Profit generated by a company is one of the most important parameters looked at by the investors. The profit forms a part of many key ratios used by investors like price to earnings ratio (PE ratio), return on equity (ROE), return on capital employed (ROCE) etc. As a result, almost all the companies make their best attempt to generate as high a profit as possible from their business.

Most of the time, companies work hard on their business strategy, generate higher revenue, control their costs, and improve their operating efficiency in order to generate high profits. In these cases, the companies work with their business strengths to produce high returns from their business for their shareholders.

However, sometimes, investors would notice that companies resort to tricks other than genuine business efforts to increase their profits.

During our investing journey, we have had the experience of analysing hundreds of companies both for our website as well as for our personal investments. During our analyses, we have come across many such instances where companies seem to have attempted to show profits that are higher or losses that are lower than the actual financial position.

In many of these cases, the companies and their management apart from their genuine business efforts to increase profits also resorted to other tricks so that they could report higher profits.

We have noticed that most of the attempts by the companies to inflate profits fall under the following categories:

- Playing around with expenses: Companies show higher profits by:

- Trying not to show certain expenses in the profit and loss statement (P&L) or

- When they show expenses in the P&L, then they resort to some conventions that these expenses despite being present in the P&L do not reduce the profits.

- Playing around with profits or losses from investments in financial instruments, subsidiaries, joint ventures etc. In these cases, we have come across instances where:

- Companies had shown profits when they actually seemed to make losses.

- In some other cases, companies showed profits when there were no profits.

- In still other cases, companies showed profits on investments in circumstances where the investor is not able to justify profits using common sense.

- In a few cases, the companies showed losses in the P&L, but they resorted to conventions where these losses despite being in P&L, did not reduce the profits.

- In addition, we also came across cases where companies resorted to delaying acknowledgement of losses on their investments to the last extent possible. Only when they could not postpone it any further, then they recognized the losses after many years of investments losing their fair value.

- Refusing to spend on expenses that they are required to do and thereby showing higher profits.

- Changing accounting policies whenever it suits them to show higher profits. Many times, companies changed the accounting assumptions to show higher profits even though the auditors highlighted it.

The current article is an attempt to present illustrations with live examples of cases so that investors may learn to identify the practices of companies and their management to show higher profits.

We believe that investors should focus on the systematic approach with which these cases are analysed and the sections of the annual reports used to identify such practices. This is because, only by understanding the underlying process, an investor would be able to use it in their own analysis and make an informed investment decision.

1) Companies inflate profits by playing around with expenses

As mentioned above, we have come across cases where companies show higher profits by either trying not to show some expenses in the P&L or when they show expenses in the P&L, then they use some conventions so that these expenses do not reduce their profits despite being present in the P&L.

Let us see illustrative examples for each of these situations.

A) Companies do not show some expenses in the P&L:

While analysing companies, investors will come across cases where companies do some spending but do not show it as an expense in the profit and loss statement. One of the methods used by companies to achieve this goal is to use the concept of capitalization.

Companies capitalize even those expenses in fixed assets, as per investors should be recognized as an expense in the P&L. As a result, the companies show lower expenses and higher profits in the year.

Let us see some examples of such cases.

i) Globus Spirits Ltd:

Globus Spirits Ltd is a manufacturer of country liquor (IMIL) and bottler for Indian made foreign liquor (IMFL) having a presence in multiple states with distilleries in Rajasthan, Haryana, West Bengal, and Bihar. The company owns IMIL brands like Nimboo, Narangi, Heer Ranjha, and Ghoomar.

In FY2014, the auditor of Globus Spirits Ltd pointed out that until FY2013, the company has capitalized advertisement and promotional expenses of about ₹36 cr. as intangible assets in the fixed assets.

Ideally, Globus Spirits Ltd should have deducted these expenses from the profit & loss statement as expenses in the years in which the company spent this money.

FY2014 annual report, page 45:

Basis for Qualified Opinion: As on March 31, 2014, Fixed Assets include Intangible Assets aggregating to ₹2,886.60 Lacs (March 31, 2013 – ₹3,608.25 Lacs) under the head “Knowhow and New Brand Development” representing intangibles internally generated by the Company through expenditure on advertisement and promotional expenses. Such recognition is not in accordance with Accounting Standard – 26 “Intangible Assets”. Had the Company complied with requirements of AS-26, Fixed Assets as at March 31, 2014 would have been lower by ₹2,886.60 Lacs (March 31, 2013 – ₹3,608.25 Lacs), Depreciation and amortisation expense for the year would be lower by ₹721.65 Lacs, Net profit after taxes for the year would be converted into net losses after tax of ₹1,477.82 Lacs and Reserves and Surplus would be lower by ₹1,905.45 Lacs

This qualified opinion by the auditor indicates that the pretax profits for the years before FY2014 were higher to the extent of ₹36 cr.

After this observation by the auditor, Globus Spirits Ltd deducted these expenses over the next five years (FY2014-18) as additional depreciation of about ₹7.2 cr. each year.

Therefore, while analysing companies, an investor should pay specific attention to the expenses that companies capitalize in their fixed assets. By focusing on these items, she would be able to identify cases where the companies may have inflated their profits using the route of capitalization.

An investor may read the complete analysis of Globus Spirits Ltd in the following article: Analysis: Globus Spirits Ltd

ii) Emmbi Industries Ltd:

Emmbi Industries Ltd is engaged in the manufacturing of technical textile products: flexible intermediate bulk container (FIBC) / various polymer-based packaging products, geotextiles, water conservation products (Aqua Sure) etc.

While analysing the FY2016 annual report, an investor notices that Emmbi Industries Ltd has been capitalizing certain expenses like brand development expenses, foreign trade fair expenses and knowledge development expenses, which on the face of it look like expenses that should be charged to P&L and not capitalized.

FY2016 annual report, page 72:

These expenses seem like advertising expenses and the money spent to participate in a foreign trade fair, which as per investors, should be deducted as an expense in the profit and loss statement.

It is advised that an investor should examine these expenses further and may get a clarification from the company about the nature of these expenses, which warrants them to be capitalized.

An investor may read the complete analysis of Emmbi Industries Ltd in the following article: Analysis: Emmbi Industries Ltd

B) Companies show expenses in P&L but nullify their impact on profits:

At first glance, such a situation will come across as counterintuitive to the investor. She wonders how is it possible that an expense is present in the P&L, but it is still not reducing the profits.

Upon deeper analysis, the investor would notice that in such cases, the companies show a particular expense in the P&L but simultaneously show a transfer entry shifting an amount from the reserves to the P&L, which is usually exactly equal to the mentioned expense. The net result is that the transfer from the reserves overcomes the impact of reduction by the expense.

As a result, the profit of the company remains unaffected as if, the expense simply did not happen.

Let us see some examples to see it in real-life cases.

i) Emami Ltd:

Emami Ltd is a leading FMCG company in India, engaged in the manufacturing of herbal and ayurvedic products sold under Emami (Personal & Cosmetic), Himani (Ayurvedic) and Zandu brands.

While analysing the annual reports of the company, an investor notices that from FY2013 to FY2014, the net intangible assets decreased from ₹67 cr. to ₹7.78 cr. This is primarily due to the decline in goodwill by ₹60.97 cr.

The decline in goodwill is a regular amortization charge by which Emami Ltd has been decreasing its gross goodwill of ₹478.99 cr. over the years. In the previous years, it has been amortizing the goodwill at about ₹100-102cr. per annum.

Below is the relevant extract from the FY2014 annual report of Emami Ltd:

The amortization of goodwill in the normal course of business and accounting is an expense in the profit and loss statement just like the depreciation expense for tangible assets. As a result, the profit of any company declines accordingly on the amortization of goodwill.

However, one important thing that an investor would notice while analyzing the amortization of goodwill by Emami Ltd is that it is transferring an amount equal to the yearly goodwill amortization from its general reserve to the profit & loss statement every year.

FY2014 annual report, page 139:

This entry nullifies the impact of goodwill amortization on its profits. Though it does not impact the overall cash position of the company.

If Emami Ltd were not following this practice of transferring amounts from general reserve to profit & loss statement, then its profit before tax would have been lower by an equal amount every year. Emami Ltd has disclosed this practice in its significant accounting policies:

Intangible Assets : a. Goodwill – Consequent to the scheme of arrangement being accounted for under Purchase Method by adopting book value method, the cost representing goodwill recognised is being amortised to Statement of Profit & Loss over, the estimated useful life of five years. As per the terms of the scheme equivalent amount of such amortisation is transferred from General Reserve.

In the normal course of business, it might amount to overstating of profits, however, as explained by Emami Ltd, it is doing the same as per the scheme of the arrangement, which I assume would have been approved by any competent authority (in most cases a court of law) that would have allowed the company to adjust goodwill amortization directly against its reserves without impacting profit & loss statement. The annual report does not provide details of which competent authority, if any, has approved/allowed such treatment of goodwill amortization against the general reserve.

However, an investor would appreciate that as a result of the practice of Emami Ltd to transfer the amount equal to the amortization of goodwill, from reserves to the P&L, the impact of amortization expense on the profits is nullified.

An investor may read the complete analysis of Emami Ltd in the following article: Analysis: Emami Ltd

ii) Indo Count Industries Ltd:

Indo Count Industries Ltd is an Indian textile player, which has a significant share in the home textile segment of the USA and has marquee clients like Walmart, JC Penney, Target, etc. as customers.

While analysing the annual reports of Indo Count Industries Ltd, an investor comes across an interesting case of revaluation of assets by the company. In the FY2016 annual report of Indo Count Industries Ltd, page 128, an investor would come to know that the company had done a revaluation of its assets in 2008 and 2009:

i) The company revalued its land, buildings and plant & machinery (except for electronics division and 2 D.G. sets of spinning division) as on 01-10-2008 based on the valuation made by an approved valuer. Accordingly, the original cost of such assets resulted in gross increase in the value of assets over their original cost by ₹ 14,365.45 lac (excluding the assets sold till 31-03-2016), increase in depreciation upto 31-03-2016 on revaluation by ₹ 6,937.02 lac and thereby net revaluation reserve as at 31-03-2016 is ₹ 7,42843 lac.

ii) Revaluation of 2 D.G. sets of spinning division was carried out on 01-04-2009 by an approved valuer.The revaluation resulted in a gross increase in the value of assets over their original cost by ₹ 1,238.07 lac (excluding the assets sold till 31-03-2016), increase in depreciation upto 31- 03-2016 on revaluation by ₹ 721.92 lac and thereby net revaluation reserve as at 31-03-2016 is ₹ 516.15 lac.

Assets held by companies, just like the assets held by us, keep on changing in valuation over the years e.g. during growing times certain assets like land increase in value and the company is right in reassessing the value of such assets and changing their value in the balance sheet. The original value of these assets in the balance sheet is the acquisition cost, which can now be increased/decreased to reflect the current value so that the balance sheet and book value can be closer to real valuations.

However, what is surprising in the revaluation done by Indo Count Industries Ltd is that they have revalued assets like building, plant & machinery, diesel generator (DG) sets as well and valued them at a higher valuation than the acquisition cost despite using them for their operation for some time.

The company may have reasons to believe that building, plant & machinery and diesel generator sets may also increase in value over-usage & time. However, by common logic, it seems more probable that the value of diesel generator sets, plant & machinery and the building goes down due to usage related wear & tear. Therefore, an investor should analyze further to understand the peculiar nature of mentioned diesel generator sets, plant & machinery and the building that they are increasing in value with usage over time.

By analyzing the FY2010 annual report, the investor would notice that the company has revalued its above-mentioned assets by about ₹178.7 cr.

The investor would appreciate the importance of analysis of the extent of the revaluation reserve when she notices that the company has been reducing its depreciation expense every year by adjusting a part of the revaluation reserve against it in the profit & loss statement, which is leading to lower depreciation expense and thereby higher profits.

A look at the notes to the accounts under the depreciation section of the FY2016 annual report (pg. 135) would indicate that Indo Count Industries Ltd has used about ₹11 cr. (FY2016) and ₹12 cr (FY2015) respectively from the revaluation reserve and reduced its depreciation expense by the same amount.

The equivalent adjustment from the revaluation reserve can be seen in the note on reserves in the FY2016 annual report (pg. 124):

The net impact of the above transaction is that in FY2015 the profit before tax (PBT) becomes higher by about ₹12 cr and in FY2016, the PBT becomes higher by about ₹11 cr when compared to a scenario when the company would not have revalued its diesel generator sets, plant & machinery and building and such revaluation reserve would not have been there.

An investor would notice that in FY2010, the total amount of revaluation reserve created by Indo Count Industries Ltd was ₹178.7 cr. An investor would appreciate that the company would adjust this revaluation reserve part by part over the years against depreciation expense, which would effectively increase their profit before tax (PBT) by an equal amount over the next few years.

The analysis of revaluation reserves section of the FY2016 annual report shared above indicates that by FY2016, the company has already utilised about ₹84 cr worth of revaluation reserve and about ₹94 cr worth of revaluation reserve still remains to be adjusted, which would be adjusted in coming years.

An investor can interpret that from FY2010 to FY2016, Indo Count Industries Ltd has reported cumulative PBT of ₹84 cr because of revaluation of diesel generator sets, plant & machinery and building on a higher amount despite using them for some time and despite the usual wear & tear associated with operational usage. And the company would further show PBT of ₹94 cr in future years by adjusting this remaining revaluation reserve on March 31, 2016.

It is as good as a scenario, where if any company wishes to increase its profits by ₹100 cr in future years, then it simply needs to revalue its assets up by ₹100 cr and keep on adjusting the revaluation reserve thus created for reducing the depreciation expenses over coming years.

Alternatively, it can also be interpreted as a situation where:

- First, the company revalued its assets upwards and created the revaluation reserve. This exercise increased the amount of shareholder’s equity by the amount of revaluation reserve. This step increased the equity without impacting debt. Therefore, the debt to equity ratio, which is one of the key parameters monitored by external stakeholders declines and the capital structure of the company becomes better.

- However, when the time comes to recognise the depreciation on the now increased size of assets, the company adjusts the revaluation reserve against depreciation saying that it will provide depreciation only on the actual cost of assets and not the revalued amount. This adjustment of the depreciation expense removes the impact of the increase in asset value on the profits.

Therefore, the company is able to show a lower debt to equity ratio and maintain its profitability as well. It’s a win-win situation for the company on both the aspects of the balance sheet as well as the P&L account.

Therefore, it becomes paramount that the investor should understand the nature of diesel generator sets, plant & machinery and building which increased in value despite usage and the usual wear & tear associated with operational usage. Otherwise, the profits showed by Indo Count Industries Ltd to the extent of ₹178.7 cr at the PBT level (equal to the revaluation reserve at FY2010) and related net profits after tax of about ₹125 cr. (deducting 30% tax from PBT of ₹178.7 cr), would not have any sound basis.

Therefore, an investor would appreciate that while analysing companies, she should read every line of the disclosures in the financial statements, so that she is able to identify cases where companies attempt to show higher profits using such conventions.

An investor may read the complete analysis of Indo Count Industries Ltd in the following article: Analysis: Indo Count Industries Ltd

2) Companies inflate profits by playing around with profits or losses from investments

In these cases, investors would come across multiple interesting cases where companies showed profits when they actually seemed to make losses. Companies reported profits on investments when actually; they did not have any profits.

In some cases, companies showed profits on investments by such transactions where the investor is not able to justify profits using common sense. In a few other cases, investors would notice that the companies showed losses in the P&L, but they resorted to conventions where these losses despite being in P&L, did not reduce the profits.

In some other cases, investors would notice that the companies resorted to delaying acknowledgement of losses on their investments to the last extent possible. Only when they could not postpone it any further, then they recognized the losses after many years of investments losing their fair value.

The attempt of companies in all these cases is usually to show a higher profit or a lower loss than what the actual situation is.

Let us see examples of cases where companies worked around investment gains or losses to inflate profits.

A) Companies show profits when in fact there seems to be a loss:

These cases are tricky to interpret. If an investor reads the annual report only for the year in which the company has reported the gain on investment, then she may miss the complete picture. Therefore, it is essential that the investor should read all the annual reports since the original investment was made by the company and along the way keep reading all the annual reports in between focusing on developments related to that particular investment.

By reading all the historical annual reports, the investor would be able to understand the actual cost of the investment, which she can then compare with the realization value in the later years to understand whether the company had made a real profit or not.

Let us see an example.

i) Datamatics Global Services Ltd:

Datamatics Global Services Ltd (DGSL) is an Indian company providing Information Technology, business process management (BPM), engineering, data, and analytics services. The company provides IT products for robotics process automation (RPA), analytics, business intelligence, and automated fare collection (AFC).

While doing an analysis of DGSL, an investor comes across the formation of an employee welfare trust by the company. The analysis of the transactions of the company with the employee welfare trust provides interesting insights.

In 2010, the company established the Datamatics Employees Welfare Trust in order to execute its employee stocks options plan.

FY2011 annual report, page 24:

The following Special Resolutions were passed at the previous three Annual General Meetings:

3. AGM held on August 12, 2010:- (i) Formation of Datamatics Employees Welfare Trust for transfer of shares granted under the existing ESOP Schemes.

In the same year, Datamatics Global Services Ltd gave a loan of about ₹7 cr to Datamatics Staff Welfare Trust to buy equity shares of the company. FY2011 annual report, page 50:

Amount recoverable from ESOP Trust consists of ₹ 69,347,270 paid to Datamatics Staff Welfare trust during the year for purchase of 1,753,261 Equity shares of the Company.

While reading the annual reports of the company, it seems that the company has used the names of the trust: Datamatics Employees Welfare Trust and Datamatics Staff Welfare Trust. This is evident from the disclosures of the company in later annual reports, where the mentioned amount of loan to the names of both the trust is the same. E.g. in the FY2013 annual report, page 70, the amount of loan in the previous year (P.Y) as well as the number of shares purchased are the same in reference to Datamatics Employee Welfare Trust, which was in the FY2011 annual report in reference to Datamatics Staff Welfare Trust.

Employee Stock Option Scheme: The Datamatics Employee Welfare Trust (Trust) had purchased 1,753,261 shares of Company for granting stock options to the employees. The purchases are fi nanced by loans from the Company. Amount recoverable from Trust as on March 31, 2013 is ₹ 64,952,691 (P.Y. ₹ 69,347,270).

Therefore, we believe that the company has used these names interchangeably. For any further clarification, an investor may contact the company directly.

From the above disclosures, an investor realized that Datamatics Global Services Ltd has formed a trust and has given it a loan of ₹7 cr in order to purchase shares. Subsequently, the trust has purchased 1,753,261 shares in order to grant them to the employees who exercise their ESOPs (employee stock options).

It seems a situation where the trust has created an inventory of stocks of the company by purchasing it from the open market. Subsequently, whenever, any employee exercises its ESOPs, then the employee pays the exercise price (ESOP price) to the trust and the trust grants the required number of shares to the employee from its inventory of shares.

In such a scenario, an investor would appreciate that the income of the trust is the money paid by employees to exercise their ESOPs. Whereas the outflow for the trust has been the money paid by it to acquire 1,753,261 stocks for which it had taken a loan of ₹7 cr from Datamatics Global Services Ltd. The average cost of these shares to the trust comes out to be about ₹39.5 per share.

In such a situation, an investor would appreciate that the trust can repay the loan to Datamatics Global Services Ltd only when it takes more money from the employees when they exercise their ESOPs than the money that it had paid to acquire the shares. Therefore, the trust must charge at least ₹39.5 per share from the employees to grant them shares to make any money and repay the loan to the company.

However, when an investor analyses the pricing formula of the ESOPs of the company, then she realizes that the options granted by the company are exercisable at ₹5 per share.

FY2015 annual report, page 38:

An investor notes that out of the multiple ESOPs scheme approved by Datamatics Global Services Ltd, until FY2015, it had granted options only out of the Key ESOPs schemes of 2006 and 2007. The company did not grant any options out of the general ESOPs schemes of 2007 and 2011 as well as the Key ESOPs scheme of 2011. An investor may draw the following interpretations from this information:

- It may be that the Key ESOPs Schemes are only for senior employees and the General ESOPs schemes may include other lower designation employees as well. If this were the case, then an investor would note that out of different ESOPs schemes, the company granted options only to the senior management under Key ESOPs and did not grant any option to general employees under General ESOPs schemes.

- The options granted under Key ESOPs schemes are exercisable at a price of ₹5 per share whereas the cost price of each share to the trust is ₹39.5.

Therefore, in terms of the financial situation of the trust, it had to spend ₹39.5 per share to acquire equity shares of the company, which it had to grant to employees by accepting the exercise price of ₹5 per share from them.

An investor will appreciate that in such a situation, the trust can never repay the loan of ₹7 cr taken by it to acquire the equity shares.

Datamatics Global Services Ltd closed all its existing ESOP schemes in FY2016.

FY2016 annual report, page A22:

EMPLOYEE STOCK OPTION PLANS (ESOP): The Board of Directors, on the recommendation of Nomination and Remuneration Committee, have at their meeting held on May 27, 2016 approved the closure of Key ESOP Scheme 2006, General ESOP Scheme 2007, Key ESOP Scheme 2007, General ESOP Scheme 2011 and Key ESOP Scheme 2011. There are no existing granted options in any of the above-mentioned ESOP schemes

As a result, of the closure of all the existing ESOP schemes, the trust was rendered without purpose and it was liquidated in FY2016.

FY2016 annual report, page A102:

EMPLOYEE STOCK OPTION SCHEME: The Datamatics Employees Welfare Trust (Trust) had purchased 1,753,261 shares of the Company for granting stock options to the employees. The purchases are financed by loans from the Company. During the year Trust was liquidated and ₹ 48.59 million has been received and shown as extraordinary items. The amount includes ₹ 40.29 million towards profit on sale of investments and balance towards other income net of expenses over the years.

An investor notes that on liquidation of the trust in FY2016, Datamatics Global Services Ltd received back an amount of ₹4.9 cr. While reading the annual report of FY2015, an investor notices that on March 31, 2015, the outstanding loan given by the company to the trust was ₹6.3 cr.

FY2015 annual report, page 101:

In light of the above information, an investor would appreciate that the loan outstanding to the trust was ₹6.3 cr whereas the amount received on its liquidation was ₹4.9 cr. As a result, the company seems to have lost ₹1.4 cr out of its loan to the trust.

However, when an investor analyses the FY2016 annual report further, then she notices that Datamatics Global Services Ltd instead of recognizing the loss of ₹1.4 cr in its P&L statement, the company has recognized the liquidation value of ₹4.9 cr as an exceptional income in the P&L.

FY2016 annual report, page A68:

Exceptional income of ₹ 48.6 million received from Datamatics Employee Welfare Trust on its liquidation.

An investor is confused by this accounting treatment by the company. An investor may think that the company could recognize an income/profit in the P&L only when it received an amount higher than the loan outstanding. Therefore, Datamatics Global Services Ltd could recognize an exceptional income of ₹4.9 cr on the liquidation of the trust when it would have received a total of ₹11.2 cr from the liquidation of the trust (11.2 = 6.3 + 4.9 i.e. ₹6.3 cr of loan recovery and ₹4.9 cr of surplus exceptional income). However, as per the disclosure of the company in the FY2016 annual report, the amount received from the liquidation of the trust including the profit on the sale of investment is stated at ₹4.9 cr.

FY2016 annual report, page A102:

During the year Trust was liquidated and ₹ 48.59 million has been received and shown as extraordinary items. The amount includes ₹ 40.29 million towards profit on sale of investments and balance towards other income net of expenses over the years.

In light of the above information, it is not clear why Datamatics Global Services Ltd recognized a profit/exceptional income on the liquidation of the trust instead of the loss due to the under-recovery of the loan given to the trust.

On the face of it, this might seem like a case where the company had incurred a loss of ₹1.4 cr on the loan given by it to the trust as it received only ₹4.9 cr against the outstanding loan of ₹6.3 cr. However, the company has reported an exceptional income/profit of ₹4.9 cr.

An investor may contact the company directly to seek clarifications in this regard.

From the above case, an investor would notice that it is essential to read the detailed notes to the financial statements and not make conclusions based only on the data provided by the company in the tables of profit and loss and other statements in the annual report.

An investor may read the complete analysis of Datamatics Global Services Ltd in the following article: Analysis: Datamatics Global Services Ltd

B) Companies show profits when there are no profits at all:

While analysing companies, an investor will come across some such cases where companies resorted to showing profits in such transactions while as per the investor, there is not any profit during the year.

Many times, these transactions are related to the transfer of assets from the company to its subsidiaries etc.

Let us see an example of such a case.

i) India Glycols Ltd:

India Glycols Ltd is an Indian company manufacturing glycols, ethylene oxide derivatives using renewable raw material (alcohol, molasses), guar gum derivatives, alcohol & spirits, industrial gases, and nutraceuticals.

While analysing the company, an investor comes across transactions of the company with its wholly-owned subsidiary, IGL Infrastructure Pvt. Ltd, which provides interesting insights to the investor.

While analysing the past annual reports of India Glycols Ltd., an investor notices that in FY2015, the company established a new wholly-owned subsidiary, IGL Infrastructure Pvt. Ltd (IGL Infra) and then transferred its commercial building (rental business division) to IGL Infra on March 31, 2015, for consideration of ₹184 cr.

FY2015 annual report, page 79:

On receipt of approval of the shareholders and NOIDA Authority, during the year the Company had entered into a Business Transfer Agreement (BTA) with wholly owned subsidiary company, IGL Infrastructure Private Limited (‘IGL Infra’) (formed during the current year) for sale of its Rental Business Division on slump sale basis w.e.f. 30 th Mar 2015 for consideration of ₹18,420.00 Lacs, pending receipt of the final ‘NOC’ from 2 banks (approval since received). The consideration has been included under Short Term Loans & Advances Receivable. Profit on sale this amounting to ₹5,194.26 Lacs is included under exceptional items. (Refer Note No. 46(d)).

As per the generally followed principles of consolidation, a wholly-owned subsidiary is included in the consolidated financials of the company. As a result, the transactions between the company and its wholly-owned subsidiaries are ignored while preparing consolidated financials i.e. whether a company keeps an asset on its own books or it transfers the asset to its wholly-owned subsidiary, its consolidated financials will not change.

However, in the case of the sale of rental business by India Glycols Ltd to IGL Infra, the company recognized this transfer as a sale to any third party. As a result, it recognized a profit of ₹52 cr in its consolidated financials due to this sale of assets to its wholly-owned subsidiary.

FY2015 annual report, page 113 (notes to consolidated financials):

On receipt of approval of the shareholders and NOIDA Authority, during the year the Company had entered into a Business Transfer Agreement (BTA) with wholly owned subsidiary company, IGL Infrastructure Private Limited (‘IGL Infra’) (formed during the current year) for sale of its Rental Business Division on slump sale basis w.e.f 30 th March 2015 for a total consideration of ₹18,420.00 Lacs, pending receipt of the final ‘NOC’ from 2 banks (approvals since been received). The consideration has been included under Short Term Loans & Advances Receivable. Profit on sale on this amounting to ₹5,194.26 Lacs is included under exceptional items. (Refer No. 46(d))

An investor is confused when she notices that the company has recognized profit on a sale transaction of assets to its wholly-owned subsidiary in its consolidated financials. To find the reasons, upon further reading of the annual report, an investor notices that the company did not consider IGL Infra in its consolidated financials for FY2015 despite it being its wholly-owned subsidiary.

FY2015 annual report, page 97:

For Consolidation IGL Infrastructure Pvt. Ltd., a wholly owned subsidiary has not been considered as the investment is held temporarily with a view to its subsequent disposal in the near future.

The company stated that it did not consider IGL Infra in its consolidated financials as it had plans to sell this subsidiary in the near future.

As a result, the company treated IGL Infra as a third party company and it recognized the profits of ₹52 cr in its profit and loss statement by merely transferring the rental business division to its wholly-owned subsidiary without the division actually being sold to any third party.

The company sold IGL Infra to its promoters in the next financial year in Sept 2015 (FY2016) because the company changed the status of IGL Infra in its related party details from a subsidiary to an enterprise controlled by key management personnel from Sept 15, 2015.

FY2016 annual report, page 89:

Relationship

A. Subsidiary Company

- IGL Infrastructure Private Limited (IGL Infra) (Ceased on 14.09.2015)

D. Enterprises over which Key Management Personnel have significant influence:

- IGL Infrastructure Private Limited.(IGL Infra) (w.e.f. 15.09.2015)

If the company had followed the normal customs of consolidation and recognition of profits on the sale of assets, then it would have recognized the sale of the rental business and its profit in its consolidated financials in FY2016 when IGL Infra was sold by the company to its promoters.

However, the company used different principles of consolidation and as a result, did not use IGL Infra for consolidation in FY2015 despite it being its wholly-owned subsidiary. Therefore, India Glycols Ltd recognized a profit of ₹52 cr in its consolidated financials in FY2015 by merely shifting the asset from its books to the books of a wholly-owned subsidiary, without doing an actual sale to any third party.

An investor would appreciate that due to these events, the company preponed the recognition of the profit of ₹52 cr from FY2016 to FY2015 before the actual sale of rental assets to any third party. One reason for the same could be that the company reported losses of (₹89 cr) during FY2015 and it might be an attempt by the company to show lower losses in FY2015 than what it might have had to report otherwise.

Nevertheless, it seems a case where the company did not have any profits from the sale of the rental business in FY2015 as the business was transferred to its wholly-owned subsidiary. However, the company recognised a profit of ₹52 cr in its consolidated financials by using an assumption that it would not consolidate its wholly-owned subsidiary in its financials. The company treated this asset transfer to the wholly-owned subsidiary as a sale to a third party in FY2015.

As a result, an investor would notice that the profit of the company for FY2015 became higher by ₹52 cr (i.e. it reported a loss lower by ₹52 cr) due to this assumption.

Cases like India Glycols Ltd further stress the need that an investor should read every line of the annual report so that she is able to identify different assumptions used by the company in preparing its financials. Only after reading these assumptions, she would be able to assess whether she can take the reported profits at the face value.

An investor may read the complete analysis of India Glycols Ltd in the following article: Analysis: India Glycols Ltd

C) Companies generate profits by some transactions where the occurrence of profit defies common sense:

Many times, investors would notice that companies report profits from certain transactions. However, when an investor puts the transaction to the basic scrutiny of the investing world, then she notices that the company might not have made profits in such a situation.

In such a situation, the investor should increase her level of due diligence and reassess her assumptions before taking any investment decision.

Let us see an example.

i) Datamatics Global Services Ltd:

While analysing the annual reports of Datamatics Global Services Ltd, an investor comes across a case of an issue of compulsory convertible preference shares (CCPS), which were later bought back by the company. This transaction provides interesting insights to the investors.

In the FY2014 annual report, an investor notices that Datamatics Global Services Ltd has raised money by issuing compulsory convertible preference shares (CCPS) worth ₹77 cr in one of the subsidiary companies.

FY2014 annual report, page 67:

Read: A Guide to Basics of Preference Shares / Preferred Shares

First, this issuance of CCPS comes as a surprise to the investor because as per the reported financials, Datamatics Global Services Ltd has always been a cash-rich company. At the end of FY2013, the company had a cash & investment balance of ₹87 cr, which increased to ₹136 cr at the end of FY2014.

An investor may believe that Datamatics Global Services Ltd might have raised the money by CCPS if it was a very low-cost source of funds. A low-cost source of funds may provide the company with interest rate arbitrage where the company can put this money in safe investments like fixed deposits with banks so that the company can earn a risk-free interest difference.

However, after reading further about the terms of the CCPS an investor notices that the CCPS provides for a reasonable return to the subscribers/investors in the form of an internal rate of return (IRR) of 9% to 16% per annum. FY2014 annual report, page 67:

Conversion / exit terms: In call option, the holders of the compulsorily convertible preference shares at any time after expiry of the lock in period and prior to September 30, 2015 (call option period), Datamatics Global Services Limited (DGSL) shall be entitled (but not be obligated) to exercise an option either by itself or through any affiliate to call upon the investors to sell all (and not less than all) their respective preference shares to DGSL and/or its Affiliate, which shall be a price per share which will yield an IRR of 16% per annum on the investor amount.

In put option, in the event of DGSL does not exercise the call option prior to the completion of the call option period, the investors shall have (1) the right to convert their respective preference shares into equity shares of LPSPL at conversion price determined based on the conversion ratio as specified in the Articles of association or (2) at any time after expiry of the call option period, but prior to December 31, 2015 (put option period), the right to exercise an irrevocable option (the put option) to require DGSL to purchase, either directly or through an Affiliate, all (and not less than all) their outstanding preference shares held by the investors at a price per share which will yield an IRR of 9% per annum on the investor amount.

Notwithstanding anything contained herein preference shares shall be compulsorily converted into equity shares of LPSPL after a period of 20 years from the date of issue of such preference shares

The above information indicates that the CCPS have stipulated call and put option:

- Datamatics Global Services Ltd may ask the investors/subscribers of CCPS by September 30, 2015, to sell these shares to it and in turn, Datamatics Global Services Ltd will provide 16% return per annum (IRR) to the investors.

- The investors may ask Datamatics Global Services Ltd to purchase the CCPS/convert them into shares by December 31, 2015, and in turn, Datamatics Global Services Ltd will provide them with a return of 9% per annum (IRR).

Therefore, an investor would appreciate that Datamatics Global Services Ltd has raised the money from CCPS by guaranteeing a short-term return of 9% to 16% to the CCPS subscribers.

On further analysis, an investor notices that in FY2017, Datamatics Global Services Ltd exercised its option to purchase the CCPS from the subscribers and as a result, the CCPS ceased to exist in the balance sheet.

FY2017 annual report, page 103:

The above information indicates that Datamatics Global Services Ltd has exercised its option (i.e. asked the subscribers to sell the CCPS to it). While reading the FY2017 annual report, an investor gets to know that the company had issued the CCPS for ₹77 cr and it had purchased/bought them back at a price of about ₹47 cr. (₹22 cr + ₹25 cr).

FY2017 annual report, page 90:

Attention is drawn to Note no. 34 wherein a subsidiary of the Company, had issued preference shares worth ₹ 771.76 million to outside shareholders in earlier year. During the year, the same was purchased / bought back by the Company/subsidiary for ₹ 217.80 million and ₹ 250 million respectively, resulting in total exceptional gain of ₹ 303.96 million. Considering the fact that preference shares are a financial liability and bought back from outside shareholders, the resultant gain is recognised as exceptional gain in the Consolidated statement of Profit and Loss

The above data indicate that Datamatics Global Services Ltd bought back the CCPS at a price of ₹47 cr. (₹22 cr + ₹25 cr) and as a result, it recognized a gain of ₹30 cr (30 = 77 – 47) on this transaction. The company reported a gain because it paid back only ₹47 cr against ₹77 received by it when it issued CCPS.

As per the original terms of the CCPS, an investor would remember that in the situation when Datamatics Global Services Ltd asks the subscribers to sell the CCPS to it, then it had to give a return of 16% per annum (IRR) to the subscribers. However, this guaranteed return was applicable only until September 30, 2015, whereas the company bought back the CCPS in FY2017.

Therefore, it may seem to the reader that Datamatics Global Services Ltd is no longer bound to give the guaranteed return of 16% to CCPS subscribers.

However, if an investor notices that over the period during which CCPS were outstanding i.e. FY2014 to FY2017, the performance of Datamatics Global Services Ltd had improved as indicated by the following parameters:

- Total sales of the company increased from ₹734 cr in FY2014 to ₹852 cr in FY2017.

- Net profit after tax (PAT) of the company increased from ₹49 cr in FY2014 to ₹65 cr in FY2017.

- The total debt of the company declined from ₹91 cr in FY2014 to ₹55 cr in FY2017.

- The cash & investments of the company increased from ₹134 cr in FY2014 to ₹140 cr in FY2017.

- The share price of Datamatics Global Services Ltd increased from ₹49.30 on March 31, 2014 (closing price on BSE) to ₹128.15 on March 31, 2017 (closing price on BSE) representing an increase of about 160%.

In light of all these positive developments related to Datamatics Global Services Ltd from FY2014 to FY2017, it comes as a surprise that the subscribers of the compulsory convertible preference shares (CCPS) agreed to take a loss of ₹30 cr on their investment of ₹77 cr in CCPS.

It seems counterintuitive that the subscribers of CCPS had to take a loss on their investment while the business performance of Datamatics Global Services Ltd is improving and its share price is increasing. In addition, the CCPS subscribers had an option to convert the CCPS to equity shares and then sell these shares in the stock market to recover their investment. When the share price of Datamatics Global Services Ltd increased by 160% from FY2014 to FY2017, then it is difficult to understand why the CCPS subscribers took a substantial loss of about 40% on their investment (30/77 = 39%).

It is advised that investors may do further analysis of the CCPS transaction and may contact the company directly to understand more about the reasons why the CCPS subscribers accepted a loss while the business, as well as the stock price performance of the company, was improving.

The above case highlights the importance of in-depth reading of annual reports to an investor so that she is able to make her own opinion about the transactions reported by the company in its financial statements.

An investor may read the complete analysis of Datamatics Global Services Ltd in the following article: Analysis: Datamatics Global Services Ltd

D) Companies show losses from investments/subsidiaries in the P&L, but nullify their impact on profits:

Similar to the cases discussed above where companies resorted to using reserves to set off certain expenses to inflate their profits, many times, companies use similar conventions to nullify the losses suffered by them on account of their investments in subsidiaries etc.

An in-depth analysis of the financial statements of the companies will indicate to the investor that in such cases, the companies show the loss in the P&L but simultaneously show a transfer entry shifting an amount from the reserves to the P&L, which is usually exactly equal to the mentioned expense. Many times, companies create a special reserve for this purpose.

The net result is that the transfer from the reserves overcomes the impact of reduction by the losses shown in the P&L. As a result, the profit of the company remains unaffected.

Let us see some examples.

i) Escorts Ltd.

Escorts Ltd is an Indian company involved in the manufacturing of tractors & agricultural machinery, construction equipment and railways equipment.

While analysing the company, an investor comes across transactions related to one of the subsidiaries of Escorts Ltd, Escorts Agri Machinery Inc. (USA) (EAMI), which had become bankrupt. As a result, Escorts Ltd had to take over all the liabilities of EAMI. The transactions in relation to EAMI provide a few learnings to the investors.

In the past, the wholly-owned subsidiary (100% owned) of Escorts Ltd in the USA, EAMI, could not perform as per expectations. As a result, Escorts Ltd merged EAMI in itself in FY2009.

After this merger was over, then Escorts Ltd disclosed that it had to absorb losses/write-offs to the extent of ₹641.82 cr (= 156.53 + 485.29) in FY2009. Moreover, there were additional losses in subsequent years on account of EAMI.

FY2009 annual report, page 98:

EAMI has been amalgamated with the Company with effect from the appointed date. EAMI is an investing company holding other overseas operational companies. On amalgamation, all the subsidiaries of EAMI have become direct subsidiaries of the Company. The amalgamation has been accounted for under the ‘Pooling of Interest Method” in accordance with AS-14 Accounting for Amalgamations. Accordingly, all the assets and the liabilities of EAMI have been taken at their book value as appearing in the books of EAMI on the appointed date, based on their unaudited financial statements. The entire share capital of EAMI and investment in the equity share capital of EAMI as appearing in the books of EL stands cancelled and inter se amount of loans, advances and other current account balances of EAMI with the Company also stand cancelled. EAMI being the wholly owned subsidiary of the Company no consideration is required to be paid.

As envisaged by the aforesaid Scheme, a separate reserve account titled “Business Reconstruction Reserve” (BRR) has been created by transferring amounts lying to the credit of Revaluation Reserve, Amalgamation Reserve, Capital Redemption Reserve and Shore Forfeiture Reserve with effect from the appointed date. The Compony has got its immovable properties in the form of Land & Buildings valued by a reputed independent valuer resulting in net addition of Rs. 672.72 crores to their book value as on the appointed dote. The corresponding credit has been given to the BRR.

Business Reconstruction Reserve has been utilised to adjust profit and loss account debit balance of Rs.156.73 crores brought forward from earlier years. An amount of Rs. 485.29 crores has also been utilized from BRR to adjust the difference between the value of assets and liabilities taken over upon amalgamation, provision/write down/write off in the valve of the fixed assets, investments, current assets, loans and advances, excess depreciation on the account of revaluation of the fixed assets and all the expenses incurred in carrying out and implementing the Scheme as detailed in Schedule-2 “Reserves &Surplus” and Schedule- 17 “Exceptional Items”.

Investors would note that in FY2009, Escorts Ltd recognized a total diminution in the value of ₹641.82 cr out of which ₹156.53 cr was accumulated losses and another ₹485.29 cr was on account of impairment of assets, investments, excess liabilities etc. An investor would note that the deterioration of the value of the assets of the wholly-owned subsidiary, EAMI of ₹485.29 cr was already there on the ground in the USA even before FY2009. However, the company recognised this impairment/loss recognized in the financials only at the time of the merger in FY2009 when EAMI became bankrupt.

This seems a case where the company delayed the acknowledgement of poor performance and loss of investment value in its subsidiary until the last moment instead of recognizing it during the previous years when the actual impairment was taking place. As a result of not acknowledging this deterioration in the financial position of the subsidiary in the previous year, Escorts Ltd could present a better financial picture to the investors.

Moreover, from the above disclosure, an investor would notice that the company created a special reserve, business reconstruction reserve (BRR) and the company adjusted these losses directly to BRR in the balance sheet by bypassing the profit and loss statement.

As a result of this bypassing of losses from the profit and loss statement using BRR, the company could report higher profits.

The auditor of the company highlighted this aspect in its report in the annual report where the auditor mentioned that such a treatment of the write-offs directly to the balance sheet bypassing profit & loss statement, though approved by the Honorable High Court, is not as per the accounting standards.

FY2009 annual report, page 77:

In our opinion, the Balance Sheet, Profit & Loss Account ond Cash Flow Statement dealt with by this report comply with the Accounting Standards referred to in subsection (3C) of Section 211 of the Companies Act, 1956, except accounting treatment as described above regarding creation and utilization of Business Reconstruction Reserve pursuant to a scheme of arrangement as duly sanctioned by the High Court of jurisdiction.

It seems that the amount of loss recognized in FY2009 (₹641.82 cr) did not reflect the entire loss of value as in FY2012; the company had to recognize another value erosion of ₹369.79 cr. In FY2012 as well, Escorts Ltd adjusted the value erosion/write-off directly to the balance sheet in BRR bypassing the profit and loss statement.

FY2012 annual report, page 74:

Pursuant to the Scheme of Arrangement (Scheme) under Sections 391 to 394 which has been approved by the Hon’ble High Court of Punjab & Haryana vide its Order dated 17th September 2009, an amount of ₹ 369.79 crores on account of, receivables, fixed assets, inventories, loans & advances which is doubtful of recovery/realization has been provided for/written off and adjusted through Business Reconstruction Reserve.

Had the Scheme not prescribed for the aforesaid accounting treatment as approved by the Hon’ble High Court, the balance sheet (including reserves & surplus) and the statement of profit and loss would have been impacted to that extent.

Therefore, an investor would notice that in the case of EAMI, Escorts Ltd suffered losses to the extent of ₹1,000 cr, which were directly adjusted in the balance sheet bypassing the profit & loss statement.

Had the Honorable High Court not permitted this adjustment, then the profit performance of the company as represented by the P&L would have looked very different. Moreover, while assessing the overall cumulative profitability of the company over the years, investors may make adjustments accordingly at their end.

This aspect of significant write-offs adjusted to the balance sheet has been highlighted by credit rating agencies as well.

ICRA in its report of March 2016 for the company stated that any balance sheet adjustment of write-offs like the one done in the past via BRR is an event risk for assessment of Escorts Ltd.

ICRA March 2016 report, page 1:

Going forward, EL’s ability to divest the loss-making auto components segment without any substantial write-off or any major debt-funded inorganic expansion would remain key rating sensitivities. Further, any balance sheet adjustment, similar to write-offs from BRR in the past, is an event risk.

Therefore, it is advised that investors should go beyond the reported financial numbers in the tables in the annual reports and read all the notes, assumptions, observations by the auditors etc., so that they may assess the full nature of financial transactions of the company and take a decision accordingly.

An investor may read the complete analysis of Escorts Ltd in the following article: Analysis: Escorts Ltd

E) Companies delay acknowledgement of losses on their investments until the last moment:

As discussed in the case of Escorts Ltd above, many times, investors would notice that companies keep carrying those investments at their original value, which might have lost their entire worth many years back. Investors would notice that in such cases, auditors of the company and even regulators like stock exchanges highlight this issue to the company. However, some times, management of the company do not reverse their stance despite many signs that the investment has lost its value.

Then one day, the management finally realises that it can no longer carry the investment on its original cost, and then it acknowledges its losses many years after the original loss of investment.

In such cases, an investor would notice that the financial statements of the company for all the preceding years represented a higher profit than the actual financial position. This is because the investment of the company had lost its worth many years back and the company should have recognized losses in the preceding years. As a result, the profits of the preceding years remain inflated.

Let us see another example of such a situation where the company delayed acknowledging the loss of its investments in its subsidiaries to the last minute.

i) India Glycols Ltd:

While analysing India Glycols Ltd, an investor notices that during FY2010-2019, India Glycols Ltd made many investments in its subsidiaries/outside entities, which ultimately resulted in losses. However, as discussed below, an investor would notice that the company delayed in recognition of these losses in the investment value until the very last moment when a change in accounting standards mandated it to provide for these losses.

- IGL Finance Ltd (IFL)/National Spot Exchange Ltd (NSEL): Over the years, India Glycols Ltd has invested about ₹150 cr in IFL by way of equity and inter-corporate deposits. IFL primarily invested this money in the contracts offered by National Spot Exchange Ltd (NSEL). In 2013, the govt. sensed a fraud in NSEL and shut down the exchange. NSEL defaulted on its obligations and as a result, the investors in its contracts are yet to recover their money. Therefore, the investments done by India Glycols Ltd in NSEL via IGL Finance Ltd represent a loss of the money generated by the company from its operations.

FY2019 annual report, page 101:

In earlier year the company had given (included in current Loan) Inter Corporate Deposit (ICD) of ₹14,649.64 Lakhs (Previous Year ₹14,649.64 Lakhs) to its subsidiary IGL Finance Ltd. (IGLFL) (A 100% subsidiary). IGLFL in earlier year had invested funds for short term in commodity financing contracts offered by National Spot Exchange Ltd. (NSEL). NSEL had defaulted in settling the contracts on due dates, for which IGLFL has initiated legal and other action and in turn IGLFL did not pay back due amount to the company. Accordingly considering the prudence no interest on above ICD has been accrued for the period from 01-09-2013 onwards.

- Shakumbari Sugar and Allied Industries Limited: in FY2008, India Glycols Ltd purchased a sugar mill, Shakumbari Sugar and Allied Industries Limited (SSAIL) for backward integration. Over the years, India Glycols Ltd invested about ₹160 cr in SSAIL by way of equity, preference share capital, inter-corporate deposits, and advances. By FY2012, SSAIL shut down its operations, its net-worth was fully eroded, it defaulted to its lenders and was declared sick/bankrupt. Now, India Glycols Ltd has written off its entire investment in SSAIL. The investment in SSAIL represents the loss of the money earned by India Glycols Ltd from its operations.

FY2019 annual report, page 101:

(i) Company has Investment of ₹5,427.50 Lakhs (Previous year ₹5,427.50 Lakhs) in equity share capital and 10% cumulative redeemable preference share capital in subsidiary company namely Shakumbari Sugar and Allied Industries Limited (SSAIL) whose net worth has been fully eroded and SSAIL has also been declared sick industrial undertaking as per provision of Sick Industrial Companies Act. 1985.

(ii) In earlier year, the company has also given to SSAIL-Inter corporate deposit (ICD) amounting to ₹1,915.13 Lakhs (Previous Year ₹1,915.13 Lakhs) (including interest thereon) and advances of ₹8,453.81 Lakhs (Previous Year ₹8,453.81 Lakhs) and also corporate guarantee extended of ₹ Nil (Previous Year ₹3,749.34 Lakhs) (excluding penal interest, penalty etc). No due certificate from Central Bank of India is awaited.

(iii) Based upon the application and adoption of fair value of the aforesaid investment, ICD and advances are carried at nil value.

SSAIL defaulted in repayments to its lenders (FY2014 annual report, page 92):

As stated above and in view of financial tightness SSAIL could not pay on time and made default in repayment of:

i) Principal:- Central Bank of India ₹742.11 Lacs (Apr-13 to Mar-14), Axis Bank ₹177.90 Lacs (Jan-14 to Mar-14) & IDBI Bank ₹208.33 Lacs (Jan-14 to Mar-14)

ii) Interest :- Central Bank of India ₹5.41 Lacs (Apr-13 to Mar-14), Axis Bank ₹40.57 Lacs (Feb-14 to Mar-14) & IDBI Bank ₹53.95 Lacs (Feb-14 to Mar-14)

The lenders initiated recovery proceedings against SSAIL (FY2015 annual report, page 113):

Central Bank of India (CBI) vide its letter dated 28.05.2014 had issued a notice under Section 13(2) of SARFAESI Act 2002 to SSAIL and IGL. The said notice was replied by SSAIL and IGL has challenged the legality of issuance of such notices. CBI, thereafter, on 11.09.2014 had issued another notice under Section 13(4) of SARFAESI on SSAIL and IGL, which has been challenged in DRT, Lucknow. As per the legal opinion, the notice is not valid since SSAIL has already been registered with BIFR as sick Company.

By looking at the above information, an investor would acknowledge that the investment decisions of India Glycol Ltd in NSEL and SSAIL did not work well for the shareholders and the company lost a lot of money due to these investments.

However, an investor notices that India Glycols Ltd did not acknowledge it in its financial statements until many years. It was only in FY2017 when the company adopted Indian Accounting Standards (IndAS), then due to the mandatory adoption of a fair value approach, the company provided for/wrote off these investments.

a) Investment in National Spot Exchange Ltd in NSEL via IGL Finance Ltd:

The company wrote off its investment in NSEL in FY2017 upon adoption of IndAS.

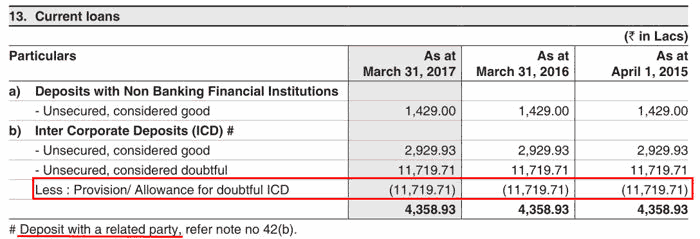

FY2017 annual report, page 16:

On date of transition to Ind-AS, based on the expected credit loss policy and other estimation made by the IGLFL management, IGLFL has made a provision of ₹11,719.71 lacs against the total outstanding of ₹14,444.43 lacs from NSEL. Simultaneously, the same amount has been provided for against ICD’s received from the Holding Company. IGLFL is confident of recovery of its dues from NSEL over a period

An investor may note that the NSEL fraud took place in 2013 and the company could make a recovery of only about ₹10 cr in FY2015.

FY2015 annual report, page 11:

Company has so far recovered ₹10.31 Crores from NSEL.

Since then, it seems the company did not receive any money from NSEL; however, the company hesitated to write-down this investment until the new accounting standards (IndAS).

An investor may believe that during this period of FY2013-2017, the company did not recognize the loss/write-down of the money due from NSEL and as a result, the financial statements of the company kept on reflecting that the entire investment in NSEL is safe. Investors may note that such delay in the non-recognition of the write-off of investments in NSEL presented a better picture of the financial position of the company than it actually was.

Moreover, the auditor of the company have repeatedly questioned such non-recognition of losses on the investment done in NSEL since FY2014 and highlighted the same in its audit reports.

FY2014 annual report, page 69:

Basis for Qualified Opinion:

Attention is invited to Note no 47 regarding non provision against total exposure amounting to ₹14,503.44 lacs in NSEL, where the management is confident about its recoverability for the reason as stated in said note, and our inability to comment thereon.

The National Stock Exchange (NSE) took up this matter and asked the company to revise its financials in the light of observations of the auditor. However, the company contested the objections of NSE and did not revise the financials.

FY2015 annual report, page 113:

Company has received letters dated 30th Oct 2014 and 05th May 2015 from National Stock Exchange of India (NSE), wherein the Company has been advised to reinstate its financials w.r.t. qualification raised by the statutory auditor of the company for the years FY 2012-13 on investments and loans to SSAIL and to suitably rectify the qualification raised for the year FY 2013-14 by the statutory auditor w.r.t. investment and loan to IGLFL respectively. For SSAIL, the Company has written letters to NSE for granting opportunity to represent the case and for IGLFL the Company has requested NSE to clarify the issue for effect to their directive.

Finally, the company has to recognize the loss in the value of its investments only when it adopted the new accounting standards (IndAS), which have stringent fair valuations criteria.

Nevertheless, an investor would notice that the company has recognized the reduction in the value of its investments directly in the balance sheet without recognizing it as a loss in the profit and loss statement.

FY2017 annual report, page 77:

Looking at the above table, an investor would notice that the company has recognized the non-recoverability of the inter-corporate deposits (₹117.19 cr) in the balance sheet. However, when the investor analyses the profit and loss statement (see the table below), then she notices that the P&L does not have the deduction of ₹117.19 cr as an expense. Instead, the relevant section for recognition of losses on investments/advances etc. in the P&L recognizes losses of only about ₹2 cr in FY2017 and about ₹13.5 cr in FY2016.

FY2017 annual report, page 85:

Please note that the practice of the company to recognize losses on investments directly to the balance sheet without affecting the P&L may not be against the law. The company would have used the discretions provided to the management under the law for the recognition/classification of these items.

Nevertheless, irrespective of the method of representation in the financial statements, investors should remember that the money, which was invested by the company in NSEL, for which there is a very low probability of recovery, is effectively a loss of money. Therefore, investors may make suitable adjustments in their analysis.

b) Delays in the write-off of investments in Shakumbari Sugar and Allied Industries Ltd:

India Glycols Ltd has followed a similar approach with respect to its investments in Shakumbari Sugar and Allied Industries Ltd. (SSAIL) where it invested about ₹160 cr in SSAIL via different instruments.

SSAIL stopped its operations in FY2012. It started defaulting to its lenders. Its net worth was fully eroded. It was referred to the Board for Industrial and Financial Reconstruction (BIFR) as a sick company. Its banker, Central Bank of India initiated legal proceedings to recover its money (SARFAESI Act). The statutory auditor started highlighting the doubtfulness of recovery of its investments in SSAIL since FY2013.

FY2013 annual report, page 36:

Qualification

Attention is invited to Note no. 34 of financial statements regarding non-provision against investment and loans & advances in subsidiary company Shakumbari Sugar and Allied Industries Limited (SSAIL) amounting to ₹5,427.50 Lacs and ₹1,713.30 Lacs (including interest accrued thereon) respectively,…

Net Profit for the year, investments, loans & advances and reserve & surplus are without considering the above which cannot be ascertained or otherwise for the reason stated in para above.

As discussed above, the National Stock Exchange (NSE) took up this matter and asked the company to revise its financials in the light of observations of the auditor. However, the company contested the objections of NSE and did not revise the financials.

Finally, with the adoption of new accounting standards (IndAS), the Company recognized impairment/losses on its investments in SSAIL. Nevertheless, the company recognized these losses directly in the balance sheet without affecting the profit and loss statement.

Once again, investors may note that while recognizing these write-offs, the company may not have acted against the law. Instead, it may have used the discretions allowed to the management under the law for recognition/classification of these items.

However, investors will remember that the money once gone from the company, which it cannot recover, is a loss and therefore, investors can make suitable adjustments in her analysis.

Upon further analysis of the financials of India Glycols Ltd, an investor notices that in FY2018, the company recognized a profit on the one-time settlement (OTS) scheme offered by Central Bank of India to SSAIL under other income i.e. routed it through profit and loss statement, which results in showing higher profits of the company.

FY2018 annual report, page 134:

The recognition of gain on one-time settlement by the company in FY2018 comes as a sharp contrast to its hesitation to recognize losses on its investments despite multiple observations by the auditors, follow up by stock exchanges etc. This is also pertinent in the light that Central Bank of India had not yet closed the matters on “One Time Settlement” at its end, as in the FY2019 annual report, the company highlighted that the bank has asked for further money from the company.

FY2019 annual report, page 145:

During the year, the Subsidiary Company (Shakumbari Sugar & Allied Industries Limited) paid the remaining amount in full in respect of one time settlement (OTS) amount of ₹ 4200.00 Lakhs to Central Bank of India in pursuance of OTS entered during previous year. However, the Bank has further demanded ₹ 208.86 Lakhs for uncharged commission on bank guarantees. The said Company has filed a writ petition against the said demand in the High Court, Allahabad.

Therefore, while analysing the events, an investor notices that the company has attempted to defer recognition of losses on its non-performing investments as long as possible despite observations from the auditor and national stock exchange. Even when it had to recognize the losses on these investments, then it deducted the provisions/write-offs directly to the balance sheet without affecting the profit and loss statement.

On the contrary, the company recognized the profits/gains on the one-time settlement scheme from the bank immediately in its profit and loss statement even though the bank has still not settled all the dues at its end.

Therefore, an investor would acknowledge that she should be very cautious while taking the reported financial numbers by companies at the face value. She should always study the annual reports in detail and then make up her opinion about the financial position of any company.

An investor may read the complete analysis of India Glycols Ltd in the following article: Analysis: India Glycols Ltd

3) Companies report higher profits by not making expenses that they are required to do

Many times, investors would come across cases, where the companies do not do spending related to expenses mandated by the law like corporate social responsibility (CSR) expenses.

Companies avoid spending on CSR citing one reason or the other, in turn, reducing their expenses, and thereby, inflate their profits.

Let us see some examples:

i) India Glycols Ltd:

In the FY2019 annual report, while analysing the CSR section, an investor notices that India Glycols Ltd has disclosed that it does not have any CSR liability for FY2019 as it has suffered an average net loss of ₹70.8 cr for the last three years.

FY2019 annual report, page 35:

3. Average net profit/loss of the company for last three financial years: The average net loss of the Company for the preceding three financial years was ₹ 7,083.38 Lakhs.

4. Prescribed CSR expenditure (2% of the amount as in item no.3 above): Nil

5. Details of CSR spent during the financial year:

(a) Total amount to be spent for the financial year: Nil

(b) Amount unspent, if any: N.A.

(c) Manner in which the amount spent during the financial year is detailed below: In view of the average loss during the last 3 financial years, the Company was not under any obligation to spend any amount on the CSR activities during the FY 2018-19, however, the Company has voluntarily contributed Rs 65.87 Lakhs on the following activities under CSR:

However, an investor notices that India Glycols Ltd has reported profits for each of the last three years.

- FY2019: net profit after tax (PAT) of ₹133 cr

- FY2018: PAT of ₹97 cr

- FY2017: PAT of ₹35 cr

Therefore, it seems that the disclosure by the company in FY2019 that it has suffered an average net loss of ₹70.8 cr for the last three years may not be correct.

An investor may contact the company directly for further clarification.

However, if the company is required to spend money on CSR and it avoids spending the money, then the company is effectively declining mandatory expenses and inflating its profits.

An investor may read the complete analysis of India Glycols Ltd in the following article: Analysis: India Glycols Ltd

ii) Datamatics Global Services Ltd:

While analysing the annual reports of the company, an investor notices that Datamatics Global Services Ltd has not spent the full eligible amount on corporate social responsibility (CSR).

When an investor tries to find out the reasons for such non-spending, then she gets to know that the company has cited lower profit margins of the company, increasing costs and the need to conserve resources of the company to deploy in future growth as the reason for not spending full money on CSR.

FY2019 annual report, page 35-36:

In case the Company has failed to spend the two per cent of the average net profit of the last three financial years or any part thereof, the company shall provide the reasons for not spending the amount in its Board report :-

……However, the global economic competition has induced the corporates to become cost conscious. During the year under review, the margins of the Company have been reduced on account of increase in various costs. The Company’s growth is dependent on the Company’s capability to use the Company’s resources in a channelized manner. Therefore, considering the financial condition and goals of the Company, the Board of Directors have thought it prudent to conserve the resources of the Company so that they can be deployed for various future growth initiatives and expansion plans by targeting new customer segments and markets across different geographies.

An investor notices that the company CSR expenditure liability of the company for FY2019 was ₹0.79 cr. Out of this amount the company spent only ₹0.12 cr and did not spend the remaining ₹0.67 cr so that it could be conserved to deploy in future growth plans.

FY2019 annual report, page 35:

Prescribed CSR Expenditure (2% of this amount as mentioned in Sr. No. 3 above): ₹ 7.85 million.

Details of CSR spent during the financial year:

(a) Total amount spent for the financial year: ₹ 1.21 million.

(b) Amount unspent: ₹ 6.64 million.

(c) Manner in which the amount spent during the financial year is detailed below.

An investor notices that Datamatics Global Services Ltd has been a cash-rich company and had a cash & investment balance of ₹130 cr on March 31, 2016. The company had a bank balance of more than ₹68 cr on March 31, 2019.

FY2019 annual report, page 92:

An investor may appreciate that the company has a large amount of ₹68 cr in the bank balance and it refuses to spend a comparatively minuscule ₹0.67 cr on CSR citing that the company needs to conserve these funds to deploy for future growth.

Similarly, the company did not spend comparatively minuscule amounts of ₹0.52 cr in FY2017 and ₹0.53 cr in FY2018 citing that it needs these funds for funding future growth plans. Datamatics Global Services Ltd had a bank balance of ₹67 cr in FY2017 and ₹81 cr in FY2018.

FY2018 annual report, page 109:

The hesitation of Datamatics Global Services Ltd in spending a comparatively minuscule amount on CSR despite having large bank balance may be interpreted in any of the following probable ways:

- The cash and bank balance of the company disclosed by it are suspect and the company is striving to conserve every penny to survive OR

- The company does not have the willingness to spend even comparatively minuscule amounts on CSR.

An investor may analyse these scenarios and draw her own conclusions.

If Datamatics Global Services Ltd does not have the willingness to spend money on CSR even though it is very small compared to its profits and bank balance, then it seems that such cases had led to the govt. to make non-spending of CSR money a criminal offence in its budget of July 2019.

However, recently, the govt. has proposed that CSR norm violations will not be treated as a criminal offense. Instead, these will be treated as civil offenses.

Nevertheless, an investor should acknowledge that if the company is not willing to spend even minuscule money on CSR, then it indicates that the company is willing to go to any extent to report high-profit margins.

An investor may read the complete analysis of Datamatics Global Services Ltd in the following article: Analysis: Datamatics Global Services Ltd

4) Companies inflate profits by changing accounting policies whenever it suits them even if the auditors highlight it

Many times, while analysing companies and reading annual reports, an investor would come across situations where the auditor of the company will highlight that the company has changed an accounting assumption during the year, which has an impact of inflating the profit or showing a lower loss during the financial year.

Investors should focus on such observations by the auditors of the companies and incorporate these learnings into their investment decisions.

Let us see an example.

i) India Glycols Ltd: