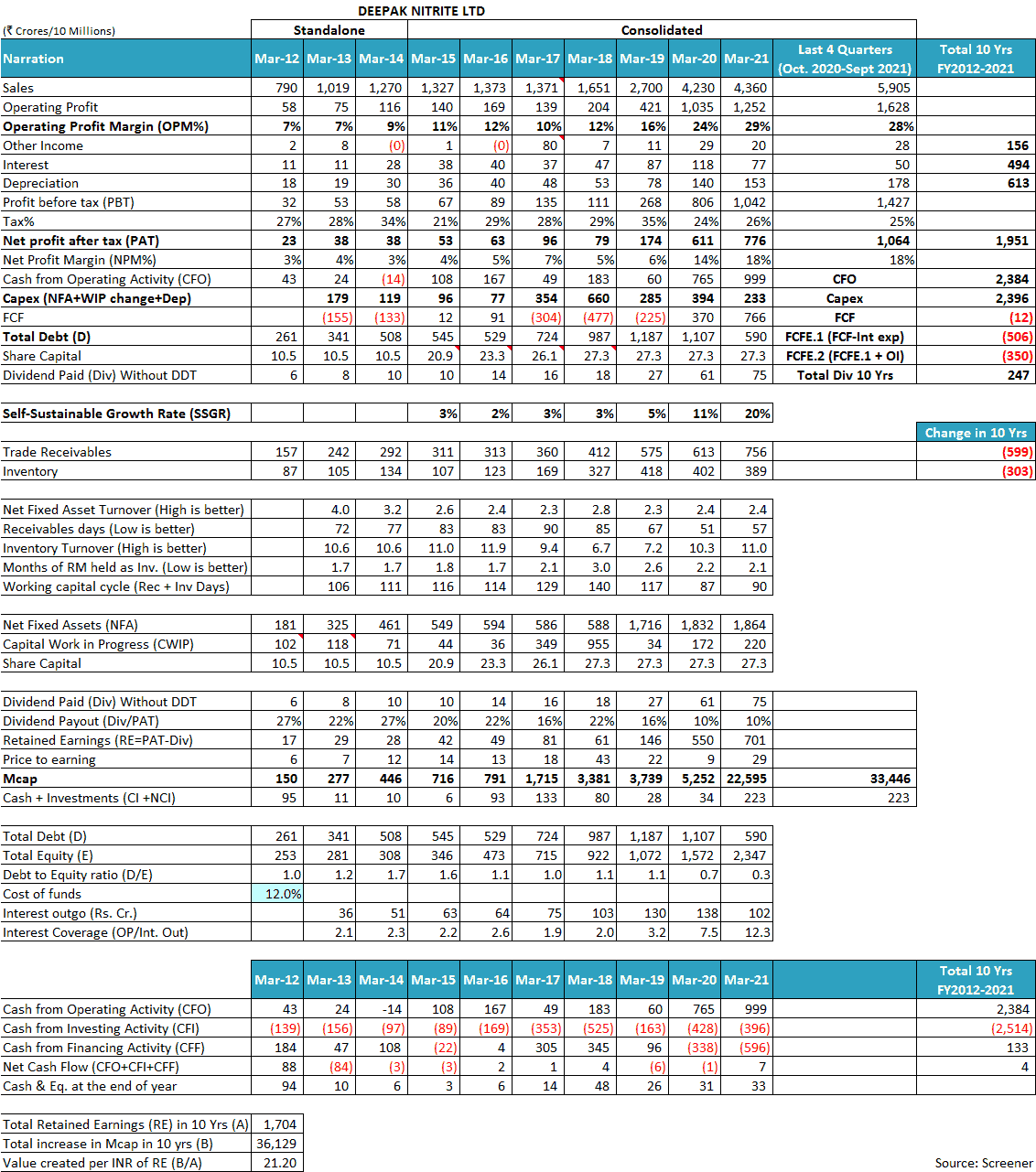

The current section of the “Analysis” series covers Deepak Nitrite Ltd, India’s leading manufacturer of Phenol, Acetone, optical brightening agents (OBA), fuel additives and other chemical intermediates like sodium nitrite/nitrates etc.

“Analysis” series is an attempt to share with all the readers, our inputs to the company analysis submitted by readers on the “Ask Your Queries” section of our website.

To benefit the maximum from this article, an investor should focus on the process of analysis instead of looking for good or bad aspects of the company. She should learn the interpretation of different types of data and transactions and pay attention to the parts of annual reports etc. used to get the information. This will help her in improving her stock analysis skills.

Deepak Nitrite Ltd Research Report by Reader

Hello sir,

Thanks a lot for sharing your articles and analysis with users like me, who are complete novices in the field of investigation. I have learnt a lot from your articles and tried my best in whatever way I can try in studying Deepak Nitrite Ltd.

Thanks for sparing some time to highlight what I can improve in my analysis.

Thanks and regards,

Sumit Malik

1) Financial Analysis:

- Sales growth for Deepak Nitrite Ltd is low at approx. below 5%.

- Net profit margin (NPM) is more than 15% in 2021 and profit margin seems to be improving

- The tax payout ratio is above 25%.

- The interest coverage ratio is more than 10.

- The debt to equity ratio is reducing, which is a good sign as it is decreasing since debt is decreasing.

- Cumulative PAT vs CFO: cCFO (10 Yrs.) is ₹2,331 cr. cPAT (10 Yrs.) ₹1,851 cr. There is a difference of approx. ₹480 cr while comparing cumulative CFO and cumulative PAT for 10 yrs.

- As per the self-sustainable growth rate (SSGR), the company is capable of growing at a 20% rate without taking debt from external sources.

- Peer comparison: Sales growth with respect to peers is outstanding. Earnings per share (EPS) at this price to earnings (PE) ratio is better than renowned companies e.g. Pidilite Industries Ltd.

2) Business & Industry Analysis

Deepak Nitrite Ltd is one of India’s leading and fastest-growing chemical intermediates manufacturing companies. It has a presence in basic chemicals, fine & speciality, performance products and phenolics (Phenol, Acetone & Iso-Propyl Alcohol). It is a leading producer of inorganic salts, xylidines, cumidines, toluidines, phenolics, IPA etc. It has six manufacturing facilities across Nandesari and Dahej in Gujarat, Roha and Taloja in Maharashtra and Hyderabad in Telangana. (Source: Annual report)

3) Management Analysis

- Deepak Chimanlal Mehta is the director of 21 companies as of today.

- Sailesh Chimanlal Mehta, son of Deepak Mehta, is director of 13 companies.

- Promoter shareholding is more than 45%.

- Foreign institutional investors (FII) holding is about ~10%.

A few important observations, which I want to highlight, are as follows:-

- Net profit margin (NPM) is improving over recent years, which is in the company’s favour.

- Interest expense is declining since 2018, which is also in favour.

- Tax payout is consistent and is close to 25%.

- Even though the receivable days have increased from last year, yet if we compare it in long term, it has significantly reduced.

Regards,

Sumit Malik

Dr Vijay Malik’s Response

Dear Sumit,

Thanks for sharing the analysis of Deepak Nitrite Ltd with us! We appreciate the time & effort put into the analysis.

While analysing the history of Deepak Nitrite Ltd for the last 10-years (FY2012-FY2021), an investor would notice that originally, the company did not have any subsidiary; therefore, it used to report only standalone financial data.

In FY2014, the company formed a wholly-owned subsidiary (WOS), Deepak Nitrite LLC in the USA. However, the company still reported standalone financials because; the subsidiary did not have any operations.

FY2014 annual report, page 94:

During the year, company has incorporated a subsidiary ‘Deepak Nitrite LLC’, a Limited Liability Company in the United States of America. The said Subsidiary has no transactions up to March 31, 2014. Therefore, consolidated financial results have not been prepared and published

In the next year, FY2015, Deepak Nitrite Ltd changed the name of its subsidiary in the USA to Deepak Nitrite Corporations Inc., took 49% shareholding in Deepak Gulf LLC in Oman and acquired 100% shareholding of Deepak Phenolics Ltd (earlier known as Deepak Clean Tech Ltd).

FY2015 annual report, page 33:

Last year, your Company also incorporated Deepak Nitrite Corporation, Inc. in North Carolina, USA to take care of marketing & operations part of customers in Northern and Southern American region. Your Company is also having an Associate Company Deepak Gulf LLC in Oman with 49% of holding in total Share Capital.

FY2015 annual report, page 44:

Acquiring the entire Share Capital of Deepak Phenolics Limited (earlier known as Deepak Clean Tech Limited) and then investing in the said wholly owned subsidiary company.

As in FY2015, the subsidiaries and associate companies of Deepak Nitrite Ltd had started to conduct financial transactions; therefore, the company started to report consolidated financial performance from FY2015 onwards.

We believe that while analysing any company, an investor should always look at the company as a whole and focus on financials, which represent the business picture of the entire company including its subsidiaries, joint ventures etc. Consolidated financials of a company present such a picture. Therefore, if a company reports both standalone as well as consolidated financials, then in such a case, it is advised that the investor should prefer the analysis of consolidated financials of the company, whenever they are present.

Further advised reading: Standalone vs Consolidated Financials: A Complete Guide

Therefore, in the case of Deepak Nitrite Ltd, we have analysed standalone financials until FY2014 and consolidated financials from FY2015 onwards.

With this background, let us analyse the financial performance of the company.

Financial and Business Analysis of Deepak Nitrite Ltd:

While analyzing the financials of Deepak Nitrite Ltd, an investor notices that the sales of the company have grown at a pace of 21% year on year from ₹790 cr in FY2012 to ₹4,360 cr in FY2021. Further, the sales of the company have increased to ₹5,905 cr in the 12-months ended September 30, 2021, i.e. during Oct. 2020-Sept. 2021.

While analysing the sales growth of the company over the last 10-years, an investor notices that the sales of the company increased every year except in FY2017 when the sales of Deepak Nitrite Ltd declined marginally from ₹1,373 cr in FY2016 to ₹1,371 in FY2017.

While analysing the profitability of Deepak Nitrite Ltd, an investor notices that the operating profit margin (OPM) of the company has also increased every year in the last 10-years (FY2012-FY2021) except FY2017 when the OPM of the company declined from 12% in FY2016 to 10% in FY2017.

To understand the reasons for the financial performance of Deepak Nitrite Ltd, an investor needs to read the publicly available documents of the company like annual reports, conference calls, credit rating reports, fund-raising prospectuses as well as its corporate announcements. Then she would understand the factors leading to the increase in its revenue and profit margins as well as the reasons for the decline in performance in certain periods.

After going through the above-mentioned documents, an investor notices the following key factors, which influence the business of Deepak Nitrite Ltd. An investor needs to keep these factors in her mind while she makes any predictions about the performance of the company.

1) Dependence of raw material of Deepak Nitrite Ltd on crude oil prices:

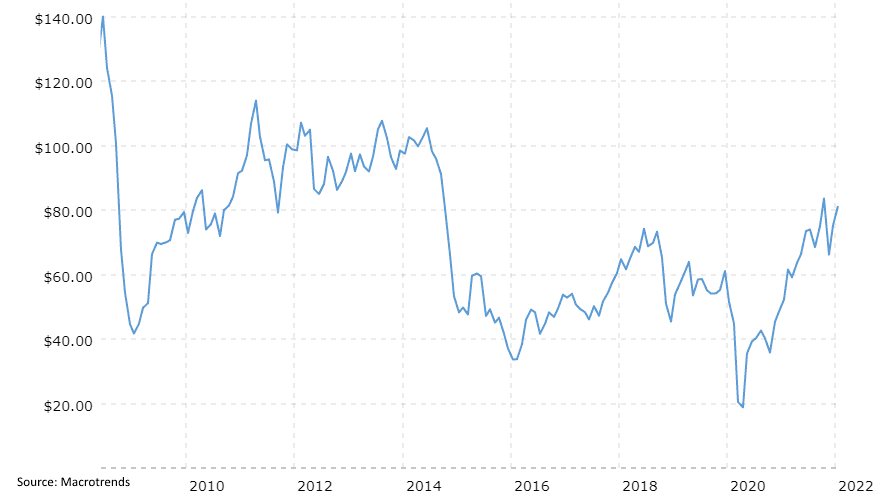

One of the key features that an investor learns while analysing Deepak Nitrite Ltd is that its business has significant linkages to crude oil prices. This is because; most of the raw materials used by Deepak Nitrite Ltd are derived from crude oil.

The largest contribution to the revenues of Deepak Nitrite Ltd (about 58% in FY2021) is from the phenolic business (phenol, acetone and isopropyl alcohol). In the case of phenolic business, the key raw materials are benzene and propylene, which are derived from crude oil. As a result, their prices are strongly linked to crude oil prices.

Conference call, February 2021, page 11:

Somsekhar Nanda: The top line in Deepak Phenolics depends on the crude price and hence the prices of propylene, benzene and hence phenol and acetone.

An investor would appreciate that the phenolic business, which is currently, the largest contributor to Deepak Nitrite Ltd.’s business was started in FY2019. However, in the case of other products as well, the raw material prices are strongly linked to crude oil prices.

FY2016 annual report, page 37:

crude oil and related petrochemical intermediates, which form an important source of raw materials for your Company

Even for the products, which the company is producing for more than a decade, the prices of the raw materials are linked to crude oil prices.

FY2010 annual report, page 23:

An ongoing threat to your Company’s business is crude oil prices. An increase in price could significantly increase raw material prices.

Conference call, May 2011, page 2:

there has been a fair amount of volatility in price of crude and resulting volatility in our key raw material

Therefore, an investor would appreciate that the prices for the raw material of almost all the products manufactured by Deepak Nitrite Ltd are dependent on crude oil prices.

Moreover, an investor would appreciate that crude oil is one of the most volatile commodities in the world. In the past, the prices of crude oil have witnessed very sharp fluctuations. The following chart from Macrotrends, showing historical prices of crude oil indicates that from 2008 until now, crude oil prices have witnessed levels from $20 to $140 per barrel.

An investor would notice that crude oil prices touched a high of about $140 per barrel in 2008 and then declined to about $40 in 2009. Then, the prices recovered to about $115 in 2011 only to decline sharply over 2014-2016 to about $30 in 2016. Thereafter, the crude oil prices increased again to about $70 per barrel in 2018 and then declined to about $20 in 2020. Currently, the prices have increased to about $80 in 2022.

Therefore, an investor would appreciate that the crude oil prices have been very volatile over the last decade and have moved up and down in a cyclical manner. As a result, the raw material prices for Deepak Nitrite Ltd would also be highly volatile during this period.

The investor would also acknowledge that when any company faces such significant volatility in its raw material prices, then it becomes a challenge for it to maintain stability in its business on the parameters like profitability.

Moreover, it is not only the raw material prices of Deepak Nitrite Ltd that depend on crude oil prices; for many products, the demand from the customers is also dependent on crude oil prices. This is because; many customers reduce the purchase of products from Deepak Nitrite Ltd when crude oil prices are in the declining phase. After all, they attempt to minimize inventory losses.

In the FY2015 annual report, Deepak Nitrite Ltd highlighted to its investors that some of the customers reduced their purchases during the year when crude oil prices were declining.

FY2015 annual report, page 32:

Towards the beginning of the second half of FY 2014-15, due to the sharp decline in international crude oil prices, there was disruption in volume off-take from some of your Company’s customers who decided to minimize inventory to insulate them from heightened volatility. As a result of this, some products witnessed temporary decline in demand.

Let us see how Deepak Nitrite Ltd has managed such challenges when its business model is significantly dependent on volatile crude oil prices.

2) Formula based pricing of end products as well as the raw material of Deepak Nitrite Ltd:

While analysing the business of Deepak Nitrite Ltd, an investor comes across multiple instances where the company intimated to its shareholders that its pricing arrangements with both, its customers as well as its suppliers are formula-based, which allow regular revision of prices.

The company has been following the formula-based pricing for both its customers as well as its suppliers for a very long time. During its conference call with investors in February 2011, Deepak Nitrite Ltd highlighted the formula based selling prices to the customers as well as formula based purchase prices from its suppliers, which are linked to crude oil prices.

Conference call, February 2011, page 5:

Sanjay Upadhyay: Yes Abhijeet, just to add on this, where we feel that prices are fluctuating violently we go by formula base pricing where customer also understands the price mechanism, so that is how we try to manage those things, where it is a long-term contract there we try to see that it is a formula based pricing linked to the major raw material which are crude based.

Umesh Asaikar: Similarly we try to enter with some of our suppliers on formula base. It will be fair to everybody, and then one lands up with proper, fair and reasonable manufacturing margins, and one is not exposed to violent trends and volatility in material prices.

Even after the passage of more than 10-years, in October 2021, Deepak Nitrite Ltd again emphasized to the investors that formula-based pricing is the best proposition in its business.

Conference call, October 2021, page 3:

Maulik Mehta: As mentioned earlier, our approach instead of timing the market both from RM and FG side, was focused on back-to-back formula-based arrangements with suppliers and customers both where the contracts are signed with a predetermined benchmark index on an annualized basis, which allows us to procure at the best rate possible. Parallelly, with our customers also, in many cases we have formula-based pricing, whereby we are able to pass on raw material price increases after a period of time. We believe under the current situation of high volatility; this is the most optimal approach one can have.

Therefore, an investor would appreciate that Deepak Nitrite Ltd has built a business model where most of its business is via products where the sale prices is calculated by using a formula based on an index (linked to crude oil price). The company follows the same formula based pricing with its suppliers as well.

As a result, when the crude oil prices increase, then the cost of raw materials for Deepak Nitrite Ltd increases. Similarly, as the cost of raw material for Deepak Nitrite Ltd increases, it is able to increase the selling price of its products to its customers and therefore, it is able to protect is profit margins.

In the conference call done by the company with investors in May 2011, it highlighted that it has been able to maintain its margins because it could pass on the increase in its costs to its customers.

Conference call, May 2011, page 2:

Umesh Asaikar: …we are in a position to pass on the increase in price line and thus we were able to maintain the margins.

In the above chart showing crude oil prices, an investor would note that in 2020-2021, crude oil prices increased sharply from about $20 per barrel to about $80 per barrel. As a result, the raw materials of Deepak Nitrite Ltd increased significantly. However, despite such an increase, the company reported its highest-ever operating profit margin because it could pass on the increase in the cost of its raw material to its customers.

Conference call, May 2021, page 4:

Maulik Mehta: …This was achieved despite a significant increase in raw materials almost across the board as the company was able to pass on a lot of the cost.

From the above discussion, an investor would notice some important observations. She would note that the key raw material used by Deepak Nitrite Ltd are derivatives of crude oil. Therefore, its raw material prices are very volatile. However, the company is able to pass on the increase in its costs to its customers by way of formula-based pricing.

An investor would note that due to formula-based pricing linked to crude oil prices, the sales prices of Deepak Nitrite Ltd are highly volatile. As a result, many times, during the periods when crude oil prices decline, then the company is not able to increase its sales despite a significant increase in the volumes.

For example, in FY2010, the sales of the company declined in value by 7% from ₹572 cr in FY2009 to ₹532 cr in FY2010; despite an increase in the volume of sales by more than 20%.

FY2010 annual report, page 27:

Financial Year 2009-10 has been an eventful year for your Company. The turnover for the year was Rs. 532 crores compared to Rs. 572 crores in the previous year…Your Company has been able to increase the quantitative volumes by more than 20% compared to the previous year.

Again, in FY2016, when the crude oil prices declined sharply from about $130 per barrel in 2014 to about $30 per barrel in 2016, its raw material prices declined and in turn, the company had to reduce its sales price, which affected its revenue.

FY2016 annual report, page 37:

The prices of crude oil and related petrochemical intermediates, which form an important source of raw materials for your Company declined significantly over the past one year thereby impacting top-line growth.

Nevertheless, due to formula-based pricing, the company is able to avoid any hit on its profit margins. Therefore, an investor would appreciate that over the last 10-years, the company has been able to report continuously improving operating profit margin.

However, after making a detailed reading of the public documents, an investor notices that the pass-through of increased costs is not a simple and straight event. Deepak Nitrite Ltd faces multiple challenges before it can get a higher price from its customers.

Further advised reading: How to do Business Analysis of a Company

3) Challenges in increasing prices to customers despite formula-linked arrangements:

In the prospectus for its qualified institutional placement (QIP) in January 2018 (source: BSE), Deepak Nitrite Ltd acknowledged that there have been occasions when it could not pass on the increase in its costs to its customers.

QIP prospectus, January 2018, page 38:

there have also been occasions when we have been unable to pass on increases in raw materials prices to our customers.

At times, Deepak Nitrite Ltd could not pass on the increase in the raw material prices to its customers because of the fear of losing market share.

In October 2021, in the press release declaring the Q2-FY2022 result, Deepak Nitrite Ltd intimated to its shareholders that it did not increase the prices of its leading products to maintain market share. Under this dynamic strategy, the company increased the prices of products other than its leadership products.

Q2-FY2022 press release, October 2021, page 2:

Assessing the market situation, the Company deployed a dynamic strategy this quarter, which involved focusing on preserving market share for leadership products while driving pricing for some other products.

Moreover, an investor notices that the contracts entered by Deepak Nitrite Ltd with its customers allow for revision in the prices only at fixed intervals like every quarter. Therefore, it can increase prices only after a gap of 3-months from the previous price change.

However, an investor would notice that the crude oil prices and hence its raw material prices are very volatile and can fluctuate a lot during the period of a quarter (3-months). Therefore, at times, Deepak Nitrite Ltd was stuck in situations where after a recent price revision, the raw material prices increased significantly. However, it could not increase its prices and had to take a hit on its margins during the period until the subsequent price revision.

For example, in May 2021 conference call, Deepak Nitrite Ltd highlighted to its investors that it could not increase the prices to some of its customers where the review of pricing is after each quarter. In such a case, Deepak Nitrite Ltd had to absorb the increase in its costs.

Conference call, May 2021, page 4:

Maulik Mehta: …In some products where there is more of a long-term relationship where the contractual clause is to look at price reviews every quarter. We had to absorb the cost increase within the quarter and look at how best we can ensure that we are able to pass it on the next opportunity that we have to review.

On many previous occasions, Deepak Nitrite Ltd had highlighted this challenge of absorbing an increase in raw material costs during the period between the dates of the pricing review. For example, in the FY2015 annual report, the company highlighted this as a major weakness of its business model, to its investors.

FY2015 annual report, page 34:

WEAKNESSES: One of the major hurdles for the chemical industry is its susceptibility to volatile raw material costs particularly BCC. Absorbing cost of this volatile market becomes challenging, as there are time lags before any costs benefit or price hike can be passed on to customers.

In FY2012, the company suffered a hit on its profitability when it could not pass on the increase in raw material prices to its customers.

Conference call, May 2012, page 3:

Sanjay Upadhyay: PAT was impacted by lag in passing the high increase in the price of key raw material.

Therefore, an investor would appreciate that when the raw material of any company are highly volatile (linked to crude oil prices), then having a formula-based product pricing may also not be sufficient. This is because; such arrangements allow for revision in the prices after a fixed interval like a quarter. However, the crude oil prices and hence, the raw material costs can change significantly during this period.

In addition, at times, companies like Deepak Nitrite Ltd are not able to increase prices because they face intense competition from global chemical manufacturers. The company had intimated to its shareholders that it faces strong price-based competition from foreign companies.

QIP prospectus, January 2018, page 44:

We face price pressures from foreign companies that are able to produce chemicals at competitive costs and consequently, supply their products at cheaper prices.

Deepak Nitrite Ltd had highlighted to its investors that the products made and the processes followed by it are the same, which are followed by other global manufacturers e.g. in China. Therefore, it faces strong competition from China.

Conference call, February 2021, page 19:

Maulik Mehta: Of course, we face significant competition from China, of course, our processes that we employ across multiple products, in many of these cases, Chinese companies also do the same. This has always been a feature for the chemical intermediate segment, and is not expected to change.

Therefore, despite formula-based pricing arrangements, before increasing prices to its customers Deepak Nitrite Ltd has to continuously think of the threat of foreign competitors taking away its market share.

An investor would notice that in the recent period, there have been significant challenges in sea trade due to shortage of containers as well as unavailability of ships for sending cargo via sea.

Conference call, February 2021, page 3:

…challenges on international shipping, due to container and ship unavailability.

Conference call, August 2021, page 9:

Maulik Mehta: And there were a lot of export disruptions where ship berthing was not available, where you had the Suez Canal issue…

Conference call, October 2021, page 6:

There were supply restriction bottlenecks due to container shortage…

An investor would appreciate that due to challenges in trade-by-sea, the freight costs would increase and it becomes difficult to import goods at a cheap price. Deepak Nitrite Ltd also highlighted to its investors in May 2015 conference call that due to the above-mentioned challenges, sea freight has gone up and now, it is difficult for people to import and sell in India.

Conference call, May 2021, page 10:

Sanjay Upadhyay: …sea freight are also going up. It is extremely difficult for people to import and sell in India.

Therefore, an investor would notice that during FY2021 and later, Deepak Nitrite Ltd has taken significant advantage of the difficulties faced by the importers in procuring goods from abroad. Because of the high demand due to lower imports, the company is able to run its factories at very high utilization levels. For example, in FY2021, the company was running its phenol plant at a capacity utilization level of 130%.

Conference call, May 2021, page 13:

Sanjay Upadhyay: In fact, today we are running at 130% capacity utilization

An investor would appreciate that such high capacity utilization levels lead to a lot of operating leverage benefits i.e. lower per-unit cost of products. In addition, lack of competition from cheaper imports has Deepak Nitrite Ltd to charge a high price of its goods to its customers.

As a result, it does not come as a surprise to the investor when she notices that during FY2021, Deepak Nitrite Ltd has reported its highest-ever operating profit margin (OPM) of 29% and an OPM of 28% in the 12-months ended September 30, 2021, i.e. during Oct. 2020-Sept. 2021.

Further advised reading: How to do Business Analysis of a Company

4) Lack of long-term contracts with customers and suppliers:

While analysing the business history of Deepak Nitrite Ltd an investor notices that in the past, the company did not have any long-term supply arrangements with either its customers or its suppliers. The company highlighted this as a risk in the prospectus before the QIP in January 2018.

QIP, January 2018, page 39:

We do not have long term agreements with majority of our suppliers. We do not have long term agreements with any of our customers.

An investor would note that if a company does not have long-term supply arrangements/contracts with its customers, then it continuously faces the risk of customers shifting to the competitors without much difficulty. This is because; in the absence of long-term contracts, the barriers to entry to the competitors go down.

QIP, January 2018, page 39:

Absence of such long term agreements exposes us to the risk that our customers may cease to source products from us.

Similarly, an absence of long-term supply arrangements with the suppliers puts Deepak Nitrite Ltd at the risk of failure to get raw material when it requires it urgently.

QIP, January 2018, page 39:

Short term supplier contracts subject us to risks such as price volatility, unavailability of certain raw materials in the short term and failure to source critical raw materials in time, which would result in a delay in manufacturing of the final product.

An investor would notice that the lack of long-term supply agreements with customers and suppliers exposes Deepak Nitrite Ltd to many risks. Then, she wonders, why the company is not going for long-term contracts.

Upon reading the past annual reports, an investor comes across the fact that it has not been the case always. Previously, the company used to enter into long-term contracts and used to highlight it to the investors as one of the major achievements.

For example, in the FY2010 annual report, Deepak Nitrite Ltd pointed out to the investors that it has entered into long-term contracts with customers and suppliers, which has increased the durability of its business model.

FY2010 annual report, page 4:

…has been able to enter into long-term contracts with both suppliers and customers, thereby enhancing the durability of its business model.

Therefore, it looks like originally, the company preferred to have long-term contracts with its suppliers and customers. However, subsequently, Deepak Nitrite Ltd had to pay a penalty to one of its key suppliers for natural gas, GAIL (India) Ltd, when it could not use its contracted quantity of natural gas.

As per the FY2016 annual report, when Deepak Nitrite Ltd did not use the committed amount of natural gas, then GAIL (India) Ltd asked it to pay a penalty of ₹7.18 cr. After arbitration, it seems that the penalty amount was reduced to ₹1.41 cr.

FY2016 annual report, page 171:

The Company has entered into a long term contractual arrangement with GAIL India Limited (“GAIL”) for supply of Gas with a Take or Pay obligations. A communication was received from GAIL regarding non-consumption of committed quantity for the year 2014. Accordingly, the Company is required to deposit a sum of ₹ 718.00 Lacs which may subsequently be adjusted in future against the consumption of Gas. The matter has been referred to an arbitrator for settlement, which is pending. However, GAIL has offered the Company to settle the matter amicably by paying one-time charges of ₹ 141.00 Lacs. Based on the above understanding, the Company has prudently provided for the said charges during the year.

Advised Reading: How to study the Annual Report of a Company

It seems that due to such experience, the company avoided long-term contracts and by January 2018 (date of QIP prospectus); Deepak Nitrite Ltd started preferring short-term contracts with its suppliers as well as customers.

However, in the absence of long-term contracts, the risks of short-term contracts highlighted by Deepak Nitrite Ltd in its QIP prospectus came true and the company realized the benefits of entering into long-term contracts.

Therefore, in the current year (FY2022), Deepak Nitrite Ltd has again started stressing about entering into long-term contracts with its customers. The company acknowledged that in the past, it did not prioritize long-term contracts with customers because they were already giving it a business for the last 10-15 years. Therefore, the company thought that why ‘bother’ about getting into long-term contracts.

However, it seems that now, the company has realized that long-term contracts make a strong relationship between the customer and supplier. Therefore, now, Deepak Nitrite Ltd has again started focusing on long-term contracts with customers.

Conference call, October 2021, pages 11-12:

Abhijit Akella: …the investor communication also talks about various long-term formula linked arrangement that you are kind of working on, so could you share some more insights…

Maulik Mehta: …Earlier, Deepak itself stayed away from this because we said look we have 10 years, 15 years relationship with these customers, they have been depending on us, they have been giving us a lion’s share of their requirements, why bother to get into that, but as we have gone ahead in the last couple of years, we have realized that their focus then can shift towards business development, market development rather than worrying about annual discussions with Deepak and that has successfully transpired itself into a more solidified relationship…

Therefore, an investor would notice that over FY2010-FY2022, Deepak Nitrite Ltd has seen its focus shift from long-term contracts in FY2010 to preferring short-term contracts by FY2018. It seems that the penalty imposed by GAIL (India) Ltd for the non-usage of a committed amount of natural gas may have played a role in this transition. However, now, Deepak Nitrite Ltd has once again realized that having long-term contracts is good for a strong relationship between the suppliers and customers. Therefore, in FY2022, the company is again showing a preference for long-term contracts.

Going ahead, an investor should closely monitor whether the company continues to stick to long-term arrangements with its customers and suppliers or it switches back to short-term contracts.

5) Focus on high-value products and energy efficiency by Deepak Nitrite Ltd:

While reading about the business of Deepak Nitrite Ltd over the years, an investor notices that from FY2012 to FY2021, the company increased its operating profit margin (OPM) from 7% to 29%. This improvement of about 22% in the OPM is significant. As a result, an investor needs to analyse the reasons for the same.

When an investor observes the different expenses incurred by Deepak Nitrite Ltd and compares them year on year by benchmarking them as a percentage of sales, then she notices that two parameters, raw material costs and power & fuel have shown the most remarkable improvement over the last 10-years (FY2012-FY2021).

The below table compares different expenses as a percentage of sales for Deepak Nitrite Ltd in FY2012 and FY2021.

An investor would notice that from FY2012 to FY2021, Deepak Nitrite Ltd could reduce its raw material costs as a percentage of sales from 67% in FY2012 to 51% in FY2021; thereby, adding 16% (= 67 – 51) to its operating profit margin (OPM).

A reduction in the raw material cost as a percentage of sales indicates that Deepak Nitrite Ltd has focused on high margin products over the years, which has resulted in an improvement in profitability.

While analysing the annual reports of Deepak Nitrite Ltd over the years, an investor comes across multiple instances where the company highlighted an improvement in the product mix i.e. selling more high-margin products, as a reason for the improvement in its profit margins.

In the FY2016 annual report, Deepak Nitrite Ltd highlighted that an improvement in the product mix resulted in higher profitability.

FY2016 annual report, page 37:

A combination of factors including favourable product mix, efficiency gains and better realisations across key products also contributed to better EBITDA performance.

In FY2018 also, the company mentioned improvement in the product mix (selling more high margin products) as the reason for increasing profits.

FY2018 annual report, page 50:

Full resumption of normal operations and favourable shift in product mix led to better PAT performance

The company continued to improve its product mix in the subsequent years i.e. FY2019, FY2020 and FY2021 as well.

FY2019 annual report, page 66:

Margin expansion was a result of product-mix adjustments, better realisation, and cost leadership initiatives

FY2020 annual report, page 55:

The expansion of margins was an outcome of enhancements in the product mix, improved realizations and cost reduction efforts undertaken at Company level.

FY2021 annual report, page 71:

The Company undertook several enhancements in the product mix, improved realisations and cost-reduction efforts that helped deliver better margins.

Looking at the above disclosures, an investor would appreciate that changing the product mix of the company over the years, has contributed significantly to the improvements in the profit margins of the company. From the changing product mix, an investor would note that Deepak Nitrite Ltd is able to manufacture different products in its plants as per the changing market scenario i.e. its plants are multipurpose.

In a multipurpose plant, Deepak Nitrite Ltd can easily switch production from one product to another whenever it realises that any particular product is commanding a higher profit margin in the market.

In multiple instances in the past, Deepak Nitrite Ltd has highlighted that its plants are multipurpose and provide it with the flexibility to change the products that are manufactured at a short notice.

Conference call, May 2010, page 7:

Deepak Mehta: Right…the benefit is these multipurpose plants help us to see that if there are any spurt in demands for any other segments we can quickly switch over and make those intermediate.

In the FY2017 annual report, the company explained to its investors that it could report a higher margin in its basic chemicals segment when it shifted production away from fuel additives to other intermediates. The company decided to produce other intermediates because the demand for fuel additives was low and the multipurpose plants allowed it to produce other products.

FY2017 annual report, page 31:

Basic Chemicals: While business of Fuel Additives was subdued during the year, the same production lines could have been utilised for producing other contributory products during the year, which gave boost to the margin in this business segment.

The credit rating agency, ICRA, highlighted in its report for the company in January 2018 that multipurpose plants allowed Deepak Nitrite Ltd to use the production lines of fuel additives to produce Sodium Nitrite and Sodium Nitrate.

Credit rating report, ICRA, January 2018, page 2:

…the facilities are designed to provide flexibility to change the product mix to cater to market requirements. For instance, the company used a few of its production lines, originally meant for fuel additives, to manufacture sodium nitrite/ sodium nitrate given the decline in demand for fuel additives.

Advised Reading: Credit Rating Reports: A Complete Guide for Stock Investors

In the conference call in August 2021, the company highlighted to the investors that it focuses on chemical processes instead of specific chemical products while designing its manufacturing plants. The company mentioned that in the past when it focused on making plants for a specific product, then it had to suffer. Therefore, it changed its strategy to focus on multipurpose plants.

Conference call, August 2021, page 19:

Maulik Mehta: So, it is not like the Deepak Nitrite of old where one plant only focused on making one product, we have learnt at a very high cost the need to be fungible and have the flexibility of product.

As per the company, it focuses on developing integrated product chains where many products can be produced instead of focusing on specific products.

Conference call, October 2021, page 3:

Maulik Mehta: The Company’s business strategy is to prioritize the development of integrated product chains over standalone products…

Therefore, an investor would appreciate that Deepak Nitrite Ltd has preferred to create multipurpose manufacturing plants where it can switch production from one chemical to another as per changing market scenario. Due to this flexibility, the company has been able to improve its product mix over the years to focus more on high-margin products. This is one of the most important factors leading to a significant improvement in the profit margins of the company.

From the above table on the analysis of operating expenses of Deepak Nitrite Ltd as a percentage of its sales, an investor would remember that the other parameter leading to significant savings for the company was power & fuel costs. Over FY2012-FY2021, Deepak Nitrite Ltd decreased its power & fuel costs from about 10% of sales in FY2012 to about 6% of sales in FY2021, which contributed an improvement of about 4% in the operating profit margin (OPM) of the company.

While reading the annual reports of Deepak Nitrite Ltd, an investor notices that the company has continuously focused on improving its energy efficiency and has taken multiple steps about the same over the years.

In FY2010, the company highlighted that it is shifting away from the usage of furnace oil to using natural gas and coal in its manufacturing plants.

Conference call, May 2020, page 7:

Deepak Mehta: I would say some significant portion is also going for bringing in more energy efficiency in all these four sites, wherever possible we have been moving into investments in using gas which is now more readily available, thanks to Reliance, wherever possible we are now moving from furnace oil based boilers to coal based boilers…

In addition, to reduce the power costs, Deepak Nitrite Ltd is constructing a captive power plant in Dahej, which as per the company, is about to get completed soon.

FY2021 annual report, page 25:

Expand Capabilities: Completion of captive power plant is nearing

Conference call, October 2021, page 5:

Maulik Mehta: …we are expecting to commission IPA to manufacture 30,000 tonnes of additional capacity and 29-megawatt cogent plant during this current quarter.

The new captive power plant would be in addition to another captive power plant that it has in Nandesari, near Vadodara, which it commissioned in 2004 (as per FY2011 annual report, page 17).

Therefore, an investor would note that Deepak Nitrite Ltd has taken steps to improve its cost efficiencies, which has contributed to an increase in its profit margins.

The credit rating agency, CRISIL, highlighted the role of cost efficiencies in the improvement of its profit margins in its report for Deepak Nitrite Ltd in August 2020.

The group’s operating profitability improved to 25.1% in fiscal 2020 from 16.1% in fiscal 2019 supported by extraordinary performance of PP segment as well as increase in the margins for the BC segment owing to cost efficiency measures…

Going ahead, an investor should keep a close watch on the raw material costs as well as other cost efficiency measures of Deepak Nitrite Ltd. This is because; a tight control on the same is needed to keep its operating profit margins at current improved levels.

An investor would also remember that in the recent period, due to difficulties in the sea trade i.e. ship shortage, container shortage etc., the importers are not able to source cheap goods from overseas manufacturers. As a result, Deepak Nitrite Ltd is able to charge a high price to its customers and run its plants at very high utilization levels exceeding 100%. This has resulted in the best ever profit margins for the company.

Further advised reading: How to do Business Analysis of Chemical Companies

Going ahead, an investor should keep a close watch on the profit margins because; the supply chain bottlenecks like challenges of sea trade would not continue forever. Once the supply chain problems are resolved, then the competition from foreign manufacturers would increase, which may bring down the profit margins.

The company itself realizes this; as a result, it has acknowledged that the current profit margins on some of its products like Phenol are not sustainable.

Conference call, August 2021, page 18:

Sanjay Upadhyay: …Phenol, of course, you can’t expect this kind of EBITDA margins every quarter, so I cannot commit on that.

Therefore, an investor should be cautious while projecting the currently improved profit margins in her future projections.

While analysing the tax payout ratio of Deepak Nitrite Ltd., an investor notices that for most of the years, the tax payout ratio of the company has been in line with the standard corporate tax rate prevalent in India. It was only in FY2015 when the company reported a tax payout ratio of 21%. The primary reason for the lower tax payout ratio in FY2015 was an adjustment of minimum alternate tax (MAT) credits of about ₹11 cr.

In recent years, the tax payout ratio has declined to 25% from the previous years’ level of about 30%, which seems to be in line with the recent changes in the corporate tax rates implemented by India.

Further advised reading: How to do Financial Analysis of a Company

Operating Efficiency Analysis of Deepak Nitrite Ltd:

a) Net fixed asset turnover (NFAT) of Deepak Nitrite Ltd:

When an investor analyses the net fixed asset turnover (NFAT) of Deepak Nitrite Ltd in the past years (FY2013-21), then she notices that the NFAT of the company has declined from 4.0 in FY2013 to 2.4 in FY2021.

While analysing the business decisions taken by Deepak Nitrite Ltd during the last 10-years (FY2012-FY2021), an investor notices that the company has consistently invested money in creating additional manufacturing capacity during this period.

Some of the major capital expenditure projects undertaken by Deepak Nitrite Ltd during the last 10-years are:

- FY2011-FY2013: Optical brightening agent (OBA) project in Dahej, Gujarat: Phase 1 was completed in March 2013 (FY2014 annual report, page 45) and the remaining project was completed in FY2015 (FY2015 annual report, page 7).

- FY2011-FY2014: Brownfield expansion of salt section in Nandesari, Vadodara: commissioned in June 2013 (FY2014 annual report, page 45).

- FY2017-FY2019: A very large greenfield project in Dahej for Phenol and Acetone was commissioned in November 2018 (FY2019 annual report, page 18).

- FY2020-FY2021: Isopropyl Alcohol (IPA) plant, 30,000 MTPA in Dahej (FY2020 annual report, page 37).

- FY2021-FY2022: Doubling of the capacity of IPA plant from 30,000 MTPA to 60,000 MTPA and a captive power plant of 29 MW (Conference call, October 2021, page 4).

While analysing the various investor communications done by Deepak Nitrite Ltd, an investor gets to know that the asset turnover of the investments done by the company in the last 10-years, is in the range of 1.50 to 2.25 times.

In May 2010, the company intimated to its shareholders that the asset turnover for the investments planned for OBA and salts segments was expected to be 1.50-1.75 times.

Conference call, May 2010, page 9:

Paurav Lakhani: So roughly the additional sales from this Dahej plant would be in the region of what…?

Deepak Mehta: Again this depends upon the product mix, but I can say that our turnover to investment has been in the ratio of about 1.5 to 1.75 to 1.

While planning the large Phenol project in May 2016, the company intimated to its shareholders that it is expecting a turnover ratio of about 2.25 times on its investment in the project.

Conference call, May 2016, page 6:

Arun Malhotra: The same asset turnover, means on Rs. 1200 crore of CAPEX…?

Somsekhar Nanda: The asset turn ratio on a normal crude price, crude price is subdued now, on a normal situation it will be about 2.25x:1.

Further, in May 2021, while elaborating the strategy for upcoming capacity expansion projects, the company intimated to its shareholders that it expects an asset turnover ratio of about 1.75 to 2.00 times on its investments.

Conference call, May 2021, page 16:

Onkar Ghugardare: I was looking into what can be the asset turnover.

Sanjay Upadhyay: Normally we look at 1.75 to 2x

Therefore, an investor would appreciate that almost all the projects undertaken by the company during the last 10-years have an asset turnover ranging from 1.50 – 2.00 times.

The largest project undertaken by Deepak Nitrite Ltd, the Phenol project, commissioned for a cost of ₹1,400 cr reported a turnover of about ₹2,561 cr in FY2021 (FY2021 annual report, page 271) while running at a capacity utilization of 115% (FY2021 annual report, page 14). It amounts to an asset turnover of about 1.83 (=2,561 / 1,400).

As the new investments done by Deepak Nitrite Ltd in the last 10-years are producing a lower fixed asset turnover than the historical fixed assets (in FY2013, the NFAT was 4.0), therefore, the NFAT of the company has come down over the last 10-years to 2.4 in FY2021.

Going ahead, an investor should keep a close watch on the progress of the newly announced project and the capacity utilization levels of Deepak Nitrite Ltd so that she can assess whether the company is utilizing its assets efficiently or not.

Further advised reading: Asset Turnover Ratio: A Complete Guide for Investors

b) Inventory turnover ratio of Deepak Nitrite Ltd:

While analysing the efficiency of inventory utilization by Deepak Nitrite Ltd, an investor notices that over the last 10 years (FY2013-FY2021), the inventory turnover ratio (ITR) of the company has remained constant at the levels of about 10.5-11.0. The ITR was 10.6 in FY2013 and 11.0 in FY2021.

However, during these years, the ITR has witnessed significant fluctuation when it declined to its lowest to 6.7 in FY2018. Thereafter, the ITR started increasing and it improved significantly to 11.0 in FY2021.

Therefore, when an investor analyses the efficiency of inventory management of Deepak Nitrite Ltd, then she may see it in terms of two different periods; first, until FY2018 and then the second period from FY2019 until date.

An investor would recollect from the above discussion on net fixed asset turnover that during the first phase, FY2013-FY2018, Deepak Nitrite Ltd had done a major capital expenditure in Dahej, Gujarat, where it created a plant to manufacture optical brightening agents (OBA), which is a part of the colours segment.

OBA was a forward integration step for Deepak Nitrite Ltd because it was already making the raw material for OBA, which is Diamino stilbene disulfonic acid (DASDA) and Para Nitro Toluene (PNT), which is used to make DASDA.

FY2012 annual report, page 8:

Our greenfield expansion in Dahej is a forward integration to manufacture OBA. With the completion of this greenfield project at Dahej, we will complete the vertical integration from Toluene to Optical Brightening Agent – OBA (Toluene ->PNT -> DASDA -> OBA). This feat places us amongst the very few fully integrated player in the world with such a capability.

The company highlighted that it is one of the very few fully integrated manufacturers of OBA. Deepak Nitrite Ltd had created a large capacity of OBA because; soon it captured 75% of the domestic market for OBA.

FY2018 annual report, page 45:

Your Company is the only fully integrated manufacturer of Optical Brighteners (OBAs) which is backward integrated up to the feedstock of toluene. In this segment, your Company caters to 75% of the domestic requirement of brighteners

To analyse the business dynamics of OBA production, when an investor analyses the locations where Deepak Nitrite Ltd manufactures each of these products in the OBA chain, then she gets to know that:

- Toluene is converted into PNT (Para Nitro Toluene) in the Nandesari plant near Vadodara, Gujarat

- PNT is converted into DASDA in its Hyderabad plant in Telangana

- Thereafter, DASDA is converted into OBA in its newly created plant in Dahej, Gujarat.

An investor would appreciate that to make OBA; first, the company has to buy Toluene in Gujarat and process it into PNT in Nandesari. Then, it has to send it about 1,050 km away to Hyderabad in Telangana to convert it into DASDA. Thereafter, it has to send DASDA back to Gujarat in the Dahej plant, which is about 1,020 km away from Hyderabad.

Therefore, an investor would appreciate the long distances the products have to travel to be converted from Toluene to OBA. Moreover, an investor would note that some of these products are hazardous and require special transport arrangements like special containers, speed limits, temperature etc., which further increases the cost of transportation and hence, the cost of inventory management and production.

Further advised reading: How to do Business Analysis of a Company

Such a production process where dangerous chemicals are moved crisscross across the country to make the final product puts pressure on the efficiency of inventory management. As a result, the more OBA the company produced, the more its inventory turnover suffered. It seems to be one of the key reasons for the decline in the inventory turnover ratio (ITR) of Deepak Nitrite Ltd declined from 10.6 to 6.7 during FY2013-FY2018.

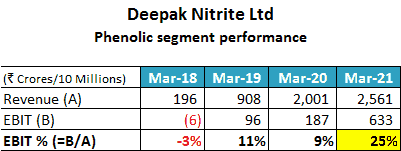

Deepak Nitrite Ltd started the production of its Phenol plant at Dahej, Gujarat in November 2018 (FY2019) in its wholly-owned subsidiary, Deepak Phenolics Ltd (DPL). This plant is a very large plant when compared to the existing size of business operations of Deepak Nitrite Ltd. Therefore, any improvement or deterioration in the operating efficiency of the Phenol plant was going to significantly affect the entire company.

In the case of Phenol production as well, the company had to undertake significant transportation of its raw material because its key raw material to produce Phenol, Benzene, is sold by refineries. In the case of many international manufacturers of Phenol, they have their plants within the refinery premises in order to reduce the cost of production. However, Deepak Nitrite Ltd did not enjoy such an advantageous location.

The company highlighted it as one of the major disadvantages to its shareholders in its conference call in February 2021 (pages 14-15).

Maulik Mehta: Our competitive disadvantage primarily, if I am comparing to global marquee players in the same segment, is that they manufacture phenol and acetone right next to their raw material sources. So normally they do it attached to a refinery… and we have no easy access to putting the plant up in the same premises as refiners.

Therefore, the company had to tie up with large refineries present at a distance. It even had to consider sourcing the raw material, benzene, from faraway places like Bhatinda in Punjab about 1,250 km away.

Conference call, May 2021, page 9:

Maulik Mehta: …Now there is a new benzene plan that is coming up in Bhatinda, so we continue to see small, medium and big opportunities to optimize our supply chain…

Deepak Nitrite Ltd has acknowledged that the cross-country shipment of hazardous chemicals in its production process poses a risk and as a result. As a result, it has done special arrangements to contain the damages in any toward incident like placing first respondents at every 120 km on the route.

FY2019 annual report, page 69:

Considering the cross-country movement of over 6 Lakhs MT of explosive/hazardous materials, DPL is committed towards improving the safety standards for road transportation. DPL has interfaced with Loss Control Services (LCS) for ‘First Respondents’ services with an aim to minimise the environmental and social impact of in-transit incidents. LCS has a strong network of First Respondents stationed every 120 kms between the facility and DPL’s sources/destinations. LCS’s teams possess adequate know-how and experience in handling materials and are equipped with a 24-hour central control room.

Looking at the dangerous nature of the chemicals being transported, Deepak Nitrite Ltd has implemented a logistic safety management system, which does real-time, GPS-based monitoring of its transport vehicles.

FY2020 annual report, page 81:

Logistic Safety Management System: Your Company has, along with its peers, founded Nicer Globe, an independent platform, which provides real-time monitoring of the movement of dangerous goods across the length and breadth of India…with GPS for real-time monitoring for the safety of its customers, carriers, suppliers, distributors and contractors.

An investor would appreciate that all these special arrangements to transport dangerous products increase the cost of production. Therefore, in order to control the costs and be competitive with the larger multinational manufacturers, the company had to improve the efficiency of its logistical activities.

The company highlighted to the investors that it has put in a lot of effort and technology to save on logistics costs in order to be competitive.

Conference call, May 2021, page 8:

Maulik Mehta: I think here again it is the pennies that take care of the pounds, we do software modeling, we do a lot of analysis about how we can manage material movement without risking too much.

The management of the company stated that the logistics planning in the production process involves so much time & effort that it looks like they are a logistics company that happens to produce phenol and acetone.

Conference call, May 2021, page 8:

Maulik Mehta: …I still remember Mr. Mehta’s one point to a group of investors, he said that sometime the phenolic business seems like we were actually running a logistics company that happens to make phenol and acetone.

Therefore, an investor would appreciate that due to the strong focus on logistics planning in the phenol business, which is now about 58% of the overall revenue of Deepak Nitrite Ltd in FY2021, the company has done significant improvements in the efficiency of inventory management.

Therefore, it seems to be the major reason for the improvement in the inventory turnover ratio (ITR) of Deepak Nitrite Ltd since FY2019 when the Phenol plant became functional. The ITR of Deepak Nitrite Ltd has increased from 6.7 in FY2018 to 11.0 in FY2021.

Going ahead, an investor should monitor the inventory turnover ratio of Deepak Nitrite Ltd so that she can assess whether the company is utilizing its inventory efficiently or not.

Further advised reading: Inventory Turnover Ratio: A Complete Guide

c) Analysis of receivables days of Deepak Nitrite Ltd:

While analysing the receivables days of Deepak Nitrite Ltd, an investor would notice that the receivables days of the company used to be in the range of 72 days to 85 days from FY2013 to FY2018. Thereafter, the receivables days improved to 57 days in FY2021. The significant change in the business of Deepak Nitrite Ltd during recent years (since FY2019) has been the operationalization of the phenol plant.

Deepak Nitrite Ltd is currently, the largest domestic producer of phenol with a market share of about 65%.

FY2020 annual report, page 27:

Through DPL, we achieved a key milestone by substituting majority of the local market imports of Phenol and Acetone, and reportedly attaining a market share of about 65% in the country.

It seems that due to a strong position in the phenol market, Deepak Nitrite Ltd is able to get its money for phenol from the customers in a comparatively shorter period than in the case of other products. As a result, its receivables days have witnessed an improvement ever since the phenol plant has become operational.

Going ahead, an investor should keep a close watch on the receivables position of the company to monitor whether its receivables days go back to the previous levels of 72-85 days.

Further advised reading: Receivable Days: A Complete Guide

From the above discussion, an investor would appreciate that in the last 10-years; Deepak Nitrite Ltd has kept its efficiency of inventory management under control and has improved its efficiency of receivables collection. As a result, the company has been able to grow in the last 10-years without deterioration of its working capital position.

When an investor compares the cumulative net profit after tax (cPAT) and cumulative cash flow from operations (cCFO) of Deepak Nitrite Ltd for FY2012-21, then she notices that over the last 10-years (FY2012-FY2021), the company has converted its profit into cash flow from operations.

Over FY2012-21, Deepak Nitrite Ltd reported a total net profit after tax (cPAT) of ₹1,951 cr. During the same period, it reported cumulative cash flow from operations (cCFO) of ₹2,384 cr.

It is advised that investors should read the article on CFO calculation, which would help them understand the situations in which companies tend to have the CFO lower than their PAT. In addition, the investors would also understand the situations when the companies would have their CFO higher than the PAT.

Further advised reading: Understanding Cash Flow from Operations (CFO)

Learning from the article on CFO will indicate to an investor that the cCFO of Deepak Nitrite Ltd is higher than the cPAT due to the following factors:

- Depreciation expense of ₹613 cr (a non-cash expense) over FY2012-FY2021, which is deducted while calculating PAT but is added back while calculating CFO.

- Interest expense of ₹494 cr (a non-operating expense) over FY2012-FY2021, which is deducted while calculating PAT but is added back while calculating CFO.

The Margin of Safety in the Business of Deepak Nitrite Ltd:

a) Self-Sustainable Growth Rate (SSGR):

Read: Self Sustainable Growth Rate: a measure of Inherent Growth Potential of a Company

Upon reading the SSGR article, an investor would appreciate that if a company is growing at a rate equal to or less than the SSGR and it can convert its profits into cash flow from operations, then it would be able to fund its growth from its internal resources without the need of external sources of funds.

Conversely, if any company attempts to grow its sales at a rate higher than its SSGR, then its internal resources would not be sufficient to fund its growth aspirations. As a result, the company would have to rely on additional sources of funds like debt or equity dilution to meet the cash requirements to generate its target growth.

An investor may calculate the SSGR using the following formula:

SSGR = NFAT * NPM * (1-DPR) – Dep

Where,

- SSGR = Self Sustainable Growth Rate in %

- Dep = Depreciation rate as a % of net fixed assets

- NFAT = Net fixed asset turnover (Sales/average net fixed assets over the year)

- NPM = Net profit margin as % of sales

- DPR = Dividend paid as % of net profit after tax

(For systematic algebraic calculation of SSGR formula: Click Here)

While analysing the SSGR of Deepak Nitrite Ltd, an investor would notice that over the years, the company had an SSGR in the single digits. It is only recently that a significant improvement in the product prices due to supply chain disruptions in China as well as in the sea trade has allowed Deepak Nitrite Ltd to enjoy very high-profit margins.

FY2020 annual report, page 55:

This performance has been partially caused by supernormal realisation in DASDA owing to China’s temporary disruption and hence may be seen in light of this.

The company even acknowledged that such margins are not sustainable.

Conference call, August 2021, page 18:

Sanjay Upadhyay: …Phenol, of course, you can’t expect this kind of EBITDA margins every quarter, so I cannot commit on that.

An investor would appreciate that the recent high prices of the products have led to an improvement in the profit margins of Deepak Nitrite Ltd, which may not sustain at these levels going ahead. These high margins have increased its SSGR in recent years to 20%. Any correction in the margins in the future may lead to a decline in the SSGR of Deepak Nitrite Ltd.

Therefore, an investor is looking at a situation, where over most of the last 10-years, the SSGR of Deepak Nitrite Ltd has been in the single digits whereas, over the same period, the company has grown its sales at a CAGR of about 21%.

As the company has grown its sales more than its SSGR; therefore, in order to grow its sales from ₹790 cr in FY2012 to ₹4,360 cr in FY2021, the company has to raise additional capital in the form of incremental debt and equity dilution multiple times.

Over the last 10-years (FY2012-FY2021), the company has raised an additional debt of ₹329 cr as its total debt has increased from ₹261 cr in FY2012 to ₹590 cr in FY2021 (329 = 590 – 261).

Over and above the debt, in the last 10-years, Deepak Nitrite Ltd has diluted its equity three times for meeting the funds’ requirements of the phenol plant. It raised a total of ₹383 cr from FY2016 to FY2018.

- FY2016: QIP1: ₹83.3 cr (FY2016 annual report, page 43)

- FY2017: QIP2: ₹150 cr (FY2017 annual report, page 5)

- FY2018: QIP2: ₹150 cr (FY2018 annual report, page 21)

Therefore, an investor would notice that during the last 10-years (FY2012-FY2021), the company has grown its business beyond what its internal resources could sustain in the terms of SSGR. As a result, it had to raise a total of ₹712 cr (additional debt: ₹329 cr + additional equity: ₹383 cr) to meet its funds’ requirement.

Deepak Nitrite Ltd has always followed the route of taking on additional capital for its growth because even in the previous decade, it had raised additional equity. Deepak Nitrite Ltd raised about ₹45 cr in May 2006 by way of a rights issue and about ₹15 cr by way of conversion of warrants in February 2010 (QIP prospectus, January 2018, page 62).

Deepak Nitrite Ltd realizes that its growth aspirations are beyond what its internal resources can sustain in terms of SSGR. The recent increase of SSGR in FY2021 to 20% seems to be based on unsustainable product prices and profit margins.

The company realizes it. Therefore, the company has made it very clear that in order to maintain the growth momentum; it would have to continue raising additional capital by way of incremental debt and equity dilution.

In 2021, Deepak Nitrite Ltd intimated to its shareholders that it is not looking forward to becoming a debt-free company indicating that it will keep raising debt for expanding its business.

Conference call, February 2021, page 9:

Somsekhar Nanda: …never ever we have said that we would like to be zero debt Company or a low levered Company. We would like to grow, and which means you will have to infuse capital in form of debt or equity. And for that matter, if we have to increase our debt levels, that is fine…

Conference call, August 2021, page 13:

Maulik Mehta: But, in fact, Mr. Sanjay Upadhyay has told us many times that, look, he is very tired of people asking him about zero debt, he is not interested in being a zero-debt Company.

The company also realizes that its funds’ requirements are beyond what its internal resources can provide. Therefore, to fund its recently announced capital expenditure of about ₹1,200 cr for new products like solvents, fluorination platform, brownfield expansion of existing products and more capex to be announced later, Deepak Nitrite Ltd has already initiated the process to raise additional equity.

In December 2021, Deepak Nitrite Ltd has initiated a postal ballot process to obtain approvals from its shareholders for a qualified institutional placement (QIP) of about ₹2,000 cr. In the postal ballot notice to the shareholders for approving the QIP, the company has acknowledged that the internal resources of the company would only be able to meet a partial funds’ requirement. Therefore, it would have to raise additional money by way of equity dilution.

The corporate announcement, December 29, 2021, page 9:

While it is expected that the internal generation of funds would partially meet the funding requirement of its growth objectives, it is thought prudent for the Company to have enabling approvals to raise capital at an appropriate time for the purpose of funding some of these growth opportunities…

From the above discussion, an investor would appreciate that Deepak Nitrite Ltd is continuously relying on outside capital for meeting its growth aspirations. Frequently raising equity money by way of qualified institutional placements (QIP) and debt is a clear indication in this regard.

Moreover, when an investor analyses the history of Deepak Nitrite Ltd right from its beginning in 1970, then she notices that the company has launched its initial public offer (IPO) on the Bombay Stock Exchange (BSE) in 1971 even before it had started manufacturing any product. Effectively, Deepak Nitrite Ltd constructed its first manufacturing plant by raising equity money from public shareholders via an IPO.

Source: Company website: Legacy

It was this very trust that gave Deepak Nitrite’s very first IPO great success. Conducted even before the company had started manufacturing, it was oversubscribed by 20 times.

Therefore, an investor would notice that Deepak Nitrite Ltd started the foundation of its entire business by raising equity from outside shareholders even before it could start manufacturing a product. Therefore, it seems that consistently relying on additional money is a consistent practice at Deepak Nitrite Ltd. and it has shown the same by relying on debt and QIP in the past and also by going for approval for another QIP for its upcoming capital expansion plans.

Nevertheless, an investor should appreciate that the growth aspirations of the company are beyond what its internal resources can sustain and the recent increase in SSGR is due to abnormally high product prices and elevated profit margins, which may not sustain in the future.

The company has acknowledged it and the investor may keep a close watch on the equity dilution levels and incremental debt that Deepak Nitrite Ltd raises so that she may timely assess whether these are in the best interests of the shareholders or the company is going overboard.

An investor arrives at a similar conclusion when she analyses the free cash flow (FCF) position of Deepak Nitrite Ltd.

b) Free Cash Flow (FCF) Analysis of Deepak Nitrite Ltd:

While looking at the cash flow performance of Deepak Nitrite Ltd, an investor notices that during FY2012-2021, it generated cash flow from operations of ₹2,384 cr. During the same period, it did a capital expenditure of about ₹2,396 cr.

Therefore, during this period (FY2012-2021), Deepak Nitrite Ltd had a negative free cash flow (FCF) of (₹12) cr (=2,384 – 2,396).

In addition, during this period, the company had a non-operating income of ₹156 cr and an interest expense of ₹494 cr. As a result, the company had a total negative free cash flow of (₹350) cr (= -12 + 156 – 494). Please note that the capitalized interest is already factored in as a part of the capex deducted earlier.

In addition, during the last 10-years (FY2012-FY2021), Deepak Nitrite Ltd paid out a total dividend of ₹247 cr (excluding dividend distribution tax, DDT) to its shareholders. Over and above this amount, Deepak Nitrite Ltd would have paid a DDT of about ₹50 cr being 20% of the dividend paid. Therefore, Deepak Nitrite Ltd paid out about ₹300 cr to its shareholders in dividends and the dividend distribution tax.

Therefore, Deepak Nitrite Ltd faced a total cash flow deficit of about ₹650 cr (= 350 + 300).

Deepak Nitrite Ltd resorted to meet this cash flow gap by way of raising incremental debt of ₹329 cr as its total debt has increased from ₹261 cr in FY2012 to ₹590 cr in FY2021 (329 = 590 – 261). Over and above the debt, in the last 10-years, Deepak Nitrite Ltd has diluted its equity three times for meeting the funds’ requirements of the phenol plant. It raised a total of ₹383 cr from FY2016 to FY2018.

Going ahead, an investor should keep a close watch on the free cash flow generation by Deepak Nitrite Ltd to understand whether the company continues to generate surplus cash from its operations.

Further advised reading: Free Cash Flow: A Complete Guide to Understanding FCF

Self-Sustainable Growth Rate (SSGR) and free cash flow (FCF) are the main pillars of assessing the margin of safety in the business model of any company.

Further advised reading: 3 Simple Ways to Assess “Margin of Safety”: The Cornerstone of Stock Investing

Additional aspects of Deepak Nitrite Ltd:

On analysing Deepak Nitrite Ltd and after reading annual reports, DRHP, its credit rating reports and other public documents, an investor comes across certain other aspects of the company, which are important for any investor to know while making an investment decision.

1) Management Succession of Deepak Nitrite Ltd:

Deepak Nitrite Ltd is a part of the Deepak group, which was founded by Mr C. K. Mehta. Currently, Mr C. K. Mehta is the chairman-emeritus of the company since August 5, 2016 (FY2017 annual report, page 46).

At present, four members of the Mehta family are a part of the board of directors and executive management of the company.

- Mr Deepak C. Mehta (age 66 years) son of Mr C. K. Mehta is the chairman and managing director of the company.

- Mr Ajay C. Mehta (age 63 years) son of Mr C. K. Mehta and brother of Mr Deepak Mehta is a non-executive director of the company. He resigned from the position of managing director of Deepak Nitrite Ltd from December 1, 2017 (FY2018 annual report, page 61). Currently, he is the managing director of one of the group companies, Deepak Novochem Technologies Limited (FY2020 annual report, page 31).

- Mr Maulik D. Mehta (age 38 years) son of Mr Deepak C. Mehta is the executive director and chief executive officer of the company.

- Mr Meghav D. Mehta (age 34 years) son of Mr Deepak C. Mehta and brother of Mr Maulik D. Mehta is the executive director of Deepak Phenolics Ltd, the wholly-owned subsidiary of the company (FY2021 annual report, page 21).

The following disclosures in the annual reports of Deepak Nitrite Ltd would help an investor understand the relationships of the various members of the Mehta family with each other.

FY2014 annual report, page 41:

Mr Meghav D. Mehta: Grandson of Shri Chimanlal K. Mehta, son of Shri Deepak C. Mehta and nephew of Shri Ajay C. Mehta

FY2019 annual report, page 59:

Mr Deepak C. Mehta: Father of Shri Maulik D. Mehta and Brother of Shri Ajay C. Mehta

Therefore, an investor would note that currently, three generations of the Mehta family are associated with Deepak Nitrite Ltd. The founder-promoter is appointed as the chairman emeritus of the company and the members of the other two generations are present as executive members.

The presence of younger family members at executive positions within the group, while the senior members are still handling responsibilities, looks like a good succession plan. This is because the young members can learn about the fine nuances of the business under the guidance of senior members until the seniors decide to take retirement.

Currently, it looks like Mr Deepak C. Mehta and his family are taking care of Deepak Nitrite Ltd and his brother Mr Ajay C. Mehta is taking care of Deepak Novochem Technologies Limited.

Within the family of Mr Deepak C. Mehta, it seems that his younger son Mr Meghav D. Mehta is being groomed to handle the phenolic segment under Deepak Phenolics Ltd whereas his elder son Mr Maulik D. Mehta is being groomed to handle other chemicals segments of Deepak Nitrite Ltd.

Going ahead, an investor may keep a close watch on the relationships among the promoter family members to understand whether any ownership issues arise between them. An investor may contact the company directly for any clarifications in this regard.

Further advised reading: How to do Management Analysis of Companies?

2) Project execution by Deepak Nitrite Ltd:

From the above discussion in the section on the net fixed asset turnover ratio, an investor would remember that over the last 10-years, Deepak Nitrite Ltd has executive many capital expansion projects. An investor needs to assess these projects in terms of their completion within time and cost estimates to understand the project execution skills of the company.

2.1) Optical brightening agents (OBA) project at Dahej, Gujarat:

Deepak Nitrite Ltd intimated to its shareholders in May 2011 that it is planning to build a manufacturing plant at Dahej for an investment of about ₹150 cr. It mentioned that the plant would be completed in 15 months i.e. by August 2012.

Conference call, May 2011, page 2:

Umesh Asaikar: At Dahej we are setting up manufacturing facilities for a fine and speciality performance chemical which will result in to forward integration of one of our existing products DASDA. We will require a capital outlay of Rs. 150 Crore for this project… Both these projects are estimated to be completed in the next 15 months.

However, in the FY2014 annual report, the company intimated to its shareholders that the first stream of phase one of the project was completed in March 2013.

FY2014 annual report, page 45-46:

Phase I of your Company’s Greenfield expansion plan at Dahej commenced its first stream of commercial production in March 2013.

The rest of the project was completed in FY2015.

FY2015 annual report, page 7:

Following the Greenfield and Brownfield expansion, our facilities at Dahej and Nandesari are fully operational

Therefore, an investor would note that initially, Deepak Nitrite Ltd had estimated to complete the OBA project at Dahej in August 2012. However, the project was delayed significantly. It suffered delays of about 2 years and was completed in FY2015.

When an investor attempts to estimate the capital expenditure done by Deepak Nitrite Ltd on this project from the annual reports, then she gets the following data:

- FY2012: ₹8 cr (FY2012 annual report, page 80)

- FY2013: ₹140 cr (FY2014 annual report, page 91)

- FY2014: ₹62 cr (FY2014 annual report, page 91)

- FY2015: ₹80 cr (FY2015 annual report, page 153)

From the above data, an investor would note that Deepak Nitrite Ltd spent about ₹290 cr (= 8 + 140 + 62 + 80) on the project against an initial estimate of ₹150 cr.

Therefore, from the above discussion, it seems that the execution of the OBA project at Dahej by Deepak Nitrite Ltd left scope for improvement. This is because; the project witnessed cost as well as time overruns.

2.2) Nandesari: brownfield expansion project of Inorganic intermediates (solar storage salts):

In May 2011, Deepak Nitrite Ltd intimated to its shareholders that it is going for a brownfield expansion project at Nandesari near Vadodara for an investment of about ₹50 cr. It mentioned that the plant would be completed in 15 months i.e. by August 2012.

Conference call, May 2011, page 2:

Umesh Asaikar: We are also planning to expand our facility at Nandesari in Gujarat. This expansion is especially being executed for growth on our inorganic intermediates business…With a capital outlay of only Rs. 50 Crore… Both these projects are estimated to be completed in the next 15 months.

However, the project witnessed a delay, as it could not be completed by August 2012. It was completed in June 2013.

FY2014 annual report, page 45:

The Brownfield expansion at the Nandesari facility was commissioned in June 2013

When an investor attempts to estimate the capital expenditure done by Deepak Nitrite Ltd on this project from the annual reports, then she gets the following data:

- FY2012: ₹19 cr (FY2012 annual report, page 80)

- FY2013: ₹3 cr (FY2014 annual report, page 91)

- FY2014: ₹56 cr (FY2014 annual report, page 91)

From the above data, an investor would note that Deepak Nitrite Ltd spent about ₹78 cr (= 19 + 3 + 56) on the project against an initial estimate of ₹50 cr.