The current section of the “Analysis” series covers Marine Electricals (India) Ltd, a leading Indian player in electrical solutions for marine/shipping and other industries. It specialises in power control and distribution equipment like switchboards, starters, power management systems etc. It also executes projects for data centres, automobiles etc. and has recently entered into the electric vehicle charging segment.

Please note that to get maximum benefit from this article, an investor should focus on the process of analysis instead of looking for good or bad aspects of the company. She should learn the interpretation of diverse types of data and transactions, and pay attention to the parts of annual reports etc., used to get the information. This will help her improve her stock analysis skills.

Marine Electricals (India) Ltd: Detailed Fundamental Analysis

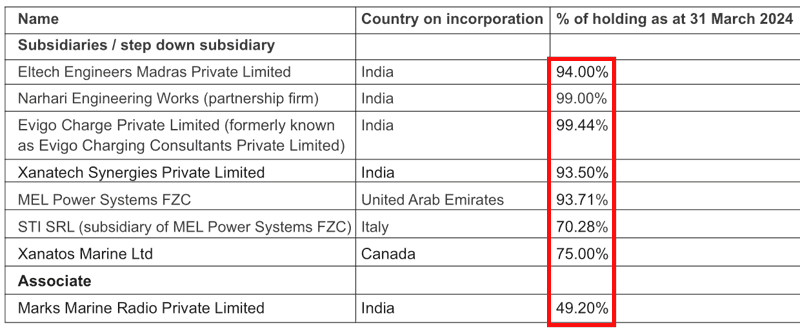

Over the years, Marine Electricals (India) Ltd has incorporated multiple subsidiaries, joint ventures and associate companies, both within India and overseas. As a result, it has reported both standalone as well as consolidated financials.

On June 30, 2025, the company had 8 subsidiaries, including 5 Indian and 3 foreign subsidiaries. Q1-FY2026 results, page 8:

Indian subsidiaries:

- Eltech Engineers Madras Private Limited

- Narhari Engineering Works

- Evigo Charge Private Limited

- Xanatech Synergies Private Limited

- Marks Marine Radio Private Limited

Foreign subsidiaries:

- MEL Power Systems FZC, UAE

- STI SRI, Italy

- Xanatos Marine Ltd, Canada

We believe that while analysing any company, an investor should always look at the company as a whole and focus on financials, which represent the business picture of the entire company, including its subsidiaries, joint ventures etc. Consolidated financials of a company present such a picture. Therefore, if a company reports both standalone as well as consolidated financials, then the investor should prefer the analysis of the consolidated financials of the company.

As a result, while analysing the past financial performance of Marine Electricals (India) Ltd, we have analysed its consolidated financials.

Further recommended reading: Standalone vs Consolidated Financials: A Complete Guide

With this background, let us analyse the financial performance of Marine Electricals (India) Ltd.

Financial and Business Analysis of Marine Electricals (India) Ltd:

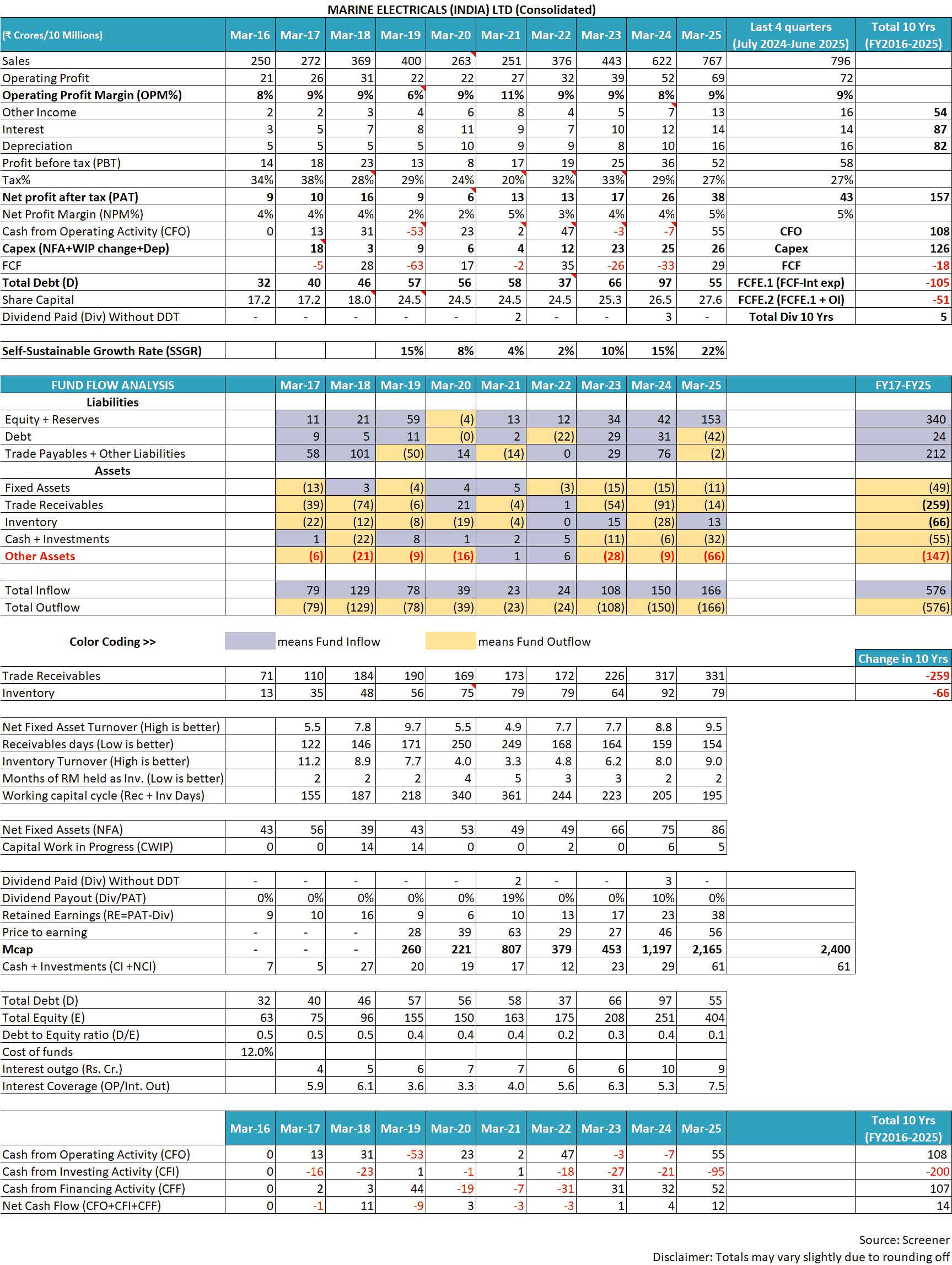

In the last 10 years (FY2016-FY2025), the sales of Marine Electricals (India) Ltd have increased at 13% year on year, from ₹250 cr in FY2015 to ₹767 cr in FY2025. Further, sales have increased to ₹796 cr in the 12 months ended June 2025, i.e. July 2024-June 2025.

Over the years, the operating profit margin (OPM) of Marine Electricals (India) Ltd has fluctuated in the range of 6% to 11%. In recent years, the company has reported an OPM of about 9%. The net profit margin (NPM) of the company has also shown similar sharp fluctuations and has fluctuated between 2% to 5%.

To understand more about Marine Electricals (India) Ltd along with fluctuations in its profit margins, an investor needs to read the publicly available documents of the company like its annual reports from FY2013 available on National Stock Exchange (NSE) website, red herring prospectus (RHP) of Sept 2018, credit rating reports from ICRA from 2020 and its corporate announcements submitted to NSE etc.

The above-mentioned documents show that the following key factors have influenced the business of Marine Electricals (India) Ltd, which are critical to understand for any investor.

1) Intense price-based competition faced by Marine Electricals (India) Ltd:

Both the operating segments of the company, marine as well as industrial, face intense price-based competition. The company faces competition from organised as well as unorganised, small as well as big players, domestic as well as international players in its business.

Red herring prospectus (RHP), September 2018, pages 26 and 111:

Competition emerges not only from the organized sector but also from the unorganized sector and from both small and big players.

We face competition from various local domestic and international players.

Marine Electricals (India) Ltd operates in an industry that faces rapid technological changes, and as a result, numerous large multinational companies with deep financial and technological strength dominate the industry and provide intense competition to smaller players.

Red herring prospectus (RHP), September 2018, pages 19, 26 and 89:

The industry we cater is characterized by rapid technological changes, evolving industry standards, changing client preferences that could result in product obsolescence and short product life cycles.

Some of our competitors include Siemens , L&T, Schindler etc.

Key players operating in the marine fully electric propulsion market include ABB Group, Rolls-Royce Plc, Wärtsilä, YANMAR CO., LTD., Caterpillar, Oceanvolt, and Hyundai Heavy Industries Co., Ltd.

As a result of such strong competitors, Marine Electricals (India) Ltd faces intense price-based competition where it has to offer low prices to win customers. If the company attempts to raise prices, then it faces a strong threat of losing its customers to its competitors.

Red herring prospectus (RHP), September 2018, pages 47-48:

Price is an important aspect…To remain aggressive and capitalize a good market share, we believe in offering competitive prices to our customers. This helps us to sustain the cut-throat competition and withhold a strong position in the market. Further it helps us to prevent loss in Company’s market share.

One of the major reasons for such intense price-based competition is that there are low barriers to entry in the industry, leading to many small players entering the industry and competing for market share.

Credit rating report by ICRA, January 2020, page 4:

industry segment remains intensely competitive due to the presence of many small and large players…the entry barriers within the marine segment remain low

Also read: How to do Business Analysis of a Company

2) Poor bargaining power of Marine Electricals (India) Ltd impacting profit margins:

Such industry conditions lead to low bargaining power of Marine Electricals (India) Ltd over its customers, which exposes it to volatile profit margins as seen in its historical financial performance. This is because, due to its weak negotiating position, the company is not able to pass on an increase in its input costs to its customers.

Credit rating report by ICRA, April 2025, page 3:

competition from established players and weak bargaining power with its reputed clientele limit MEIL’s ability to fully pass on the impact of raw material cost

Credit rating report by ICRA, April 2025, page 1:

competitive bidding process in the marine segment and stiff competition in the industry segment limit the company’s pricing flexibility.

Most of the company’s projects are fixed-price contracts, meaning that if, later on, its raw material prices increase, then Marine Electricals (India) Ltd has to take a hit on its profit margins as it can no longer pass on the increased costs to its customers.

Credit rating report by ICRA, April 2025, page 1:

delay could impact the revenues and profitability, given the largely fixed price nature of the contracts in the marine segment.

Due to its weak negotiating position, Marine Electricals (India) Ltd has to suffer even when the delay in projects is from the customers’ end.

Credit rating report by ICRA, April 2025, page 2:

delays in project execution from the customers’ end could defer revenue recognition for the company, thereby impacting profitability

Also read: How to analyse New Companies in Unknown Industries?

3) Loss of profits due to the weak ability of Marine Electricals (India) Ltd to timely recover money from its customers:

Very frequently, the company has faced difficulties in recovering money from its customers. As a result, it has reported long overdue receivables.

As per the latest available annual report of the company for FY2024, about ₹33 cr was overdue from its customers for more than 3 years.

FY2024 annual report, page 243:

An investor may note that these are undisputed receivables, meaning that the customer does not deny its obligation to pay them. However, still, the company has still not been able to collect them even after more than 3 years from their due date.

When companies are not able to collect money on time, then, invariably, some customers default on payments, which impacts the profitability of the company, as it is like doing work for free for the customer while spending money from its own pocket for raw material and labour.

In FY2024, the company reported bad debt of ₹6.33 cr (FY2024 annual report, page 224).

Due to the inability to recover money from customers on time, it has to raise funds from working capital finance from the bank, on which it has to pay interest, which further impacts its profit margins.

However, its requirement for funds for working capital is so much that beyond a point, lenders hesitate to give it loans, and then it has to dilute equity to raise money for funding its receivables/working capital.

In FY2019, Marine Electricals (India) Ltd came out with an initial public offer (IPO) in which about two-thirds of the money (₹32 cr out of the total IPO of ₹42.8 cr) was for working capital requirements (RHP, Sept 2018, page 77).

RHP, September 2018, page 19:

Our business is working capital intensive and hence, trade receivables form a substantial part of our current assets and net worth.

Credit rating report by ICRA, January 2020, page 2:

high working capital intensity of business emanating from the elongated receivables with the presence of sizeable debtors of over six months thereby exerting pressure on the company’s liquidity profile

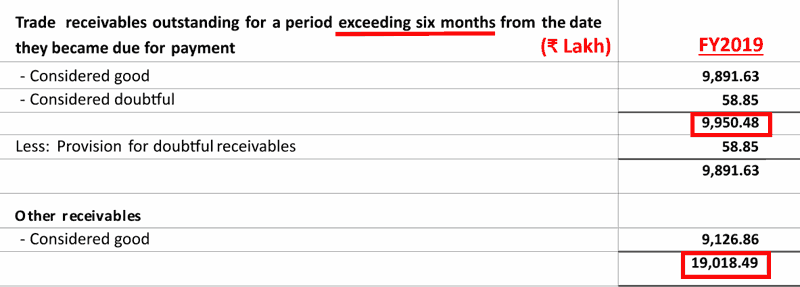

At the end of FY2019, the company had about ₹99.5 cr trade receivables outstanding for more than 6 months from their due date, which was more than half of the overall receivables of about ₹190 cr.

FY2019 annual report, page 120:

In FY2021, Marine Electricals (India) Ltd wrote off ₹5 cr of receivables as non-recoverable, i.e. bad debt (FY2021 annual report, page 211).

The company failed to properly assess the recovery of trade receivables in case of acquisitions as well.

In FY2022, the company acquired a 75% stake in a Canadian company, Xanatos Marine Ltd, for about ₹13 cr (USD 1,550,000).

FY2022 annual report, page 255:

Company has entered…to purchase 75 class “A” Common Shares…of Xanatos Marine Ltd…a Canadian Company…representing 75%…for a total consideration of USD 1,550,000

However, trade receivables of about CAD 164,000 (about ₹1.05 cr @₹63.79/CAD) that were outstanding at the time of acquisition could not be recovered until FY2025 and ultimately had to be written off.

Press release, Q3-FY2025 results, page 2:

In one of the overseas subsidiary, the company has written off one of the pre-acquisition debtors amounting to CAD 1.64 lakhs (Rs 1 crore)…despite continuous pertinent efforts were not recoverable

Such losses due to the inability to recover its trade receivables from customers impact the profitability of Marine Electricals (India) Ltd.

Further recommended reading: Receivable Days: A Complete Guide

4) Capital misallocation in the solar segment by Marine Electricals (India) Ltd:

Over the years, the company has lost a significant sum of money due to its decision to enter EPC (engineering, procurement and construction) work in solar energy.

In FY2017, Marine Electricals (India) Ltd got its first solar EPC order.

RHP, September 2018, page 122:

2017: Awarded order for 50MW Solar Power plant EPC by NLC India Ltd.

The project was expected to be completed within 23 months from allotment (February 28, 2017), i.e. by January 31, 2019. (Source: NLCIndia.in report, page 10)

However, even after 6 years, the company could not deliver the project, and in 2023, NLC India had to reopen the project for other bidders (Source: NLC India Invites Online Bids for BOS Works of 50 MW Solar Power Project in Neyveli: Solarquarter.com, June 7, 2023)

During the period of this long delay, Marine Electricals (India) Ltd reported continuous losses in its solar segment.

- FY2019: loss of ₹5.77 cr (FY2019 annual report, page 130)

- FY2020: loss of ₹6.87 cr (FY2021 annual report, page 220)

- FY2021: loss of ₹4.88 cr (FY2021 annual report, page 220)

- FY2022: loss of ₹3.93 cr (FY2023 annual report, page 242)

- FY2023: loss of ₹2.23 cr (FY2023 annual report, page 242)

During FY2019 and FY2020, when the company’s profit after tax declined to ₹6 cr in FY2020 from ₹16 cr in FY2018, the main reason was the losses from the solar division.

Investor presentation, February 2021, page 25:

In FY 19 & 20, drop in earnings mainly due to Solar Segment registered net Loss of Rs. 59 mn & Rs. 52 mn respectively

Over FY2019-FY2023, the company reported losses of about ₹23.68 cr as detailed above. After FY2023, Marine Electricals (India) Ltd stopped reporting solar as a separate segment and decided to exit the solar business.

Credit rating report by ICRA, January 2022, page 1:

ICRA notes the company’s exit from the loss-making solar segment

Also read: Credit Rating Reports: A Complete Guide for Stock Investors

Even though the company had decided to exit from the solar segment, its problems did not end there.

For the NLC India project, it had subcontracted its work to GE Power Conversion (India) Pvt Ltd (GE Power). Later on, GE Power claimed that Marine Electricals (India) Ltd did not fulfil its obligations according to their contract and asked for damages.

In August 2024, GE Power won the arbitration, and the arbitrator directed Marine Electricals (India) Ltd to pay ₹21.34 cr plus interest to GE Power.

Credit rating report by ICRA, August 14, 2024, page 1:

As per the award, MEIL has been directed to pay an amount of Rs. 21.34 crore plus interest to GE Power Conversion Limited (GEPC). The dispute is related to a 50-MW solar power project (awarded to MEIL by NLC India Ltd.), which was sub-contracted to GEPC.

Acknowledging the award, the company paid out about ₹1.4 cr to GE Power in November 2024 and filed an appeal in the Bombay High Court.

Q2-FY2025 results, page 16:

The Company have admitted part claim of Rs 85.37 lakhs and have paid the admitted amount along with interest of RS 55.10 lakhs on 06 November 2024…the Company has subsequently filed application with the Bombay High Court on 24 October 2024 to set aside the arbitration award and the outcome is awaited.

By June 30, 2025, Marine Electricals (India) Ltd has provided for a total of about ₹12.9 cr towards this award.

Q1-FY2026 results, page 13:

Company has made a prudent provision of Rs 216.91 Lakhs and Rs. 1,077.51 lakhs during the quarter ended 30 June 2025 and during year ended 31 March 2025 respectively.

If the Bombay High Court also decides the case against the company, then it will have to bear this significant loss on payments to be made to GE Power.

As if the losses in the solar division and the significant award were not sufficient, Marine Electricals (India) Ltd also lost about ₹5.84 cr that it had paid to a Chinese supplier for purchasing solar modules. The Chinese supplier neither provided the solar modules nor returned the money.

FY2024 annual report, page 104:

Company had paid an advance of USD 8,00,000 to a supplier in China during the financial year 2017-18 for procurement of solar PV modules…Company has determined that the said advance is no longer recoverable and the entire amount of Rs 584.48 lakhs have been charged to standalone statement of profit and loss

It seems a case of poor vendor/supplier selection by the company that impacted the shareholders.

Moreover, poor execution of projects by the company is not limited to the solar division. In the past, as per RHP, the company faced delays in project execution and had to pay penalties/liquidated damages to its customers.

RHP, September 2018, page 18:

In the past, we have been required to re – negotiate some of the terms such as price, date of delivery and scope of work of our contracts due to a delay in delivering the product owing to a combination of internal as well as external factors beyond our control. We were also required to pay liquidated damages for such delays.

In FY2022, the GST department asked the company to pay ₹1.20 cr for GST on bank guarantee invocation.

FY2023 annual report, page 248:

During the previous year, pursuant to inspection by GST Department, the Company paid Rs. 120.14 lakhs towards GST on bank guarantee invocation.

Normally, in the business of Marine Electricals (India) Ltd, a bank guarantee is invoked by a customer when the supplier does not meet its obligations. In this case, it might be any shortcoming by Marine Electricals (India) Ltd in project execution that might have led to its customer invoking the bank guarantee.

An investor may contact the company directly to get clarifications about this bank guarantee invocation and whether it was due to any poor project execution by Marine Electricals (India) Ltd.

Going ahead, an investor should keep a close watch on timely project execution by Marine Electricals (India) Ltd as any delays will impact is profitability.

Also read: How to Identify if Management is Misallocating Capital

5) Capital mis-allocation in the EV (electrical vehicles) segment by Marine Electricals (India) Ltd:

The company entered the EV charging segment in FY2021 when it acquired a 74% stake in Evigo Charging Consultants Private Limited (FY2021 annual report, page 227).

- In FY2021, Evigo reported a loss of ₹0.13 cr (FY2021 annual report, page 228).

- In FY2022, Evigo reported a loss of ₹0.43 cr (FY2022 annual report, page 250).

- In FY2023, Evigo reported a loss of ₹3.30 cr (FY2023 annual report, page 250).

- In FY2024, Evigo reported a loss of ₹5.37 cr (FY2024 annual report, page 240).

Marine Electricals (India) Ltd is yet to publish its FY2025 annual report. When the same is available, then the investor should check the financial performance of Evigo.

Since FY2021, Evigo has continuously made losses and has needed more capital to run and expand its operations. However, it seems that Marine Electricals (India) Ltd is the party that is providing this capital, and the other entities that held a 26% stake are not. It is visible from the fact that additional capital infusion by Marine Electricals (India) Ltd has increased its stake in Evigo from 74% in FY2021 to 99.44% in FY2025.

For example, in FY2023, Marine Electricals (India) Ltd infused ₹1 cr in Evigo, and its shareholding increased to 98.88%.

FY2023 annual report, page 144:

Post the allotment of shares pursuant to conversion of CCPS, the shareholding of the Company in Evigo has increased from 71.04% to 98.88%.

In FY2024, Marine Electricals (India) Ltd converted its loan of ₹1.02 cr to Evigo into equity, and its shareholding further increased to 99.44%.

FY2024 annual report, page 139:

Post the allotment of shares pursuant to conversion of loan, the shareholding of the Company in Evigo has increased from 98.88% to 99.44%.

In this instance, conversion of the loan of ₹1.02 cr led to an increase in shareholding of Marine Electricals (India) Ltd by 0.56% (= 99.44 – 98.88), implying that the company is assigning a total valuation of ₹182 cr to Evigo (= 1.02 / 0.56%).

In October 2024, Evigo gave away 11.75% stake in it, which should be valued at about ₹21.39 cr (= 182 * 11.75%), to other entities, only for ₹0.23 cr (₹22.77 lac) by allotting them sweat equity of 277,000 shares at ₹10 per share. As a result, the stake of Marine Electricals (India) Ltd in Evigo declined from 99.44% to 87.69%.

Q3-FY2025 results, page 5:

On 17 October 2024…Evigo Charge Private Limited (“Evigo”), has considered and approved allotment of 2,77,000 Equity Shares of face value of Rs. 10 each as sweat equity at Rs. 10 per share which resulted in dilution of holding of the company in Evigo from 99.44% to 87.69%.

So, on Oct. 17, 2024, Evigo gave away 11.75% stake, which ideally should have been valued at ₹21.39 cr, to other entities for only ₹0.23 cr. indicating a total value of ₹1.95 cr (=0.23 / 11.75%).

Moreover, within a couple of months, in December 2024, Evigo again converted a loan of ₹1.12 cr (₹111.84 lakh) given by Marine Electricals (India) Ltd into shares, which resulted in an increase of shareholding of the company in Evigo by 3.985% i.e. from 87.69% to 91.675%. At this time, Evigo was valued at ₹28.10 cr (= 1.12 / 3.985%).

Q3-FY2025 results, page 5:

on 24 December 2024 Board of Directors of a Evigo, has considered and approved allotment of 11,18,382 Equity Shares…by conversion of loan (including interest) amounting to Rs. 111.84 lakhs given by the Company to Evigo. Past the allotment of shares pursuant to conversion of loan, the shareholding of the Company in Evigo has increased from 87.69% to 91.675%.

After the above analysis, an investor is left with interesting observations that:

- Whenever Evigo needs money for business/expansion, it is Marine Electricals (India) Ltd that has to contribute and get allotment of shares at very high valuations of ₹182 cr (FY2024), ₹28 cr (Dec. 2024) etc.

- Whereas other entities that don’t even support Evigo with funds infusion are given sweat equity at very low valuations, like ₹2 cr (Oct. 2024).

Moreover, Evigo is making these significant changes in its valuation within a very short period of time: ₹182 cr (FY2024) to ₹2 cr (Oct. 2024) to ₹28 cr (Dec. 2024).

An investor may contact the company directly to understand why Evigo has changed its valuation so sharply and who these other entities are to whom Evigo has allotted stake at very low valuations.

Also read: Why Management Assessment is the Most Critical Factor in Stock Investing?

6) Steps taken by Marine Electricals (India) Ltd to protect its profit margins:

To minimise the impact of an increase in raw material prices on its profitability, the company tries to purchase material only when it wins a contract, i.e., a back-to-back arrangement.

Credit rating report by ICRA, April 2025, page 3:

company enters into back-to-back arrangements with its suppliers

In addition, the company tried to focus on research & development (R&D) to improve its products to gain negotiating power over its customers.

In FY2017, Marine Electricals (India) Ltd set up an R&D unit in Mumbai and in FY2018, another R&D unit in Kochi.

FY2017 annual report, page 6

Your Company has set up Research and Development facilities in Mumbai

FY2018 annual report, page 7:

Your company has in addition to R&D facility in Mumbai started a R&D facility in Kochi

Marine Electricals (India) Ltd does not disclose the expense/cost incurred by it on R&D in its annual report. In the absence of an assessment of R&D costs as a percentage of revenue, an investor is not able to assess how much focus the company has on R&D.

An investor may contact the company directly to get clarifications about its annual R&D expense.

Intense price-based competition, inability to pass on an increase in input costs to customers, and losses due to capital misallocations are some of the reasons that have impacted Marine Electricals (India) Ltd and led to volatility in its business performance.

Going ahead, an investor should keep a close watch on the profit margins of the company.

Over the last 10 years (FY2016-FY2025), the tax payout ratio of Marine Electricals (India) Ltd has largely been in line with the standard corporate tax rate in India except during a few years when deferred taxes (FY2018), impact of shifting to new tax regime (FY2021) and tax adjustments of earlier years (FY2022) affected its tax payout ratio.

Also read: How to do Financial Analysis of a Company

Operating Efficiency Analysis of Marine Electricals (India) Ltd:

a) Net fixed asset turnover (NFAT) of Marine Electricals (India) Ltd:

Over the years, NFAT of the company has increased from 5.5 in FY2017 to 9.5 in FY2025. The NFAT declined in FY2020-FY2021 to reach 4.9 in FY2021, which was due to mainly due to poor performance in the solar segment.

After exiting the solar segment, the company has improved its asset utilisation, and its NFAT has increased from 4.9 in FY2021 to 9.5 in FY2025.

Going ahead, an investor should keep a close watch on the fixed asset turnover levels of the company to assess whether it is able to optimally utilise its manufacturing assets.

Further advised reading: Asset Turnover Ratio: A Complete Guide for Investors

b) Inventory turnover ratio (ITR) of Marine Electricals (India) Ltd:

Over the years, the inventory turnover ratio of the company has also fluctuated in line with its NFAT. ITR used to be 11.2 in FY2017, which deteriorated to 3.3 in FY2021 primarily due to long delays in the execution of its solar EPC project for NLC India Ltd.

After exiting the solar division, Marine Electricals (India) Ltd has seen its ITR improve to 9.0 in FY2025.

Going ahead, an investor should keep a close watch on the inventory position of the company to understand whether it is able to keep its working capital situation under control or not.

Further advised reading: Inventory Turnover Ratio: A Complete Guide

c) Analysis of receivables days of Marine Electricals (India) Ltd:

Over the years, receivables days for the company have deteriorated from 122 days in FY2017 to 154 days in FY2025. The company saw its receivables days extend to 250 days in FY2020 when due to its poor execution of NLC India’s solar project, a large sum of receivables was stuck.

Credit rating report by ICRA, January 2020, pages 2-3:

high working capital intensity of business emanating from the elongated receivables with the presence of sizeable debtors of over six months thereby exerting pressure on the company’s liquidity profile…There has been a considerable delay in execution of Rs. 198.49 crore solar EPC project for NLC India Limited.

As discussed earlier, Marine Electricals (India) Ltd has faced situations where a large sum of receivables was overdue for more than 3 years.

Inability to collect receivables on time has forced the company to repeatedly dilute its equity to raise money to pay its suppliers and keep running its business.

In FY2019, it raised about ₹48 cr in IPO out of which about ₹32 cr was for funding its working capital, which it primarily used to repay its trade payables of ₹29.76 cr (FY2019 annual report, page 101).

Thereafter, in FY2022, it raised ₹29.25 cr via allotment of warrants, which was to meet long-term working capital.

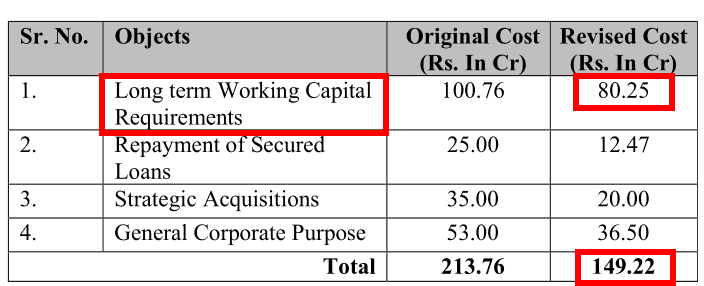

In FY2025, it raised about ₹149.22 cr via preferential allotment of equity shares and warrants, out of which ₹80.25 cr is for long-term working capital.

Corporate announcement to NSE, November 13, 2024:

Marine Electricals (India) Ltd has been continuously raising money via equity dilution to run its business. Moreover, in FY2026, the company is planning to raise further ₹30 cr.

Credit rating report by ICRA, April 2025, page 2:

company raised over Rs. 145 crore over FY2023-FY2025, with another ~Rs. 30 crore expected in FY2026, primarily to fund the capital expenditure (capex) and working capital requirements

Going ahead, an investor should watch the trend of receivables days of Marine Electricals (India) Ltd to assess whether it is able to collect its receivables on time to run its business from its business/operating cash flows, or it continues to dilute equity to meet its day-to-day funding needs.

Further recommended reading: Receivable Days: A Complete Guide

When an investor compares the cumulative net profit after tax (cPAT) and cumulative cash flow from operations (cCFO) of Marine Electricals (India) Ltd for FY2016-FY2025, then she notices that over the years (FY2016-FY2025), the company is not able to convert its profit into cash flow from operations.

Over FY2016-25, Marine Electricals (India) Ltd reported a total cumulative profit after tax (cPAT) of ₹157 cr. During the same period, it reported a cumulative cash flow from operations (cCFO) of ₹108 cr.

It is advised that investors should read the article on CFO calculation, which would help them understand the situations in which companies tend to have the CFO lower than their PAT. In addition, the investors would also understand the situations when the companies would have their CFO higher than PAT.

Further recommended reading: Understanding Cash Flow from Operations (CFO)

The Margin of Safety in the Business of Marine Electricals (India) Ltd:

a) Self-Sustainable Growth Rate (SSGR):

Read: Self Sustainable Growth Rate: a measure of Inherent Growth Potential of a Company

Upon reading the SSGR article, an investor would appreciate that if a company is growing at a rate equal to or less than the SSGR and it can convert its profits into cash flow from operations, then it would be able to fund its growth from its internal resources without the need for external sources of funds.

Conversely, if any company attempts to grow its sales at a rate higher than its SSGR, then its internal resources would not be sufficient to fund its growth aspirations. As a result, the company would have to rely on additional sources of funds, like debt or equity dilution, to meet the cash requirements to generate its target growth.

An investor may calculate the SSGR using the following formula:

SSGR = NFAT * NPM * (1-DPR) – Dep

Where,

- SSGR = Self Sustainable Growth Rate in %

- Dep = Depreciation rate as a % of net fixed assets

- NFAT = Net fixed asset turnover (Sales/average net fixed assets over the year)

- NPM = Net profit margin as % of sales

- DPR = Dividend paid as % of net profit after tax

(For systematic algebraic calculation of SSGR formula: Click Here)

Over the years, the SSGR of Marine Electricals (India) Ltd has been highly fluctuating between 2% to 22%. This is because the company faced sharp fluctuations in its NFAT and NPM due to the poor performance of its solar division.

Nevertheless, the average of SSGR of all the reported years from FY2019 to FY2025 is about 11% whereas during the last 10 years, the company has grown at a pace of 13% year on year.

In addition, companies with working capital-intensive businesses that are not able to convert their PAT into CFO need to raise debt to meet their growth requirements, even though their SSGR is higher than sales growth, because the SSGR formula factors in NPM without factoring in its conversion into CFO.

The situation becomes further clear when an investor does a free cash flow analysis of Marine Electricals (India) Ltd.

b) Free Cash Flow (FCF) Analysis of Marine Electricals (India) Ltd:

While looking at the cash flow performance of Marine Electricals (India) Ltd, an investor notices that during FY2016-FY2025, it generated a cash flow from operations of ₹108 cr. During the same period, it made a capital expenditure of about ₹126 cr.

Therefore, during this period (FY2016-FY2025), Marine Electricals (India) Ltd had a negative free cash flow (FCF) of (₹18) cr (= 108 – 126).

In addition, during this period, the company had a non-operating income of ₹54 cr and an interest expense of ₹87 cr. As a result, the company had a total negative free cash flow of (₹51) cr (= – 18 + 54 – 87). Please note that the capitalised interest is already factored in as part of the capex deducted earlier.

In order to meet this shortfall, Marine Electricals (India) Ltd relied on both debt as well as equity dilution.

Over FY2016-FY2025, the company raised additional debt of ₹23 cr as its total debt increased from ₹32 cr in FY2016 to ₹55 cr in FY2025.

In addition, as discussed earlier, during this period, it raised money of about ₹225 cr by diluting equity by IPO (FY2019: ₹48 cr), warrants (FY2022: ₹29 cr), and preferential allotment of shares and warrants (FY2025: 149 cr).

Going ahead, an investor should keep a close watch on the cash flow position of Marine Electricals (India) Ltd to understand whether the company is able to generate surplus cash from its business or it keeps on relying on outside funds for growth and running its day-to-day operations.

Further recommended reading: Free Cash Flow: A Complete Guide to Understanding FCF

Self-Sustainable Growth Rate (SSGR) and free cash flow (FCF) are the main pillars of assessing the margin of safety in the business model of any company.

Further advised reading: 3 Simple Ways to Assess “Margin of Safety”: The Cornerstone of Stock Investing

Additional aspects of Marine Electricals (India) Ltd:

On analysing Marine Electricals (India) Ltd and after reading annual reports, credit rating reports and other public documents, an investor comes across certain other aspects of the company, which are important for any investor to know while making an investment decision.

1) Management Succession of Marine Electricals (India) Ltd:

The company is run by brothers Mr Vinay Uchil (Chairman, age 54 years) and Mr Venkatesh Uchil (Managing Director, age 47 years).

As per related party transactions details in the FY2024 annual report, the company paid a total of ₹18 lakh to Ms. Rashmi Uchil, wife of Mr Vinay Uchil, which included professional fees of ₹9 lakh and rent payment of ₹9 lakh.

Other than these members of the promoter family, there are no details of any member from the next generation presently working in the company.

As per the RHP filed by the company for its IPO in 2018, Mr Vinay Uchil has a son, Master. Dhairyash Vinay Uchil and Mr. Venkatesh Uchil has two daughters, Ms. Devashree Venkatesh Uchil and Ms. Jaanvi Venkatesh Uchil. (RHP, September 2018, pages 150-151).

It has been 7 years since Marine Electricals (India) Ltd came out with its IPO; however, it seems that until now, none of the members of the next generation have joined the family business.

An investor may contact the company directly to understand more about the succession planning of the promoters.

The presence of a well-thought-out management succession plan is essential in the case of promoter-run businesses, as it provides for a smooth transition of leadership over the generations and provides continuity in the business operations of any company. Moreover, if the next generation joins the business in active roles while the older generation is still active, then it allows them a good time to learn the business under able guidance.

Further advised reading: How to do Management Analysis of Companies?

2) Frequent resignations of key personnel: CFO and Company Secretary:

Ever since Marine Electricals (India) Ltd came out with its IPO in 2018, it has seen frequent resignations of important personnel.

For example, at the position of chief financial officer (CFO), it has had the following people:

- Rohit Shetty: from August 3, 2018, to October 19, 2019

- Aditya Desai: from November 14, 2019, to June 24, 2020

- Namita Sethia: from July 30, 2020, to July 30, 2022

- U. M. Bhakthavalsalan from August 4, 2022, to January 16, 2025

- Mr Sunil Kumar Dalmia from January 16, 2025

During the same period, Marine Electricals (India) Ltd has had the following people as company secretary cum compliance officer:

- Sudhir Gupta: from August 1, 2018, to November 16, 2018

- Veedashri Chaudhari from December 7, 2018, to May 23, 2019

- Reesha Ratanpal from July 20, 2019, to February 26, 2021

- Mitali Ambre from February 27, 2021, to December 13, 2023

- Deep Shah from February 14, 2024

An investor would note that when people do not wish to continue in positions like CFO and company secretary/compliance officer for long in any company, then she should increase her level of due diligence in the company.

Also read: Why We cannot always Trust What Management Claims

3) Marine Electricals (India) Ltd always leaves a small shareholding in its subsidiaries for other entities:

An investor notes that the company has never formed a wholly-owned subsidiary for any of its business initiatives. It has always brought in other entities as minority shareholders. A look at the list of subsidiaries of the company at March 31, 2024, from the FY2024 annual report, page 180, will confirm it.

From the earlier discussion on Evigo Charge Private Limited, an investor would remember that the presence of other minority shareholders in subsidiaries opens up the possibilities of shifting of economic benefits from minority shareholders of the listed/parent entity to minority shareholders of the subsidiary. It happens if the subsidiary company sells a stake to the parent at a higher valuation and then sells the stake to its other minority entities at a lower valuation.

Such minority shareholdings in subsidiaries become curious situations when they belong to the promoters of the parent/listed company.

For example, take the case of Athmar India Private Limited (Athmar).

On February 7, 2024, Marine Electricals (India) Ltd incorporated Athmar and took a 50% shareholding in it.

FY2024 annual report, page 248:

Company has incorporated a company named as Athmar India Private Limited (“Athmar”) on 07 February 2024 and has subscribed 5,000 equity shares…comprising 50% stake…As at 31 March 2024, Athmar is yet to commence its business operations.

Thereafter, in August 2024, the company entered into a memorandum of understanding (MoU) with Cummins India Ltd to jointly supply, commission, and service marine power and propulsion solutions for the Indian Navy and private ship owners.

Corporate announcement to NSE, August 13, 2024:

(MEIL) has entered into a MOU with M/s. Cummins India Limited…for facilitating Supply, Commissioning and after Sales Services in the specific areas , Diesel Generator Sets or Integrated Propulsion and Power Generation Solutions with Conventional or Diesel-Electric Configuration for the Indian Navy in particular besides Private Ship Owners.

However, in the same announcement, Marine Electricals (India) Ltd also declared that Athmar India Private Limited (Athmar) is also a part of this MoU.

Corporate announcement to NSE, August 13, 2024:

M/s Athmer India Private Limited, an associate of Marine Electricals India ltd, also is participating in this MOU

Thereafter, in February 2025, the company sold its 50% stake in Athmar to its promoters, Mr Vinay Uchil.

Q3-FY2025 results, pages 1 and 11:

Approved divestment of 50% of equity investment…of Athmar India Private Limited…Post the Proposed Transaction, Athmar India Private Limited will cease to be associated of the Company

Yes, buyers belong to the Promoter. Mr Vinay Uchil is Promoter and Director of the Marine Electricals (India) Limited.

When an investor looks at this whole transaction, it seems like the listed company formed an associate company, helped it to enter into an MOU with a reputed company like Cummins India Ltd and then sold its stake to the promoters. When an investor notices that promoters are the guiding force that decides most of the decisions of any listed company, then such a transaction seems like the promoters themselves made the listed entity sell its stake in Athmar to themselves.

An investor may contact the company directly to understand the reasons why it sold its stake in Athmar to promoters and what benefits this sale brings to the minority shareholders of Marine Electricals (India) Ltd.

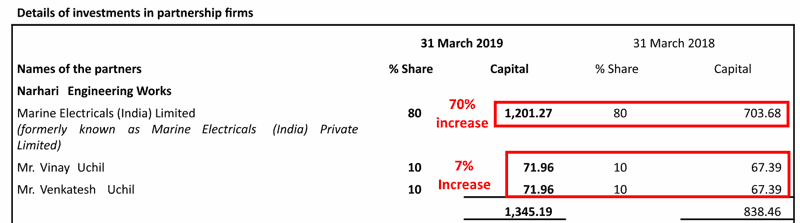

Let us take another example of a partnership firm, Narhari Engineering Works, which Marine Electricals (India) Ltd has formed with promoters. The company has an 80% share of the partnership, and promoters Mr Vinay Uchil and Mr Venkatesh Uchil have 10% share each.

An investor may note that, as discussed earlier in the case of Evigo Charge Pvt. Ltd, in such partnership structures as well, most of the time, the listed company ends up providing most of the funding requirements.

Take, for example, in FY2019, in Narhari Engineering Works, the capital contribution/share of Marine Electricals (India) Ltd increased much more (70%) than its promoters (7%), whereas the profit sharing stayed the same at 80:10:10.

FY2019 annual report, page 79:

So, effectively, in such structures, the minority shareholders of the listed company end up funding a large share of the monetary requirements of the partnership firm, whereas the promoters in their personal capacity continue to enjoy a fixed profit/benefit share from the partnership firm without proportionate capital contribution.

In FY2023, the company purchased 19% additional share of Narhari Engineering from promoters by paying ₹1.98 cr. However, promoters still kept 1% stake with themselves.

FY2023 annual report, page 144:

Company has increased its % holding in its Subsidiary, Narhari Engineering Works, a partnership firm, by way of further acquisition of 19% holding from the existing partners for a consideration of Rs 197.93 lakhs

Whenever an investor notices that a company is establishing new entities/subsidiaries with less than 100% shareholding and the other entity holding the remaining stake is not a well-known company joining as a joint venture partner, then the investor should be cautious. She should increase her due diligence because if the other minority shareholders are promoters, then it provides a route for shifting of economic benefits from public shareholders of the listed company to promoters.

An investor may contact the company directly to get clarification about the minority shareholders of all the subsidiaries of the company. She should try to ascertain/rule out whether these entities are promoters or their friends and family.

Also read: Why Management Assessment is the Most Critical Factor in Stock Investing?

4) Related party transactions of Marine Electricals (India) Ltd with promoter entities:

Over the years, the company has entered into numerous transactions with multiple promoter entities, where each such transaction opens up the possibility of shifting economic benefits from public shareholders to promoters.

For example, every year, Marine Electricals (India) Ltd pays rent of a significant amount to promoter entities. In FY2024, it paid a rent of about ₹3.3 cr to related parties (FY2024 annual report, page 231).

Similarly, numerous promoter entities operate in related businesses of Marine Electricals (India) Ltd and, in turn, enter into sale and purchase transactions with the company.

For example, in FY2024, the company made purchases of about ₹3 cr and sales of about ₹2.9 cr to related parties (FY2024 annual report, page 231).

An investor may note that each of such sale/purchase transactions provides an opportunity for shifting of economic benefit from public shareholders to promoters if the listed company buys goods/services from promoter entities at a price higher than their market price or sells goods/services to promoter entities at a price lower than their market price. Therefore, an investor should always do deeper due diligence of such sale/purchase transactions with related parties.

In FY2022, Marine Electricals (India) Ltd wrote off ₹5.81 lakh as bad debt from a related party, KDU Worldwide Technical Services Ghana Private Limited (FY2022 annual report, page 240). This is similar to a promoter entity taking goods from the listed entity and not paying for them.

At times, the company has given advances to promoter entities, which have stayed outstanding for multiple years, even though the name of the said promoter entity did not figure under the purchases made by the company.

For example, DKM Precision Engineers, a partnership firm in which promoters are partners. Marine Electricals (India) Ltd gave an advance of ₹3 cr to DKM Precision Engineers in FY2019 under the heading “Advance to suppliers” (FY2019 annual report, page 129).

Marine Electricals (India) Ltd did not disclose any purchases from DKM Precision Engineers in FY2019 or FY2020 or FY2021, or FY2022 (Source: FY2019 annual report, page 128; FY2020 annual report, page 102; FY2021 annual report, page 143; FY2022 annual report, page 168).

During these four years, the advance of ₹3 cr was continuously outstanding from DKM Precision Engineers without any purchase.

In FY2022, DKM Precision Engineers repaid the advance money of ₹3 cr (FY2022 annual report, page 168).

This transaction might seem like a case where the promoter entity, DKM Precision Engineers, used Marine Electricals (India) Ltd as a lender to give it an interest-free loan that it used for almost 4 years.

In another instance, Marine Electricals (India) Ltd made payments on behalf of related parties, and the secretarial auditor of the company highlighted it in its report to shareholders.

FY2020 annual report, page 52:

The Company has made on account payments on behalf of related parties being private limited Companies and Partnership firms, wherein directors are interested.

Such transactions have the potential of shifting economic benefits from public shareholders to promoters.

An investor should do a deeper due diligence of such transactions, especially in cases like Marine Electricals (India) Ltd, where the companies face continuous funds deficit due to their working capital-intensive business and inability to recover trade receivables on time.

So, on the one hand, such companies have to raise debt and dilute equity to raise money to run their business, and on the other hand, they end up giving the precious money to promoter entities as interest-free loans/advances.

Also read: How Promoters benefit from Related Party Transactions

5) More instances of capital misallocation by Marine Electricals (India) Ltd:

5.1) Dividends funded by debt and equity dilution:

Due to a working capital-intensive business model and inability to timely collect money from customers, Marine Electricals (India) Ltd has faced a continuous liquidity crunch. As a result, it had to continuously raise money by additional debt and equity dilution, as we discussed earlier.

However, despite such liquidity constraints, the company declared dividends for FY2021, FY2024, and FY2025. This is despite the company diluting its equity multiple times via IPO, warrants, preferential allotment of shares etc. to meet working capital requirements.

Moreover, as per the credit rating report of ICRA, April 2025, Marine Electricals (India) Ltd plans to raise further ₹30 cr via equity dilution in FY2026.

5.2) Blocking capital in property given on rent to others, whereas raising money by debt and equity dilution to run its business:

Marine Electricals (India) Ltd owns a building (investment property), which had a market value of ₹29 cr in FY2023 and is valued at the ready reckoner rate at ₹23.3 cr in FY2024 (market price might be higher than this).

The company has given this property on rent to others instead of using this capital, which is currently blocked in a non-operating activity.

FY2024 annual report, page 208:

Investment property comprise of a commercial building that is leased to third party…As at 31 March 2024, the fair value of the property has been updated to Rs. 2,327.60 lakhs…previous year’s fair value of Rs. 2,917.04 lakhs.

fair value of the Group’s investment property has been determined using the ready reckoner rate published by local municipal authorities, rather than an independent valuation report

As per the FY2024 annual report, page 222, Marine Electricals (India) Ltd earned a rental income of ₹2.01 cr in FY2024.

As per the related party transactions details of FY2024, the company received a rental income of ₹24 lakh from a related party Switch N Control Gears Private Limited (FY2024 annual report, page 238).

An investor may contact the company directly to understand why it continues to dilute its equity and raise more debt while about ₹25-30 cr of its capital is blocked in a commercial property, which it can free up to infuse in the business.

Also read: Are professionally managed companies safer for shareholders?

6) Acquisitions done by Marine Electricals (India) Ltd:

6.1) Property acquired by the company is under dispute:

In FY2023, in an auction, Marine Electricals (India) Ltd purchased a property, “factory premises situated in Mumbai consisting of land and building” owned by Ciemme Jewels Limited, facing bankruptcy resolution proceedings under IBC (Insolvency and Bankruptcy Code) (Source).

The company paid a total of ₹13.4 cr to acquire the property. However, this auction came under dispute and all the forums: NCLT, NCLAT and Supreme Court ruled against the acquisition of the property by Marine Electricals (India) Ltd.

FY2024 annual report, page 172:

During the previous year, the Company became successful bidder in the e-auction…consideration paid by the Company amounted to Rs 1,160.00 lakhs and also incurred other expenditures amounting to Rs 177.80 lakhs…was challenged by another unsuccessful bidder…NCLT…was set aside by NCLT…the decision of NCLT was upheld by NCLAT and Supreme Court.

Now, the company is asked to vacate the factory premises, and Marine Electricals (India) Ltd is asking for a refund of ₹13.4 cr paid by it. However, the company plans to fight to retain the property.

FY2024 annual report, page 172:

Company filed a reply in response to the liquidator’s request to vacate the premises, seeking refund of the entire consideration paid and expenditure incurred if the premise is to be vacated, while the Company still aims to retain the ownership.

An investor would appreciate that legal and administrative proceedings might involve significant delays. She should keep a close watch on this matter as ₹13.4 cr is a significant sum of money for the company, and if this money is stuck unproductively, then it will have a detrimental impact on the liquidity position of the company.

6.2) Acquisition of Xanatos Marine Ltd, Canada, by the company:

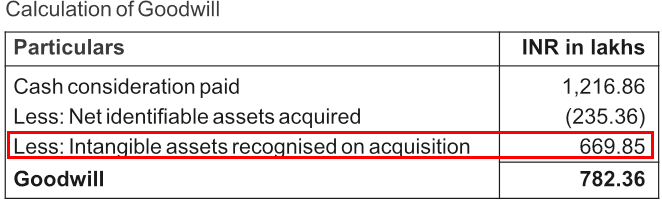

In FY2024, Marine Electricals (India) Ltd acquired a 75% stake in Xanatos Marine Ltd (Xanatos), a Canada-based company providing vessel traffic services on ports and coasts for USD 1.55 million (₹12.17 cr.)

Xanatos has been in a very poor financial condition with negligible sales and is making losses.

FY2024 annual report, page 247:

Xanatos had reported revenue of Rs Nil and loss after tax of Rs 35.16 lakhs from the date of acquisition till 31 March 2023. Had the entity been acquired from 1 April 2022, they would have reported revenue of Rs 26.18 lakhs and loss after tax of Rs 108.01 lakhs during F.Y. 2022-23.

At the time of acquisition, Xanatos had a negative value of identifiable assets of (₹2.35 cr). In addition, as per earlier discussion, an investor would note that subsequently, a debtor refused to pay about ₹1 cr to the company (bad debt written off).

The only value that Marine Electricals (India) Ltd got on acquisition was intangible assets of ₹6.7 cr.

FY2024 annual report, page 247:

The intangible assets pertain to the TITAN software platform used for managing vessel traffic for ports etc.

FY2024 annual report, page 71:

Marine Electricals offers two such systems…a) TITAN SENTINEL…b) TITAN AVIPS…Marine solutions software is acquired from Xanatos, Canada with complete Transfer of Technology (ToT) and know-how.

So, effectively, Marine Electricals (India) Ltd acquired TITAN software for ₹12.17 cr. and plans to use it to provide vessel traffic solutions to ports.

However, when an investor tries to find out why Xanatos despite developing TITAN software reached a stage of bankruptcy with negative identified assets, very negligible revenue and net losses, then she notices that winning orders for vessel traffic solution from ports/coast guard involves intense competition from very large global players like Lockheed Martin, Saab AB, BAE Systems, Thales, Northrop Grumman, Elbit Systems Ltd (Sources: 1, 2).

Winning such orders from ports and the coast guard involves a long project cycle, and the inability to continuously win newer clients/contracts would have contributed to the financial decline of Xanatos.

Such software solutions require a continuous large investment in upgrading and maintaining them. If a company is not able to dedicate a significant sum of money towards such software, then the solution faces the risk of becoming outdated and getting ignored for future orders/tenders.

Therefore, an investor should keep a close watch on Marine Electricals (India) Ltd’s development of TITAN software and whether it is able to win orders for this solution. Otherwise, it might turn out to be a suboptimal business proposition, as in the case of Xanatos Marine Ltd, which suffered a lot financially despite originally developing this software solution.

Also read: How to Identify if Management is Misallocating Capital

7) Weakness in internal controls and processes at Marine Electricals (India) Ltd:

On numerous occasions, an investor comes across instances that indicate that internal controls and processes at Marine Electricals (India) Ltd have room for improvement.

For example, in FY2021, the company did not appoint a woman independent director to its board despite being a strict legal requirement. As a result, the company had to pay a total penalty of ₹489,700 to NSE.

FY2022 annual report, page 59:

National Stock Exchange…had imposed a fine…In response…company had appointed Mrs. Archana Rajagopalan…as Non-Executive Independent Woman Director and made a total payment of Rs. 4,89,700/-

In FY2021, the company did not get an independent valuation report for its properties despite the legal requirement. As a result, the statutory auditor of the company highlighted this non-compliance in its report under “Emphasis of Matter”.

FY2021 annual report, page 162:

Emphasis of Matter…Company has not obtained valuation report…of its investment property…Accordingly, fair value disclosure requirement as required under Ind AS 40…is not complied with by the Company.

During FY2019 and FY2020, Marine Electricals (India) Ltd made delays in filing statutory documents like shareholders’ and board resolutions etc. and also missed details while making these filings (FY2019 annual report, page 43 and FY2020 annual report, page 52).

In FY2024, the company did not deposit undisputed statutory dues to the government on time. (FY2024 annual report, page 111).

At times, the annual reports of the company had errors in the data.

For example, in the FY2019 annual report, on page 15, details of the actual utilisation of IPO proceeds had an error. The total of funds utilised for working capital requirements and general corporate purpose, added to ₹4,087.96 lakh instead of ₹4087.36 shown in the annual report.

Similarly, in the FY2021 annual report, while describing segmental performance, the company mentioned that it achieved revenues of ₹18201.33 cr for the electrical segment and ₹1786.02 cr for the solar segment, which totalled to about ₹2,000 cr, whereas the actual revenue of Marine Electricals (India) Ltd in FY2021 was about ₹250 cr.

The company seems to have made a mistake in writing crores, whereas the actual numbers were in lakhs.

FY2021 annual report, page 53:

The Company achieved revenues of Rs. 18201.33 Crores for Electricals & Electronics segment and Rs. 1786.02 Crores for Solar segment during FY 2020-21 as against Rs. 18720.20 Crores for Electricals & Electronics segment and Rs. 1872 Crores for Solar segment during FY 2019-20.

The Company achieved PBIT of Rs. 2041.16 Crores for Electricals & Electronics segment and Rs. (488.17) Crores for Solar segment during FY 2020-21 as against Rs. 1548.05 Crores for Electricals & Electronics segment and Rs. (687.75) Crores for Solar segment during FY 2019-20.

Also read: How to study Annual Report of a Company

8) Numerous corporate announcements made by Marine Electricals (India) Ltd:

The company has a habit of filing frequent corporate announcements with the National Stock Exchange (NSE). These vary from participation in events, order wins etc.

At times, the company has made an announcement about proposed capacity expansion without disclosing any meaningful factual details about the expansion.

For example, the corporate announcement by the company to NSE on August 19, 2024 (click here):

Subject: Expansion of Narhari Engineering Works (A Subsidiary of MEIL) – Enhancing Naval and Marine Capabilities.

Narhari Engineering works is in the process of expanding its manufacturing facility to build both Naval and Marine motors up to a range of 1MW and also start manufacturing Naval and Marine application Alternators for the same range in its new manufacturing facility under construction in Palghar.

This will help Marine Electricals India Limited increase its inhouse product offering for DG sets to be assembled in its plant in the near future.

The above announcement lacks key factual information, like:

- What is the size of the expansion, i.e. any parameter to judge by what amount/percentage the capacity will increase?

- What is the total cost of the expansion? How will the company fund this cost? How much debt will it take? How much funding will be from internal accruals or from equity dilution?

- What is the timeline for when the expansion work will start? When does the company expect the expansion work to be completed?

In the absence of these critical information pieces, an announcement becomes just a vague advertisement focused on influencing the perception in the minds of investors without giving any meaningful inputs to analysts.

We believe that investors should be cautious while reading the corporate announcements by companies that have a habit of filing very frequent disclosures about either vague information or small business developments, like every order win. Such announcements might be an attempt by companies to influence the perception and behaviour of investors.

In the past, there have been instances where companies influenced their share price by making positive corporate announcements, which later on, SEBI found to be false.

For example, take the case of Urja Global Ltd, which made fake announcements of supplying a fake mineral “Zacobite” to a Japanese company, Nippon Shinyaku Co Ltd. The announcement led to a sharp increase in the company’s share price. However, later on, SEBI found that all of it was fake. The Japanese company denied signing any contract with Urja Global. SEBI barred Urja Global Ltd and its executives from the market for 2 years (Sources: SEBI, CNBC TV18)

The top brass of Urja Global — now barred by SEBI from the markets — thought nothing of thinking up the non-existent Zacobite, which it was purportedly going to supply to Nippon Shinyaku Co Ltd. Simply put, Zacobite does not exist. Not on the Periodic Table, not even on a Google search. That’s right. The company decided to sell a product that does not exist.

Therefore, it is advised that investors should be very cautious while analysing corporate announcements made by companies and always cross-check the developments mentioned in these announcements from independent sources like customers, media and government authorities’ websites.

Also read: Why We cannot always Trust What Management Claims

The Margin of Safety in the market price of Marine Electricals (India) Ltd:

Currently (September 4, 2025), Marine Electricals (India) Ltd is available at a price-to-earnings (PE) ratio of about 56.9 based on consolidated earnings of the last 12 months (July 2024-June 2025).

We recommend that an investor read the following articles to assess the P/E ratio to be paid for any stock, which considers the strength of the business model of the company as well. The strength in the business model of any company is measured by way of its self-sustainable growth rate and the free cash flow generating ability of the company.

In the absence of any strength in the business model of the company, even a low PE ratio of the company’s stock may be a sign of a value trap, where, instead of being a bargain, the low valuation of the stock price may represent the poor business dynamics of the company.

- 4 Principles to Decide the Ideal P/E Ratio of a Stock for Value Investors

- How to Earn High Returns at Low Risk – Invest in Low P/E Stocks

- Hidden Risk of Investing in High P/E Stocks

Analysis Summary

Overall, Marine Electricals (India) Ltd has grown at a rate of 13% year on year in the last 10 years (FY2016-FY2025). However, its profit margins have been very volatile during this period.

The company operates in industries dominated by large multinational players such as Siemens, ABB, Rolls-Royce, and Wärtsilä. Low entry barriers attract small competitors, resulting in intense price-based competition.

The company is forced to keep prices low, limiting its ability to pass on rising input costs. Most of its projects are fixed-price contracts, which expose its profitability to execution delays and increases in input costs. Due to its weak negotiating position, even customer-side delays hurt its profitability.

Marine Electricals (India) Ltd faces strong difficulties in collecting payments from its customers on time. In FY2024, ₹33 crore was overdue for more than three years, with additional bad debts like ₹6.3 crore written off in FY2024 and ₹5 crore in FY2021. In FY2019, over half its receivables were pending beyond six months.

Acquisitions added to the problem—trade receivables of about ₹1 crore from Canadian subsidiary Xanatos Marine had to be written off. This cash-flow gap forces Marine Electricals (India) Ltd to rely on working capital loans and repeated equity dilutions, including IPO funds (FY2019), warrants (FY2022), and preferential allotments (FY2025).

The company’s foray into solar EPC proved disastrous. The flagship NLC India 50 MW project remained incomplete even after six years, leading to re-tendering in 2023. Between FY2019 and FY2023, solar operations generated cumulative losses of ₹23.7 crore.

To further add to its problems, the arbitration against subcontractor GE Power resulted in a ₹21.3 crore award against the company, for which provisions of nearly ₹13 crore have been made. Additionally, ₹5.8 crore paid as an advance to a Chinese supplier for solar modules was lost. Such failures underscore poor execution and vendor selection.

Since acquiring Evigo Charge Pvt Ltd in FY2021, Marine Electricals (India) Ltd has funded continuous losses—₹0.1 crore in FY2021, rising to ₹5.4 crore in FY2024. Evigo required repeated capital infusions, which were made by Marine Electricals (India) Ltd and increased its stake from 74% to 99.4%. However, valuations of Evigo for allotting shares to the company raise many doubts.

In FY2024, the company valued Evigo at ₹182 crore, while just months later, sweat equity was issued at a notional value of only ₹2 crore, heavily diluting the stake of Marine Electricals (India) Ltd. Shortly after, the valuation jumped again to ₹28 crore. These erratic shifts in valuation, coupled with minority shareholders gaining cheap equity without meaningful funding support, require that investors increase their level of due diligence.

The company repeatedly sets up subsidiaries and partnerships with minority stakes left for others/promoters. For example, Narhari Engineering Works, majority-owned by the company, required disproportionate funding from the listed company while promoters retained fixed profit shares. Athmar India, co-owned by the company and later sold entirely to promoters after entering an MoU with Cummins India, might suggest a possible transfer of business opportunities to promoter-owned entities.

Marine Electricals (India) Ltd frequently enters into related-party transactions. In FY2024, the company paid ₹3.3 crore as rent to promoter entities and engaged in ₹6 crore worth of sales/purchases with them. Instances of bad debts from related parties and prolonged advances (₹3 crore to DKM Precision Engineers, outstanding for years without purchases) further highlight the risks of transfer of economic benefits from public shareholders to promoters.

The company has a history of lapses: non-appointment of a woman director (penalty ₹4.9 lakh), failure to obtain mandatory property valuations, late filing of statutory documents, errors in reporting IPO utilisation and revenue figures (mistaking lakhs for crores). Frequent CFO and company secretary resignations worsen concerns about the stability of financial oversight.

Marine Electricals (India) Ltd paid dividends in years when it relied on debt and equity dilution, raising concerns of financial imprudence. It has locked up ₹25–30 crore in a commercial property leased out for rentals while struggling with liquidity. Its acquisitions also raise doubts in the minds of investors: the disputed ₹13.4 crore property purchase under bankruptcy proceedings remains unresolved, while the Xanatos Marine acquisition brought negligible revenues, continuing losses, and further receivable write-offs.

The company frequently issues vague or promotional announcements, such as the Palghar capacity expansion, without disclosing cost, funding, or timelines. Such practices risk influencing investor sentiment without providing analytical value.

Going ahead, an investor should keep a close watch on the profit margins of the company, its transactions with promoter entities, funding of its subsidiaries with very low contribution by other minority shareholders, and the timely collection of its receivables from customers. She should also monitor churn of key employees like the CFO and the company secretary, and frequent equity dilutions. The investor should be cautious if the company makes vague or unnecessary corporate announcements.

Further recommended reading: How to Monitor Stocks in your Portfolio

These are our views on Marine Electricals (India) Ltd. However, investors should do their own analysis before making any investment-related decisions about the company.

You may use the following steps to analyse the company: “Selecting Top Stocks to Buy – A Step by Step Process of Finding Multibagger Stocks”

I hope it helps!

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

I, Vijay Malik, am a SEBI-registered Research Analyst (Regn. No. INH100008364). This article is for educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.

{kind=link}

2 thoughts on “Analysis: Marine Electricals (India) Ltd”

While these marginal businesses, along with Nibe and Vadilal, are important from the point of view of what not to invest in, in the past, we have read great analyses of major players like Abbott and Godfrey. Hope to read more of those.

Dear Satyen,

Thanks for sharing your feedback and for highlighting analyses of Abbott India Ltd and Godfrey Phillips India Ltd — I’m glad you found those useful.

Our focus here is less on giving views on particular companies and more on helping readers build their own analysis process. That’s why we encourage investors to go through annual reports, credit rating reports, competitor filings, and other public documents in detail.

This guide explains the step-by-step process we follow: Selecting Top Stocks to Buy – A Step-by-Step Process of Finding Multibagger Stocks

If you prepare a comprehensive analysis of a company using this approach, I’d be happy to share inputs on your work in the form of an article on the website.

All the best for your investing journey!

Regards,

Dr Vijay Malik