GRM Overseas Ltd (GRM), one of India’s leading rice exporters and branded rice players, has attracted a lot of investor attention due to a significant improvement in business performance after Covid and the launch of its domestic branded business under the “10X” brand.

Our experience shows that during periods of euphoric narratives, investors may at times overlook and underestimate key risks that can become important in the long term. As a result, the current article focuses on some of the aspects that a long-term investor should examine closely before forming an opinion about the company.

Please note that this analysis is not intended to arrive at a buy or sell conclusion. Instead, it aims to highlight commonly overlooked factors that tend to get ignored during periods of strong business growth.

Key Risks Long-Term Investors Should Examine

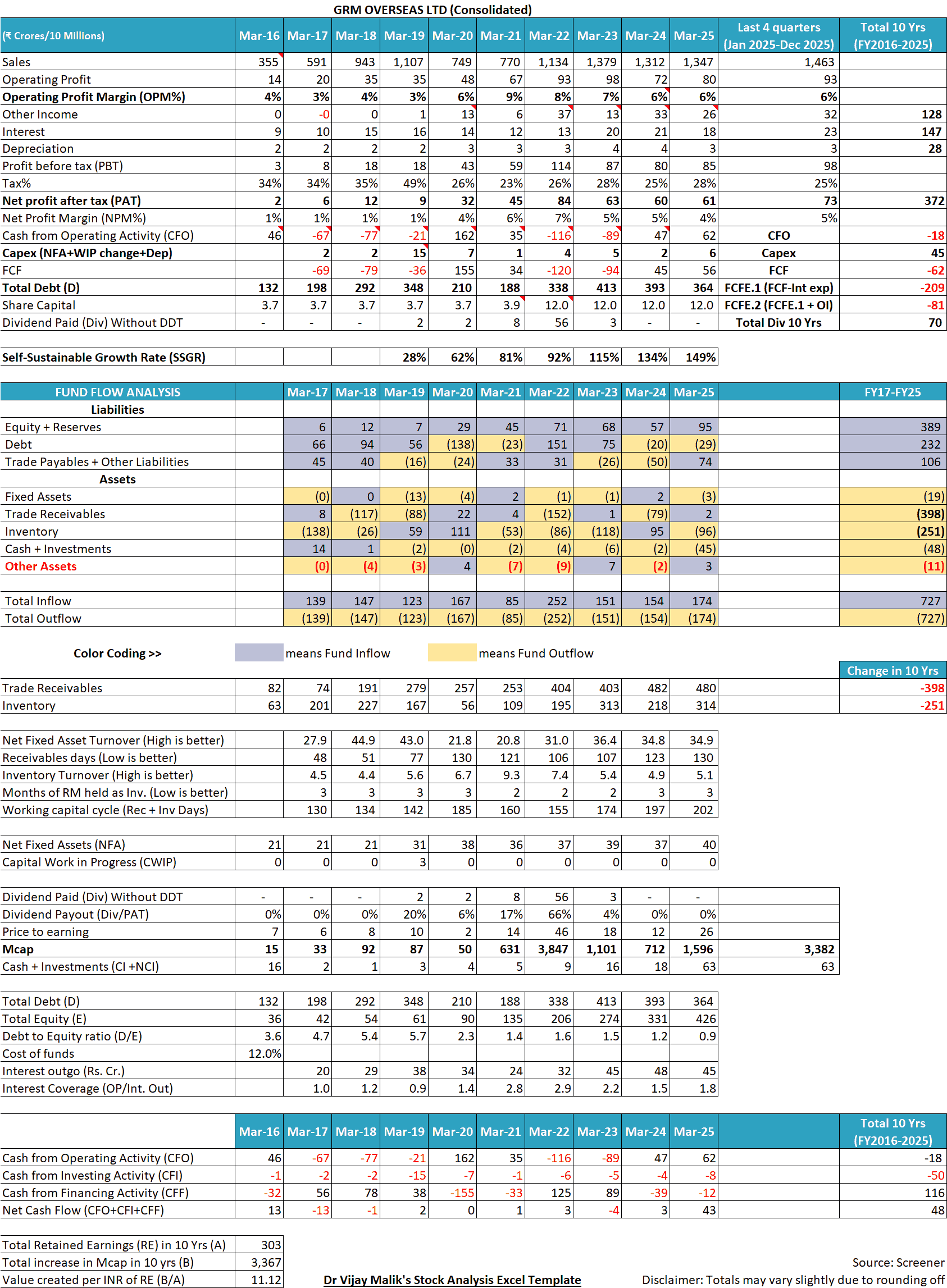

A snapshot of the financial performance of GRM Overseas Ltd over the last 10 years is provided below to set the context for the discussion that follows:

1) Limited Pricing Power of GRM Overseas Ltd in the Basmati Rice Business

Business of basmati rice is highly competitive where GRM faces intense price-based competition from numerous unorganized players as well as from other larger established Indian as well as Pakistani companies like KRBL Ltd (India Gate), Chaman Lal Setia Exports Ltd (Daawat) in both domestic as well as in exports markets (Annual report (AR) 2019, p.5, AR2003 p.10).

Due to this, until now, GRM has not been able to establish a significant branded presence in its key markets, both exports and domestic. In exports, about 95% of the company’s business is supplying rice for private labels of large superstores.

Selling to private labels is a commodity business where the customer can easily switch suppliers if they get acceptable quality at a lower price. As a result, whenever input costs increase, GRM Overseas Ltd has to take a hit on its profit margins (AR2024, p.6).

International grains market faced significant uncertainties, which drove up commodity prices, while inflation persisted throughout the year. These factors pressured our margins in FY24.

Due to its low pricing power, the company is losing out on the improvements in the operating profit margins (OPM) that it had achieved during Covid times. OPM used to be about 3-6% before Covid, which increased to about 9% during Covid and is now again down to 6%.

When pricing power is limited, businesses often compensate through volume growth, which typically increases working capital requirements. This linkage becomes important while analysing GRM’s cash flow profile.

Investor takeaway:

Long-term investors should remember that businesses mainly supplying to private labels work similar to commodity businesses. In such industries, growth in volumes does not necessarily translate into sustained profitability because customers can switch suppliers easily. Whenever input costs rise or competitive intensity increases, their margins are hurt. Therefore, before projecting future profitability, investors should determine whether the company has true pricing power or whether everything is dictated by the buyers.

Also read: How to do Business Analysis of a Company

2) When Growth Consumes Cash: The Working Capital Reality of GRM Overseas Ltd:

Among all aspects discussed in this article, the cash flow behaviour of GRM Overseas Ltd provides the best insights into its business model because cash flow ultimately reflects whether growth creates economic value or merely expands balance sheet size.

GRM’s business requires a large amount of working capital due to both significant inventory requirements and providing long credit periods to its customers.

Good quality basmati rice requires storage/ageing for multiple years to bring out the best flavour. Additionally, rice is a seasonal agricultural product. Therefore, GRM Overseas Ltd has to purchase rice in bulk to meet year-long requirements as well as store it over long periods, which increases its inventory levels significantly.

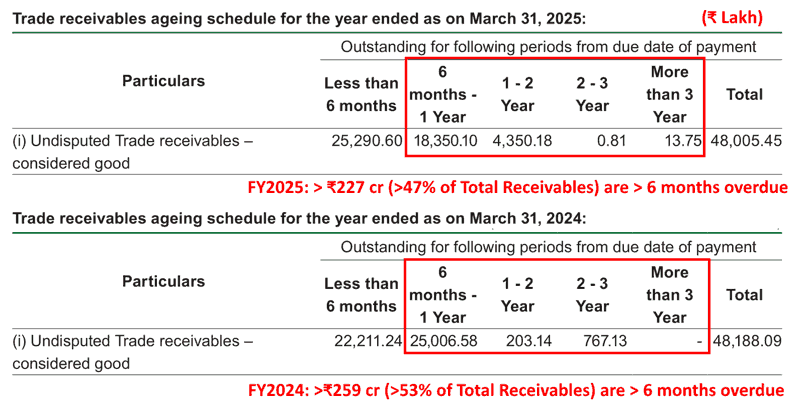

Additionally, the company has to give long credit periods to its customers, at times, even more than 90 days (Credit rating report (CR) by Acuite, August 2022).

GRM has low negotiating power against its large customers like Walmart, TESCO, Carrefour etc. (AR2019, p.5). As a result, its receivables are frequently further delayed over its credit period.

In recent times, more than 50% of its receivables have been more than 6 months overdue from their payment date. AR2025, p.223:

Over the years, the receivables collection efficiency of GRM Overseas Ltd has deteriorated as its receivables days have increased from 48 days in FY2017 to 130 days in FY2025.

As a result, any growth shown by GRM leads to an even larger amount of money getting stuck in its working capital. Over the last 10 years (FY2016-FY2025), the sales of the company grew by 3.8 times from ₹355 cr to ₹1,347 cr. During the same time, trade receivables of the company increased to 5.8 times from ₹82 cr to ₹480 cr.

In fact, despite reporting a cumulative net profit after tax (cPAT) of ₹372 cr during the last 10 years (FY2016-FY2025), GRM reported a negative cumulative cash flow from operations (cCFO) of (₹18) cr.

Investor takeaway:

Long-term investors should note that revenue growth alone does not create shareholder value if increasing sales require disproportionately higher investment in inventory and receivables. In working-capital-intensive businesses, growth can actually consume more cash instead of generating it, making the company financially weaker despite reporting higher profits. Long-term investors should always analyse whether incremental growth releases cash or locks more capital inside the operating cycle, because sustainable compounding ultimately depends on cash generation rather than mere balance sheet size expansion.

Also read: Understanding Cash Flow from Operating Activities (CFO)

3) Profit vs Cash Flow: Why the Reported Growth of GRM Overseas Ltd requires External Funding

Due to negative cash flows, GRM Overseas Ltd is not able to sustain its growth aspirations from internal accruals and becomes dependent on external funding, such as incremental debt and equity dilution.

Over the last 10 years, it raised ₹232 cr as additional debt, as its total debt increased from ₹132 cr in FY2016 to ₹364 cr in FY2025.

Additionally, it raised about ₹150 cr by equity dilution by issuing warrants for ₹12.5 cr in 2021 and for ₹136.05 cr in 2025-2026 (AR2021, p.103; CR Acuite, April 2025). Each of these rounds of warrant allotment diluted the stake of existing minority shareholders.

Investor takeaway:

A continuous gap between reported profits and operating cash flows indicates that a business model may not be self-sustaining. When internal cash generation is insufficient, companies are forced to rely on debt or equity dilution to fund growth. While such funding can support business expansion temporarily, a prolonged dependence on external capital shifts risk toward minority shareholders via high leverage or stake dilution. Investors should therefore evaluate not just whether a company is growing, but whether it can finance that growth from internally generated cash over time.

Also read: Free Cash Flow: A Complete Guide to Understanding FCF

4) Capital Allocation Decisions and Promoter Incentives:

GRM Overseas Ltd has been using funds from equity dilution into seemingly non-core activities like investments in Tobox Ventures Private Limited, running an office cafeteria management SaaS software: GoKhana (₹11.8 cr, AR2023, p.189) and Rage Coffee (₹10 cr, AR2025, p.166).

Within a short time, GRM Overseas Ltd sold its investment in Tobox for ₹8 cr at a loss of ₹3.8 cr to shareholders (AR2025, p.208, 221).

Moreover, the company plans to invest about ₹200 cr on such digital-first, non-core businesses around lifestyle and wellness concepts (AR2025, p.8).

GRM plans to invest INR 200 crore…The objective is to incubate small acquisitions, invest in emerging lifestyle and wellness concepts, and engage the next generation of Indian consumers through agile. tech- enabled business models.

An investor may also note that promoters of GRM Overseas Ltd have been selling stakes in the company at a higher price in the market to purchase shares at a lower price in preferential warrants allotment.

Promoters sold a total of 1,625,000 shares (Atul Garg: 1,000,000 + Mamta Garg: 625,000) on Sept 5, 2025, at about ₹371.85 per share (closing price on BSE on Sept 25, 2025) for a total of ₹60.4 cr. (Source: BSE, BSE)

Promoters used a part of this money to subscribe and exercise 1,208,000 warrants (Hukam Chand Garg, Atul Garg and Mamta Garg) at a price of ₹150/- per warrant/share in Feb. 2026 for a total of about ₹12.08 cr. effectively making a profit of about 150% per share (Source: BSE)

Please note that these prices are pre-bonus issue of December 2025.

Moreover, in the AGM for 2025, GRM Overseas Ltd has approved transactions up to ₹750 cr with a promoter-group company, Eros Agro & Farms Private Limited, for the sale, purchase of goods and services, as well as transfer of resources (Source: AR2025, p.255; BSE).

Please note that such actions do not automatically imply adverse intent; however, they require closer scrutiny from minority shareholders, as these have the potential to shift economic benefits from minority shareholders to promoters if such sales and purchases are at prices different from market prices.

Investor takeaway:

The quality of a business ultimately depends not only on operations but also on how its management allocates capital. When companies raise funds from shareholders but deploy them into unrelated or experimental ventures, investors must evaluate whether the capital allocation discipline is working for long-term shareholder interests. Additionally, promoter actions involving preferential allotments, related-party transactions etc. require deeper analysis, as misalignment of incentives can gradually transfer economic value away from minority shareholders even when business performance appears stable.

Also read: How to do Management Analysis of Companies?

5) Forex Gains and the Illusion of Operational Improvement:

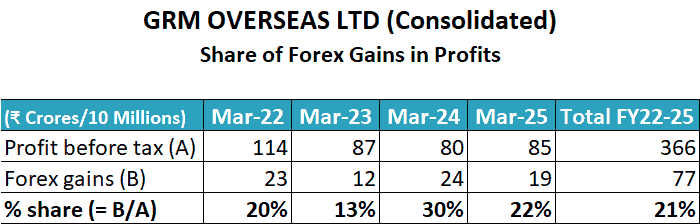

In recent years, a large portion of the company’s profits has been contributed by forex gains. From FY2022-FY2025, forex gains have contributed to about 21% of overall profits.

An investor should note that forex gains represent movement in currencies favourable to the company. It does not represent any operational excellence as currency movements are outside the control of the company.

Moreover, large forex gains may indicate significant unhedged forex positions by the company, which can hurt the company if, in the future, currencies move against the company (CR Acuite, January 2019).

Therefore, investors should analyse whether profit margins stay attractive even when forex gains are excluded from profits.

Investor takeaway:

Investors analysing export-oriented companies should distinguish between operational profitability and gains arising from favourable currency movements. Forex gains are largely external and cyclical in nature and may reverse when currency trends change. Mistaking such gains as business improvement can lead to overestimation of sustainable earnings power. Long-term investors should analyse core operating performance excluding forex effects to understand whether earnings are stable or not.

Conclusion: Learning for Long-Term Investors

Periods of industry upcycles often make investors focus on expansion opportunities while underestimating the risks in the business model of companies. The discussion on GRM Overseas Ltd highlights how industry economics, working capital requirements, cash flow realities, capital allocation decisions, and non-operational profit drivers can influence the long-term outcomes for shareholders.

Importantly, many of these aspects do not become visible on a broad analysis of revenue growth or reported profitability. Instead, an investor gets to know them only when she examines how a business converts profits into cash, how its growth is funded, and whether management incentives are aligned with minority shareholders over extended periods.

For long-term investors, the objective of such analysis is not to arrive at immediate buy or sell conclusions, but to refine the approach used while analysing any company. Over time, avoiding risky businesses helps as much in investment success as identifying future winners.

In my own investment process, analyses like this primarily serve as filtering tools. Only businesses that demonstrate durable cash generation, capital allocation, and an alignment of promoter incentives with shareholders are considered suitable for long-term portfolio inclusion.

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

I, Vijay Malik, am a SEBI-registered Research Analyst (Regn. No. INH100008364). This article is for educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.