not able to enjoy clear ownership and control of respective businesses. Even after about 40 years since the death of their father, the brothers are not able to cleanly segregate their business interests to avoid disputes (Source: Fortune India).

1.1 Atul and Rahul Kirloskar’s actions on Sanjay Kirloskar:

1.1.1 Fight over the Kirloskar brand for pumps:

In 2009, Kirloskar family members entered into a Deed of Family Settlement (DFS, copy), which was an attempt to peacefully and cleanly segregate the family’s business interests. Eldest son, Atul, got Kirloskar Oil Engines Limited (KOEL), middle son, Sanjay, got Kirloskar Brothers Ltd (KBL) and youngest son, Rahul, got Kirloskar Pneumatic Company Ltd (KPCL), apparently with non-compete clauses.

In 2017, KOEL (under Atul) acquired a pump manufacturer, La-Gajjar Machineries Private Limited (LGM), which competed with KBL (Sanjay) (Source). Also, Atul and Rahul asked Sanjay to stop using the Kirloskar brand for its products, which was an attempt to launch the Kirloskar brand of pumps under KOEL (Atul) (FY2019 annual report (AR) of KBL, pages 72-73).

The promoters seemed to settle the trademark, though temporarily in 2020 (AR2020, KBL, page 85):

Company received a letter dated March 3, 2020 from KPL intimating alleged withdrawal of termination of license as mentioned in notices dated April 2, 2018, with effect from March 3, 2020

However, in 2024, the dispute arose again when Kirloskar Proprietary Ltd (KPL), the owner of the Kirloskar trademark and apparently currently under the control of Atul and Rahul, again asked KBL to stop using the Kirloskar name for its pumps. (AR2025, page 171). The matter is currently sub judice in the Bombay High Court and a Pune Court.

Launch of Kirloskar pumps by any competing Kirloskar group company or inability to use the Kirloskar brand by KBL for its pumps is bound to have a strong impact on the business of Kirloskar Brothers Ltd.

1.1.2. Allegation of financial misdeeds against Sanjay:

In 2022, Atul and Sanjay, who own a significant stake in KBL due to the complicated crossholding structure of Kirloskar group companies, levelled charges of financial missteps against Sanjay and the board of directors, especially highlighting legal and professional expenses of about ₹274 cr since FY2016. They asked for a forensic audit of KBL in an extraordinary general meeting (EGM). However, their resolutions were defeated in the EGM in Dec. 2022 (Source).

1.2. Actions of Sanjay on Atul and Rahul:

1.2.1. KBL’s letter to SEBI reopening the investigation of insider trading:

In Oct. 2020, SEBI held numerous Kirloskar family members, including the three brothers, Atul, Sanjay and Rahul, liable for insider trading in shares of Kirloskar Brothers Ltd during 2010.

These trades were apparently a part of the shuffling of Kirloskar group companies among promoter family members. (Source: SAT order in the matter, Oct. 12, 2022, page 19):

The entire transaction was to reorganize the Kirloskar family holdings in the group companies whereby the selling promoters from Alpana group sold their shares of KBL in their possession to another promoter i.e. KIL

When SEBI initially got information about these trades of 2010, it had asked questions from the involved parties in 2012, and at that time, KBL had intimated to SEBI that only the CFO and the company secretary (CS) of the company had access to unpublished price-sensitive information (UPSI), which is not shared with the directors (SEBI order, Oct. 30, 2020, page 43). Based on this information, SEBI did not proceed with any detailed investigation in the case.

However, in 2016, KBL sent a letter to SEBI stating that it wanted to revise its earlier (2012) reply to SEBI and now, in 2016, stated that, among others, the financial information (UPSI) was available to promoters and directors as well (SEBI order, Oct. 30, 2020, page 44).

KBL vide letter dated April 27, 2016 had informed SEBI that reply given by KBL vide letter in May 10, 2012…needs to be revised. Accordingly, KBL…submitted revised response…stating that “……financial information of the company is shared and made available only to those persons who are the promoters, Directors…

Based on this revised submission by KBL in 2016, SEBI opened a detailed investigation into the trades of Oct. 2010 and in Oct. 2020 convicted Kirloskar family members of insider trading.

Later, when Atul and Rahul Kirloskar’s family members appealed against the SEBI order to SAT, KBL appealed to SAT that the penalties against the Atul and Rahul group should be increased. However, SAT found that there was no insider trading in the entire episode (Source: SAT sets aside SEBI insider trading order against Atul Kirloskar, Rahul Kirloskar and Nihal Kulkarni)

SAT order also dismisses the appeal filed by Kirloskar Brothers Limited for enhancement of penalties and disgorgement of amounts against us

1.2.2. Kirloskar Brothers Ltd filed a case in SEBI against the Atul and Rahul Kirloskar group:

In 2021, KBL (Sanjay Kirloskar) filed complaints against Atul and Rahul Kirloskar group companies, Kirloskar Oil Engines Limited (KOEL), Kirloskar Industries Limited (KIL), Kirloskar Pneumatic Company Limited (KPCL) and Kirloskar Ferrous Industries Limited (KFIL) claiming that these companies are misleading investors by falsely claiming 130 years of history (Source: Kirloskar feud | Sanjay Kirloskar takes battle against brothers to SEBI).

Lesson for investors:

It is unfortunate that, almost 40 years after the demise of Mr Chandrakant Kirloskar, his sons (Atul, Sanjay and Rahul) have still not come to a peaceful settlement about their personal and business interests. Currently, even most of their children are in their 40s; however, looking at petty personal issues getting blown up as full legal and corporate battles using regulatory bodies as tools, an investor wonders whether even the next generation is willing to settle things peacefully.

An investor always carries the risk of any small incident (say, someone parked a car in the wrong place in the family house) ending up hurting the business of public companies and their shareholders.

Also read: How to do Management Analysis of Companies?

2. Shareholding Structure and Constraints on Strategic Decision-Making:

Due to crossholdings of Kirloskar group companies in each other, Atul and Rahul Kirloskar are stuck with a significant shareholding in KBL, most of which is via Kirloskar Industries Ltd (23.91% on March 31, 2026).

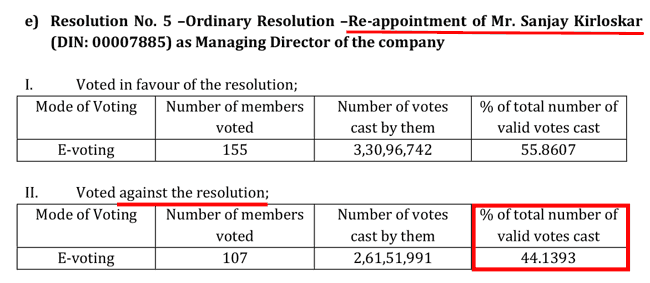

As a result of a frictional relationship, Atul and Rahul Kirloskar’s groups vote against resolutions in shareholders’ meetings of KBL. For example, in the 2025 AGM, there was significant voting against the appointment of Sanjay Kirloskar (44% votes against), his son, Alok Kirloskar (33% votes against), as well as the adoption of financial statements (33% votes against) (Source: Scrutinizer’s Report).

Therefore, if Atul and Rahul Kirloskar control more than 33% voting power of Kirloskar Brothers Ltd, then Sanjay Kirloskar will not be able to execute his vision/decisions that require a special majority, i.e. more than 75% votes in favour.

In Indian corporate law, decisions about constitutional changes, i.e. changes in Memorandum of Association (MOA) or Articles of Association (AOA), corporate restructuring, i.e. approval of mergers, demergers, and amalgamations, changes in share capital, and other strategic moves require a special majority, i.e. >75% shareholders’ support.

With the current situation among the warring Kirloskar brothers, it seems that the family infighting might impact KBL’s business by stopping it from pursuing attractive business opportunities that might arise in future.

3. Limited Transparency in Certain Expense Heads of Kirloskar Brothers Ltd:

In 2022, Atul and Rahul Kirloskar claimed that KBL has spent about ₹274 cr for professional & legal expenses of Sanjay Kirloskar from FY2016-FY2022 (Source: BusinessLine). In its response, in the 2022 EGM notice (page 19), KBL stated that these were primarily paid to consultants like Boston Consulting Group (BCG) and KPMG etc.

Consolidated financials of KBL for the last 10 years (FY2016-FY2025) show a total “Professional, consultancy and legal expenses” of about ₹584 cr.

When analysts asked the management for details about these expenses in a conference call, the company refused to share the breakup, stating that this matter is sub judice (Concall, August 2023, page 15).

Chittaranjan Mate:…it is legal and professional and consultancy fees. Right. They are not legal expenses. Right. It’s a mix of various things. And the breakup of that, we cannot disclose here, because that is a matter of subjudice

An investor may do her own analysis regarding whether courts have stopped KBL from being more transparent by providing details of such large, contentious expenses. She may form her own opinion whether spending ₹60-80 cr on consultants every year has provided enough value for KBL. Please note that these large professional expenses continued even in the years like FY2016, FY2017 and FY2019 when either KBL made net losses or barely reported any profits.

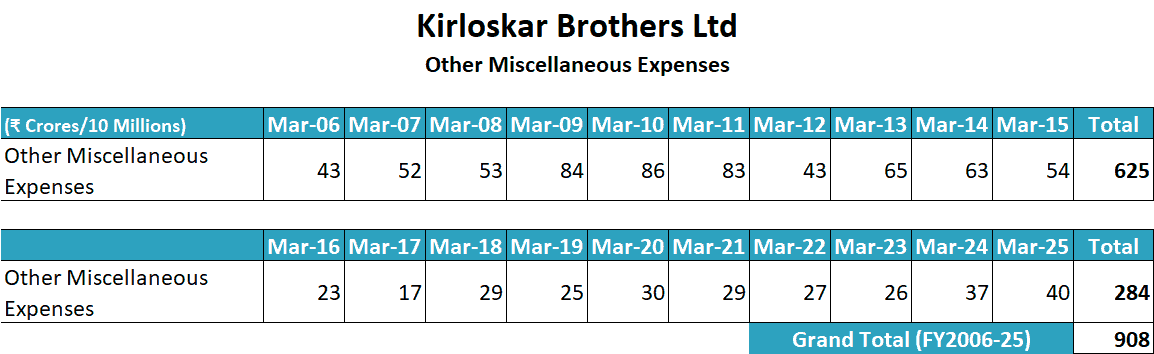

In addition, every year, Kirloskar Brothers Ltd has shown a large amount of “Other Miscellaneous Expenses” for which no details are provided. In the last 10 years (FY2016-2025), KBL showed about ₹284 cr of other misc expenses, and in the previous 10 years (FY2006-2015), it showed a much larger number of about ₹625 cr as other misc. expenses, totalling about ₹908 cr.

Currently, every year, KBL spends in excess of ₹100-125 cr on “Professional, consultancy and legal expenses” and “Other Miscellaneous Expenses” for which investors do not have any details (FY2025: ₹125 cr, FY2024: ₹107 cr).

Also read: Why Management Assessment is the Most Critical Factor in Stock Investing?

4. Capital Allocation Track Record and Strategic Shifts of Kirloskar Brothers Ltd:

Despite being in business for more than 100 years, in the recent past, KBL made some substantial capital misallocations.

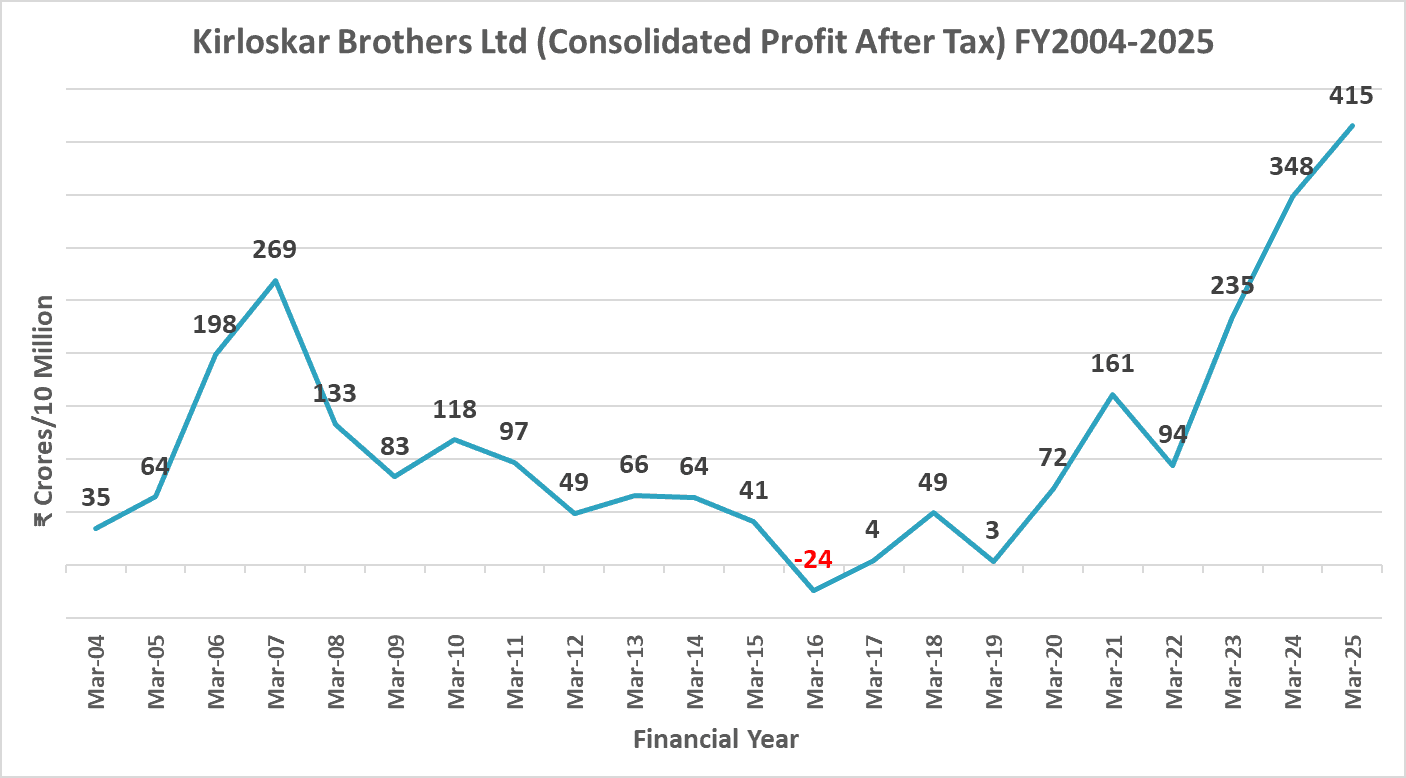

It reported a peak profit of ₹269 cr in FY2007. However, thereafter, its performance saw massive deterioration, declining into losses in FY2016. The company could cross the profit levels of FY2007, after 17 long years in FY2024.

In 2007, Kirloskar Brothers Ltd was highly enthused about the engineering, procurement and construction (EPC) segment and decided to become a total (turnkey) solutions provider. It even acquired Aban Constructions Pvt. Ltd (AR2007, P3).

KBL has moved from a product company to a total system solution provider… we have acquired Aban Constructions Pvt. Ltd.

However, the enthusiasm about the EPC business turned out to be a big capital-destructing decision for KBL. It realised that the EPC business has too many outside-control factors and it was losing money on a lot of its projects, which remained stuck even after 6-8 years.

Conference call (Concall), May 2015:

Management:…projects have been stuck not because we don‟t want to proceed, but because of situations there at the project site it is like site not available, land not available, and still farmer agitation, power supply not available.

still about 700 odd crores of orders which are the old legacy orders…which we have to go ahead and complete. So, there will be some bleeding going ahead on those orders

During this phase, KBL faced a strong liquidity crisis.

Concall, Aug. 2023:

Sanjay Kirloskar: when we started going into this business in a big way of EPC contracting, that we were running short of money. .. you had to get a new order so that you could get the advance so that you could pay your bills.

It soon had to take large write-offs on its investments in EPC business, projects, and receivables. Even in FY2025, it has more than ₹110 cr of receivables outstanding for more than 3 years from the due date (AR2025, P344).

Along the way, it invested significantly in overseas acquisitions and business: SPP Pump (UK, 2004), USA office (2006), Netherlands JV with Industrial Pump Group (2008, 2014), Braybar Pumps (South Africa, 2010, 2013), SyncroFlo (USA, 2014), Rodelta Pumps (Netherlands, 2016).

However, its overseas business became too concentrated on the oil & gas sector, and when in FY2015-2016, oil prices declined sharply, the slowdown in the industry caused significant losses in its international operations, from which it took a lot of years to recover.

Credit rating report (CR) by CRISIL, Feb. 2016:

company’s total loss increased to Rs.450 million for the nine months through December 2015 from Rs.290 million in the corresponding period of the previous year, mainly on account of losses in the international business where demand for pumps from the oil and gas segment has been impacted due to lower crude prices.

CR CRISIL, Aug. 2019:

international subsidiary reported net loss of Rs 99 crore in fiscal 2019 (15 months period ended March 2019) as compared to Rs 40 crore loss in fiscal 2018

CR CARE, Feb. 2024

Overseas subsidiary…reported losses in FY22 and historically in FY19 and FY20.

Subsequently, the company could recover by getting almost completely out of the projects business, which now forms about 3% of overall revenue, down from 75% in FY2010 (AR2023, P17). It also undertook a lot of cost-cutting measures in its international business to turn it around.

CR CARE, Dec. 2025:

improvement in profitability is considering the international business recording profitability compared to losses in the past and increasing focus on product business…KBL has reduced its exposure to projects business,

However, currently, the company’s international business faces challenges from deindustrialisation in the UK due to high energy prices, oil & gas policy uncertainty (Concall, Nov. 2025).

In addition, KBL is facing significant losses in its foundry business, which used to be under The Kolhapur Steels Ltd (TKSL, now merged with Karad Projects & Motors Ltd).

TKSL had been under financial stress ever since KBL acquired it under Board for Industrial and Financial Reconstruction (BIFR) proceedings in 2008. Since then, it has been continuously infusing more money into TKSL. Despite all efforts, TKSL was again referred to BIFR in 2014, requiring more funding (2015, 2016, 2017). KBL even did a strategic shift from consuming all production of TKSL in-house to seeking outside customers. However, TKSL has remained a pain point for KBL and led to continuous write-off of capital (about ₹56 cr over 2020-2025).

An investor needs to closely watch capital allocation decisions of Kirloskar Brothers Ltd, as in the past, the company had even ventured into completely unrelated businesses like silk production by acquiring 200 hectares of land in Nasik, as well as running a full-fledged printing division, none of which made good returns for shareholders.

Also read: How to Identify if Management is Misallocating Capital

4.1. Cyclicality vs Structural Improvement in Performance:

In recent years, Kirloskar Brothers Ltd has reported a sharp improvement in its profitability after a long period of weak performance. At first, this improvement may appear to be a sustainable turnaround led by better strategic and business execution. However, an investor needs to assess whether this improvement is truly sustainable or just a cyclical recovery of end-user industries.

Historically, the company’s performance has been significantly influenced by external factors like capital expenditure cycles in infrastructure and industrial sectors, demand from the oil & gas industry, especially for its international business and the policy environment for large projects. The downturn in these industries led to severe deterioration of KBL’s performance.

The recent improvement in performance has come with a recovery in industrial capex, an improved demand environment after Covid, and the exit from loss-making project business. Therefore, it is important for investors to clearly separate the improvement due to management actions (like exiting EPC, cost control) and the improvement due to cyclical tailwinds. This is because cyclical improvements may not sustain, and dependent businesses may show deterioration in performance when the cycle turns.

5. Internal Financial Controls and Reliability of Reported Numbers:

Over the years, statutory auditors of KBL, as well as its subsidiaries, have reported weaknesses in internal controls, thereby raising questions about the reported financial statements. For example, in FY2016, the auditor cautioned about potential inaccuracies in both the balance sheet and the profit & loss statement due to ineffective financial controls.

AR2016, P71:

Qualified opinion: a) Company’s internal financial controls over accurate and timely estimation of costs relating to project business were not operating effectively which could potentially lead to incorrect revenue recognition.

b) The Company’s internal financial controls for timely assessment of the eligibility of claims receivable were not operating effectively, which could potentially lead to incorrect balances being stated in the balance sheet and consequently its effect on Profit or Loss.

In the same year, the auditors also cautioned shareholders about ineffective financial controls over inventory at its joint venture (JV), Kirloskar Ebara Pumps Limited (AR2016, P116).

In FY2019, statutory auditors cautioned shareholders about inadequate internal controls at its overseas subsidiary, Rodelta Pumps International, raising doubts on revenue, cost of sales, inventories, debtors and work in progress (AR2019, P274).

Previously, during FY2010-FY2012, auditors raised serious questions about its subsidiary Kirloskar Constructions and Engineers Limited related to valuation of inventories, noncompliance with accounting standards, weak internal controls, non-confirmation of receivables & advances and non-provisioning of income tax liabilities, Liquidated damages etc. (AR2010, P96-97; AR2011, P90-91; AR2012, P88-89).

In light of these numerous instances of weak financial controls and processes, investors should be extra cautious and do in-depth due diligence while assessing the financial data reported by Kirloskar Brothers Ltd and preferably do independent checks from multiple sources before making any final opinion.

Also read: How to study Annual Report of a Company

Conclusion: Learning for Long-Term Investors

The analysis of Kirloskar Brothers Ltd highlights how long operating history and recent improvement in financial performance may not always capture the full picture from a long-term investor’s perspective. Many of the highlighted risks, like promoter dynamics, capital allocation decisions, or accounting weaknesses, usually get ignored in the phases of growth and profitability.

Over the years, KBL has gone through multiple phases of expansion, strategic shifts, and course corrections. While recent years show an improved business strategy, an investor should carefully analyse whether this reflects a sustainable long-term improvement or is due to favourable industry conditions.

An investor should pay special attention to key strategic decisions by promoters. Ongoing promoter disputes, with cross-holding structures, introduce an uncertainty that may lead promoters to make decisions that may not be fully aligned with minority shareholders.

For an investor, the key takeaway from this article is not about forming a buy, sell or hold view on the company. Instead, she should understand how such risk factors can affect long-term compounding. She should note that businesses operating in cyclical industries, with complex structures, often need a higher degree of due diligence.

In my own investment process, analyses like this serve as a filtering mechanism. Over time, avoiding situations where outcomes depend on multiple external or unpredictable factors can be as important as identifying high-quality opportunities. The objective is to focus on businesses where improved performance is due to sustainable competitive strengths in the business model instead of cyclical upturns in the industry.

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

I, Vijay Malik, am a SEBI-registered Research Analyst (Regn. No. INH100008364). This article is for educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.