The current section of the “Analysis” series covers Stallion India Fluorochemicals Ltd, an Indian company operating in the refrigerant & industrial gases sector, working on debulking, blending and distribution of gases like Hydrocarbons (HC), Hydrofluorocarbons (HFCs), and Hydrofluoroolefins (HFOs) for industries like air conditioning, refrigeration, fire-fighting, automobiles, pharmaceuticals etc.

Please note that to get maximum benefit from this article, an investor should focus on the process of analysis instead of looking for good or bad aspects of the company. She should learn the interpretation of diverse types of data and transactions, and pay attention to the parts of annual reports etc., used to get the information. This will help her improve her stock analysis skills.

Stallion India Fluorochemicals Ltd: Detailed Fundamental Analysis

Stallion India Fluorochemicals Ltd does not have any subsidiaries, joint ventures or any child entities. Therefore, over the years, the company has published only standalone financials.

We believe that while analysing any company, an investor should always look at the company as a whole and focus on financials, which represent the business picture of the entire company, including its subsidiaries, joint ventures etc. Consolidated financials of a company present such a picture. Therefore, if a company reports both standalone as well as consolidated financials, then the investor should prefer the analysis of the consolidated financials of the company.

As a result, while analysing the past financial performance of Stallion India Fluorochemicals Ltd, we have analysed its standalone financials.

Further recommended reading: Standalone vs Consolidated Financials: A Complete Guide

With this background, let us analyse the financial performance of Stallion India Fluorochemicals Ltd.

Financial and Business Analysis of Stallion India Fluorochemicals Ltd:

Financial performance of Stallion India Fluorochemicals Ltd from FY2021 onwards is available in readily publicly available documents like the red herring prospectus (RHP) and its annual reports.

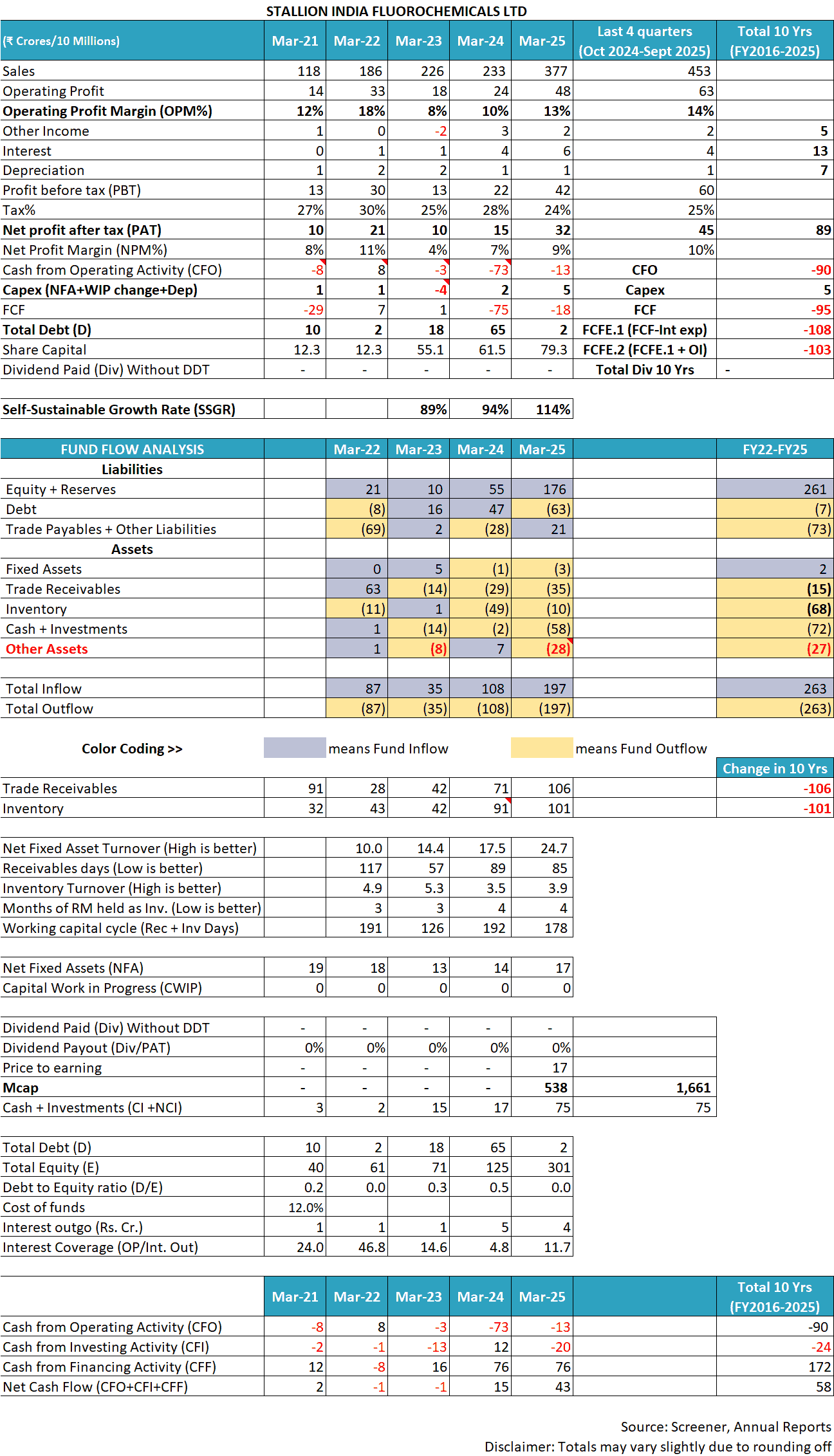

Stallion India Fluorochemicals Ltd has grown its sales from ₹118 cr in FY2021 to ₹377 cr in FY2025 at an annualised rate of 33%. Further, in the last 12 months (Oct. 2024-Sept 2025), it increased its sales further to ₹453 cr.

However, its profit margins did not show such consistent growth. Instead, both operating profit margin (OPM) and net profit margin (NPM) have shown cyclical trends.

The OPM was 12% in FY2021 and increased to 18% in FY2022, and thereafter, it declined sharply to 8% in FY2023. Post FY2023, the OPM has consistently improved to 13% in FY2025 and 14% in the last 12 months (Oct. 2024-Sept 2025).

The net profit margin (NPM) of Stallion India Fluorochemicals Ltd has followed a similar trend. It increased from 8% in FY2021 to 11% in FY2022; then decreased to 4% in FY2023, and then increased to 9% in FY2025. In the last 12 months (Oct. 2024-Sept. 2025), the NPM increased further to 10%.

To understand more about Stallion India Fluorochemicals Ltd and fluctuations in its profit margins, an investor needs to read the publicly available documents of the company like its annual reports from FY2021 available on company’s website (here, here), red herring prospectus dated January 21, 2025 for its initial public offer (IPO), as well as corporate announcements submitted by the company to stock exchanges etc.

In addition, an investor should also read the following article explaining the key factors affecting the business of chemical companies: How to do Business Analysis of Chemical Companies

The above-mentioned documents show the following key aspects about the business of Stallion India Fluorochemicals Ltd, which are critical to understand for any investor.

1) Stallion India Fluorochemicals Ltd lacks pricing power over its customers because it deals in commodity products without any special differentiation:

The company supplies various refrigerants and other specialised gases to its customers, like R32, R152a, R410a, R134a, SF6 etc. These are standard chemical products where, once a required purity level is established, then a customer can easily replace the R32 gas provided by one supplier with the R32 gas from another supplier without any impact on their operations.

As a result, Stallion India Fluorochemicals Ltd loses any pricing power over its customers because if any supplier stresses on charging a higher price for these chemicals/gases, then the customer can easily buy these from other suppliers/competitors.

This lack of pricing power limits the profit margin that it can earn from its customers. Over time, the company has clearly stated that its current profit margins are peak and it would be difficult to increase them further.

Conference call transcript, Oct. 2025, page 32:

Shazad Rustomji:…current activity we are in, it will never grow. The PAT level cannot grow, meaning it’s at optimum.

Due to a lack of pricing power, Stallion India Fluorochemicals Ltd finds it difficult to pass on volatility in its input costs to its customers and has to take a hit on its profit margins when costs go up.

FY2025 annual report, page 10:

Threats: Volatility in raw material prices, particularly in refrigerants, may exert pressure on operating margins and overall cost structures.

Stallion India Fluorochemicals Ltd faces such low negotiating power over its customers because its business does not include very high value addition. At times, its business activities involve transferring the gases from large containers into small cylinders and selling them.

Red herring prospectus, January 2025, page 28:

In some instance our Raw Material and our final products are same as the gases are debulked into smaller quantities and sold in under our brand name “Stallion”.

As a result, at times, even though the contracts with customers state that the company can get reimbursement of forex changes from the customers, still, in reality, customers do not give any such benefit to the company.

Conference call transcript, August 2025, page 8:

Shazad Sheriar Rustomji:…Although your all contracts will say, okay, the dollar is at this price, but nobody really increases the price and gives you.

Advised reading: How to do Business Analysis of a Company

2) Stallion India Fluorochemicals Ltd faces intense price-based competition from large-integrated players who have created oversupply in the market:

The company faces intense competition from both global and Indian players.

FY2025 annual report, page 46:

Competitive Intensity: Both domestic and international players are active in the Indian market

As per the RHP, page 131, the global players active in the segment are: Honeywell International Inc., The Chemours Company Dongyue Group, Zhejiang Juhua Co., Ltd., Arkema Inc., and Zhejiang Sanmei Chemical Industry Co. Ltd.

Apart from global players, there are many domestic players who are larger in size and have greater market share than Stallion India Fluorochemicals Ltd.

RHP, January 2025, page 140:

- SRF Ltd (SRF, 30% market share)

- Gujarat Fluorochemicals Ltd (GFL, 26% market share)

- Navin Fluorine International Ltd (NFIL, 13% market share)

Most of the competitors of Stallion India Fluorochemicals Ltd are much larger, stronger and better integrated in their operations.

RHP, January 2025, page 167:

some of these competitors outpace us in terms of scale, considerable financial, manufacturing, research and development and other resources… more extensive product portfolios, larger sales teams, intellectual property assets and broader market appeal

Conference call, October 2025, page 12:

Shazad Rustomji:…peer companies that are there are beautifully integrated. They’re very strong companies….we would want to be like that.

RHP, January 2025, page 35:

The peer competitors has size advantage, most of the peer competitors are much larger than our company, and it may give them advantage of scale of business

As per Stallion India Fluorochemicals Ltd, these larger, stronger and better integrated competitors have already created an oversupply of products in the Indian market, and they have to sell their excess capacity in export markets.

Conference call, August 2025, page 4:

Shazad Sheriar Rustomji:…India already has sufficient capacity for R-32. And India also has excess capacity, which is exported out of India.

In addition, cheaper imports from China have flooded the Indian market to an extent that India had to put an anti-dumping duty on imports from China.

RHP, January 2025, page 30:

(“DGTR”) initiated an investigation…of anti-dumping for the import of Hydrofluorocarbon (HFC) “Component R-32” which forms the part of a Raw material used in our Business. The DGTR…imposed an anti-dumping duty of USD 1,519.70 MT.

Due to the oversupply situation in the Indian market created by much stronger Indian and global players, combined with cheaper imports from China, Stallion India Fluorochemicals Ltd faces intense price-based competition.

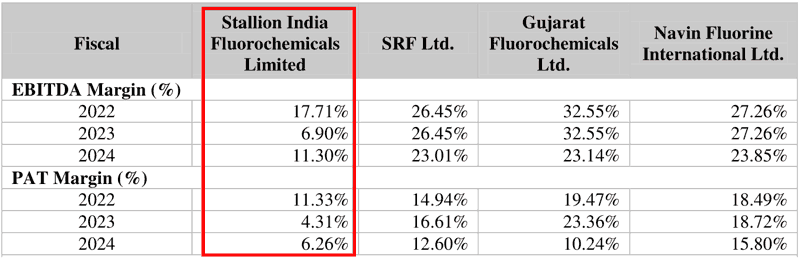

As a result, over the years, Stallion India Fluorochemicals Ltd has reported the lowest profit margins compared to its competitors like SRF, GFL and NFIL.

RHP, January 2025, page 35:

Advised Reading: How to analyse New Companies in Unknown Industries?

3) The business of Stallion India Fluorochemicals Ltd is cyclical:

As per the promoters of the company, their business faces high cyclicity in the prices of products, where from the bottom of the cycle to the peak, the prices can increase 4 times.

Conference call, May 2025, page 15:

Shazad Sheriar RustomJi: In our product, fluctuations are over 100%, meaning it’s about 300% increase is not unheard of. We have seen three cycles where the 300% increase is. So basically, the fluctuation in 4x,

Conference call, Oct. 2025, page 13:

Shazad Rustomji: helium is, say, at INR 1,200. Three years ago, the same helium was at INR 4,800.

As per the company, its products face cycles of about 5 years, with 2 years in the down-phase and then 3 years in the up-phase.

Conference call, Aug. 2025, page 11:

Shazad Sheriar Rustomji: So helium has got, like, a period where two years will be down, down, down, and, again, three years will be up. The residents (?refrigerants) also have the same cycle, two years, three years, or two years, one year up, two years again down, and three years up.

Currently, the cycle seems to be at a peak, which is also resulting in good margins for the company. As per the promoters, currently, profit margins are much higher than normal for a company like Stallion India Fluorochemicals Ltd.

Conference call, May 2025, pages 10, 17:

Shazad Sheriar RustomJi:…this is a cyclical upturn…So currently, when it’s on the up, everyone will have excellent results

Currently, EBITDA margin and the PAT margins are much higher than for a company like us, not physically currently manufacturing the molecule.

As Stallion India Fluorochemicals Ltd acknowledges that the profit margins of the company are currently higher than normal, and it is the up-phase of a cyclical business, therefore, investors should be very careful before projecting the current profit margins in the future while doing their analysis.

Advised reading: How AI Can Help Investors: Case Study of Call Transcripts

4) Non-flexible, non-fungible operations of Stallion India Fluorochemicals Ltd lead to capital-intensiveness:

As per the company, the machinery required to handle any gas is unique and cannot be used for handling other gases.

RHP, January 2025, page 33:

at our existing facilities we cannot blend new gases due to technical requirement as the facilities are set up with specific machines which only blend/debulk those gases for which the machinery is set up.

As a result, if the company wishes to expand its product portfolio to new gases, then it has to install new machinery specific to new products.

RHP, January 2025, page 33:

if we want to blend new specialty gas, we cannot do so at our existing facility as it requires installation of new machineries for blending the new gas, which will require additional capital expenditure

It is for this reason that when Stallion India Fluorochemicals Ltd planned to add gases for the semiconductor sector (e.g. Helium) to its portfolio, then it had to plan the installation of new equipment at its Khalapur, Maharashtra plant.

RHP, January 2025, page 95:

The infrastructure at the existing Khalapur facility…is tailored exclusively for HFC & HFO refrigerants. This setup is…different from what is essential for…Specialty and Semiconductor Gases

Each Semiconductor gas requires equipment tailored to its unique specifications…separate facility to maintain the integrity of each gas.

Therefore, limitations to use existing plants to process new gases/products increase investment requirements for companies that wish to expand their product portfolio.

Advised reading: How to study Annual Report of a Company

4.1) Seasonality of business adds to the capital-intensiveness of business:

Demand for refrigerant gases is highly seasonal, with summer months resulting in peak demand. As a result, February to May is the maximum demand for Stallion India Fluorochemicals Ltd. As per the company, about 45-50% demand for the year is in these 4 months.

RHP, January 2025, pages 24, 32:

The supply of our products is subject to periodical fluctuations with a significant portion of our turnover concentrated in the months from February to May

On one occasion, the promoter of Stallion India Fluorochemicals Ltd claimed that the difference in the monthly demand during the peak summer season and other months is about 10 times.

Conference call, May 2025, page 24:

Shazad Sheriar RustomJi:…the difference between season and off season or peak demand and non-demand is like 10x.

As a result, manufacturers have to install capacity to meet the peak season demand, which stays underutilised during the non-peak season.

Therefore, companies have to invest more money in their plants than they would have if the demand for their products were evenly spread across the year.

5) Risks faced by Stallion India Fluorochemicals Ltd in its business:

5.1) Regulatory risk:

Refrigerant gases, which are the key products of Stallion India Fluorochemicals Ltd, have significant global warming potential (GWP). As a result, they are at the centre of the global climate change action plan, with almost all the countries agreeing to cut down their usage.

For example, currently, under the Kigali Amendment of the Montreal Protocol, the Government of India, along with other countries, has agreed to the reduction of HydroFluoroCarbon (HFC) gases.

RHP, January 2025, page 138:

Government of India, in recognition of HFCs’ role in amplifying global warming, agreed to curtail HFC emissions, as part of the Kigali Amendment

Currently, in India, most industries use HFCs as refrigerants. However, with the government-mandated reduction in the usage of HFCs, the existing products of companies like Stallion India Fluorochemicals Ltd would risk becoming irrelevant, and as a result, investments made in the plants of HFCs might need to be written down.

5.2) Technological risks:

With advancements in the refrigerant gases field, continuously, newer products with lower global warming potential (GWP) are continuously invented. For example, first the industry used Chlorofluorocarbons (CFCs), then it shifted to Hydrochlorofluorocarbons (HCFCs) and subsequently to Hydrofluorocarbons (HFCs).

Now, the industry aims to replace HFCs with new generation Hydrofluoroolefins (HFOs).

With each such change in the product, companies need to install new machinery to handle and process newer gases, which increases the investment requirement of the company, alongside impairment of the investments made in the facilities for older/outgoing products.

In addition, other improvements in technology by industry-leading multinational companies (MNCs) force all the other players to make more investments to stay in the business.

For example, in the past, companies used to fill gas cylinders at a pressure of 200 bars, which resulted in each cylinder carrying about 7 cubic meters of gas. However, recently, Linde, which is a global giant in the gas industry, improved the technology to fill cylinders at 300 bars. This results in higher compression of gases, and now, a cylinder can carry 10-11 cubic meters of gas.

Conference call, August 2025, pages 9-10:

Shazad Sheriar Rustomji: industry standard was 200 bar cylinders…Linde…moved the standard to 300 bars… same 50-kg cylinder where you are filling 7 cubic meter, they can fill 11 cubic meter

This is definitely good for both the supplier and the customer because now each cylinder can carry more gas, resulting in lower logistics costs. However, a change of filling pressure from 200 bars to 300 bars would require investment in new handling/filling equipment along with new cylinders etc., resulting in higher investments and non-utilisation of existing equipment.

Conference call, August 2025, page 10:

Shazad Sheriar Rustomji:…it’s a major reengineering and redesign of the existing plant at huge cost…we went for complete design and reengineering the entire plant to now become a 300-bar plant

Therefore, investors need to keep in mind that any technological change can demand significant investments by companies to stay relevant in the industry.

5.3) Risk of competitors tying up with Honeywell or Chemours for HFOs:

The promoter of Stallion India Fluorochemicals Ltd has repeatedly claimed that Stallion India Fluorochemicals Ltd will benefit significantly with the mandated shift in refrigerant demand from HFCs to HFOs as per climate change agreements (Kigali amendment). The underlying reason is the agreement of Stallion India Fluorochemicals Ltd with Honeywell, which is one of the two players holding patents for HFOs; the other player being Chemours.

The promoter has declared that due to its tie-up with Honeywell, none of the competing Indian players would be able to manufacture or sell HFOs in India.

Conference call, August 2025, page 14:

Shazad Sheriar Rustomji: HFO is under heavy patent. So currently, besides Chemours and Honeywell. Honeywell has been associated with us since 20 years. So, we are basically Honeywell…None of the local big players who manufacture HFCs, they cannot manufacture or sell HFOs in India.

Stallion India Fluorochemicals Ltd claims that it will be a huge business opportunity for it because, apparently, Honeywell does not sell directly in India, and the sale of Honeywell’s HFOs will happen only via Stallion India Fluorochemicals Ltd.

Conference call, May 2025, page 22:

Shazad Sheriar Rustomji: Honeywell as in through stallion. No sales done by Honeywell then. It can only be done by us…meaning I can sell HFOs in India. My peer group cannot sell. They can’t sell one kilo.

However, there are multiple risks for investors in projecting this claim in the future.

First, the agreement of Honeywell with Stallion India Fluorochemicals Ltd is not an exclusive agreement. The promoter, Mr Shazad Rustomji, claims that even though the agreement is non-exclusive because American companies do not sign exclusive agreements; however, on the ground, it works as an exclusive agreement.

Conference call, May 2025, page 22:

Shazad Sheriar Rustomji: it’s a nonexclusive agreement. No American company signed the exclusive agreement. So everything is nonexclusive, but it’s pretty much worked as an exclusive agreement.

In addition, the agreement of Honeywell with Stallion India Fluorochemicals Ltd needs renewal every 3 years. The existing agreement is from January 1, 2023, to December 31, 2025.

RHP, January 2025, page 40:

The company is the distributor of Honeywell…The distributorship agreement…is entered and renewed on periodic basis between the parties. The exiting agreement was entered on January 01, 2023 and is set to expire on December 31, 2025

An investor may contact the company directly to understand the current status of renewal of the agreement.

Also, an investor should note that an agreement, which is kept non-exclusive and requires periodic renewal, is kept in this manner to allow the parties to look at other alternative business opportunities when they present themselves.

Therefore, if due to a shift from HFCs to HFOs, the business of existing large HFC players in India comes under the threat of absolute closure, then they will try their best to get access to HFOs by negotiating with the current patent holders. And in such a situation, a non-exclusive agreement keeps the door open for competitors of Stallion India Fluorochemicals Ltd to gain access to HFO products of Honeywell in addition to separate opportunities with Chemours.

Moreover, HFOs are going to be off-patent soon. Thereafter, everyone would get an opportunity to manufacture, market and sell HFOs.

Conference call, October 2025, page 27:

Shazad Rustomji: HFOs…The patents will expire in a couple of years. Then it’ll be free for everyone to use.

Therefore, investors should be cautious before they start projecting future business opportunities for Stallion India Fluorochemicals Ltd, assuming that the entire HFO sales from the Indian market would be served only by it. Otherwise, they might be in for a shock when HFOs find their entry into the market via other companies and contracts.

Over the years (FY2021-FY2025), the tax payout ratio of Stallion India Fluorochemicals Ltd has been in line with the standard corporate tax rate prevalent in India.

Also read: How to do Financial Analysis of a Company

Operating Efficiency Analysis of Stallion India Fluorochemicals Ltd:

a) Net fixed asset turnover (NFAT) of Stallion India Fluorochemicals Ltd:

Over the years, the company has reported NFAT of 10 to almost 25. Such a high NFAT indicates that the business of the company is fast processing with low value addition, like trading companies.

The promoter of the company explained that major operations of the company involve buying gas in big tanks and then filling it in small cylinders, and then selling it in the market.

Conference call, August 2025, pages 6-7:

Shazad Sheriar Rustomji:…we do not manufacture the molecules. What we do is we import in bulk 20-ton ISO tanks. they are unloaded into our holding tanks. They are tested…processing is done, cylinder cleaning, processing. Filling is done…goes into formulations and blending…And 30-40% of it goes to OEMs, 60-70% goes to aftermarket

An investor would note that such operations do not require a large investment in manufacturing assets, leading to a higher NFAT. Until now, Stallion India Fluorochemicals Ltd had net fixed assets of only ₹17 cr. on March 31, 2025.

Now, Stallion India Fluorochemicals Ltd plans to go into proper manufacturing of gases, which would require large investments in specialised manufacturing plants.

Conference call, August 2025, page 7:

Shazad Sheriar Rustomji: Now…this would be a proper manufacturing of the molecule per se, not a formulation or blending. That means you have a reactor. You have chimneys. You have a waste stream. You have raw materials that are different form.

Stallion India Fluorochemicals Ltd has already announced an investment proposal of ₹200 cr to put up a manufacturing plant to make R32 in Bhilwara, Rajasthan, which is much larger than its entire fixed capital base of ₹17 cr on March 31, 2025.

Corporate announcement to BSE, Oct. 24, 2025, page 2:

completion of the Bhoomi Pooja ceremony for its upcoming 10,000 MT R-32 manufacturing facility in Bhilwara, Rajasthan on Sunday, 19th October 2025… The project, involving an investment of around ₹200 crores

Until now, Stallion India Fluorochemicals Ltd has been able to manage its operations as low-value-adding trading operations, where it used to import gases in bulk and then transfer them into smaller cylinders, with some products undergoing blending and then selling them into the market. These low-value-adding operations allowed the company to have high NFAT levels.

However, now, the company wants to change its nature from trading operations to manufacturing operations requiring much larger investments.

In addition, the company is also planning to execute two projects of about ₹60 cr in Khalapur, Maharashtra (about ₹29 cr, RHP, January 2025, page 96) and Mambattu, Andhra Pradesh (about ₹30 cr, Conference call, Oct. 2025, page 15) for handling specialised gases.

Going ahead, an investor should keep a close watch on, first, whether the company is able to successfully finance and execute its large proposed projects and whether it can operate them efficiently.

Further advised reading: Asset Turnover Ratio: A Complete Guide for Investors

b) Inventory turnover ratio (ITR) of Stallion India Fluorochemicals Ltd:

Over the years, the inventory turnover ratio (ITR) of the company has been in the range of about 4, indicating that Stallion India Fluorochemicals Ltd has to keep inventory of about 3 months, more than 70% of which is finished goods.

FY2025 annual report, page 103:

The company has mentioned that it needs to keep a high amount of inventory due to high regulations on the import of its product, which increases the time to import the goods.

RHP, January 2025, page 91:

The presence of licensing norms for the import of HFCs, aligned with the Kigali Global Accord…introduces delays and extends lead times between payments and the receipt of goods…average lead time of 6 to 8 weeks between order placement and material receipt, emphasizing the necessity for higher holding levels

In FY2025, for sales of about ₹377 cr, the company carried an inventory of ₹101 cr. The promoter of Stallion India Fluorochemicals Ltd mentioned that he is ok with this level of inventory and would want to keep inventory at these levels as it helps to stabilise the business in light of disruptions in the supply chain.

Conference call transcript, August 2025, pages 23-24:

Shazad Sheriar Rustomji:…it is not a high inventory that we are sitting on. It is inventory that we would continue to carry because that allows us to two things…Number one, on the guaranteed price. And on second, on the supply side segment, the reliability factor.

As a result, Stallion India Fluorochemicals Ltd faces high working-capital-intensiveness in its operations.

RHP, January 2025, page 87:

Our business is working capital intensive and from our past experiences it is evident that Inventory and Receivables are the major part of the working capital

Going ahead, an investor should keep a close watch on the inventory levels of Stallion India Fluorochemicals Ltd to assess whether it is able to utilise its inventory efficiently.

Further advised reading: Inventory Turnover Ratio: A Complete Guide

c) Analysis of receivables days of Stallion India Fluorochemicals Ltd:

Over the years, Stallion India Fluorochemicals Ltd has seen receivables days in the range of 85-117 days.

As per the promoters, normally, the company provides a period of 60 days for customers to make payments; however, for new customers, it has to provide a longer credit period of about 120-160 days.

Conference call, May 2025, page 23:

Shazad Sheriar RustomJi:…cycle was usually about 60 days, and that flow was there. So, as we move to newer products…the new customers are all on 120-to-160-day cycles.

It seems that Stallion India Fluorochemicals Ltd faces challenges in recovering money from customers on time because it has undisputed receivables outstanding from its customers for more than 2-3 years after the due date.

On March 31, 2025, the company had about ₹5 cr of receivables outstanding for more than 2 years.

FY2025 annual report, page 104:

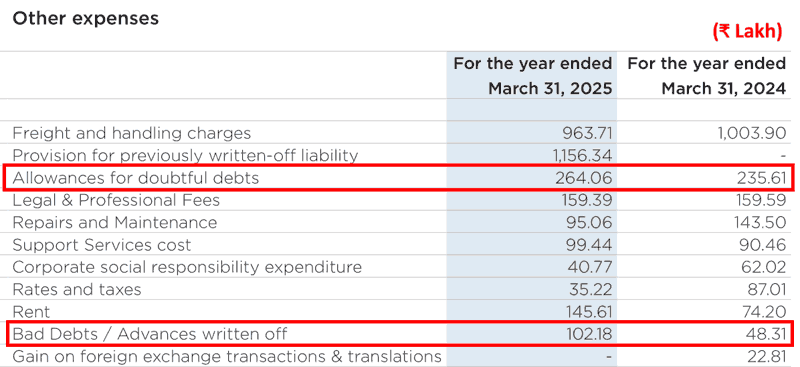

An investor would appreciate that when receivables remain overdue for a long time, there is a chance that the customers may never pay them. For example, almost every year, Stallion India Fluorochemicals Ltd has to write off about ₹2-3 cr of receivables as non-recoverable.

FY2025 annual report, page 114:

Going ahead, an investor should monitor closely whether Stallion India Fluorochemicals Ltd is able to collect its receivables on time.

Further recommended reading: Receivable Days: A Complete Guide

When an investor compares the cumulative net profit after tax (cPAT) and cumulative cash flow from operations (cCFO) of Stallion India Fluorochemicals Ltd for FY2021-FY2025, then she notices that over the years (FY2021-FY2025), the company is not able to convert its profit into cash flow from operations.

Over FY2021-25, Stallion India Fluorochemicals Ltd reported a total cumulative profit after tax (cPAT) of ₹89 cr. During the same period, it reported a cumulative negative cash flow from operations (cCFO) of (₹90) cr.

It is advised that investors should read the article on CFO calculation, which would help them understand the situations in which companies tend to have the CFO lower than their PAT. In addition, the investors would also understand the situations when the companies would have their CFO higher than PAT.

Further recommended reading: Understanding Cash Flow from Operations (CFO)

The Margin of Safety in the Business of Stallion India Fluorochemicals Ltd:

a) Self-Sustainable Growth Rate (SSGR):

Read: Self Sustainable Growth Rate: a measure of Inherent Growth Potential of a Company

Upon reading the SSGR article, an investor would appreciate that if a company is growing at a rate equal to or less than the SSGR and it can convert its profits into cash flow from operations, then it would be able to fund its growth from its internal resources without the need for external sources of funds.

Conversely, if any company attempts to grow its sales at a rate higher than its SSGR, then its internal resources would not be sufficient to fund its growth aspirations. As a result, the company would have to rely on additional sources of funds, like debt or equity dilution, to meet the cash requirements to generate its target growth.

An investor may calculate the SSGR using the following formula:

SSGR = NFAT * NPM * (1-DPR) – Dep

Where,

- SSGR = Self Sustainable Growth Rate in %

- Dep = Depreciation rate as a % of net fixed assets

- NFAT = Net fixed asset turnover (Sales/average net fixed assets over the year)

- NPM = Net profit margin as % of sales

- DPR = Dividend paid as % of net profit after tax

(For systematic algebraic calculation of SSGR formula: Click Here)

Over the years, Stallion India Fluorochemicals Ltd has had an SSGR of about 90%, which is higher than its sales growth rate of about 33%. Therefore, ideally, the company should have been able to fund its growth from its internal sources.

However, SSGR assumes that a company has converted its profits into cash flow from operations (CFO).

As discussed earlier, Stallion India Fluorochemicals Ltd has not converted its profits into CFO. On the contrary, over FY2021-2025, it has reported a deeply negative cumulative CFO of (₹90 cr) against cumulative profits of ₹89 cr.

Due to the absence of inflows from cash flow from operations, when Stallion India Fluorochemicals Ltd planned to expand its operations by creating new plants in Khalapur, Maharashtra and Mambattu, Andhra Pradesh, then it resorted to funding 100% of its project cost from the money raised in the initial public offer (IPO).

For the Khalapur, Maharashtra plant, the company proposed to fund the entire cost of ₹29.15 cr from IPO proceeds.

RHP, January 2025, page 96:

The total estimated cost of the Proposed Facility is ₹2,915.54 lakhs…and we propose to utilize ₹2,915.54 lakhs from the Net Proceeds of the Issue.

Similarly, for the Mambattu, Andhra Pradesh plant as well, the company proposed to meet the entire cost of ₹21.17 cr from the IPO money.

RHP, January 2025, page 100:

The total estimated cost of the Proposed Facility is ₹2,117.53 lakhs…and we propose to utilize ₹2,117.53 lakhs from the Net Proceeds of the Issue.

Due to the absence of cash-generating ability of the business of Stallion India Fluorochemicals Ltd, when the company planned a new “R32” manufacturing facility in Bhilwara, Rajasthan, it immediately sought shareholders’ approval to raise another ₹500 cr by issuing more equity.

FY2025 annual report, page 36:

Company purpose to raise funds upto Rs.500 Crores through issue of eligible Securities of the Company.

When an investor listens to the promoter of Stallion India Fluorochemicals Ltd speak in conference calls, then she gets the feeling that the company could not create big plants earlier, as it could not generate resources from its business. However, now, after the IPO, the promoters seem to believe that they have access to an unlimited pool of public money from which they can take any amount of money whenever they want to fund their expansion plans.

Conference call, January 2025, page 33:

Shazad Rustomji: So from the day one, we had a target set on manufacturing, never on trading…when you want to scale up from the current operations that we were to manufacturing plants, you need INR 200 crores, INR 300 crores CapEx requirements and higher…when you go into the AHF, etc., backward integration, you’ll require something like INR 450 crores, INR 500 crores.

The company is not sufficiently capitalized to do that kind of CapEx spend. So, that was the reason we moved to being a publicly listed company. So, when we’re required to raise the funds for that growth, it’s available.

Moreover, listening to the conference calls of the company indicates that the promoter is oblivious to the importance of cash flow from operations (CFO) in running a business. In fact, it seemed that the promoter is unaware of cash flow from operations as a concept and seems to be enthused only by growing profits.

Conference call, August 2025, page 26:

Luvdhavya Anchalia: Operating side usually should reflect that the order of profit we are making on a quarterly basis should turn out into cash. So, why is the cash flow on the negative side is my question?

Shazad Sheriar Rustomji: I’ll need to look into this and get back to answer…I have not fully understood. I’m not from accounts background. So, I have not fully understood your question.

From the above discussion, it turns out that the promoter and the company seem unaware of the importance of generating cash from operating activities and instead seem to plan their expansions by relying on funding from public shareholders.

The poor cash flow position of the company becomes further apparent when an investor does the free cash flow (FCF) analysis.

b) Free Cash Flow (FCF) Analysis of Stallion India Fluorochemicals Ltd:

While looking at the cash flow performance of Stallion India Fluorochemicals Ltd, an investor notices that during FY2021-FY2025, it generated a negative cash flow from operations of (₹90) cr. During the same period, it made a capital expenditure of about ₹5 cr.

Therefore, during this period (FY2021-FY2025), Stallion India Fluorochemicals Ltd had a negative free cash flow (FCF) of (₹95) cr (= -90 – 5).

In addition, during this period, the company had a non-operating income of ₹5 cr and an interest expense of ₹13 cr. As a result, the company had a total negative free cash flow of (₹103) cr (= -95 + 5 – 13). Please note that the capitalised interest is already factored in as part of the capex deducted earlier.

Stallion India Fluorochemicals Ltd funded this cash flow gap by raising about ₹160 cr in the IPO in January 2025.

Going ahead, an investor should keep a close watch on the cash flow position of Stallion India Fluorochemicals Ltd to understand whether the company is able to generate surplus cash from its business or it relies on outside funds for growth and running its day-to-day operations.

Further recommended reading: Free Cash Flow: A Complete Guide to Understanding FCF

Self-Sustainable Growth Rate (SSGR) and free cash flow (FCF) are the main pillars of assessing the margin of safety in the business model of any company.

Further advised reading: 3 Simple Ways to Assess “Margin of Safety”: The Cornerstone of Stock Investing

Additional aspects of Stallion India Fluorochemicals Ltd:

On analysing Stallion India Fluorochemicals Ltd and after reading annual reports, credit rating reports and other public documents, an investor comes across certain other aspects of the company, which are important for any investor to know while making an investment decision.

1) Management Succession of Stallion India Fluorochemicals Ltd:

The promoters of the company are Mr Shazad Sheriar Rustomji, CEO and Managing Director (age 55 years), his wife, Ms Manisha Shazad Rustomji, Executive Director (age 52 years) and their son, Mr Rohan Shazad Rustomji, Executive Director (age 26 years).

Therefore, currently, two generations of the Rustomji family are associated with Stallion India Fluorochemicals Ltd. The presence of a younger family member in an executive position on the board, while the senior members are still handling responsibilities, looks like a good succession plan. This is because the young member can learn about the fine nuances of the business under the guidance of senior members until the seniors decide to take retirement.

Advised reading: How to do Management Analysis of Companies?

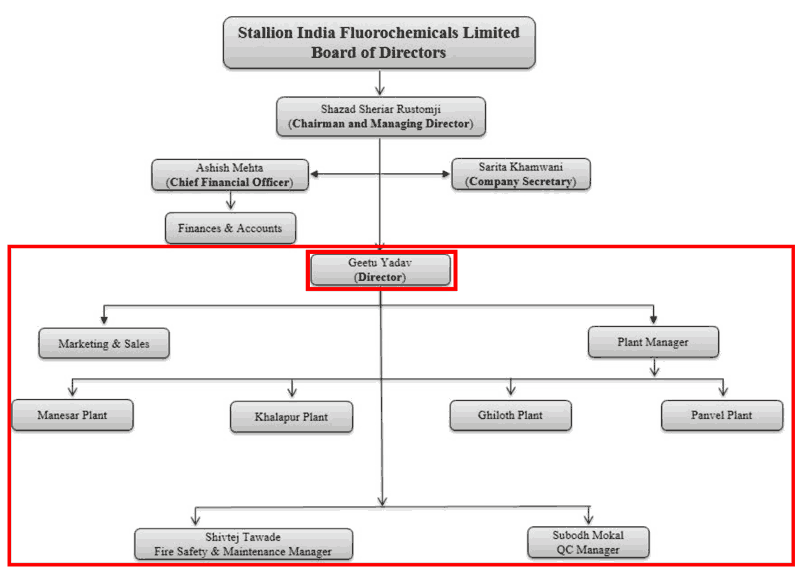

2) Ms Geetu Yadav, Executive Director, age 40 years:

Apart from the promoter family, Ms Geetu Yadav (age 40 years), Executive Director of Stallion India Fluorochemicals Ltd, seems to play a very major role in the running of the company.

She seems to handle the most responsibilities of leadership and execution in the company. As per the RHP, January 2025, page 197, Ms Geetu Yadav handles all responsibilities of marketing, sales, purchase, plant operations, quality control etc. i.e. except for finance and compliance, the entire company’s responsibilities are on the shoulders of Ms Geetu Yadav.

An investor notes that for her responsibilities, Ms Geetu Yadav receives a remuneration (₹4.4 cr), which is higher than the promoter, Mr Shazad Rustomji (₹2.6 cr).

In fact, her remuneration is higher than the remuneration of the promoter family members combined (₹3.15 cr), i.e. Mr Shazad Rustomji (₹2.6 cr), Ms Manisha Rustomji (₹0.21 cr) and Mr Rohan Rustomji (₹0.33 cr).

FY2025 annual report, page 76:

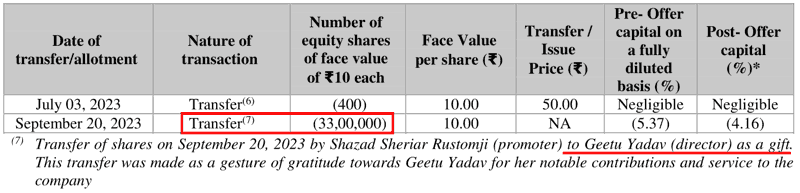

Moreover, before the IPO, the promoter, Mr Shazad Rustomji, gave Ms Geetu Yadav 3,300,000 shares of the company as a gift.

RHP, January 2025, page 78:

At the price of IPO allotment, ₹90 per share (FY2025 annual report, page 51), these 3,300,000 shares amount to a gift of about ₹30 cr.

In addition, when Stallion India Fluorochemicals Ltd proposed its employee stock options plan (ESOP) scheme in the annual general meeting (AGM) of 2025, then out of the total scheme size of 3,173,010 shares, 50% i.e. 1,586,505 shares, are reserved for Ms Geetu Yadav (Source: FY2025 annual report, pages 25 and 27).

employee Stock Options…not exceeding 31,73,010…i.e. 4% (four percent) of the issued share capital of the Company

grant, offer, issue and allot…15,86,505…Employee Stock Options (“Options)”), which constitutes 2% of the issued share capital…to Ms. Geetu Yadav, Executive Director

Therefore, it seems that Ms Geetu Yadav is the most responsible and most contributing employee of Stallion India Fluorochemicals Ltd, who runs almost the entire company. As a result, she is given remuneration more than all promoter family members combined, a gift of shares of about ₹30 cr and 50% of all the ESOPs are reserved for her.

As a result, an investor would assume that Ms Geetu Yadav, Executive Director, would be present in each and every board meeting and would contribute extensively and lead the strategic direction of the company. However, the records of attendance of Ms Geetu Yadav in board meetings show a different picture.

- In FY2025, out of the 14 board meetings held by Stallion India Fluorochemicals Ltd, Ms Geetu Yadav attended only 2 meetings (3rd and 14th board meetings) (Source: FY2025 annual report, pages 70-73).

- In FY2024, Ms Geetu Yadav attended only 5 out of the total 15 board meetings (Source: FY2024 annual report, page 18).

- In FY2023, Ms Geetu Yadav attended only 1 out of the total 7 board meetings (Source: FY2023 annual report, page 28).

Being the highest paid and most responsible employee, an investor would expect that she would be most aware of the state of business of the Stallion India Fluorochemicals Ltd and would contribute extensively during the conference calls of the company with stakeholders while discussing quarterly results.

However, it turns out that out of the three conference calls held by Stallion India Fluorochemicals Ltd until now (May, August and October 2025), Ms Geetu Yadav attended two of them (May and August 2025) and did not speak a single word in the entire conference call.

Conference call, May 2025, page 3:

Parth Raorane: The company is represented by Mr. Shazad Sheriar Rustom Ji, he is the Managing Director & CEO, and Mrs. Geetu Yadav, who is the Director

Conference call, August 2025, page 2:

Parth Raorane: The company today is represented by Mr. Shazad Sheriar Rustomji, the Managing Director and CEO of the company, and Mrs. Geetu Yadav, the Director

In the August 2025 conference call, when the promoter, Mr Shazad Rustomji, was not able to answer the query of an investor, Mr Luvdhavya Anchalia, about negative cash flow from operations, even then, Ms Geetu Yadav did not contribute/say anything to answer the investor’s query.

Ms Geetu Yadav did not attend the third conference call held by Stallion India Fluorochemicals Ltd in October 2025.

Conference call, Oct. 2025, page 2:

Parth Raorane: company will be represented by Mr. Shazad Rustomji, who is the Managing Director and CEO.

Moreover, upon a Google search, we are unable to find any public media presence of Ms Geetu Yadav apart from her status as Executive Director at Stallion India Fluorochemicals Ltd in the financial websites. The search does not bring out any LinkedIn profile, any other social media profile like X/Twitter etc., any other news article about her representing the company’s activities or any interview with media outlets about the company etc.

An investor may do her own assessment about the value contributed by Ms Geetu Yadav to Stallion India Fluorochemicals Ltd and the benefits that public shareholders derive from the maximum remuneration being paid out to her by the public-listed company.

Investors may contact the company directly for any clarifications in this regard.

Advised reading: Why We cannot always Trust What Management Claims

3) Sharp increase in promoters’ and Ms Geetu Yadav’s remuneration in FY2025:

Stallion India Fluorochemicals Ltd came out with its IPO in FY2025. In the same year, all the promoters and Ms Geetu Yadav had a substantial jump in their remuneration as compared to the pre-IPO year (FY2024).

- Remuneration of Ms Geetu Yadav increased by about 15 times from ₹30 Lakh in FY2024 to ₹440.6 Lakh (₹4.4 cr) in FY2025

- Remuneration of Mr Shazad Rustomji increased by more than 10 times from ₹24 Lakh in FY2024 to ₹261 Lakh (₹2.61 cr) in FY2025

- The remuneration of Mr Rohan Rustomji increased by more than 6 times from ₹5.3 Lakh in FY2024 to ₹32.7 Lakh in FY2025

- Remuneration of Ms Manisha Rustomji increased by 75% from ₹12 Lakh in FY2024 to ₹21 Lakh in FY2025

FY2025 annual report, page 76:

An investor may do her own assessment and form her opinion about such a sharp increase in remuneration by promoters and Executive Directors upon IPO of the company.

Advised reading: How to identify Promoters extracting Money via High Salaries

4) Related party transactions of Stallion India Fluorochemicals Ltd and a sharp increase in rent in FY2025:

The company has entered into multiple related party transactions with promoters, and among the most prominent of them is the rent payments to the promoter, Mr Shazad Rustomji.

In FY2024, Stallion India Fluorochemicals Ltd paid a rent of ₹36 lakh to Mr Shazad Rustomji; however, in FY2025, the rent increased to ₹120 lakh (₹1.2 cr).

FY2025 annual report, page 124:

In such situations of payments to promoters by public-listed companies, an investor should be cautious in her analysis because these transactions provide an opportunity for the shifting of economic benefits from public shareholders to promoters.

The investor should assess whether the rent payments are in line with the market rental prevalent for such properties. She should also ascertain the reasons for such a sharp increase in rent payments when the company came out with its IPO.

She may contact the company directly for any further clarifications.

Advised reading: How Promoters benefit from Related Party Transactions

5) Issues in the utilisation of IPO money by Stallion India Fluorochemicals Ltd:

As the IPO size of Stallion India Fluorochemicals Ltd was more than ₹100 cr, therefore, as per SEBI regulations, the company had to appoint an agency (CARE Ratings Ltd, CARE) for monitoring its utilisation of IPO money.

In its quarterly monitoring reports, CARE has highlighted multiple issues in the utilisation/spending of money by Stallion India Fluorochemicals Ltd.

For example, in its report for March 31, 2025, CARE highlighted that Stallion India Fluorochemicals Ltd claimed to spend ₹11.98 cr on issue (IPO) expenses; however, out of these, the company could not provide bills/invoices for ₹8.64 cr. Moreover, in the bank account statements of the company, CARE could not trace ₹4.75 cr of transactions claimed as issue (IPO) expenses.

Monitoring agency report for March 31, 2025, by CARE, page 8:

Of the total issue expense of Rs.11.98 crore, bank transactions of Rs.4.75 crore could not be traced. Also, for Rs.8.64 crore, supporting invoices were not provided.

Moreover, the company has disclosed in the RHP that it would spend ₹11.99 cr on issue (IPO) expenses (Source: RHP, January 2025, page 85), out of which, until March 31, 2025, it had spent ₹11.98 cr, which is expected as the IPO was completed in January 2025.

However, all of a sudden, in the September 30, 2025 quarter, Stallion India Fluorochemicals Ltd claimed to spend another ₹3.99 cr for issue (IPO) expenses.

Monitoring agency report for September 30, 2025, by CARE, page 3:

In Q2FY26 Stallion India Fluorochemicals Limited has made excess utilization of Rs.3.99 crore towards Issue expenses. Issues expenses specified in prospectus were Rs.11.99 crore, however actual spending stood at Rs.15.98 crore as on September 30, 2025 resulting in material deviation.

The monitoring agency, CARE, highlighted that the management and the chartered accountant certified these excess issue (IPO) expenses as working capital, i.e. these certificates were incorrect.

Monitoring agency report for September 30, 2025, by CARE, page 3:

The details submitted in the management and Chartered Accountant certificate incorrectly captures issue expense under working capital…this reflects discrepancy in the data submission by the company.

CARE also highlighted that, as per SEBI guidelines, for higher spending on issue expenses from the IPO money, Stallion India Fluorochemicals Ltd was supposed to take shareholders’ approval, which it did not take.

Monitoring agency report for September 30, 2025, by CARE, page 5:

Shareholder approval not available for the following deviations: As per Prospectus, the funds allocated for issue expenses were Rs.11.99 crore while the utilization towards issue expenses is Rs.15.98 crore resulting in excess utilization Rs.3.99 crore.

In addition, Stallion India Fluorochemicals Ltd used more funds for working capital (₹98.71 cr) than mentioned in the RHP (₹95 cr). As per SEBI regulations, Stallion India Fluorochemicals Ltd should have taken shareholders’ approval for such changes in the usage of IPO money. However, as per CARE, it did not take any such approval (Monitoring agency report for September 30, 2025, by CARE, page 5).

Advised reading: How to Identify if Management is Misallocating Capital

6) Delay in project execution by Stallion India Fluorochemicals Ltd:

In the RHP, while raising money from public shareholders in the IPO, the company stated that it will fund 100% of the projects’ costs from the IPO money and will complete those projects by Nov. 10, 2025 (RHP, January 2025, pages 95 and 99).

As in the IPO, the company had received the money it asked for; therefore, an investor would think that the company will go on project execution on a war footing and will try to complete it as soon as possible. However, investors were disappointed every time the company provided an update about its projects.

Every time, the company had some other reason to explain why it could not show project execution.

After its IPO in January 2025, up to March 31, 2025, the company had not spent a single rupee out of ₹21.17 cr on the Mambattu, Andhra Pradesh project and had spent only ₹64 lakh out of ₹29.15 cr (barely 2%) on Khalapur, Maharashtra project (Source: Q4-FY2025 results, May 2025, page 7).

The company provided an excuse that, because the March quarter is its best quarter in sales, therefore, it did not waste time on project execution. At the same time, the promoter mentioned that they have expanded the scope for both projects and still would complete them by Oct. 30, 2025.

Conference call, May 2025, page 6:

Shazad Sheriar RustomJi: And very honestly, we did not want to waste time or the quarter because up to March is our strongest quarter. So we did not want to waste time in, number one, in the CapEx spending

Mambattu facility was designed for five tanks…We have scaled it up to a 10-tank facility. The helium plant also, the specialty gas plant also, initial designs were different…30th October is what we are looking at completion.

As per the latest available status, by Sept. 30, 2025, on the Mambattu, AP project, Stallion India Fluorochemicals Ltd had spent only ₹2 cr out of ₹30 cr of revised cost (6.7% of total cost) and on Khalapur, MH project, spent ₹9.80 cr out of ₹29.15 cr (about 33.6% of total cost) (Sources: Q2-FY2026 results, Oct. 2025, page 5 and Conference call, Oct. 2025, page 15).

Now, instead of completing the projects on the earlier promised timeline of Oct. 30, 2025 (May 2025 conference call, page 7) or Nov. 10, 2025, in the RHP, the promoter mentioned that the projects would be completed by January end to February 2026.

Conference call, Oct. 2025, page 14:

Shazad Rustomji: we were planning to come out in by November end, we would probably move into January end or February

Even as these existing projects were getting delayed, Stallion India Fluorochemicals Ltd has announced another much larger project, “R32” manufacturing in Bhilwara, Rajasthan, with an investment budget of ₹200 cr, which again it wants to fund from public money.

Here also, the promoter has given very aggressive completion timelines of making the plant functional in 9 months by July 2025, while acknowledging that normally, companies take about 18 months to complete such a plant.

Conference call, Oct. 2025, page 16:

Shazad Rustomji: The working time, normally, a plant of that size, it would take about 18 months. We will set it up in 9 months working around the clock, including night shift, etc…By July 2026.

The promoter has continuously made tall claims of finishing projects in 50% of the time that other companies take.

Conference call, August 2025, page 26:

Shazad Sheriar Rustomji: Normally, the timelines provided by us are 50% shorter than any other company’s timelines for similar projects.

Whereas on the ground, instead of rapid project development and taking them to commencement, the company is continuously expanding the scope of projects.

For example, the Mambattu, AP project was initially planned to have 5 tanks focused on HFCs/HFOs gases. Thereafter, first, the company stated that they are expanding the scope to 10 tanks so that they can use the full development potential of the land, which will avoid them taking any shutdown in case they plan to expand the capacity later.

Conference call, May 2025, pages 6-7:

Shazad Sheriar RustomJi: In Mambattu, we are scaling up 100%…we don’t want to come to a stage where now we want to expand and we need to take a shutdown for three months for expanding the capacities. So it was decided…to complete the maximum utilization of whatever we have there and in one stage…So we’ve gone in for 100% utilization of total land, 100% utilization of whatever is possible, doubling the capacity, et cetera, and finishing it once and for all.

When an investor thought that, as the company had planned to utilise the full land potential, it could start full-fledged execution, the company came up with another update that now, it will now further expand the scope of the Mambattu project to include a semiconductor gases facility as well, apart from the originally planned HFCs and HFCs.

Conference call, August 2025, page 10:

Shazad Sheriar Rustomji: We have doubled the capacity. We have gone in for a 10-tank capacity…we have also gone for the same semiconductor facility what we have at Khalapur…We have also put that setup in the Mambattu layout…Earlier, it was two sheds. Now, it is five sheds.

Apart from expanding the scope of already announced expansion plants, Stallion India Fluorochemicals Ltd proposed to start another even larger plant for manufacturing R32 at Bhilwara, Rajasthan, even though, as discussed above, India has an oversupply of R-32.

One of the reasons provided by the promoter for the R-32 plant of ₹200 cr was that all analysts continuously asked if the company is into the manufacturing of molecules. So, now, he wants to enter into manufacturing, which the promoters have not done in more than 30 years of their business.

Conference call, August 2025, pages 4-5:

Shazad Sheriar Rustomji: And when we started, everyone wanted to know, do we manufacture the molecule? We formulate, we blend, we debulk, we pack, we provide it, but we don’t manufacture. So, now we would like to go into backward integration.

In the case of the R-32 plant as well, the company kept on expanding the scope of the project.

Originally, the promoter stated that they would go for 5,000 MTPA of R32 manufacturing, out of which the captive requirement of Stallion India Fluorochemicals Ltd would be about 2,000-3,000 MTPA. Another reason for starting with 5,000 MTPA capacity was that everyone in the industry, both in India and abroad, started with 5,000 MTPA capacity and then scaled up. Therefore, Stallion India Fluorochemicals Ltd also decided to do the same.

Conference call, August 2025, page 4:

Shazad Sheriar Rustomji: India also has excess capacity…we are looking at setting up a 10,000-ton plant for R-32….Stage 1 would be 5,000 thousand tons…Reason for going with reduced capacity is all of your industry, like all the current two manufacturers in India and…abroad…everyone has gone with the first plant that is usually of 5,000 metric tons then they scale up. So, we don’t want to be different from others. Maybe it’s a learning graph…we ourselves have a captive requirement of 2,000 tons, 3,000 tons

Dividing a large 10,000 MTPA plant into two stages in line with industry practice seemed a logical choice, as it would be the first time Stallion India Fluorochemicals Ltd would go for a proper manufacturing plant. Its other facilities are mainly bottling, debulking, and blending facilities.

However, in the October 2025 conference call, the promoter declared that they are going for the full 10,000 MTPA capacity of R-32 in one go because he is running short of time, and what would ideally take 18 months, he wants to achieve in 9 months.

Conference call, Oct. 2025, page 16:

Shazad Rustomji: it would take us minimum, minimum of 18 months to have that whole facility set up. And right now, we don’t have that time. We want to complete in 9 months the basic first stage. So, the first stage of the integration would be just the 32 manufacturer. In the second phase, earlier, we had planned 5,000 plus 5,000. Now, we’re going for 10,000 at one stroke.

The promoter of Stallion India Fluorochemicals Ltd wants to complete the projects in 50% of the time usually taken by other competitors who are much larger in size and scale of operations than Stallion India Fluorochemicals Ltd. However, he does not want to pay an advance payment to the supplier. The company claims that it does not want to pay money unless the work is done on the ground.

Conference call, August 2025, page 9:

Shazad Sheriar Rustomji: we are very prudent on how we spend money. We do not believe in giving advances too quickly. We do not believe in giving money before work is done.

An investor is left confused about whether the supplier would keep the material and machinery ready to be dispatched whenever the company wants, to complete its projects in 50% of the normal time, if they are not paid in advance. And whether it would ultimately impact the project execution on the ground.

Nevertheless, it is still in the future that an investor would get to see its impact because, as of now, the company is continuously expanding the scope of its projects and pushing the completion date further.

Advised reading: How to do Management Analysis of Companies?

7) Stallion India Fluorochemicals Ltd did not pay its supplier for the gases purchased until the supplier complained to SEBI at the time of IPO:

The company had purchased gases from Zhejiang Sanmei Chemical Industry Co. Ltd. (Sanmei) in FY2021. However, allegedly, due to some issues, it did not make payments to Sanmei.

On Dec. 2, 2021, Sanmei sent a legal demand notice for the pending payment of USD 12,51,290. However, it did not file any case in the court of law or the arbitration tribunal.

RHP, January 2025, page 30:

Sanmei’s legal representatives therefore escalated the issue by sending a demand notice on December 02, 2021, under the Insolvency and Bankruptcy Code, 2016, demanding $12,51,290.00 (“Notice”). However, there is no further proceedings.

It seems that due to the absence of any court proceedings, Stallion India Fluorochemicals Ltd did not pay the money to Sanmei and kept on sending replies to the letters/emails of Sanmei.

Stallion India Fluorochemicals Ltd even wrote back this liability, assuming that it might never have to pay this money, as a long time had passed and the supplier did not file any bankruptcy/court proceedings against it.

RHP, January 2025, page 34:

In Fiscal 2023, the Company had written back the liability of ₹949.85 lakhs, based on the belief that no further outflow of resources is probable. This decision to write back such liability was made since a substantial period of time had elapsed from the issuance of the notice by Sanmei…and no formal insolvency proceedings had been initiated by Sanmei

However, at the time of its IPO, Sanmei filed a complaint to SEBI about the dispute via the complaint portal, SCORES.

RHP, January 2025, page 30:

Company has also received a complaint on SCORES dated June 21, 2024

Once a complaint was made to SEBI, thereafter, Stallion India Fluorochemicals Ltd made the full payment of USD 1,251,290 (about ₹11 cr at ₹88 per USD) to Sanmei and settled the dispute.

FY2025 annual report, page 57:

The Company has settled dispute with…Sanmei…and made the payment of entire claim amount of USD 1,251,290 and the same was intimated to BSE and NSE on 27th June, 2025.

This incident might come across as a case where the company did not pay the money that was rightfully owed to the supplier until the supplier did not raise the issue to regulators/the court of law etc. And once the supplier escalated the issue, it made the full payment to the supplier.

Nevertheless, an investor may form her own opinion about this entire issue or contact the company directly for any clarifications.

Advised reading: How to study Annual Report of a Company

8) Withdrawal of funds by promoters from Stallion India Fluorochemicals Ltd:

In recent times, promoters have withdrawn a significant amount of money from the company.

In the IPO, promoters sold shares worth more than ₹38 cr as offer for sale (RHP, January 2025, page 1), which was the portion of IPO money that went to the promoters and not to the company.

RHP, January 2025, page 49:

The entire proceeds (net of offer expenses) from the Offer for Sale will be paid to the Promoter Selling Shareholder in proportion to his portion of the Offered Shares transferred pursuant to the Offer for Sale and our Company will not receive any such proceeds from the offer for sale component.

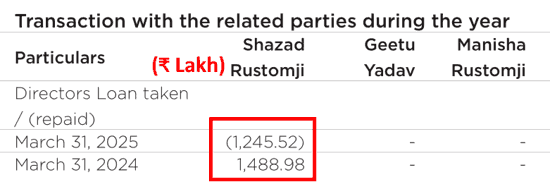

In addition, during FY2025, the year of IPO, promoters took repayment of about ₹12.5 cr of the loan given by them to the company.

FY2025 annual report, page 124:

During FY2025, Stallion India Fluorochemicals Ltd had a cash outflow from operating activities of (₹13.4 cr), cash outflow from investing activities of (₹19.7 cr). Therefore, the money used by the company to repay Mr Shazad Rustomji came from the proceeds of the IPO under cash inflow from financing activities (Source: FY2025 annual report, page 100).

Therefore, from the IPO, promoters took a total payout of more than ₹50 cr, i.e. ₹38.7 cr as offer for sale and ₹12.5 cr of loan repayment.

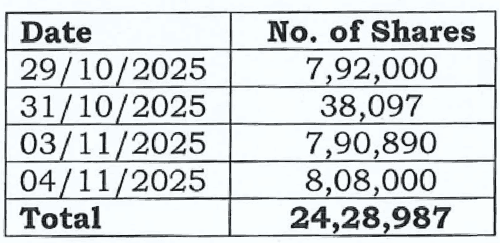

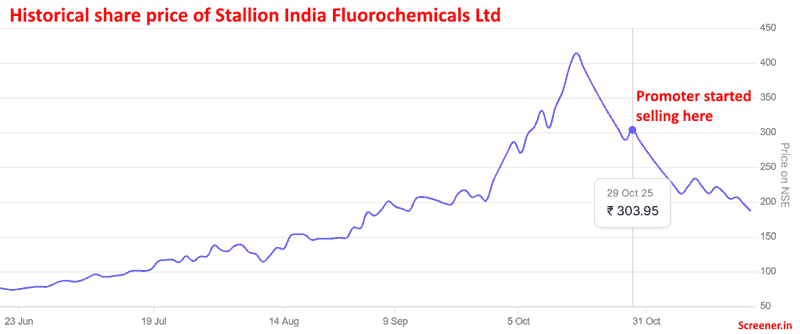

Subsequently, when the share price of Stallion India Fluorochemicals Ltd started falling sharply from mid-October, from October 29 to November 4, 2025, promoter, Mr Shazad Rustomji, sold about 3% of his stake in the company in the open market for more than ₹65 cr. These sales transactions took place on 4 days: Oct. 29, Oct. 31, Nov. 3 and Nov. 4.

Corporate announcement to BSE, Nov. 4, 2025, page 3:

The promoter disclosed the first three in the form of a press release stating that he has sold 16,20,987 shares for ₹45.74 crores to infuse back into the company as interest interest-free loan to fund the R32 project in Bhilwara, Rajasthan.

Corporate announcement to BSE, Nov. 3, 2025, page 2:

The decision to sell 16,20,987 shares amounting to ₹45.74 crores and infuse the entire amount into the company on an interest-free basis was to ensure that work on our R-32 manufacturing project at Bhilwara begins without any delay.

However, after the press release on Nov. 3, 2025, the very next day, Nov. 4, 2025, Mr Shazad Rustomji sold 808,000 more shares. The stock had hit a lower circuit at ₹247.65 on that day. So, assuming all the shares were sold at the lower circuit price, the promoter received about ₹20 cr for his sale on Nov. 4, 2025, taking the total sale value from Oct. 29 to Nov. 4, 2025, to ₹65.74 cr (=45.74 + 20).

The promoter sold these shares when the stock was in a continuous downtrend with multiple lower circuits since mid-October 2025.

The reason for such a desperate sale of shares can be to infuse capital for the project, or it can be a desperate attempt to book some profit in the recent rally while the stock price is still at a higher price than where it existed barely a few months back. Otherwise, soon after its IPO at ₹90 per share, the stock price had declined to below ₹60 before starting the current rapid rally to over ₹400, which seems to have lasted until mid-October.

As things stand today, in the recent past, the promoters have taken out more than ₹115 cr from their investments in Stallion India Fluorochemicals Ltd via ₹38 cr as offer for sale in IPO, ₹12.5 cr loan repayment and ₹65 cr as recent sale of 3.06% stake in the open market.

On Nov. 24, 2025, Stallion India Fluorochemicals Ltd intimated stock exchanges that the promoter has infused funds into the company on an interest-free basis. However, the announcement does not mention the exact amount of money infused.

Corporate announcement to BSE, Nov. 24, 2025, page 2:

Funds Received by a small sale of promoter’s stake were introduced interest free into the company.

An investor should keep a close watch on any further stake sale by the promoter, the amount of money infused by the promoter in the company by way of contacting the company directly, asking the promoter when he interacts with shareholders in the next conference call and analysing the financial statements when they are disclosed.

Advised reading: How to know if Promoters are Losing Commitment to the Company

The Margin of Safety in the market price of Stallion India Fluorochemicals Ltd:

Currently (November 25, 2025), Stallion India Fluorochemicals Ltd is available at a price-to-earnings (PE) ratio of about 33 based on earnings of the last 12 months (October 2024- September 2025).

We recommend that an investor read the following articles to assess the P/E ratio to be paid for any stock, which considers the strength of the business model of the company as well. The strength in the business model of any company is measured by way of its self-sustainable growth rate and the free cash flow generating ability of the company.

In the absence of any strength in the business model of the company, even a low PE ratio of the company’s stock may be a sign of a value trap, where, instead of being a bargain, the low valuation of the stock price may represent the poor business dynamics of the company.

- 4 Principles to Decide the Ideal P/E Ratio of a Stock for Value Investors

- How to Earn High Returns at Low Risk – Invest in Low P/E Stocks

- Hidden Risk of Investing in High P/E Stocks

Analysis Summary

Stallion India Fluorochemicals Ltd has increased its sales sharply by 33% year on year over FY2021–25; however, it operates in commoditised refrigerant gases without any meaningful differentiation, and its products are easily replaceable, taking away the pricing power of the company. As per the management, current profit margins represent peak profitability and are difficult to sustain. The company is unable to pass on volatility in input prices to its customers because its business is very low-value-adding.

The company faces intense price-based competition from much larger, integrated global and domestic players. The Indian market faces oversupply, which, coupled with very cheap imports from China, makes it a very difficult market to operate. As a result, Stallion India Fluorochemicals Ltd has lower margins when compared with its peers.

The business of refrigerant gases is capital-intensive due to non-fungible machinery; each gas requires dedicated equipment. Moreover, the business is highly seasonal, due to which players have to create a higher capacity just during the peak season of February–May.

The company faces high risks from a regulatory and technological perspective. Moreover, Stallion India Fluorochemicals Ltd.’s heavy reliance on the relationship with Honeywell is risky because the agreement is non-exclusive and requires renewal every three years. Also, the patents of HFOs will soon expire, which will open the market to all players.

The company’s business is working capital-intensive. The company holds large inventories to manage import-related delays and experiences high receivable days with regular write-offs. Despite reporting ₹89 crore of cumulative PAT over FY2021–25, it generated a deeply negative cumulative CFO of -₹90 crore, resulting in negative free cash flow.

As a result, all capacity expansions, including Khalapur, Mambattu, and the proposed R32 manufacturing plant in Bhilwar, are being funded through IPO proceeds and fresh equity raises, and not from internal cash generation.

A single executive director of the company, Ms Geetu Yadav, has received the highest compensation, has been gifted shares worth ~₹30 crore, and is allocated 50% of ESOPs, but she has a limited attendance in board meetings and almost nil participation in conference calls.

Stallion India Fluorochemicals Ltd witnessed a sharp increase in the promoter and executive remuneration in the IPO year. Similarly, rent payments to the promoter increased significantly in the IPO year. Reports by the monitoring agency, CARE, have highlighted missing invoices, untraceable transactions, and excess spending on issue (IPO) expenses without shareholder approval.

Project execution by the company has been repeatedly delayed despite aggressive commitments. Instead of completing the projects quickly, Stallion India Fluorochemicals Ltd has continuously expanded the scope of its projects.

The company withheld payments to an old supplier and paid only after the supplier complained to SEBI.

Promoters have also withdrawn significant money, more than ₹115 crore, from IPO’s offer-for-sale proceeds, loan repayment, and subsequent market sales during a sharp stock correction.

Going ahead, an investor should closely track the company’s ability to generate positive and sustainable operating cash flows and the timely and efficient execution of ongoing and proposed expansion projects. She should monitor the renewal terms of the Honeywell agreement as well as any stress on the balance sheet due to large expansions. She should assess the efficiency of working-capital management as well as changes in the shareholding of promoters to assess whether promoters withdraw further money from their investments in the company.

Further recommended reading: How to Monitor Stocks in your Portfolio

These are our views on Stallion India Fluorochemicals Ltd. However, investors should do their own analysis before making any investment-related decisions about the company.

You may use the following steps to analyse the company: “Selecting Top Stocks to Buy – A Step by Step Process of Finding Multibagger Stocks”

I hope it helps!

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

I, Vijay Malik, am a SEBI-registered Research Analyst (Regn. No. INH100008364). This article is for educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.

{kind=link}

2 thoughts on “Analysis: Stallion India Fluorochemicals Ltd”

Why would anyone want to invest in a business like Stallion India? It is puzzling. No pricing power, commoditised product, cyclical, huge working capital requirement, continuous capex, no differentiation, huge competition, rigorous pollution regulations, and questionable management integrity.

Hi Vamshi,

Thanks for writing to us!

Different investors follow different approaches to investing, and that often explains the gap: Choosing the Stock Picking Approach suitable to you

For fundamental investors, who look at business quality, cash flows, governance, and long-term durability, a company like Stallion India Fluorochemicals Ltd may raise many concerns. However, others follow technical analysis, price–volume trends, or momentum signals etc, who may not focus on the underlying business at all. For them, the stock is simply a chart, not a company.

Similarly, some investors prefer short-term investing or theme-based narratives rather than long-term fundamentals.

So while the business of any company may look unattractive to long-term fundamental investors, others may still find trading opportunities in it based on their own investing approaches.

Regards,

Dr Vijay Malik