The current section of the “Analysis” series covers Senores Pharmaceuticals Ltd, an Indian pharmaceutical company focusing primarily on the regulated markets of the USA, UK and Canada. The company also has a smaller presence in India and other emerging pharmaceutical markets.

Please note that to get maximum benefit from this article, an investor should focus on the process of analysis instead of looking for good or bad aspects of the company. She should learn the interpretation of diverse types of data and transactions, and pay attention to the parts of annual reports etc., used to get the information. This will help her improve her stock analysis skills.

Senores Pharmaceuticals Ltd: Detailed Fundamental Analysis

Currently, Senores Pharmaceuticals Ltd operates its business via multiple subsidiaries:

- Havix Group INC

- Senores Pharmaceuticals INC

- Ratnatris Pharmaceuticals Private Limited

- 9488 Jackson Trail LLC (Step-down subsidiary) and

- Zoraya Pharmaceuticals, LLC

As a result, now, Senores Pharmaceuticals Ltd reports both standalone and consolidated financials in its results. However, before FY2022, it used to report only standalone financials.

We believe that while analysing any company, an investor should always look at the company as a whole and focus on financials, which represent the business picture of the entire company, including its subsidiaries, joint ventures etc. Consolidated financials of a company present such a picture. Therefore, if a company reports both standalone as well as consolidated financials, then the investor should prefer the analysis of the consolidated financials of the company.

As a result, while analysing the past financial performance of Senores Pharmaceuticals Ltd, we have analysed its standalone financials for FY2021 and consolidated financials from FY2022 onwards.

Further recommended reading: Standalone vs Consolidated Financials: A Complete Guide

With this background, let us analyse the financial performance of Senores Pharmaceuticals Ltd.

Financial and Business Analysis of Senores Pharmaceuticals Ltd:

Financial performance of Senores Pharmaceuticals Ltd from FY2021 onwards is available in publicly available documents like the red herring prospectus (RHP) and its annual reports.

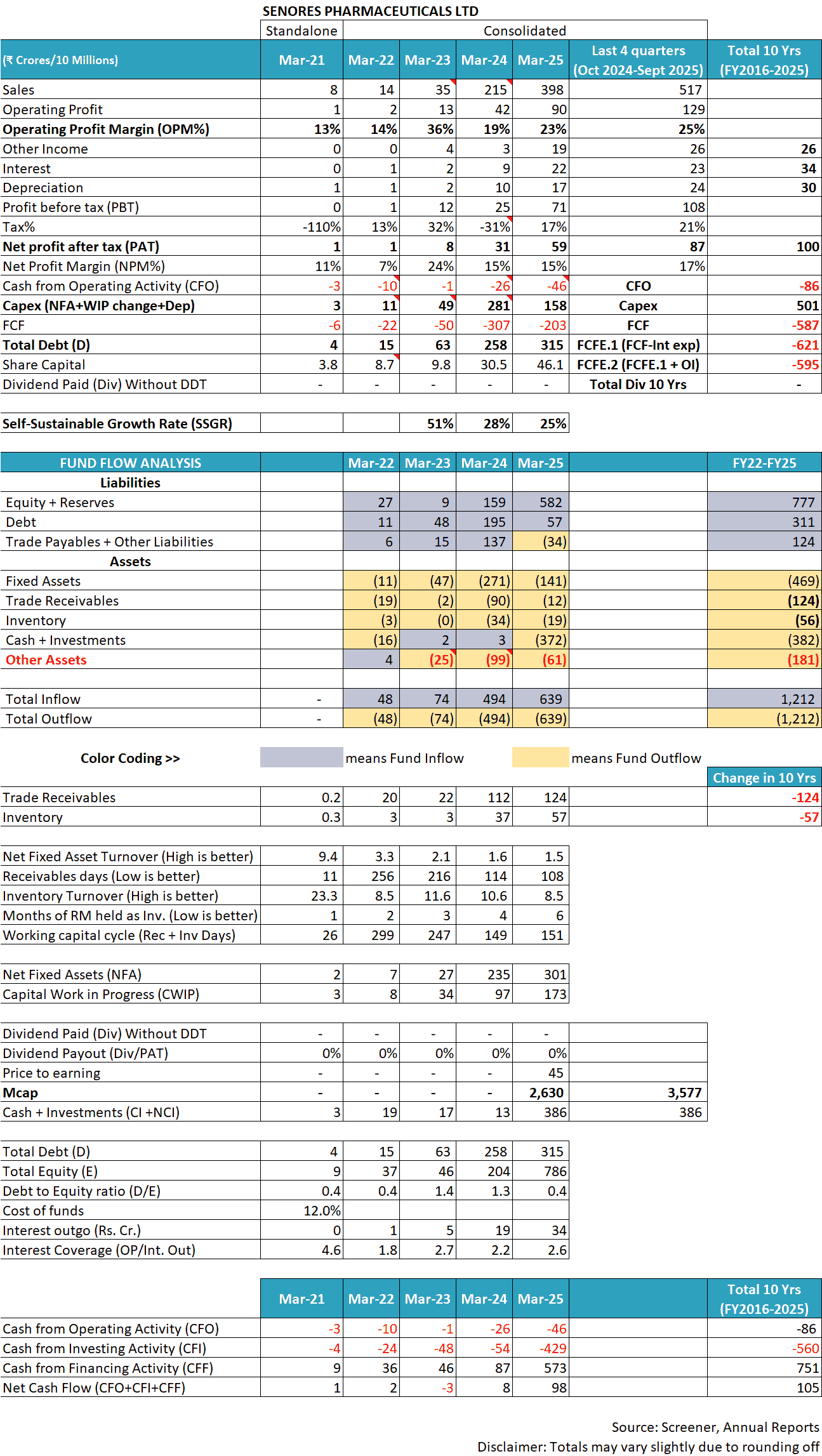

Senores Pharmaceuticals Ltd has grown its sales from ₹8 cr in FY2021 to ₹398 cr in FY2025 at an annualised rate of 166%. Further, in the last 12 months (Oct. 2024-Sept 2025), it increased its sales further to ₹517 cr.

However, its profit margins did not show such consistent growth. Instead, both operating profit margin (OPM) and net profit margin (NPM) have shown large fluctuations.

The OPM was 13% in FY2021 and increased to 36% in FY2023, and thereafter, it declined sharply to 19% in FY2024. Post FY2024, the OPM recovered to 23% in FY2025 and 25% in the last 12 months (Oct. 2024-Sept 2025).

The net profit margin (NPM) of Senores Pharmaceuticals Ltd has also shown similar fluctuations. In FY2021, the NPM was 11%, which declined to 7% in FY2022; then increased to 24% in FY2023 and since then has stabilised at 15% in FY2024 and FY2025. In the last 12 months (Oct. 2024-Sept. 2025), the NPM increased to 17%.

To understand more about Senores Pharmaceuticals Ltd and fluctuations in its profit margins, an investor needs to read the publicly available documents of the company like its annual reports from FY2021 available on company’s website (here), red herring prospectus dated December 24, 2024 for its initial public offer (IPO), as well as corporate announcements submitted by the company to stock exchanges etc.

In addition, an investor should also read the following article explaining the key factors affecting the business of pharmaceutical companies: How to do Business Analysis of Pharmaceutical Companies

The above-mentioned documents show the following key aspects about the business of Senores Pharmaceuticals Ltd, which are critical to understand for any investor.

1) The business of Senores Pharmaceuticals Ltd, generic medicines, faces intense price-based competition:

Generic medicines are like commodity products. Once the required regulatory parameters like purity, dispersion etc. are met and proven to be similar to the patented drug, then all the generic drugs are similar in their effect on the patient. As a result, any specific approved generic drug from one company can easily be replaced by the approved generic drug of another company.

As a result, pharmaceutical players from multiple countries compete in the markets of almost all countries, leading to intense competition.

Red herring prospectus (RHP), December 2024, page 64:

domestic and international pharmaceutical industry is highly competitive with several major pharmaceutical companies present. Our products face intense competition

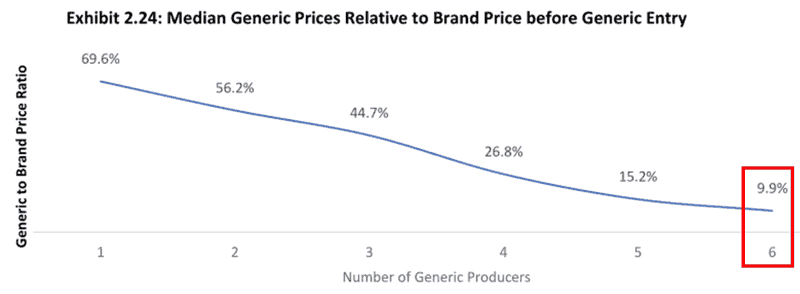

Due to the commoditised nature of generic drugs, manufacturers have to compete on price to gain entry as well as market share. For example, as patents expire, many generic players jump to launch cheaper versions of the drug in regulated markets, and it is seen that as more players enter, the price of the drug falls drastically.

As per the RHP of Senores Pharmaceuticals Ltd, page 186, for drugs in which 6 generic players enter the market, the price of the drug declines to less than 10% of the patented drug.

The intense competition is not limited only to regulated markets. Even in the emerging markets, Senores Pharmaceuticals Ltd has faced strong competition.

When it acquired emerging markets’ business by taking over Ratnatris Pharmaceuticals Private Limited (RPPL), its emerging markets’ business was making losses.

Conference call transcript, May 2025, page 9:

Swapnil Shah: So when we acquired…the company had a PAT negative, it was cash flow negative, EBITDA negative.

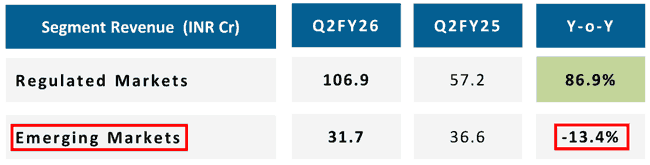

In Q2-FY2026, the emerging markets’ business of the company witnessed a decline.

In India, the company is present in the injectables segment in critical care and supplies directly to hospitals.

Conference call transcript, January 2025, pages 3-4:

Swapnil Shah:…marketing of critical care injectables in India…The focus area is to directly supply to hospitals, cutting down all the mid-level distributors and suppliers.

All hospitals, being large B2B customers, have very high negotiating/pricing power over their suppliers because, at any point in time, multiple pharmaceutical companies chase them to gain their business.

Therefore, an investor should always keep in her mind the intensely competitive nature of the pharmaceutical markets in India as well as abroad before she projects the business of any pharmaceutical company in the future.

Advised Reading: How to analyse New Companies in Unknown Industries?

2) Senores Pharmaceuticals Ltd focuses on drugs that have a smaller market/opportunity size:

Due to intense price-based competition, larger manufacturers who enjoy a lower cost of production due to economies of scale benefit witness huge competitive advantages. In such a situation, smaller players like Senores Pharmaceuticals Ltd are not able to compete.

As a result, Senores Pharmaceuticals Ltd has to select its target drugs very carefully because if big players enter into competition, then it will be priced out.

Therefore, Senores Pharmaceuticals Ltd seems to identify those small-sized drug opportunities, which are too small for large pharmaceutical manufacturers to dedicate their resources.

Conference call transcript, November 2025, page 19:

Swapnil Shah: these are not relatively like $100 million, $200 million, $500 million opportunities where the moment exclusively expires and there are like 10 people jumps in.

Moreover, Senores Pharmaceuticals Ltd does not sell these drugs under its own brand name. As it builds its product portfolio by getting approvals (ANDAs) in such smaller drug opportunities, those larger pharmaceutical players who otherwise would not invest in such drugs on their own are willing to outsource/buy these drugs from Senores Pharmaceuticals Ltd and then launch them under their own name into regulated markets.

Conference call transcript, January 2025, page 16:

Sanjay Majmudar: these are the products we generally large, big pharmas are not interested. But since they want it as a part of their pipeline

The company disclosed to its stakeholders that until now, it has not launched any drug in the regulated markets under its own brand name.

Conference call transcript, May 2025, page 10:

Sanjay Majmudar: just to clarify, we haven’t yet launched our own brands as such in the regulated manner…which are sold by the large distribution or pharma companies in their respective brands.

In this arrangement, Senores Pharmaceuticals Ltd earns its money by three components: first, as it owns the approval (ANDA), therefore, it charges a licensing fee to the customer; second, it manufactures the drug in its US plant, therefore, it earns cost of raw material plus a profit margin on it and third, it negotiates a profit share from the sales done by its customer/large pharma company from sales of these drugs.

Conference call transcript, May 2025, page 10:

Sanjay Majmudar: So our revenue model is licensing, COGS plus margin, and then profit share.

Advised reading: How to do Business Analysis of a Company

3) Senores Pharmaceuticals Ltd’s CDMO division focuses on government contracts, especially controlled substances, which ensure that every approved vendor gets a proportionate allocation:

The company has a contract development & manufacturing business (CDMO/CMO) where it manufactures drugs, especially controlled substances, for its customers who supply to the USA govt.

Conference call transcript, January 2025, page 15:

Sanjay Majmudar: on the CDMO/CMO side, they are not my products, but it’s focused on controlled substances and government

Investors should note that Senores Pharmaceuticals Ltd does not deal with the government directly. Instead, its customers/partners source the drugs from it and supply them to the US government.

Conference call transcript, July 2025, page 8:

Deval Shah: we are not dealing directly with the government again. It is just through our partners that they supply to the government. We don’t supply directly to the government

As per Senores Pharmaceuticals Ltd, the benefit of dealing with the government, especially in controlled substances, is that every approved vendor gets assured proportionate allocation of the order.

Conference call transcript, July 2025, page 6:

Swapnil Shah: So, DEA, that’s a department that US government runs, hands out the quota to each approved player for that particular product. And usually, it is distributed equally among all the approved players that’s out there.

The company has a preference for government contracts because they provide it with stable demand with lower price erosion. Almost 60-70% of the company’s business in the USA comprises government and controlled substances business.

Conference call transcript, July 2025, pages 3 and 8:

Swapnil Shah: our ability to supply to the government channel sets us apart. This access provides us with stable and consistent demand for our products…As a result, we face comparatively lower risk of price erosion

currently, almost 60%-70% business is between government and control substance of overall pie of the business that we have from the US.

Senores Pharmaceuticals Ltd is very enthusiastic about its business of supplying to the USA government, as in its recent acquisitions of multiple ANDAs from the IPO money, it has focused on those ANDAs, which have a high opportunity in the government contracts.

Press release, Q4-FY2025 results, May 2025, page 4:

Swapnil Shah: A large part of this acquired ANDA basket has considerable government contract opportunities.

As a result, currently, a major portion of Senores Pharmaceuticals Ltd’s overall ANDA portfolio is focused on the government contracts.

FY2025 annual report, page 10:

A large part of our ANDA portfolio is tailored for government contracts

Currently, the company is confident that it will not face any challenges due to ongoing trade disruptions by the Trump government because it supplies to the USA government from its US plant, which comes under local manufacturing and is immune to tariffs. However, it imports some of its active pharmaceutical ingredients (APIs) from Europe and China, which may face some risks in the future.

Conference call transcript, July 2025, page 4:

Swapnil Shah: Our entire formulation manufacturing is done locally in the US as we speak. In terms of APIs, we procure very small quantities from China and some quantities from Europe.

Nevertheless, Senores Pharmaceuticals Ltd stated that it is carrying a significant inventory of these imported APIs.

Conference call transcript, May 2025, page 8:

Swapnil Shah: we have only one product coming out of China. And for that particular product, we have about two years of supply already with us on the API side.

Still, an investor needs to keep this aspect of Senores Pharmaceuticals Ltd’s business in mind as the approval of any drug in the USA is tied to the sourcing of API from a specific source. If the company, later, wants to change the source of the API, then it needs to take approval from the US govt., which is expensive and time-consuming.

RHP, December 2024, page 52:

Regulated Markets such as the US, ANDA filings are linked to a specific API manufacturer for each API in a specific ANDA. While our Company can add additional suppliers, such an addition involves incremental cost.

Advised reading: How AI Can Help Investors: Case Study of Call Transcripts

4) The business of Senores Pharmaceuticals Ltd is very capital-intensive, both on fixed capital as well as working capital:

The company seems to be running a very capital-intensive business, which requires continuous significant investment in both its fixed assets as well as working capital for growth.

RHP, December 2024, page 45:

Our business is working capital intensive. If we are unable to borrow to meet our working capital requirements, it may materially and adversely affect our business

In the past, in almost every year of its existence, Senores Pharmaceuticals Ltd has had to raise equity and debt to meet its funding requirements.

RHP, December 2024, page 420:

For the six months ended September 30, 2024, Fiscal 2024, Fiscal 2023 and Fiscal 2022, we met our funding requirements, including satisfaction of debt obligations, capital expenditure, investments, other working capital requirements and other cash outlays, principally with issue of share capital and from external borrowings.

A key indicator of whether a company would need external capital for its operations and growth or would be able to meet it from its internal cash flows is the assessment of its free cash flow.

Over the years, Senores Pharmaceuticals Ltd has not been able to convert its reported profits into cash flow from operations (CFO). During FY2021-FT\Y2025, the company reported a cumulative profit after tax (cPAT) of ₹100 cr; however, during the same period, it reported negative cumulative cash flow from operations (cCFO) of (₹86) cr.

Additionally, the primary source of growth during FY2021-FY2024 was acquisitions of promoter-group companies by Senores Pharmaceuticals Ltd, which required significant investment, along with the acquisition of ANDAs, leading to a total capital expenditure of ₹501 cr over FY2021-FY2025.

As a result, Senores Pharmaceuticals Ltd had to fund its operations (negative CFO) as well as capital expenditure/acquisitions from external funds: equity and debt.

Below is the history of continuous equity dilution by Senores Pharmaceuticals Ltd in the past, year after year:

- FY2020: ₹1.96 cr raised by rights issue. (Source: RHP, page 101)

- FY2021: ₹6.32 cr in three tranches: ₹1 cr as rights issue in June 2020, ₹5.17 cr in rights issue in Nov. 2020 and ₹0.15 cr by preferential issue in March 2021. (Source: RHP, page 101)

- FY2022: ₹26.7 cr in two tranches: ₹6.7 cr by rights issue on Nov. 24, 2021 and ₹20 cr by conversion of compulsory convertible debentures (CCD-I) on Nov. 30, 2021. (Source: RHP, page 101)

- FY2024: ₹57 cr raised in fresh capital in the following tranches: ₹33.5 cr in rights issue and ₹20 cr in conversion of CCD-II in August 2023, and ₹3.5 cr in preferential issue in February 2024. (Source: RHP, pages 101-103)

- In addition, in FY2024, Senores Pharmaceuticals Ltd also issued equity shares for about ₹73 cr to acquire stakes in Havix Group (₹45 cr, May 2023) and Ratnatris Pharmaceuticals Private Limited (RPPL, ₹28 cr, December 2023).

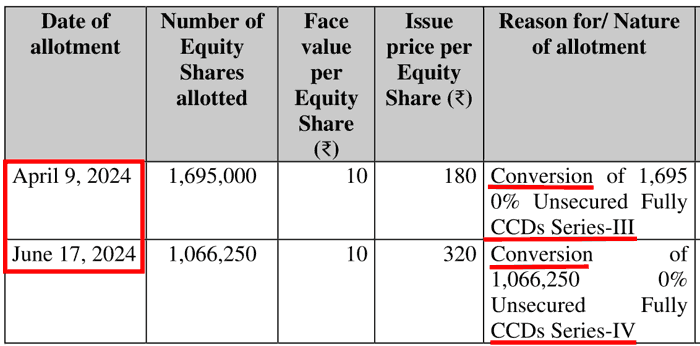

- FY2025: ₹565 cr in three tranches: ₹30.5 cr by conversion of CCD-III in April 2024, ₹34 cr by conversion of CCD-IV in June 2024 and ₹500 cr in initial public offer (IPO) in December 2024. (Source: RHP, page 104)

Therefore, over FY2020-FY2024, Senores Pharmaceuticals Ltd has raised about ₹657 cr via equity dilution via preferential issue, rights issue and CCDs and in addition, issued shares of ₹73 cr for acquiring Havix Group and RPPL.

Additionally, it raised an additional debt of ₹311 cr over FY2021-FY2025 because its total debt increased from ₹4 cr in FY2021 to ₹315 cr in FY2025.

Therefore, overall, the company raised funds of ₹968 cr in equity and debt and issued shares of ₹73 cr in acquisitions.

From FY2021 until FY2025, Senores Pharmaceuticals Ltd has continuously reported negative CFO every year, which is one of the main reasons the company had to rely on outside capital.

Its requirement to raise external money in the IPO was so strong that it paid a very high price for the money in the IPO. Out of the ₹500 cr. raised as fresh issue, Senores Pharmaceuticals Ltd paid more than ₹42 cr (almost 8.5%) as IPO expenses, and it could get only about ₹458 cr for utilisation.

RHP, December 2024, page 124:

In FY2026, the company claims to have started reporting positive CFO as it declared a net cash from operating activities of ₹24.22 cr in H1-FY026 (unaudited, Q2-FY2026 results, page 7). However, it remains to be seen whether the company is able to report a positive CFO for the full year when the audited financial statements are released.

Advised reading: When a company should sell all assets and invest money in FDs?

5) Risks faced by Senores Pharmaceuticals Ltd:

The business of the company faces some critical risks, which must be kept by the investor in her mind during analysis.

5.1) Regulatory risk of compliance of manufacturing plants:

Almost all regulatory authorities in each of the countries undertake regular as well as surprise inspections of pharmaceutical manufacturing plants. If the plants do not meet the required standards, then authorities can suspend the approval/license, and the company is not able to sell drugs from that plant. Failure of plants’ compliance is one of the biggest risks faced by Senores Pharmaceuticals Ltd.

In the past, on multiple occasions, manufacturing plants of the company have faced regulatory sanctions for not meeting quality standards and its license was temporarily suspended.

In one instance related to the production of an anti-diabetic drug, Metformin, Indian drug authorities filed a criminal complaint against its subsidiary, RPPL and one director, Jitendra Babulal Sanghvi, alleging that the company intentionally manufactured the drug with a substandard quality.

RHP, December 2024, page 427:

The Drugs Inspector, Central Drugs Standard Control Organization…has filed a criminal complaint against our Subsidiary, Ratnatris Pharmaceuticals Private Limited…and one of our Directors, Jitendra Babulal Sanghvi…alleged that Ratnatris has intentionally committed the offence of manufacturing a drug, namely, Metformin tablets IP 500 mg, which was declared “not of standard quality”…The case is currently pending

In 2024, during inspections of its subsidiary, RPPL, its license was temporarily suspended three times. In June 2024, the FDA Gujarat suspended its license for 7 days from June 24, 2024, to June 30, 2024

RHP, December 2024, page 38:

Commissioner, FDA Gujarat”) issued a show cause notice…to our Subsidiary, RPPL, which sets out certain critical and major observations…in contravention of the good manufacturing practices criteria …suspended our license…for a period of seven days from June 24, 2024 to June 30, 2024.

Thereafter, again in October 2024, FDA suspended its license for 4 days: 2 days from Oct. 4, 2024, to Oct. 5, 2024 and then for 2 days from Oct. 10, 2024, to Oct. 11, 2024.

RHP, December 2024, pages 38 and 428:

Frusemide Injection…our Subsidiary, RPPL received a letter dated April 26, 2024…stating that the Drug I sample tested was declared ‘Not of Standard Quality”…Our Subsidiary was directed to stop the sale and distribution of the Product and withdraw the stock from the market immediately…FDA passed an order on September 11, 2024 suspending our license for two days from October 4, 2024 to October 5, 2024.

Levocarnitine Injection…our Subsidiary, RPPL received a letter…stating that the Drug II sample tested was declared ‘Not of Standard Quality”…was directed to stop the sale and distribution of the Product and withdraw the stock from the market immediately…FDA passed an order on September 11, 2024, suspending our license for two days from October 10, 2024 to October 11, 2024.

In the past, its US facility in Atlanta has also faced serious observations during inspections by its customers.

RHP, December 2024, page 36:

four of our top 10 customers have conducted audits on our Atlanta Facility of which three customers have issued certain major observations

Recently, in July 2025, the USFDA inspected its Atlanta facility and issued three observations, which were later cleared in November 2025 (Source: corporate announcements to BSE, July 28, 2025 and Nov. 5, 2025).

Going ahead, an investor should keep a track of the status of criminal complaints filed by authorities against it and closely monitor the status of its approvals and inspections by regulatory authorities and customers and check if it has to recall any drugs from the market. In the past, thrice, the company had to recall its drugs from the market.

RHP, December 2024, page 36:

In the past, we have had three instances of products being recalled from markets.

5.2) Commercialisation of acquired ANDAs by Senores Pharmaceuticals Ltd:

Recently, the company has acquired multiple ANDAs from other pharmaceutical companies like Dr Reddy’s, Wockhardt, Teva etc., from the IPO money.

One of the major risks in such acquisitions is whether the company can successfully commercialise these drugs in the market, and after commercialisation, can it earn sufficient money to justify the price paid by it in acquiring these ANDAs.

This is because, if it has paid an excessive price, then even after successful commercialisation, Senores Pharmaceuticals Ltd may not make any profit if it has paid a very high price for acquiring the ANDAs.

Going ahead, an investor should keep a close watch on the profit margins of the company and whether it is able to convert its profits into cash and if it can meet its funding requirements from its internally generated cash, or it continues to rely on equity dilution and debt to finance its cash flow shortfalls.

Also read: How to do Financial Analysis of a Company

Operating Efficiency Analysis of Senores Pharmaceuticals Ltd:

a) Net fixed asset turnover (NFAT) of Senores Pharmaceuticals Ltd:

Over the years, NFAT of the company has declined from 3.3 in FY2022 to 1.5 in FY2025. A decline in the NFAT reflects that the efficiency of the company in utilising its fixed assets is going down year on year.

One of the reasons for this decline in NFAT can be that the assets acquired by Senores Pharmaceuticals Ltd, in FY2024, by acquiring promoter-group companies like Havix group, RPPL, Mascot Industries etc. were not very efficient, which has led to a decline in the NFAT of the consolidated entity.

Secondly, in February 2025, Senores Pharmaceuticals Ltd completed its greenfield API plant in Gujarat, which is yet to reach optimal utilisation levels and, as a result, lowers the NFAT of the company for FY2025.

Media release, February 26, 2025, page 1:

today inaugurated and commenced manufacturing activities at its greenfield Active Pharmaceutical Ingredient (‘API’) plant…Gujarat…with an installed capacity of ~100 Metric Tons per Annum

Additionally, the company has also started construction of the 3rd manufacturing line at its Atlanta plant in the US.

Conference call transcript, May 2025, page 9:

Swapnil Shah: We are increasing our oral solids capacities…we already got two installed lines. We are getting third line installed as we speak and fourth line is being planned

Going ahead, an investor should keep a close watch on the timely completion of the expansion of the US plant and commercialisation of India API, as well as the US oral solid capacity. She should closely monitor the NFAT of Senores Pharmaceuticals Ltd to assess whether it is able to utilise its plants efficiently.

Further advised reading: Asset Turnover Ratio: A Complete Guide for Investors

b) Inventory turnover ratio (ITR) of Senores Pharmaceuticals Ltd:

Over the years, the inventory turnover ratio (ITR) of the company has stayed stable at 8.5 in FY2022 as well as FY2025. In the interim period, the ITR had improved to 11.6 in FY2022; however, now, it has fallen back to the levels of 8.5.

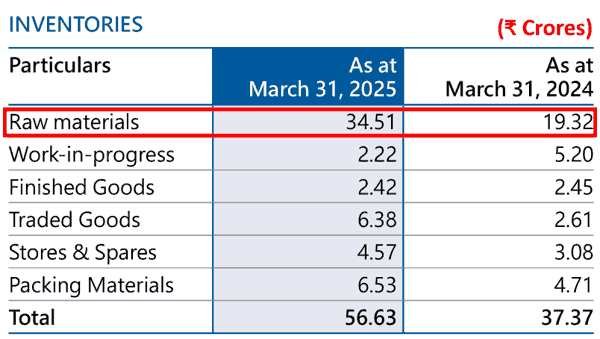

One of the reasons for the decline in inventory turnover in FY2025 is due to a sharp increase in raw materials in FY2025.

FY2025 annual report, page 207:

One of the reasons for such a sharp increase in raw materials seems to be the accumulation of API by the company in the USA, fearing trade restrictions on imports from China. As per Senores Pharmaceuticals Ltd, as of March 31, 2025, it had about 2 years’ worth of Chinese API requirements in store.

Conference call transcript, May 2025, page 8:

Swapnil Shah: we have only one product coming out of China. And for that particular product, we have about two years of supply already with us on the API side.

Going ahead, an investor should keep a close watch on the inventory levels of Senores Pharmaceuticals Ltd to assess whether it is able to utilise its inventory efficiently.

Further advised reading: Inventory Turnover Ratio: A Complete Guide

c) Analysis of receivables days of Senores Pharmaceuticals Ltd:

Over the years, Senores Pharmaceuticals Ltd has seen receivables days improve from 256 days in FY2022 to 108 days in FY2025.

In FY2022, the company had very high receivables because it had to give long credit periods to its customers to generate sales.

RHP, December 2024, page 37:

The net negative cash flows from operating activities in Fiscal 2022 was ₹ (104.47) million on account of incremental working capital requirement due to extended credit terms to the customers

In FY2024, when Senores Pharmaceuticals Ltd acquired control of Havix Group and RPPL, its receivables position deteriorated as trade receivables increased from ₹22 cr in FY2023 to ₹112 cr in FY2024.

RHP, December 2024, page 37:

The net negative cash flow from operating activities in Fiscal 2024 was ₹ (198.71) million on account of additional working capital requirements for the newly acquired subsidiaries, i.e., Havix and RPPL during Fiscal 2024.

The position of receivables was poor as at the end of FY2024, Senores Pharmaceuticals Ltd had receivables pending for more than 3 years post their due date for payment.

FY2024 annual report, page 217:

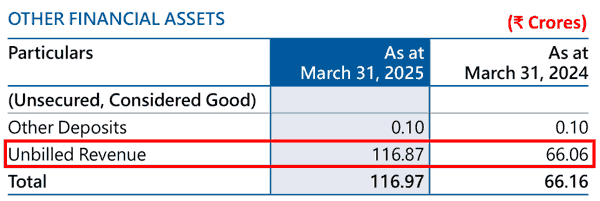

It is not only trade receivables, which are due from customers after Senores Pharmaceuticals Ltd has raised bills on its customers, and they have accepted them for payment. In the financial statements, Senores Pharmaceuticals Ltd has declared a large amount of unbilled revenue, which indicates the work done/drugs manufactured by the company, which are yet to be sent/billed to the customer; however, the company has already included these in its sales and declared them as revenue and profits in its financial statements.

For example, in FY2025, unbilled receivables of Senores Pharmaceuticals Ltd increased from ₹66 cr in FY2024 to ₹116 cr in FY2025, i.e. in FY2025, sales reported by the company included ₹50 cr for which the bills are yet to be raised and yet to be accepted by the customer.

FY2025 annual report, page 209:

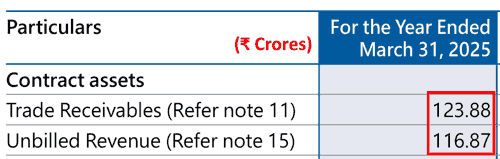

If an investor adds the unbilled revenue declared by Senores Pharmaceuticals Ltd into its trade receivables, then its working capital position turns out to be even more stretched.

For example, on March 31, 2025, out of its sales, the company had a total of about ₹240 cr outstanding for collection as contract assets (trade receivables + unbilled revenue).

FY2025 annual report, page 219:

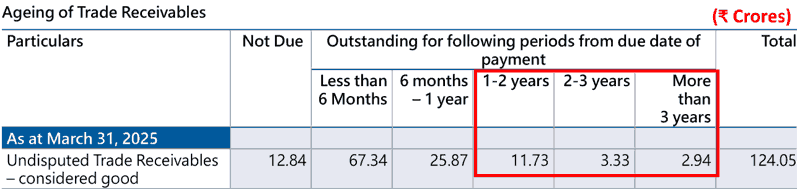

No wonder the company has a large amount of receivables outstanding for a very long time after their payment due dates. For example, in FY2025, the company had about ₹17 cr of receivables overdue for more than 1 year from their due date for payment including receivables of about ₹3 cr that we outstanding for more than 3 years from their due date.

FY2025 annual report, page 207:

Going ahead, an investor should monitor closely whether Senores Pharmaceuticals Ltd is able to collect its receivables and unbilled revenue on time.

Further recommended reading: Receivable Days: A Complete Guide

As discussed earlier, when an investor compares the cumulative net profit after tax (cPAT) and cumulative cash flow from operations (cCFO) of Senores Pharmaceuticals Ltd for FY2021-FY2025, then she notices that over the years (FY2021-FY2025), the company is not able to convert its profit into cash flow from operations.

Over FY2021-25, Senores Pharmaceuticals Ltd reported a total cumulative profit after tax (cPAT) of ₹100 cr. During the same period, it reported a cumulative negative cash flow from operations (cCFO) of (₹86) cr.

It is advised that investors should read the article on CFO calculation, which would help them understand the situations in which companies tend to have the CFO lower than their PAT. In addition, the investors would also understand the situations when the companies would have their CFO higher than PAT.

Further recommended reading: Understanding Cash Flow from Operations (CFO)

The Margin of Safety in the Business of Senores Pharmaceuticals Ltd:

a) Self-Sustainable Growth Rate (SSGR):

Read: Self Sustainable Growth Rate: a measure of Inherent Growth Potential of a Company

Upon reading the SSGR article, an investor would appreciate that if a company is growing at a rate equal to or less than the SSGR and it can convert its profits into cash flow from operations, then it would be able to fund its growth from its internal resources without the need for external sources of funds.

Conversely, if any company attempts to grow its sales at a rate higher than its SSGR, then its internal resources would not be sufficient to fund its growth aspirations. As a result, the company would have to rely on additional sources of funds, like debt or equity dilution, to meet the cash requirements to generate its target growth.

An investor may calculate the SSGR using the following formula:

SSGR = NFAT * NPM * (1-DPR) – Dep

Where,

- SSGR = Self Sustainable Growth Rate in %

- Dep = Depreciation rate as a % of net fixed assets

- NFAT = Net fixed asset turnover (Sales/average net fixed assets over the year)

- NPM = Net profit margin as % of sales

- DPR = Dividend paid as % of net profit after tax

(For systematic algebraic calculation of SSGR formula: Click Here)

Over the years, Senores Pharmaceuticals Ltd has had an SSGR of about 25%, whereas it has grown its sales at a much higher rate of 116% year on year. As a result, the company had to consistently rely on outside capital of equity infusion and raising more debt to sustain its operations as well as fund its acquisitions of subsidiaries, ANDAs, as well as construct plants.

As a result, as per earlier discussion, over FY2020-FY2025, Senores Pharmaceuticals Ltd had to infuse more than ₹1,000 cr by way of equity dilution and incremental debt. It included ₹657 cr as equity raise via preferential issue, rights issue and CCDs, ₹311 cr as incremental debt and ₹73 cr of shares issued to acquire Havix Group and RPPL.

An investor arrives at the same conclusion when she does the free cash flow (FCF) analysis of the company.

b) Free Cash Flow (FCF) Analysis of Senores Pharmaceuticals Ltd:

While looking at the cash flow performance of Senores Pharmaceuticals Ltd, an investor notices that during FY2021-FY2025, it generated a negative cash flow from operations of (₹86) cr. During the same period, it made a capital expenditure of about ₹501 cr.

Therefore, during this period (FY2021-FY2025), Senores Pharmaceuticals Ltd had a negative free cash flow (FCF) of (₹587) cr (= -86 – 501).

In addition, during this period, the company had a non-operating income of ₹26 cr and an interest expense of ₹34 cr. As a result, the company had a total negative free cash flow of (₹595) cr (= -587 + 26 – 34). Please note that the capitalised interest is already factored in as part of the capex deducted earlier.

As discussed earlier, Senores Pharmaceuticals Ltd funded this cash flow gap by raising equity and incremental debt.

Going ahead, an investor should keep a close watch on the cash flow position of Senores Pharmaceuticals Ltd to understand whether the company is able to generate surplus cash from its business, or it relies on outside funds for growth and running its day-to-day operations.

Further recommended reading: Free Cash Flow: A Complete Guide to Understanding FCF

Self-Sustainable Growth Rate (SSGR) and free cash flow (FCF) are the main pillars of assessing the margin of safety in the business model of any company.

Further advised reading: 3 Simple Ways to Assess “Margin of Safety”: The Cornerstone of Stock Investing

Additional aspects of Senores Pharmaceuticals Ltd:

On analysing Senores Pharmaceuticals Ltd and after reading annual reports, credit rating reports and other public documents, an investor comes across certain other aspects of the company, which are important for any investor to know while making an investment decision.

1) Management Succession of Senores Pharmaceuticals Ltd:

The company is promoted by Mr Swapnil Shah, managing director (age 40 years) and Mr Ashokkumar Barot, Non-executive director (age 59 years). Currently, multiple other people from the promoter group are present as non-independent directors on the board: Mr Sanjay Majumdar (chairman, age 62 years), Mr Hemanshu Pandya (age 54 years), Mr Jitendra Sanghvi (age 46 years) and Mr Arpit Shah (age 38 years).

Two children of Mr Swapnil Shah, son, Mr Vihaan Shah and daughter, Ms Suhana Shah, were disclosed as minors in the RHP (page 276). In addition, the RHP disclosed details of two children of Mr Ashokkumar Barot, son, Mr Dhananjay Barot and daughter, Ms Viraj Barot.

However, currently, as per the FY2025 annual report, none of these seem to be employed by Senores Pharmaceuticals Ltd.

Even though currently, the key promoters themselves are young; however, an investor may contact the company directly to understand whether any members of the next generation of promoters plan to join the company in an executive capacity. This would provide her with a clear idea of the succession planning of the promoters of the company.

Advised reading: How to do Management Analysis of Companies?

2) Senores Pharmaceuticals Ltd’s purchases of promoter group companies:

An analysis of corporate actions of the company indicates that promoters of the company have started multiple entities in India and abroad, focused on the pharmaceutical business. It was not like one holding company controlling all the entities and then publicly listing the holding company.

In fact, promoters kept each entity separately engaged in the pharmaceutical business and made these entities buy and sell among each other, while the rest of them continued to engage in similar/competing pharmaceutical business.

As of now, the key promoter of Senores Pharmaceuticals Ltd, Mr Swapnil Shah, has another company, Remus Pharmaceuticals Ltd, listed on the NSE-SME exchange, where he and his wife, Ms Anar Swapnil Shah, are directors and own a 33.94% stake on September 30, 2025 (click here).

When promoters have multiple entities in the same business, then apart from diverting their focus and attention from the publicly-listed entity, there is also a possibility of conflict of interest, where at times, promoters may keep their personal interest over the interests of the publicly-listed entity and its minority shareholders.

RHP, December 2024, pages 40-41:

some of our Directors and Promoters are interested in certain Group Companies, Subsidiaries, and Promoter Group, that are engaged in the same business as ours…We cannot assure you that our Directors and our Promoter Group, our Subsidiaries and our Group Companies will not provide competitive services or otherwise compete in business

Over the years, promoters have made Senores Pharmaceuticals Ltd purchase their other group entities.

2.1) Havix Group, Inc.

For example, the main business generating unit of the company, Havix Group, which owns the plant in Atlanta, USA, was a separate entity owned by promoters, and over the years, its shareholders have been selling their stake in Havix to Senores Pharmaceuticals Ltd at increasingly higher prices.

For example, as per an agreement dated December 21, 2022, with promoters, Mr Ashokkumar Barot, his son, Mr Dhananjay Barot, and promoter-group entity, Renosen Pharmaceuticals Private Limited, Senores Pharmaceuticals Ltd acquired shares of Havix Group. Subsequently, in another agreement dated April 14, 2023, Senores Pharmaceuticals Ltd acquired shares of Havix Group from promoter-group entities, Renosen Pharmaceuticals Private Limited, Aviraj Group LLC, and Aviraj Overseas LLC. (Source: RHP, December 2024, page 244)

As per the RHP, page 245, these shares were acquired from promoters at a price of USD 53 per share of Havix Group, and its aggregate shareholding increased to 66.57% (RHP, page 298).

The value of the equity shares of Havix was considered USD 53.00 per equity share

After the IPO, in March 2025, Senores Pharmaceuticals Ltd acquired more shares of Havix Group, at USD 160 per share (Corporate announcement to BSE, March 11, 2025, page 2).

Thereafter, in July 2025, the company acquired more shares of Havix Group at USD 181 per share (Corporate announcement to BSE, July 10, 2025, page 2).

An investor should note that if the corporate structure of any group is not simple and clear, like in the case of Senores Pharmaceuticals Ltd, where almost all the major business-generating entities of the company are only partly owned by it.

For example, in the case of Havix Group, which is the single biggest revenue generating entity for the company, after all these transactions, Senores Pharmaceuticals Ltd owns only 73.04% of it and there are still about 27% shares owned by others who might want to sell their stake to the company in future at prices that may not always be in the best interests of the public sharesholders of Senores Pharmaceuticals Ltd.

Advised reading: Why Management Assessment is the Most Critical Factor in Stock Investing?

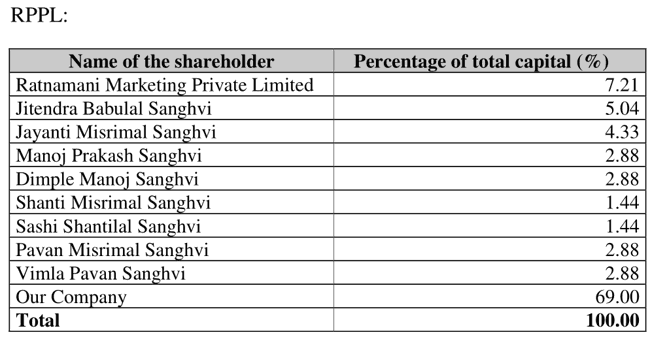

2.2) Ratnatris Pharmaceuticals Private Limited (RPPL):

Senores Pharmaceuticals Ltd acquired a 69% stake in RPPL in Nov.-Dec. 2023 for about ₹29 cr by issuing shares to promoters-group entities and related parties, Remus Pharmaceuticals Limited, Ratnamani Marketing Private Limited and Jitendra Babulal Sanghvi.

Senores Pharmaceuticals Ltd got access to the emerging markets business by acquiring RPPL.

RHP, December 2024, page 212:

RPPL, our Subsidiary, through which we undertake our Emerging Markets Business became our subsidiary with effect from December 14, 2023. Accordingly, we do not have any revenue from operations from the Emerging Markets Business for Fiscal 2023 and Fiscal 2022.

When Senores Pharmaceuticals Ltd acquired the emerging market business of RPPL, its manufacturing plant was old and its business was in a very poor shape with making continuous losses.

Conference call transcript, November 2025, page 16:

Swapnil Shah: Ratnatris, it’s about a 14-year, 15-year- old plant. When we acquired it…with EBITDA and cash loss.

Ever since the acquisition, Senores Pharmaceuticals Ltd has been continuously working on reviving it by changing the product mix or the target markets.

Conference call transcript, January 2025, pages 8 and 13:

Swapnil Shah: Emerging market there is a lot of activity that we have done in last two years in terms of changing the product mix. And earlier, last part of our focus was on the African markets. So, we are changing the product mix as well as market mix.

Sanjay Majmudar: When we acquired the whole business model has been changed.

So, it seems that before IPO, the majority shareholders, including the promoters’ other listed company, Remus Pharmaceutical Ltd, sold its stake in the poorly performing emerging markets business to Senores Pharmaceuticals Ltd. Now, the company is working hard to revive the emerging markets business.

Until now, the company has been facing significant challenges in this business. In Q2-FY2026, the emerging markets business witnessed a decline in sales.

Conference call transcript, November 2025, page 6:

Swapnil Shah: So, in the emerging market…although we have got registration approvals, those approvals have not converted yet into commercial orders, because there are import permits need to be taken, and so on

Once the emerging markets business is revived, then the remaining shareholders, who seem related parties, might sell the balance 31% to Senores Pharmaceuticals Ltd at higher prices, which might not be very beneficial for public shareholders of Senores Pharmaceuticals Ltd.

As per the RHP, page 68, most of the shareholders of RPPL are Sanghvis, including the director of Senores Pharmaceuticals Ltd, Jitendra Sanghvi.

RHP, December 2024, page 68:

Similarly, in the past, Senores Pharmaceuticals Ltd acquired other promoter-group entities like Ratnagene Lifesciences Private Limited (RLPL) and M/s Mascot Industries. Later on, these entities were merged with Senores Pharmaceuticals Ltd. (FY2024 annual report, pages 21 and 162).

When Senores Pharmaceuticals Ltd purchased a 57.67% stake in RLPL for ₹3.46 cr, then RLPL had zero/nil sales (FY2022 annual report, pages 10 and 14).

It is advised that investors should do a deeper due diligence of the transactions where Senores Pharmaceuticals Ltd purchases a stake in promoter-group entities.

Advised reading: How to Identify if Management is Misallocating Capital

2.3) Zoraya Pharmaceuticals LLC:

In November 2025, Senores Pharmaceuticals Ltd created a new entity, Zoraya Pharmaceuticals LLC (ZPL) in the USA for the commercial launch of some of the newly acquired ANDAs.

However, here also, the company has brought in other parties into the picture, as it owns only a 51% stake in ZPL, and other parties own 49%.

From the earlier discussion, an investor would remember the disclosure by the company that most of the newly acquired ANDAs are focused on the government contracts, and Senores Pharmaceuticals Ltd already claims to have a good expertise in handling government business and claims it to be one of its strongest competitive advantages.

However, still, while commercially launching the newly acquired ANDAs, it is making other entities almost equal partners (49%).

Promoters of Senores Pharmaceuticals Ltd did not disclose the names of entities that own 49% in ZPL; instead, they just said that these are entities with marketing experience.

Conference call transcript, November 2025, page 9:

Swapnil Shah: acquired 51% interest in Zoraya Pharmaceuticals LLC, based in the US…So, some of our products that we have acquired, the ANDAs, will be launched under the Zoraya platform…remaining 49% of Zoraya is somebody who already has marketing experience

An investor may contact the company directly to understand who the entities are that own a 49% stake in ZPL, and once their identity is known, then form her own opinion about what value they are capable of bringing for public shareholders of Senores Pharmaceuticals Ltd.

Advised reading: How to know if Promoters are Losing Commitment to the Company

3) Related party transactions of Senores Pharmaceuticals Ltd with promoter-group entities:

Promoters of Senores Pharmaceuticals Ltd have kept their business tightly integrated with their other group entities with numerous regular transactions of sales and purchase of goods/services, fixed assets, lending transactions etc. (Source: FY2025 annual report, pages 230-231)

Senores Pharmaceuticals Ltd has appointed promoter group entity, Remus Pharmaceutical Ltd, as one of its distributors. The company sells goods to Remus, which in turn sells it further to other customers.

FY2025 annual report, page 231:

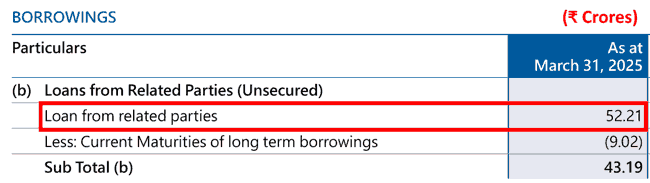

In FY2025, Senores Pharmaceuticals Ltd has taken loans of more than ₹50 cr from related parties.

FY2025 annual report, page 212:

An investor may note that each of the sale/purchase/rent/loan/professional fees transactions provides an opportunity for shifting of economic benefit from public shareholders to promoters if the listed company buys goods/services from promoter entities at a price higher than their market price or sells goods/services to promoter entities at a price lower than their market price. Therefore, an investor should always do deeper due diligence of such sale/purchase transactions with related parties.

Advised reading: How Promoters benefit from Related Party Transactions

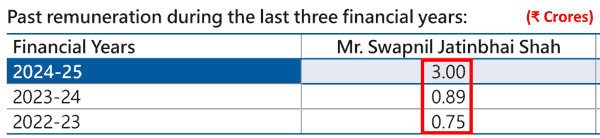

4) Sharp increase in remuneration of promoter, Mr Swapnil Shah:

From the IPO year, FY2025, the remuneration of the promoter of Senores Pharmaceuticals Ltd, Mr Swapnil Shah, has increased significantly from ₹0.89 cr in FY2024 to ₹3 cr in FY2025.

FY2025 annual report, page 61:

On the contrary, in FY2024, employees other than managerial personnel at Senores Pharmaceuticals Ltd saw their salaries decline by 22.87%.

FY2024 annual report, pages 30-31:

The average decrease in salaries of employees other than managerial personnel in financial year 2023-2024 was 22.87%.

Moreover, now, the promoter has increased his remuneration further from ₹3 cr per annum in FY2025 to ₹7.5 cr per annum plus other perquisites (FY2025 annual report, page 54).

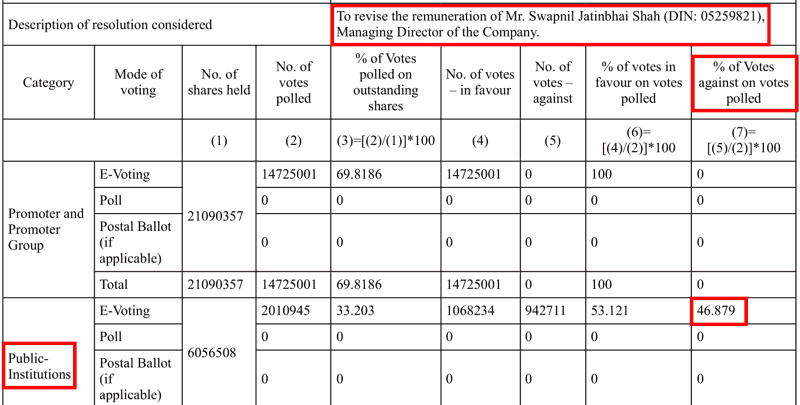

In the AGM in September 2025, a large number of public institutions voted against the remuneration hike of Mr Swapnil Shah; however, the resolution was passed.

Corporate announcement to BSE, September 2025, page 19:

An investor may also note that the IPO of Senores Pharmaceuticals Ltd also included a portion of the offer for sale in which the promoters of the company sold shares of about ₹42 cr. (Source: RHP, December 2024, page 84)

- Mr Swapnil Jatinbhai Shah (Promoter): ₹9.5 cr (250,000 shares * ₹381/-)

- Mr Ashokkumar Vijaysinh Barot (Promoter): ₹21 cr (550,000 shares * ₹381/-)

- Ms Sangeeta Mukur Barot (Promoter): ₹11.4 cr (300,000 shares * ₹381/- cr)

As per the RHP, page 102, about an year back from the IPO, in August 2023, Senores Pharmaceuticals Ltd had allotted 921,281 shares to Mr Swapnil Shah, 802,280 shares to Mr Ashokkumar Barot, and 405,455 shares to Ms Sangeeta Mukur Barot among others at ₹63/- per share i.e. in the IPO, the promters could earn a profit of more than 500% within one year of allotment of shares.

Advised reading: How to identify Promoters extracting Money via High Salaries

5) Research & development (R&D) at Senores Pharmaceuticals Ltd:

Currently, the focus of the company seems to be buying out ANDAs/drug approvals from the market to grow its business, as it has dedicated more than ₹150 cr out of the IPO money for such acquisitions.

RHP, December 2024, page 140:

The amount of Net Proceeds proposed to be deployed for funding inorganic growth through potential acquisitions and strategic initiatives includes utilization of up to ₹ 1,543.68 million.

Post IPO, Senores Pharmaceuticals Ltd has acquired multiple ANDAs from Dr Reddy’s, Wockhardt, Teva etc. and has formed a new entity, Zoraya Pharmaceuticals LLC, to commercially launch drugs under these ANDAs.

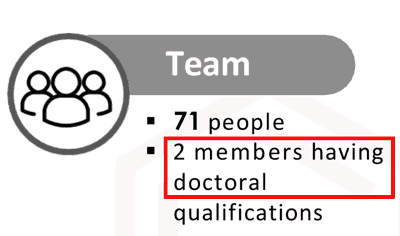

When an investor looks at the in-house R&D team of the company, then she notices that, on September 30, 2025, it had an R&D team of 71 people; however, only 2 out of these 71 members have doctoral qualifications, i.e. PhDs.

Q2-FY2026 presentation, November 2025, page 27:

Please note that if only two members of the R&D team are PhDs, then it indicates that the rest of the members are most likely B. Pharm/M. Pharm/B.Sc/M.Sc/Diploma/technician-level staff.

If the entire R&D team has only 2 PhDs, then it is unlikely that the team would have many senior scientists with deep specialisation (medicinal chemistry, advanced formulation design, process chemistry for complex injectables, regulatory science, analytical method development etc.).

It might be that most of the team might be technicians, formulators, junior scientists, or regulatory staff, which is sufficient for basic formulation development, documentation, and regulatory filing support.

The focus of Senores Pharmaceuticals Ltd in growing its business by acquiring ANDAs from other companies, in itself, might indicate that the company recognises the limitations of its in-house R&D team.

In the past, Senores Pharmaceuticals Ltd has included the money spent on acquiring ANDAs, shown in the fixed assets schedule as “Intangible Assets – Product Development” and “Intangible Assets under Development – Product Under Development”, as its R&D spending.

RHP, December 2024, page 47:

R&D Investments are additions in intangibles developed and under development, related to product development.

It is advised that an investor may directly seek any clarifications about the R&D team from the company and then form her own opinion about it.

6) Weakness in internal controls & processes at Senores Pharmaceuticals Ltd:

Over the years, an investor comes across multiple instances that indicate a scope of improvement in the internal controls & processes of the company.

For example, in the FY2025 annual report, the audit report of the company mentioned that, during the years, Senores Pharmaceuticals Ltd did not make any preferential allotment of shares on conversion of compulsory convertible debentures (CCDs).

FY2025 annual report, page 122:

Company has not made preferential allotment of shares on account of conversion of Compulsorily Convertible Debenture (CCD) during the year. Accordingly, clause 3(x)(b) of the Order is not applicable.

Whereas, in reality, during FY2025, Senores Pharmaceuticals Ltd twice allotted shares on conversion of CCDs (CCD-III and CCD-IV); first on April 9, 2024, on conversion of CCD-III and on June 17, 2024, on conversion of CCD-IV.

RHP, December 2024, page 104:

It seems that neither the auditor nor the management nor anyone at the company double-checked whether the annual report had the correct disclosure regarding the conversion of CCDs or not.

In FY2025, Senores Pharmaceuticals Ltd did not complete its responsibilities regarding foreign exchange management rules by the RBI, and as a result, ICICI Bank had to notify the RBI and issue a caution letter to the company.

RHP, December 2024, page 427:

On April 5, 2024,…ICICI Bank…issued a caution letter to us regarding an outlay breach of foreign exchange of four months and delayed completion of our merchanting trade transaction (“MTT”) contrary to the RBI A.P. (DIR Series) Circular No. 115 dated March 28, 2014.

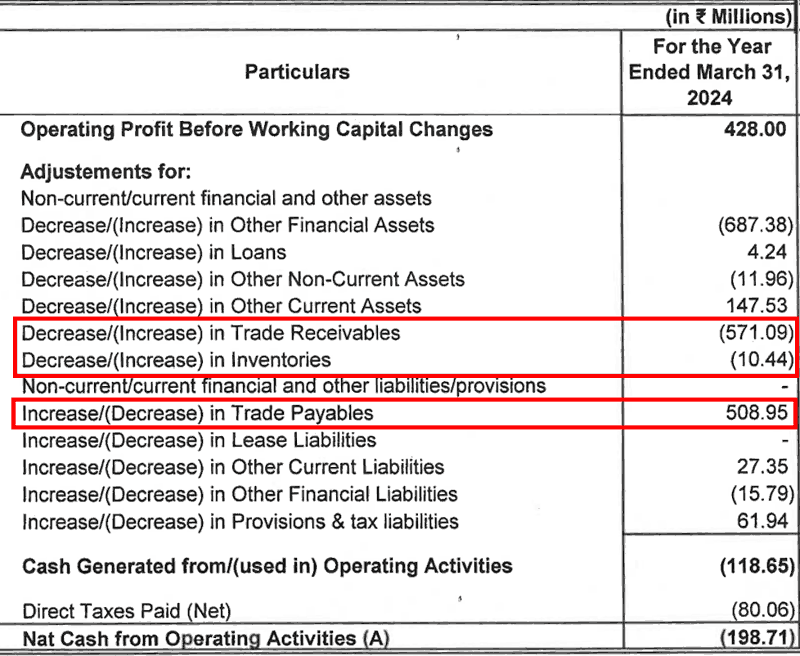

In the FY2024 annual report, the data on changes in trade receivables, inventory and trade payables included in the calculation of cash flow from operating activities does not match the data disclosed in the balance sheet. There are significant differences between the two.

For example, in the cash flow statement, under the calculation of cash flow from operating activities, Senores Pharmaceuticals Ltd has shown an increase in trade receivables of ₹571.09 million, an increase in inventories of ₹10.44 million and an increase in trade payables of ₹508.95 million.

FY2024 annual report, page 180:

Whereas, when the investor analyses the balance sheet of the company for FY2024 and FY2023, then she notices that in FY2024:

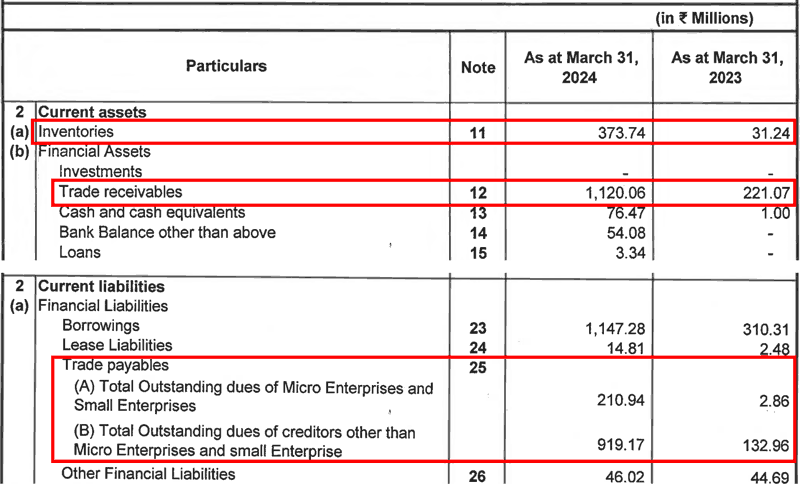

- Trade receivables have increased by ₹898.99 million (from ₹221.07 million in FY2023 to ₹1,120.06 million in FY2024), instead of the increase of ₹571.09 million shown in the cash flow statement.

- Inventories have increased by ₹342.5 million (from ₹31.24 million in FY2023 to ₹373.74 million in FY2024), instead of the increase of ₹10.44 million shown in the cash flow statement.

- Trade payables have increased by ₹994.29 million (from ₹135.82 (=2.86 + 132.96) million in FY2023 to ₹1,130.11 (=210.94+919.17) million in FY2024), instead of the increase of ₹508.95 million shown in the cash flow statement.

FY2024 annual report, pages 176-177:

Advised reading: How to study Annual Report of a Company

An investor may contact the company directly to understand the reasons for such a large difference in the financial data in the balance sheet and the cash flow statement.

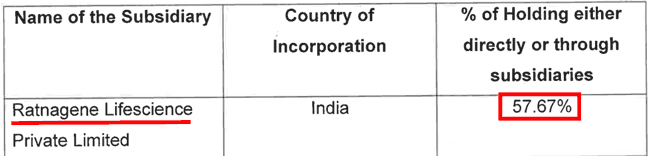

On other occasions, Senores Pharmaceuticals Ltd seems to have made an error in the annual reports while disclosing its shareholding in Ratnagene Lifescience Private Limited. In the FY2023 annual report, it disclosed that during the year, it increased its shareholding from 57.77% in FY2022 to 80.17% in FY2023.

FY2023 annual report, page 16:

However, in the FY2022 annual report, the company disclosed that its shareholding in Ratnagene Lifescience Private Limited was not 57.77%, but 57.67%.

FY2022 annual report, page 85:

An investor may contact the company directly to understand whether it is a typographical error or if one of the two data points in the annual reports is wrong.

Looking at such instances of data discrepancy, an investor should be very cautious while analysing the public disclosures of Senores Pharmaceuticals Ltd and always cross-check the numbers from multiple sources before making a final opinion.

An investor should note that in companies where internal controls and processes are weak, there is a high probability of coming across fraud conducted by employees or other stakeholders like suppliers, customers etc.

An investor may read an example in the case of National Peroxide Ltd, a Wadia Group company, where the managing director of the company attempted to take advantage of the weaknesses in the internal processes and controls and committed fraud on the company: Analysis: National Peroxide Ltd

Therefore, wherever during her analysis, an investor comes across companies showing signs of weakness in controls and processes, then she should increase the depth of her due diligence.

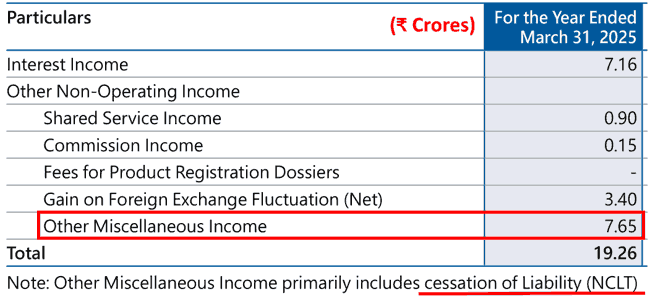

In addition, at multiple places, Senores Pharmaceuticals Ltd has disclosed some financial data in the annual reports without any meaningful explanation, which can help investors to properly understand the transaction.

For example, in the FY2025 annual report, the company has disclosed an income of ₹7.65 cr as cessation of liability (NCLT). It might indicate that Senores Pharmaceuticals Ltd was facing a dispute where some counterparty had filed a case in NCLT for recovery of money, and now, NCLT might have decided against the payment. As a result, Senores Pharmaceuticals Ltd might have included the sum of ₹7.65 as “other income”. However, no such explanation or details about any dispute in the annual report.

FY2025 annual report, page 219:

Similarly, in the FY2025 annual report, on page 222, Senores Pharmaceuticals Ltd has disclosed a disputed income tax demand of ₹20.55 cr as a contingent liability. However, the company has not shared any further details, like which year this demand pertains to, if the company has appealed against it, then at what level the appeal is pending. There are no details about what the outcome was at lower appellant levels, whether the decision was against the company, and it was further appealed at higher levels, or the decision was in favour of the company, and the income tax department appealed at higher levels.

An investor may contact the company directly for clarification in these matters.

The Margin of Safety in the market price of Senores Pharmaceuticals Ltd:

Currently (December 8, 2025), Senores Pharmaceuticals Ltd is available at a price-to-earnings (PE) ratio of about 41 based on earnings of the last 12 months (October 2024- September 2025).

We recommend that an investor read the following articles to assess the P/E ratio to be paid for any stock, which considers the strength of the business model of the company as well. The strength in the business model of any company is measured by way of its self-sustainable growth rate and the free cash flow generating the ability of the company.

In the absence of any strength in the business model of the company, even a low PE ratio of the company’s stock may be a sign of a value trap, where, instead of being a bargain, the low valuation of the stock price may represent the poor business dynamics of the company.

- 4 Principles to Decide the Ideal P/E Ratio of a Stock for Value Investors

- How to Earn High Returns at Low Risk – Invest in Low P/E Stocks

- Hidden Risk of Investing in High P/E Stocks

Analysis Summary

Senores Pharmaceuticals Ltd has delivered very strong sales growth from FY2021 to FY2025; however, most of this growth is achieved by acquisitions of promoter-group companies using significant external funding instead of internally generated cash flows.

The company operates in a highly competitive generic pharma industry and has very low pricing power over its customers. As a result, its profit margins have witnessed large fluctuations. As a result, Senores Pharmaceuticals Ltd focuses on small-sized drug opportunities, in which larger competitors are not interested.

The company’s business model relies primarily on licensing, manufacturing margins and profit-sharing with large partners/customers, focusing on the US government and controlled-substance segments. This provides stability in demand; however, it limits the company’s ability to build its own brands. Still, after IPO, while buying ANDAs, it has focused primarily on drugs that have a significant opportunity in the US government business.

Senores Pharmaceuticals Ltd has faced significant challenges in converting profits into cash. Over FY2021-FY2025, it reported a cumulative PAT of ₹100 crore but a cumulative negative CFO of (₹86) crore. Almost every year, its business required external capital to fund operations, acquisitions and capex.

The company’s free cash flows have been deeply negative, and its business is very capital-intensive both in fixed assets and working capital. Large unbilled revenue may indicate aggressive revenue booking. Recent inventory build-up and long outstanding receivables suggest weak cash discipline. The company still carries overdue receivables for more than one to three years.

The company’s governance indicates quite a few concerning areas. The group structure is complex, with many promoter-owned entities operating in the same line of business. The company has repeatedly bought promoter-group companies at rising valuations, which raises concerns among investors about capital allocation and pricing of related transactions.

Havix Group, the key US subsidiary, has seen significant stake purchases from promoter entities at sharply escalating prices. Emerging market subsidiary, RPPL, was acquired from promoters despite a history of losses and regulatory issues, including instances of substandard drug findings and temporary license suspensions. The newly formed Zoraya Pharmaceuticals LLC again involves external partners holding 49%, though their identities are not disclosed.

Related-party transactions are extensive, including loans from promoter entities and sales through the promoter-owned Remus Pharmaceuticals Ltd. Promoters’ remuneration has escalated sharply in the IPO year, whereas, in FY2024, employee compensation declined. Promoters also benefited from substantial gains in the offer-for-sale portion of the IPO by selling shares, which they had acquired in the previous year at a very low price.

Operational controls and disclosures show inconsistencies. Cash flow statement line items of the company do not reconcile cleanly with the balance sheet data, the annual report contains inaccurate statements about CCD conversions, and regulatory compliance lapses have attracted a caution letter from a bank. These gaps indicate weaknesses in internal processes and raise the risk of errors or potential misuse by stakeholders.

Going ahead, an investor should closely monitor whether the company can convert its reported earnings into sustainable operating cash flows, reduce reliance on equity dilution and debt, and improve working capital discipline. She should pay attention to the margins and profitability after commercialisation of acquired ANDAs, performance of the emerging markets business and utilisation of new API and US manufacturing capacities. She must track Senores Pharmaceuticals Ltd’s regulatory compliance, both in India and the US, related-party transactions, promoter-entity dealings, and any further acquisitions of group companies.

Further recommended reading: How to Monitor Stocks in your Portfolio

These are our views on Senores Pharmaceuticals Ltd. However, investors should do their own analysis before making any investment-related decisions about the company.

You may use the following steps to analyse the company: “Selecting Top Stocks to Buy – A Step by Step Process of Finding Multibagger Stocks”

I hope it helps!

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

I, Vijay Malik, am a SEBI-registered Research Analyst (Regn. No. INH100008364). This article is for educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.

{kind=link}