The current article aims to highlight the critical aspects of the business of tyre manufacturing companies. After reading this article, an investor would understand the factors that impact the business of tire manufacturers and the characteristics that differentiate a fundamentally strong tyre company from a weak one.

Key factors influencing the business of tyre manufacturing companies

1) Commodity nature of tyre products:

Tyres are produced as per defined specifications with respect to sizes, weight-carrying capacity, speed limits etc. Therefore, if tyres from two companies are of the same specification, they can be interchangeably used in a vehicle with almost similar performance.

Order by the Competition Commission of India (CCI), October 30, 2012, page 28:

products sold are homogenous (a consumer can potentially use tyres belonging to different brands on the same vehicles so long as the specifications are the same) which makes it difficult for businesses to charge different prices to customers.

As a result, customers can easily switch from one tyre company to another, especially in general purpose tyres, which include most of the passenger car as well as truck and bus tyres. As a result, the tyre industry has a low customer continuity.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 3:

for general-purpose products there is a high probability of customers switching to inexpensive tires because the focus is on price rather than performance. The tendencies are similar for tires for production vehicles such as trucks. Customer continuity and stability are lower for general-purpose products.

Other than general-purpose tyres, which are the largest segment of the tyre market, the industry also produces high-performance tyres as well as specialised tyres for segments like mining, aircraft, construction vehicles etc.

In these specialised segments, due to specific performance requirements, customers tend to prefer specific tyre producers as the performance of tyres may differ significantly from one producer to another.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 3:

For specialized tires used on construction machinery, mining vehicles and aircraft, the number of manufacturers handling these products is even more limited, and customers tend to place greater value on considerations such as product performance, reliability and after-sales services.

However, the share of these specialised tyres in the overall market is small. As a result, on an overall basis, tyres are primarily commodity products where maintaining customer loyalty is difficult.

Also read: How to do Business Analysis of a Company

2) Intense price-based competition from domestic manufacturers as well as imports:

As tyres are commodity products; therefore, it is easy for new products to enter the market and appeal to customers by offering a lower price. As a result, tyre companies across the world face intense competition from domestic companies as well as imports from foreign manufacturers.

During its hearing at CCI, in 2012, Apollo Tyres highlighted the competition faced by the Indian tyre industry from MNC companies as well as cheaper imports.

Order by the CCI, October 30, 2012, page 43:

Indian tyre industry is highly competitive and…has seen significant new entrants such as Michelin and Yokohama coupled with imports from other low cost countries such as China despite anti-dumping duties

During a subsequent case at CCI, Apollo Tyres highlighted the extent of competition presented by imported tyres. As per the company, the premium variants of truck and bus tyres (radial tyres) when imported from China are 30% cheaper than the non-premium variants of tyres (bias/cross-ply/nylon) tyres produced in India.

Order by the CCI against tyre companies, August 31, 2018, page 16:

import of radial tyres from China which are considerably cheaper (almost 30% cheaper than domestic bias tyres) provide very stiff competition to the domestic tyre manufacturers in the truck bus segment.

Intense competition from cheaper tyre production centres is a global phenomenon and almost all countries are facing the same. For example, In Japan, cheaper imports of tyres from South Korea, China and Taiwan have intensified the competition.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 2:

For general-purpose products, where price competitiveness is considered a key factor, Asian manufacturers such as in South Korea, China and Taiwan that use low-cost rubber materials are emerging noticeably and increasing their market share. In high-volume markets, the competitive picture is global and is becoming even more ferocious.

In addition to the manufacturers producing new tyres, the industry also faces intense competition from retreaders that put a new layer of rubber on an old tyre and make it reusable at a 30%-80% lower cost than a new tyre.

Order by the CCI, October 30, 2012, page 93:

retreaded tyres which are viewed as an important substitute for new tyres. As per ICRA Report, the price of retreaded tyres is between 30-80% lower than the price of new tyre.

As a result of a main commodity product and retreated substitutes to new tyres, companies face very intense competition.

Also read: How to analyse New Companies in Unknown Industries?

3) Low pricing power of tyre companies over their customers:

The Tyre industry is primarily divided into two segments, sales to auto original equipment manufacturers (OEMs) i.e. auto companies for installation in new vehicles and sales in the replacement market where vehicle owners change their worn-out tyres.

The purchase of tyres by auto OEMs forms about 44% of the entire tyre market sales in India. Therefore, it constitutes a very significant segment of sales for tyre companies.

Order by the CCI, October 30, 2012, page 96:

OEM demand constitutes around…44% of total demand for domestic tyre industry.

However, auto OEMs are very large businesses when compared to tyre manufacturers. In addition, due to the commodity nature of tyres, they can easily take away their large orders to a different tyre manufacturer/import. Therefore, auto OEMs have a very high negotiating power over tyre manufacturers.

The bargaining power of auto OEMs is so much that at times, tyre manufacturers end up selling tyres to auto OEMs at a loss just to retain their share in OEMs’ purchases. In 2012, JK Tyre stated this situation of tyre manufacturers to the CCI.

Order by the CCI, October 30, 2012, page 5:

OEMs are the bulk buyers and are in a position to dictate the prices based on purchase orders…It was also submitted that in comparison to the replacement market prices, the tyres are sold at a loss or marginal profit to OEMs.

Therefore, in the new vehicle market, tyre companies face the immense bargaining power of auto OEMs and in the replacement market, they face strong price-based competition from other players, imports, and retreated tyres. As a result, tyre manufacturing companies suffer from a low pricing power in their business.

Also reading: Margin of Safety in Stock Investing: A Complete Guide

4) Cyclical nature of tyre manufacturing business:

The business of tyre manufacturing companies is impacted by cyclicity at both ends – demand for tyres as well as the cost of their raw material. As a result, the business performance of tyre manufacturers faces cyclical fluctuations.

4.1) Cyclicity in demand for tyres:

Tyre consumption for installation in new vehicles is directly linked to the sale of new automobiles, which is highly dependent on the stage of recurrent “boom and bust” cycles in economies.

Order by the CCI, October 30, 2012, page 93:

The tyre industry is cyclical and seasonal in nature. According to an ICRA Report, nearly 42% of tyre demand is dependent on automotive production, which due to its cyclical and seasonal character

During the hearing at CCI, Apollo Tyres also highlighted the high cyclicity in the demand for tyres from auto OEMs.

Order by the CCI against tyre companies, August 31, 2018, pages 16-17:

demand from the OEM segment is highly cyclical as it is closely related to the demand for automobiles.

In contrast, the demand for tyres in the replacement/commercial market is due to the wearing off of tyres in the vehicles already sold and running on the roads. That is, this demand is more linked to the number of existing vehicles in the country instead of sales of new vehicles.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 1:

commercial tire market accounts for a large percentage of total demand, and production and sales are influenced more by the total number of vehicles owned than by the volume of new vehicles sold.

As a result, even though, the movements of existing vehicles also depend a lot on the level of economic activity in any country i.e. the stage of boom-and-bust cycle, still, it is less cyclical than the fluctuations in the sales of new automobiles.

Therefore, the demand for tyres from the replacement/commercial market is less cyclical than the demand from auto OEMs.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 2:

While demand for new passenger cars and trucks is influenced by economic conditions through personal consumption and capital investment, the demand fluctuation in the commercial tire market is small compared with tires for new vehicles.

Japan Credit Rating Agency, Ltd (JCRA) also highlighted this aspect of the tire industry in its rating guidelines for the industry.

Rating methodology for tires sector by JCRA, May 2014, page 1:

While demand for tires for new vehicles tends to be exposed to economic fluctuations, replacement demand for tires used for replacement serves as a buffer.

Nevertheless, due to the primary dependency of vehicle movements on economic activity, the demand for tyres faces cyclicity in overall demand.

Also read: Credit Rating Reports: A Complete Guide for Stock Investors

4.2) Cyclical nature of raw material price movements:

Key raw materials for tyre manufacturing are natural rubber, synthetic rubber, carbon black, nylon cord fabric etc. Natural rubber can be classified as an agricultural commodity whereas other components – synthetic rubber, carbon black, nylon cord fabric etc. are crude oil derivatives. Overall, these raw materials constitute about 85% of the production costs of a tyre.

Order by the CCI, October 30, 2012, pages 7 and 15:

It was stated that raw material prices are directly influenced by prices of rubber and crude oil…on which are dependent other major raw materials such as Synthetic Rubber, Carbon Black and Tyre Cord Fabric.

It was further stated that the raw materials constitute 85% of the total cost of production.

Prices of both natural rubber as well as crude oil are highly fluctuating. Natural rubber supply in the market is very volatile both in terms of price and quantity because of suppliers’ concentration in Southeast Asia where frequent natural disasters impact its availability.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 3:

bulk of natural rubber is produced in Southeast Asia and represents a geographic concentration risk, including fluctuations in the quantity supplied because of natural disasters or seasonal factors. Like natural rubber, prices for synthetic rubber also fluctuate easily, because they are linked with the cost of naphtha, which is derived from crude oil.

Therefore, tyre manufacturers frequently face intense pressure of increasing raw material costs due to both rising natural rubber as well as crude oil prices. However, due to their low pricing power over customers, both auto OEMs as well as in the replacement market, their profit margins are hit.

Rating methodology for tires sector by JCRA, May 2014, page 2:

Although all manufacturers strive to transfer higher costs of raw materials by raising prices of their products, their profitability frequently suffers when raw materials prices rise.

Tyre companies focus on following rigid raw material procurement practices because they are liable for tyre performance throughout the life of the tyre. Therefore, even if raw material costs increase, still, they are still not able to reduce the quality of raw materials to save on costs.

Order by the CCI against tyre companies, August 31, 2018, page 57:

The manufacturers remain liable for tyre failures throughout the life of the tyre. Thus, the manufacturers tend to rigidly follow the raw material sourcing, the raw material recipe and the production process

As discussed earlier, auto OEMs, due to their large order sizes, negotiate very hard and often leave very little to no profit margin to tyre manufacturers. Therefore, even though, tyre companies enter contracts providing for price escalations based on raw material prices, still, their profit margins still suffer due to the time lag of such price increases.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 4:

Selling prices for tires for new vehicles…The leading tire manufacturers, however, have introduced contracts for setting prices based on the volatility of materials prices, and this arrangement enables them to pass on higher prices to customers, albeit with a timing gap.

On the other hand, for the replacement/commercial market, the buyers are individual vehicle owners and small fleet owners where such contractual arrangements do not exist. Additionally, due to the commodity nature of tyres, prices in the replacement market follow supply and demand, which may not be linked to raw material prices.

As a result, the business performance of tyre companies including their profit margins witness cyclical fluctuations in line with economic phases (boom and bust) and commodity price cycles (natural rubber and crude oil).

Also read: How to do Financial Analysis of a Company

5) Capital-intensive nature of tyre manufacturing business:

Tyre manufacturing requires a significant amount of investment both in fixed capital as well as working capital for operations. In fact, high capital intensity is one of the entry barriers for new players in the industry.

The CCI investigation and order in 2012 revealed that a tyre manufacturing plant with a capacity of 1 million tyres per year costs about ₹600 cr.

Order by the CCI, October 30, 2012, page 96:

no new entry in the cross-ply segment has taken place leaving the entire market to the existing players. However these, significant entry barriers arise due to the high capital requirements to setup a tyre manufacturing plant. As per ICRA Report, a plant with an annual capacity of 1 million cross ply Truck and Bus Tyres cost around Rs.6 billion.

The capital intensiveness of the tyre manufacturing process is a global phenomenon as highlighted by the Japanese credit rating agency, R&I.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 4:

Tire production is equipment-intensive, requiring large-scale machines for processes such as mixing of raw materials and molding through curing. The amount of capital investment therefore tends to be quite heavy.

Moreover, due to the low pricing power of tyre manufacturing companies, they need to focus on cost competitiveness. As a result, most of the company focus on creating large plants to gain from economies of scale benefits, which increases their capital requirements.

Rating methodology for tires sector by JCRA, May 2014, page 1:

Manufacturing tires at low costs requires large-scale plants.

Tyre is a bulky commodity; therefore, its transport requires significant logistical costs. As a result, tyres are usually manufactured near end markets or where raw material is significantly cheaper.

Rating methodology for tires sector by JCRA, May 2014, pages 2-3:

Because the cost of transportation of tires is high, tires are in principle manufactured in consumption areas. It is also necessary to carry out intensive production of general-purpose models and other products in areas where costs can be sustained at a low level, given the severe global cost competition.

Therefore, to become competitive advantageous, it becomes essential for tyre manufacturers to have multiple plants in different geographical markets, which increases their capital burden.

Moreover, in the current environment of global linkages, many large automobile companies have production plants across the world. In such cases, if a tyre company wishes to be a preferred supplier to high-selling models, then it needs to arrange for supplies of its tyres to multiple automobile plants of MNC companies, which makes their operations capital intensive.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 6:

The major finished vehicle manufacturers have built their supply systems globally, and to receive orders for tires for globally strategic vehicles, a tire manufacturer is required to provide efficient, stable supply in each region.

Apart from a large amount of fixed capital, tyre companies also require significant investments in working capital. This is because, in the replacement/commercial market, companies need to provide tyre inventory as close to the end consumer as possible, which forces companies to have multiple sales channels full of tyre inventory in warehouses as well as on the store shelves. The inventory requirement is especially large for MNC tyre companies, which need to maintain inventory around the globe.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 7:

Because the commercial tire market accounts for a large proportion of total demand, tire manufacturers need to have inventories globally, which makes their working capital burden comparatively large.

Also read: Inventory Turnover Ratio: A Complete Guide

Large fixed and working capital requirements limit new entrants in the business. As a result, the tyre industry globally as well as in India is highly concentrated.

Globally, key players like Bridgestone, Michelin and Goodyear control a large segment of the market.

Rating methodology for tires sector by JCRA, May 2014, page 1:

As a result, the global tire market has become an oligopolistic market mainly with Bridgestone, Michelin, and Goodyear.

In India, the top 5 companies control more than 80% of the overall Indian tyre market.

Order by the CCI against tyre companies, August 31, 2018, page 6:

It examined the structure of the domestic tyre market and found it to be highly concentrated with OP-1 to OP-5 having combined market share in terms of turnover of around 83% of the total industry turnover.

Therefore, a large capital investment required to make space in the concentrated tyre production market dominated by old existing players acts as an entry barrier to new players.

Moreover, to establish themselves in the replacement market, tyre manufacturers have to spend money on branding, advertisement, sales promotions etc., so that they may capture the mind space of the end consumer. This is essential because, in the replacement market, the consumer herself makes the purchase decision.

Also read: Asset Turnover Ratio: A Complete Guide for Investors

6) Diversification in the business helps tyre companies:

Tyre companies bring in diversification across different aspects of their business to bring some stability to their cyclical business model.

For example, companies focus on both new (auto OEM) and replacement market to diversify their operations. Such a diversification helps tyre companies in multiple aspects.

First, auto OEM’s demand for tyres is more cyclical than the demand from the replacement market, which is comparatively stable.

Second, a presence in the new auto OEM market helps tyre companies to generate higher sales in the replacement/commercial market as well because most of the time, while replacing, consumers stick to the brand of tyres that were present in the new vehicle.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 4:

Tire manufacturers can increase consumer recognition of their products and capture demand for commercial tires more easily if their products are adopted for new vehicles. In particular, consumers who purchase a passenger car of a certain class or higher tend to prefer products made by the same company that manufactured the tires installed on their new car.

Therefore, tyre companies that have a strong relationship with auto OEMs e.g. joint development of tyres with specific properties for vehicle models, also gain a good share of the replacement/commercial tyre market.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 4:

Provided a tire manufacturer has built a strong business relationship with finished vehicle manufacturers through, for example, joint development and supplies new car tires for globally strategic vehicles, luxury marques and so forth, this will help to ensure its share of the commercial tire market.

In addition, within the new auto OEM business, any tyre company that is able to diversify its business across multiple OEMs and also across multiple vehicle models will benefit from lower fluctuations in its earnings.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 4:

A tire manufacturer can mitigate the impact from weak sales of some customers or car models, when it has well-diversified earnings sources with several leading vehicle manufacturers among its customers.

Another aspect on which tyre manufacturers bring diversification in their business model is by diversifying across different segments of tyres like radial vs. bias/cross-ply, high performance vs. general purpose, passenger vs. commercial vehicles and entering segments like construction, mining, and aircraft tyres.

Radial tyres despite being costly seem to offer a lower overall lifetime cost due to a longer life and better fuel efficiency whereas cross-ply/bias tyres offer a lower-cost alternative and can cater to price-conscious customers; thereby capturing both ends of the market.

Order by the CCI against tyre companies, August 31, 2018, pages 51 and 87:

Radial tyre has a longer life and offers higher fuel efficiency and hence, over the life of the tyre, it is effectively cheaper than cross ply tyres.

owing to factors such as initial high price 30% higher than cross ply or bias type tyres, lack of awareness among operators, poor road infrastructure, problem of overloading of trucks etc. demand of radial tyres in the truck bus segment has been slow to pick up.

Similarly, an entry in segments like construction, mining, and aircraft tyres helps the company’s sales when the automobile sector is facing a recession.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 6:

tires for industries other than automobiles, such as construction machinery, mining vehicles, farm machinery, aircraft and industrial machinery, this leads to a stable earnings base and earning capacity.

In addition, these large and super-large tyres also have higher profit margins.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 6:

The number of manufacturers that handle the large and super-large tires used on construction machinery, mining vehicles and industrial machinery is limited. Because unit prices and profitability are higher than for ordinary tires for passenger cars owing to greater fabrication difficulty, these products can pull total earnings higher.

High-performance tyres are relatively less exposed to price competition, which is more in general-purpose tyres.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 4:

While high-performance products are less susceptible to price competition, it is often difficult to raise prices of general purpose products because their sales are largely dependent on prices.

Moreover, tyre companies also tend to diversify into segments like chemicals or industrial materials to shield themselves from the cyclicity in the tyre business.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 6:

a certain level of earnings base in sectors such as chemical products or industrial materials by taking advantage of its technological superiority in rubber products, this can mitigate the risk of fluctuations in tire demand.

Therefore, tyre companies that are able to diversify their business across multiple vehicle models across OEMs and then build upon such relationships by a significant presence in the replacement market build a strong business model. In addition, diversification across different tyre types, as well as segments like chemicals, helps in the reduction of cyclicity in the earnings.

Also read: How to do Business Analysis of Chemical Companies

7) Steps taken by tyre companies to gain competitive advantages:

In order to gain competitive advantages and improve their profitability, tyre companies take several steps like focusing on the replacement market, which offers multiple advantages like being larger in size than the new auto OEM market.

Sales in the replacement/commercial market have a higher profit margin over the demand from auto OEMs.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 5:

With higher margins, in general, than those on tires for new vehicles, the commercial tire market is a source of profits.

The replacement/commercial tyre market allows companies to create brands as replacement tyres are bought by the consumer herself. Therefore, advertisement and sales promotions play a significant role in influencing the buyer’s decision in the replacement market, which is not the case for demand from auto OEMs.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 3:

As regards commercial tires, manufacturers’ advertising activities and retailers’ recommendations and services greatly influence customer continuity, because consumers purchase their tires directly.

In addition, companies strengthen their sales network by establishing a presence across their key geographic markets through either their own stores or dealers and multi-brand tyre outlets. Nevertheless, it increases the capital requirements of the business.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 5:

make them the first choice of consumers. This means it is vital to build a powerful sales network, including dealers and auto parts stores as well as direct sales outlets, and work to gain more shelf space for the manufacturer’s products.

Tyre companies attempt to differentiate themselves by adding value-adding services to their outlets like maintenance (wheel alignment and balancing etc.) to gain customers’ loyalty.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 5:

For the major tire manufacturers in particular…provide the appropriate maintenance have also emerged as a means to achieve differentiation…With respect to general-purpose tires, provision of after-sales services is critical for ensuring profitability.

Moreover, in order to reduce costs, tyre companies, especially in Japan, even attempted in-house production of natural rubber. However, such efforts were not successful due to issues in managing large-scale farms as well as labour.

Rating methodology for tires sector by JCRA, May 2014, page 2:

Internal manufacturing of natural rubber has not progressed greatly, principally because of problems in managing large-scale farms and dealing with labor issues.

Also read: Self Sustainable Growth Rate: Inherent Growth Potential of a Company

8) Risk of govt. regulations on tyre companies:

Tyre companies are a part of the automobile ecosystem, which is one of the key emitters of polluting gases. As a result, there is continuous pressure on the whole automobile industry to become more efficient and environmentally sensitive.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 3:

Fuel efficiency and emissions regulations are expected to become even more rigorous in an effort to reduce greenhouse gas emissions and control air pollution.

As a result, tyre companies have to continuously invest money to create new technologies, which have better fuel efficiency as well as make their production process more environment friendly.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 2:

efforts to meet fuel efficiency and environmental regulations, as well as on driving performance and design, sophisticated technology is required for product development and each process of manufacturing.

Such demands for technological advancements add to the capital intensiveness of the tyre manufacturing business.

Rating methodology for tires sector by Rating and Investment Information, Inc. (R&I), Japan, May 2021, page 7:

Boosting investment for the development of advanced technologies is also critical for responding to changes in the industry structure.

Due to changing industry dynamics like the emergence of electric vehicles (EVs), which are usually heavier than ICE (internal combustion engine) vehicles, tyre companies need to adapt to new demands for sturdier tyres with higher comfort. Therefore, tyre companies continuously have to evolve their products in the everchanging industry.

Price fixing, anti-competitive cartel formation by tyre companies

Tyre manufacturing is a tough business, which is capital-intensive, and produces commoditised products with low customer loyalty leading to intense price-based competition resulting in low profit margins and fluctuating business performance.

To overcome these tough challenges, tyre companies have frequently colluded with each other and resorted to anti-competitive business practices to earn higher profits. Tyre companies have colluded with each other to both limit supplies in the market and increase prices to earn a higher return.

Such practices have been a global phenomenon where both MNC tyre companies, as well as Indian tyre companies, are penalized by regulators.

For example, one of the largest tyre manufacturers in the world, Michelin, has been penalized repeatedly in Europe for anti-competitive behaviour; first in 1981 by the Netherlands and then in 2001 by the European Commission. (Source: Michelin fined by EU regulator: EUR 19.76 mn: June 20, 2001)

European Commission has decided to impose a fine of € 19.76 million on French tyre maker Michelin for abusing its dominant position…The infringement is all the more serious that this is the second time that Michelin engages in similar anti-competitive behaviour in Europe…In 1981, the Commission found Michelin guilty of the same anti-competitive behaviour in the Netherlands.

Currently, South Africa is also investigating tyre companies for anti-competitive practices (Source: Competition Commission tyre price fixing hearing underway in South Africa)

Similarly, in 1974, Indian Monopolistic and Restrictive Trade Practices (MRTP) Commission acted against the cartel of Indian tyre companies and issued a cease-and-desist order.

Order by the CCI, October 30, 2012, page 2:

even 35 years back the MRTP Commission had passed its first ‘cease and desist’ order against the cartelization by domestic tyre industry in October 1974.

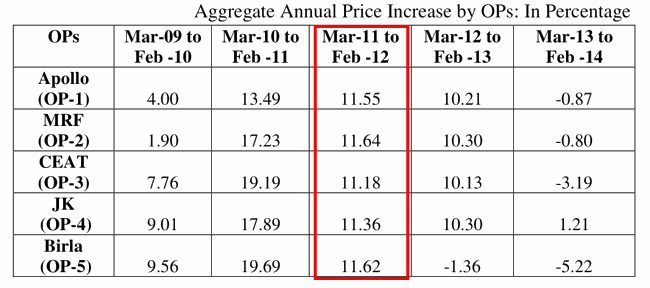

Recently, in 2018, CCI found that the top 5 Indian tyre companies, Apollo Tyres Ltd, MRF Ltd., CEAT Ltd., JK Tyre and Industries Ltd. and Birla Tyres Ltd. have formed an anti-competitive cartel and also that the industry body, Automotive Tyre Manufacturers Association (ATMA) has provided a platform for such abusive practices. As a result, CCI has put a penalty of ₹1,788 cr on the tyre companies.

CCI found multiple instances of collusion by tyre companies. For example, CCI uncovered an email conversation dated May 18, 2011, between tyre companies’ officials and an ATMA officer, which discussed about increasing tyre prices by about 10.5% by all players despite declining raw material prices (natural rubber, NR).

Order by the CCI against tyre companies, August 31, 2018, page 16:

His ‘personal view’ was that tyre companies (looking at the QI financial results) need to go for price increase (roughly) of the same magnitude as (already) done in this current fiscal (3+3+4.5), say roughly between 10-11 pc. According to him, an increase of this quantum was imperative despite softening of NR prices and in view to maintain healthy EBITA margins which, in turn, would fuel capacity expansions.

CCI found that subsequently, in 2012, all the top 5 tyre companies increased their prices by about 11%-11.5%.

Order by the CCI against tyre companies, August 31, 2018, page 55:

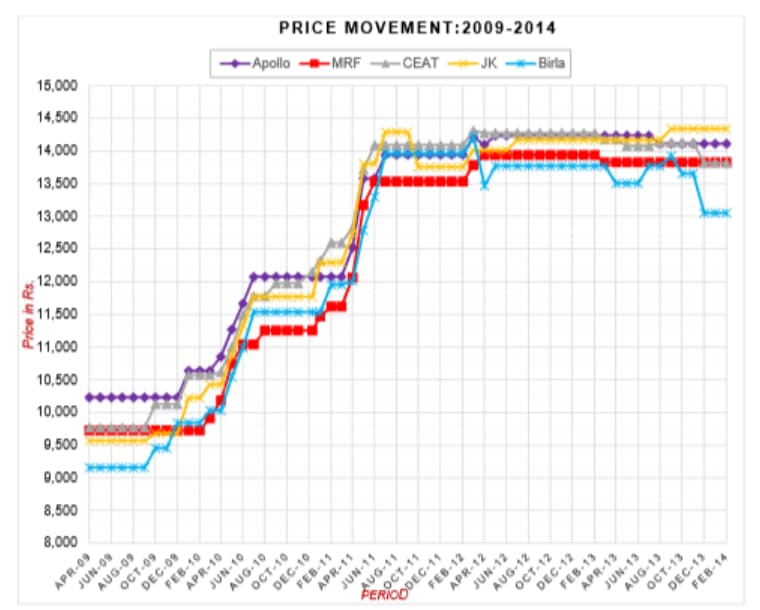

Moreover, CCI noticed that during 2009-2014, the prices by tyre companies followed exactly the same pattern i.e. price parallelism.

Order by the CCI against tyre companies, August 31, 2018, page 54:

The price changes by tyre companies were almost identical despite operations at different efficiency levels.

Order by the CCI against tyre companies, August 31, 2018, page 7:

it was observed by the DG that in the years 2011-12 and 2012-13, the percentage of price increase was nearly identical in-spite of the fact that the OPs operated at different efficiency levels.

CCI found that all tyre companies increased prices despite a decline in raw material prices as well as they coordinated their sales in such a manner that their market share stayed constant indicating that they were not competing with each other.

Order by the CCI against tyre companies, August 31, 2018, page 58:

raw material cost has declined for all the OPs while all of them have uniformly increased the price of their respective variants of tyres in the said tyre category…Such stability in the market share in the replacement market indicates that OP-1 to OP-5 were not competing with each other during 2011-12 to 2013-14 in spite of decrease in prices of inputs.

CCI observed that tyre companies stopped competition from imports by making govt. of India to impose anti-dumping duties and then increased their prices to earn higher profits, which they could use to expand capacities. Such large capacities of existing players would create higher entry barriers for new players.

Order by the CCI against tyre companies, August 31, 2018, pages 88-89:

on one side, the OPs have been getting anti- dumping duties imposed on the import of truck bus bias tyres thereby effectively shielding the domestic cross-ply/bias tyres market from external competition by way of imports and on the other hand raising the prices of cross- ply/bias tyre variants in the replacement market…they have been able to generate resources to finance capacity expansion which would lead to creation of surplus capacities over time and would enable OP-1 to OP-5 to erect entry barriers thereby enabling them to dictate prices in future. Such conduct is pernicious and has to be ripped as it affects the competitive process.

CCI noted that tyre companies have restricted production and supply of tyres in the market to increase prices and earn higher profits.

Order by the CCI against tyre companies, August 31, 2018, page 90:

OPs, by acting in concert, have increased the prices of cross ply/ bias tyres variants sold by each of them in the replacement market belonging to the truck/ bus segment and have also limited and controlled the production and supply in the said market

CCI also observed that tyre companies have exploited the dependence of individual/small buyers in the replacement market as such customers have to buy cross-ply/bias tyres from Indian manufacturers as they cannot afford radial tyres.

Order by the CCI against tyre companies, August 31, 2018, page 90:

The buyers in the replacement market are individual truck/ bus owners/ small fleet owners. Owing to huge price difference between radial tyres and cross-ply/bias tyres, they have not been able to switch over to radial tyres thereby indicating that they are locked in or are dependent on cross-ply/ bias tyres. The conduct of OP-1 to OP-5 during the impugned period as evidenced from rise in price effected and the email communications in this regard clearly reveals that OP-1 to OP-5 have been exploiting this advantage.

As a result, CCI has put a monetary penalty on the top 5 Indian tyre companies as well as their industry organization ATMA.

Tyre companies have appealed against the CCI order and currently, the case is pending in the Hon. Supreme Court of India. (Source: CCI approaches Supreme Court against NCLAT’s tyre cartel ruling)

If the Hon. Supreme Court of India upholds the order of CCI and subsequently, the anti-competitive cartel of tyre companies is broken, then India may witness a decline in tyre prices, which might lead to a reduction in the profitability and the return generated by Indian tyre companies.

As per the claims by the All India Tyre Dealers’ Federation (AITDF) to the CCI in 2012, due to their cartel, Indian tyre manufacturers are able to earn a much higher return on capital (4%-6%) when compared to their global peers (1.5%-2%).

Order by the CCI, October 30, 2012, page 25:

rate of return on capital employed in the international tyre manufacturing industry is traditionally low at 1.5%-2%, but in case of Indian tyre makers they have been having a rate of return ranging from 4% to 6% on annual basis during the last 5-6 years

Therefore, a breaking of the tyre manufacturers’ cartel and implementation of competitive market behaviour may bring down the profit margins and returns for Indian tyre companies.

To learn more about examples of industries where CCI has found cartel formations, an investor may read our following articles on business analysis of the Cement Industry and Paper Industry.

Summary

Tyre companies operate in a very tough business environment. They face intense competition from domestic manufacturers, MNC players and cheap imports. Their product, tyres, is a commodity and customers can easily switch tyres of a particular specification of one manufacturer with another. Therefore, tyre companies do not have any pricing power over their customers.

In the tyre market for new vehicles, the auto OEMs are primary buyers who put significant pricing pressure and negotiate very hard with tyre companies. As a result, tyre manufacturers have to supply tyres at a very low price to OEMs. At times, tyre companies are not able to make profits on such deals. Nevertheless, they have to supply tyres for new vehicles because there are end customers who prefer to stick to the brand of tyres of the new vehicle while buying replacement tyres.

However, even in the replacement market, competing brands, cheaper imports, and retreaded tyres continue to put pricing pressure on tyre companies.

Due to low pricing power, tyre companies face difficulties in passing on an increase in raw material prices to customers. As a result, during periods of high raw material prices, the profit margins of tyre companies decline. This is especially true during economic downturns when the sale to new auto OEMs declines and the demand from the replacement market moderates. A lower economic activity in the country impacts sales of both new and replacement tyres leading to cyclicity in the performance of tyre companies.

Tyre manufacturing is a highly capital-intensive process where companies need to create large plants to be cost-competitive. They need to create multiple plants near consumer markets/OEM plants to quickly fulfil customers’ demands. This in addition to the requirement of keeping inventory in multiple sales channels for the replacement market increases the working capital requirements for tyre companies’ operations.

In addition, tyre companies need to continuously invest money to develop new tyres to meet evolving fuel efficiency and environmental emission norms. Companies need to develop tyres that can provide comfort despite carrying higher weight of electric vehicles (EVs) increasing the capital requirement for tyre companies.

Companies need to invest in brand, advertisement, and sales promotions to create a space in the replacement market. They also need to provide maintenance services like wheel alignment and balancing as well as after-sales support in their dealerships as it has become a necessary means to differentiate from competitors.

Tyre companies try to achieve diversification in business segments like new auto OEM and replacement markets, high performance vs. general purpose tyres, and non-automobile tyres like construction, mining, aircraft tyres etc. to bring in relative stability in their earnings. Companies also focus on other rubber chemicals and related segments to achieve diversification.

Nevertheless, the business of tyre companies is tough because they do not have any extraordinary pricing power over their customers and have to invest large amounts of money in their business, which is the only entry barrier for new entrants. As a result, tyre companies historically have formed anti-competitive cartels to control pricing and supplies of tyres, globally.

Leading tyre players like Michelin as well as all the top 5 Indian tyre players have been found to collude for anti-competitive practices. CCI has penalized the top 5 Indian tyre companies for ₹1,788 cr. and asked them to stop engaging in anti-competitive practices.

This matter is currently under appeal and an investor needs to closely monitor developments in the Hon. Supreme Court of India regarding this case. If the govt. is successful in breaking the tyre cartel and market forces return to the tyre market, then tyre companies may see their profit margins and return ratios decline.

An investor should always keep in mind these multiple aspects of tyre companies to understand their business position.

- Commodity nature of tyres

- Intense price-based competition from domestic manufacturers as well as imports

- Low pricing power over their customers

- Cyclical nature of business due to cyclicity in demand of tyres as well as cyclical nature of raw material price movements

- Capital-intensive nature of business

- Diversification strengthens the business of tyre companies

- Focus on replacement market and brand building helps to gain competitive advantages

- Companies face the risk of govt. regulations on fuel efficiency and emission control norms

- Price fixing and anti-competitive cartels are formed by tyre companies, which have distorted market dynamics

We believe that if an investor analyses any tyre company by keeping the above factors in mind, then she would be able to assess its business properly.

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

I, Vijay Malik, am a SEBI-registered Research Analyst (Regn. No. INH100008364). This article is for educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.