The current section of the “Analysis” series covers Titan Biotech Ltd, an Indian company engaged in the manufacturing of biotechnology products such as protein hydrolysates, collagen, peptones and dehydrated culture media.

Please note that to get maximum benefit from this article, an investor should focus on the process of analysis instead of looking for good or bad aspects of the company. She should learn the interpretation of diverse types of data and transactions, and pay attention to the parts of annual reports etc., used to get the information. This will help her improve her stock analysis skills.

Titan Biotech Ltd: Detailed Fundamental Analysis

Over the years, Titan Biotech Ltd has had multiple child entities like subsidiaries, associate companies etc. As a result, it has reported both standalone and consolidated financials.

On March 31, 2025, the company had the following two associate companies. FY2025 report, page 71:

- Peptech Biosciences Limited (36.87% stake) and

- Titan Media Limited (48.44% stake)

We believe that while analysing any company, an investor should always look at the company as a whole and focus on financials, which represent the business picture of the entire company, including its subsidiaries, joint ventures etc. Consolidated financials of a company present such a picture. Therefore, if a company reports both standalone and consolidated financials, then the investor should prefer the analysis of the consolidated financials of the company.

As a result, while analysing the past financial performance of Titan Biotech Ltd, we have analysed its consolidated financials.

Further recommended reading: Standalone vs Consolidated Financials: A Complete Guide

With this background, let us analyse the financial performance of Titan Biotech Ltd.

Financial and Business Analysis of Titan Biotech Ltd:

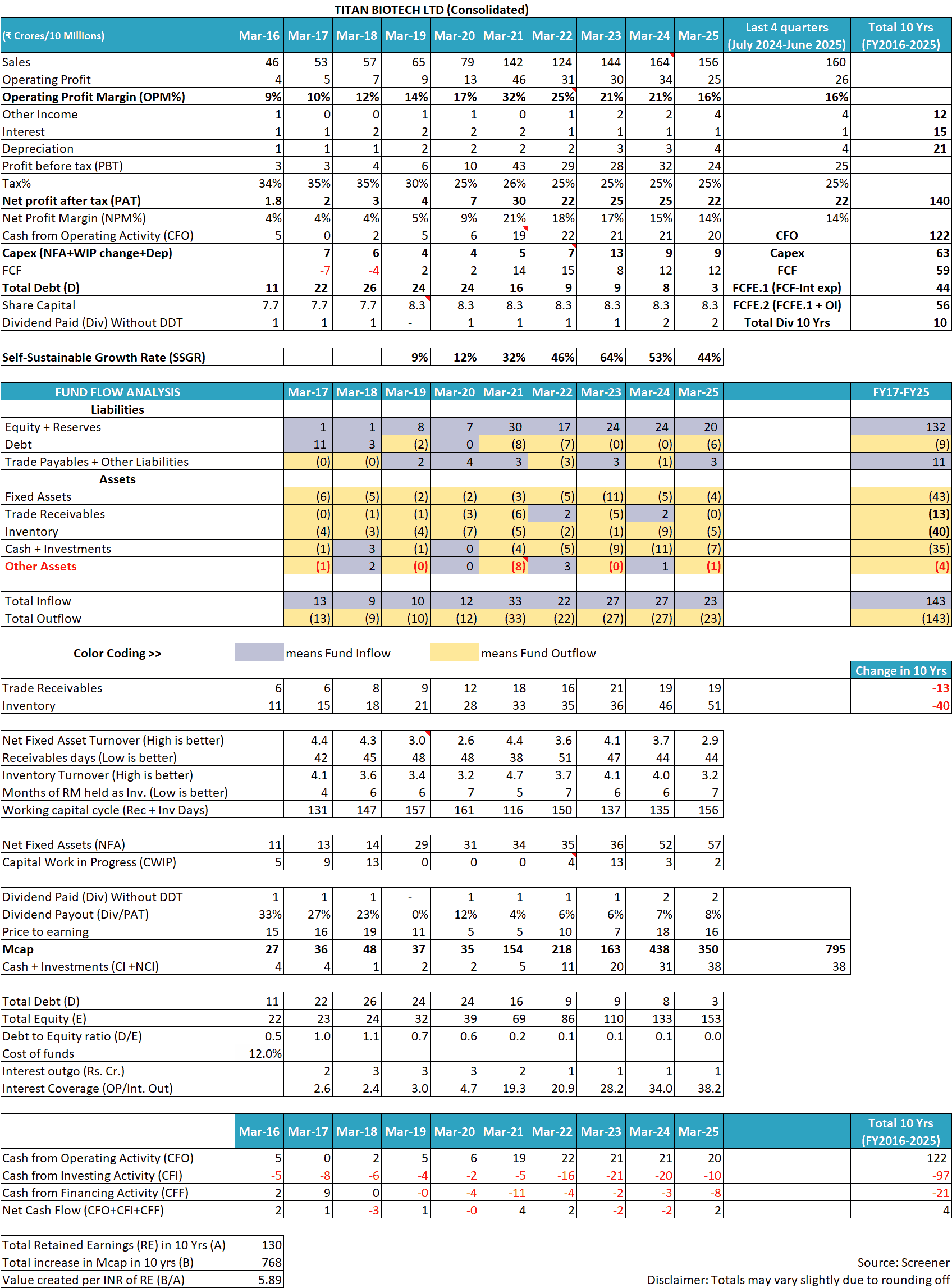

In the last 10 years (FY2016-FY2025), the sales of Titan Biotech Ltd have increased at 15% year on year, from ₹46 cr in FY2015 to ₹156 cr in FY2025. However, growth of sales has not been consistent, and it has seen periods of declining sales. For example, in FY2022, its sales declined by about 13% from ₹142 cr in FY2021 to ₹124 cr in FY2022. Subsequently, in FY2025, its sales declined by about 5% from ₹164 cr in FY2024 to ₹156 cr in FY2025. Thereafter, sales of Titan Biotech Ltd increased to ₹160 cr in 12 months ending June 2025, i.e. July 2024-June 2025.

Over the years, the operating profit margin (OPM) of Titan Biotech Ltd has fluctuated significantly in the range of 9% to 32%. The OPM was 9% in FY2016, which increased to 32% in FY2021. Thereafter, the OPM has consistently declined to 16% in FY2025 and 12 months ended June 2025, i.e. July 2024-June 2025.

The net profit margin (NPM) of the company has also shown similar sharp fluctuations and has fluctuated between 4% to 21%. The NPM increased from 4% in FY2016 to 21% in FY2021, and thereafter, it declined consistently to 14% in FY2025 and 12 months ending June 2025, i.e. July 2024-June 2025.

To understand more about Titan Biotech Ltd, along with fluctuations in its profit margins, an investor needs to read the publicly available documents of the company like its annual reports from FY2013 available on National Stock Exchange (NSE) website, red herring prospectus (RHP) of Sept 2018, credit rating reports from ICRA from 2020 and its corporate announcements submitted to NSE etc.

The above-mentioned documents show that the following key factors have influenced the business of Titan Biotech Ltd, which are critical to understand for any investor.

1) Intense price-based competition faced by Titan Biotech Ltd:

The company faces strong competition from both organised and unorganised, as well as global and domestic companies.

FY2025 annual report, page 92:

Stiff Competition both on domestic and International level poses some threat to the market share of company

The company faced strong competition from the unorganised sector when numerous players entered the industry and hurt the revenue of the company both in terms of sales volume and price. (Source: FY2021 AGM video around 39m:25s).

Titan Biotech Ltd has a very moderate size of business, and it faces competition from numerous international multinational players that are much larger in size with a higher financial and business strength, which puts them at a competitively advantageous position than Titan Biotech Ltd.

FY2025 annual report, page 92:

Your Company operates in a highly competitive market…Some of the competitors of the Company have greater financial, marketing and other resources, which enables them to pursue more vigorous marketing and expansion activities.

As per a report on “Markets and Markets”, in the collagen segment, Titan Biotech Ltd faces competition from companies primarily from developed countries like the US, Europe, Japan and South Korea (Source).

Top 10 Companies in the Collagen Market

- Darling Ingredients (US) Ashland (US)

- Tessenderlo Group (Belgium)

- GELITA AG (Germany)

- Nitta Gelatin NA Inc (Japan)

- Nippi Collagen NA Inc (Japan)

- Collagen Solution (UK)

- Titan Biotech (India)

- Weishardt Holding SA (France)

- DSM (Netherlands)

- Amicogen (South Korea)

The company highlighted that during FY2025, one of the reasons for the decline in its financial performance, both sales and profit margins, was stiff competition and rising costs.

FY2025 annual report, page 92:

revenue of the Company reduced as compared to previous year…mainly due to Economic Slowdown in the Global market, stiff competition, rising cost

Titan Biotech Ltd acknowledged that due to intense competition, it faces challenges in passing on higher input costs to its customers.

FY2025 annual report, page 91:

The major risk is frequent increase in price of few raw materials which can increase the cost of product and can make few products unprofitable unless the increase is passed on to the user which may at times be difficult due to stiff competition.

During Covid period, in FY2021, the company benefited immensely from increased demand for its products that were used in viral transport kits (VTKs). It led to the record operating and net profit margins for Titan Biotech Ltd in FY2021. It reported the highest ever OPM of 32% and NPM of 21% in FY2021. (Source: FY2021 AGM video around 37m:20s).

However, as discussed earlier, soon thereafter, numerous unorganised players entered the segment, and sales volume as well as sales price of its Covid-related products declined, resulting in a decline in sales and profit margins of Titan Biotech Ltd in FY2022.

FY2022 annual report, page 91:

The fall in operating profit margin is only due to reduction in sales & margin from Covid related products only…Net profit is falling due to reduction in sale & margin of Covid related products

Since the peak profit margins in FY2021, the margins of the company have been on a continuous declining trend. An investor should keep a close watch on the profit margins of the company to assess whether it is continuously losing its pricing/negotiating power over its customers.

Also read: How to do Business Analysis of a Company

2) Working-capital-intensive business model of Titan Biotech Ltd, at times leading to liquidity crunch:

Due to low bargaining power over its customers, the company faces issues in collecting money from its customers. As a result, the company has faced bad debts, i.e. receivables were written off by the company e.g. in FY2021, FY2019, FY2014, FY2013 etc.).

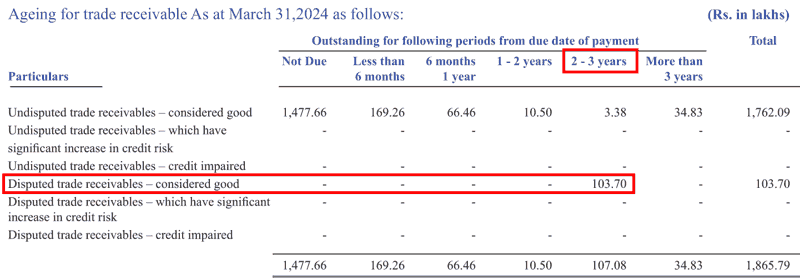

Also, at times, there have been disputes between the company and its customers about the money due for the goods provided by Titan Biotech Ltd. For example, on March 31, 2024, ₹1.03 cr of receivables were under dispute and were pending for a long period of 2-3 years from the customer.

FY2024 annual report, page 167:

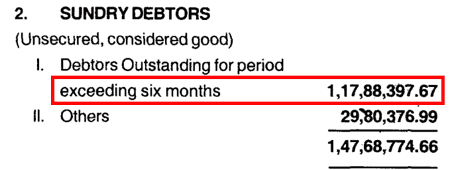

In the past, Titan Biotech Ltd has faced severe working capital issues. For example, in FY2005, at one point in time, more than 70% of its overall trade receivables were delayed by more than 6 months from their due date.

FY2025 annual report, page 31:

In FY2002, the company faced a strong liquidity crunch to such an extent that it could not pay listing fees to stock exchanges.

FY2002 annual report, page 7:

As the Company is facing through a severe liquidity crunch, in order to reduce the necessary cost, the Board of Directors have decided to delist the shares

In FY2003, due to a liquidity crunch, the company could not pay the listing fees of the Bombay Stock Exchange (BSE) on time.

FY2003 annual report, page 8:

There is no non-compliance…except Rs 15000/- paid to stock exchange Mumbai for late payment of listing fee

At times, a shortage of working capital hurts its business performance.

FY1997 annual report, page 4:

but due to shortage of working capital desired results could not be achieved.

High working capital requirements of Titan Biotech Ltd have been one of the reasons for its repeated equity dilution, where shareholders had to infuse money to meet its funding requirements.

FY2017 annual report, page 10:

Company need funds for its business working capital and long term financial needs and therefore it proposes to issue further equity shares to the companies in the promoter group

Over the years, Titan Biotech Ltd has had to repeatedly resort to equity dilution to meet its cash shortfall.

Nevertheless, as we discuss below, in recent years, the company seems to have managed its financial position and is currently carrying surplus cash.

Going ahead, an investor should keep a close watch to assess whether it is able to maintain its capital position or it has to rely on outside/additional funds to run its business.

Also read: Operating Performance Analysis: A Simple & Complete Guide

3) Development of new products by Titan Biotech Ltd:

In order to improve the value proposition that it offers to its customers, Titan Biotech Ltd has attempted to increase its product offerings so that it can gain a higher share of customers’ business.

For example, the company developed Amino acid Chelates and harmonised media in FY2010 (Source: FY2010 annual report, page 11).

Further, since FY2021, Titan Biotech Ltd is developing products for health supplements.

FY2021 annual report, page 74:

FUTURE PLANS: The Company is developing product for health supplement.

However, it seems that despite efforts of almost 5 years, the company is yet to gain any significant success in products for health supplements because even in FY2025, Titan Biotech Ltd is still in the process of developing them.

FY2025 annual report, page 60:

FUTURE PLANS: The Company is developing product for health supplement.

An investor may contact the company directly to understand whether it still plans to develop products for health supplements, and if so, then what is the current stage of progress and how much time and investment it is expected to take for their commercial launch.

Over the last 10 years (FY2016-FY2025), the tax payout ratio of Titan Biotech Ltd has been in line with the standard corporate tax rate in India.

Also read: How to do Financial Analysis of a Company

Operating Efficiency Analysis of Titan Biotech Ltd:

a) Net fixed asset turnover (NFAT) of Titan Biotech Ltd:

Over the years, NFAT of the company has decreased from 4.4 in FY2017 to 2.9 in FY2025. A declining NFAT indicates sub-optimal utilisation of assets by the company.

The decline in NFAT has coincided with the capital expenditure done by Titan Biotech Ltd.

For example, it did a major revamp/modernisation of its plant in Bhiwadi in FY2019. As the new plant became functional, it took time to increase its commercial utilisation. As a result, the NFAT of Titan Biotech Ltd declined from 4.3 in FY2018 to 2.6 in FY2020.

Later, during Covid, in FY2021, the demand for the company’s products increased, which increased its capacity utilisation. However, in recent years, the company has done another round of capital expenditure in its manufacturing plants in FY2023-FY2024.

As a result of suboptimal capacity utilisation of the new capital expenditure, the NFAT of Titan Biotech Ltd has declined from 4.1 in FY2023 to 2.9 in FY2025.

Going ahead, an investor should keep a close watch on the fixed asset turnover levels of the company to assess whether it is able to optimally utilise its manufacturing assets.

Further advised reading: Asset Turnover Ratio: A Complete Guide for Investors

b) Inventory turnover ratio (ITR) of Titan Biotech Ltd:

Over the years, the inventory turnover ratio (ITR) of the company has declined from 4.1 in FY2017 to 3.2 in FY2025. A decline in ITR indicates declining efficiency of inventory management by the company.

An ITR of 4 (in FY2017) indicates that the company needs to keep about 3 months of sales as inventory with itself, whereas an ITR of about 3 (in FY2025) indicates that now, Titan Biotech Ltd needs to keep about 4 months of sales as inventory with itself.

An increase in inventory requirement makes its operations working capital-intensive.

Going ahead, an investor should keep a close watch on the inventory position of the company to understand whether it is able to keep its working capital situation under control or not.

Further advised reading: Inventory Turnover Ratio: A Complete Guide

c) Analysis of receivables days of Titan Biotech Ltd:

Over the years, receivables days for the company have deteriorated from 42 days in FY2017 to 44 days in FY2025. The company saw its receivables days extend to 51 days in FY2022 when, as discussed earlier, it faced a significant amount of receivables disputes with its customers for about ₹1.03 cr (Source: FY2022 annual report, page 169).

However, thereafter, the receivables days of Titan Biotech Ltd have improved to 44 days in FY2025.

Going ahead, an investor should watch the trend of receivables days of Titan Biotech Ltd to assess whether it is able to collect its receivables on time to run its business from its business/operating cash flows, or it continues to dilute equity to meet its day-to-day funding needs.

Further recommended reading: Receivable Days: A Complete Guide

When an investor compares the cumulative net profit after tax (cPAT) and cumulative cash flow from operations (cCFO) of Titan Biotech Ltd for FY2016-FY2025, then she notices that over the years (FY2016-FY2025), the company is not able to convert its profit into cash flow from operations.

Over FY2016-25, Titan Biotech Ltd reported a total cumulative profit after tax (cPAT) of ₹140 cr. During the same period, it reported a cumulative cash flow from operations (cCFO) of ₹122 cr.

It is advised that investors should read the article on CFO calculation, which would help them understand the situations in which companies tend to have the CFO lower than their PAT. In addition, the investors would also understand the situations when the companies would have their CFO higher than PAT.

Further recommended reading: Understanding Cash Flow from Operations (CFO)

The Margin of Safety in the Business of Titan Biotech Ltd:

a) Self-Sustainable Growth Rate (SSGR):

Read: Self Sustainable Growth Rate: a measure of Inherent Growth Potential of a Company

Upon reading the SSGR article, an investor would appreciate that if a company is growing at a rate equal to or less than the SSGR and it can convert its profits into cash flow from operations, then it would be able to fund its growth from its internal resources without the need for external sources of funds.

Conversely, if any company attempts to grow its sales at a rate higher than its SSGR, then its internal resources would not be sufficient to fund its growth aspirations. As a result, the company would have to rely on additional sources of funds, like debt or equity dilution, to meet the cash requirements to generate its target growth.

An investor may calculate the SSGR using the following formula:

SSGR = NFAT * NPM * (1-DPR) – Dep

Where,

- SSGR = Self Sustainable Growth Rate in %

- Dep = Depreciation rate as a % of net fixed assets

- NFAT = Net fixed asset turnover (Sales/average net fixed assets over the year)

- NPM = Net profit margin as % of sales

- DPR = Dividend paid as % of net profit after tax

(For systematic algebraic calculation of SSGR formula: Click Here)

Over the years, the SSGR of Titan Biotech Ltd has been highly fluctuating between 9% to 64%. This is because the company faced sharp fluctuations in its NFAT and NPM. Nevertheless, the average of SSGR of all the reported years from FY2019 to FY2025 is about 37% whereas during the last 10 years, the company has grown at a pace of 15% year on year.

As a result, over the years, the company has kept its debt levels under check.

The situation becomes further clear when an investor does a free cash flow analysis of Titan Biotech Ltd.

b) Free Cash Flow (FCF) Analysis of Titan Biotech Ltd:

While looking at the cash flow performance of Titan Biotech Ltd, an investor notices that during FY2016-FY2025, it generated a cash flow from operations of ₹122 cr. During the same period, it made a capital expenditure of about ₹63 cr.

Therefore, during this period (FY2016-FY2025), Titan Biotech Ltd had a free cash flow (FCF) of ₹59 cr (= 122 – 63).

In addition, during this period, the company had a non-operating income of ₹12 cr and an interest expense of ₹15 cr. As a result, the company had a total free cash flow of ₹56 cr (= 59 + 12 – 15). Please note that the capitalised interest is already factored in as a part of the capex deducted earlier.

Over the years, Titan Biotech Ltd has used this surplus cash to:

- Reduce its total debt by ₹8 cr from ₹11 cr in FY2016 to ₹3 cr in FY2025.

- Pay dividends of about ₹10 cr during FY2016-FY2025 and

- Increase its cash & investments by ₹34 cr from ₹4 cr in FY2016 to ₹38 cr in FY2025.

However, in the past, the business of Titan Biotech Ltd did not generate surplus cash, and as a result, it had to undergo multiple rounds of equity dilution to raise funds for its business.

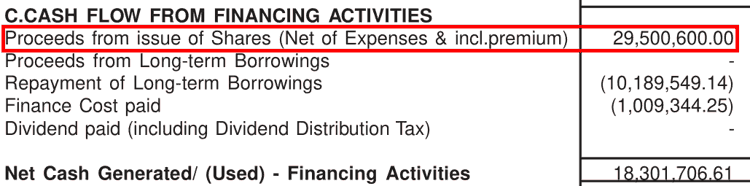

For example, in FY2012, it raised funds by issuing shares for about ₹2.95 cr to institutional investors: Ace Securities Pvt. Ltd. and AVB Shares Trading Pvt. Ltd. (Source: FY2012 annual report, pages 44 and 93).

Thereafter, in FY2015, Titan Biotech Ltd raised further capital of ₹4.2 cr by issuing shares to promoters and non-promoter entities (Source: FY2015 annual report, pages 56 and 73).

Subsequently, in FY2019, the company issued shares on a preferential basis to raise ₹4.2 cr from promoters and non-promoter entities (Source: FY2019 annual report, pages 60 and 154).

Going ahead, an investor should keep a close watch on the cash flow position of Titan Biotech Ltd to understand whether the company continues to generate surplus cash from its business or it relies on outside funds for growth and running its day-to-day operations.

Further recommended reading: Free Cash Flow: A Complete Guide to Understanding FCF

Self-Sustainable Growth Rate (SSGR) and free cash flow (FCF) are the main pillars of assessing the margin of safety in the business model of any company.

Further advised reading: 3 Simple Ways to Assess “Margin of Safety”: The Cornerstone of Stock Investing

Additional aspects of Titan Biotech Ltd:

On analysing Titan Biotech Ltd and after reading annual reports, credit rating reports and other public documents, an investor comes across certain other aspects of the company, which are important for any investor to know while making an investment decision.

1) Management Succession of Titan Biotech Ltd:

The company is run by Mr Naresh Kumar Singla (Managing Director, age 66 years) and Mr Suresh Kumar Singla (Managing Director, age 65 years).

Currently, family members of both Mr Naresh and Mr Suresh, including the next generation, have joined the business.

Two sons of Mr Naresh Kumar Singla, Mr Raja Singla and Mr Shivom Singla, both aged 36 years, are working as Whole Time Directors/Executive Directors on the board of the company. (Source: FY2025 annual report, pages 25-27).

From the family of Mr Suresh Kumar Singla, his wife, Ms Manju Singla (Director, age 61 years), his son, Mr Udit Singla (Whole Time Director/Executive Director, age 36 years) and his daughter, Ms Supriya Singla (Director, age 36 years) are present on the board of the company. (Source: FY2025 annual report, pages 25-27).

The presence of members of the next generation of families in the company when the founding promoters are still serving an active role seems to be a well-thought-out management succession plan.

It is especially essential in the case of promoter-run businesses, as it provides for a smooth transition of leadership over the generations and provides continuity in the business operations of any company. Moreover, as the next generation seems to have joined the business in active roles while the older generation is still active, it might allow them a good time to learn the business under able guidance.

Nevertheless, an investor should keep a close watch on the dynamics between the members of the two promoter families. This is because any discord between the families of Mr Naresh Kumar Singla and Mr Suresh Kumar Singla regarding ownership, strategic direction, use of capital etc. might lead to infighting and, in tur,n divert the focus of the leadership away from the best interests of public shareholders.

Also read: How to do Management Analysis of Companies?

2) Remuneration to promoters’ family members by Titan Biotech Ltd:

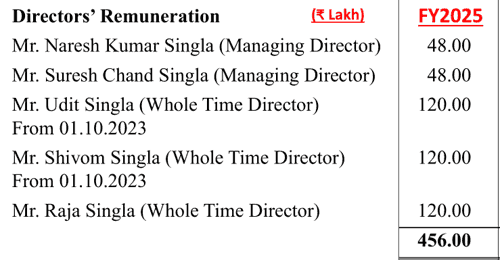

In FY2025, the company paid a remuneration of ₹0.48 cr (₹48 lakh) each to its founding promoters (managing directors): Mr Naresh Kumar Singla and Mr Suresh Chand Singla.

However, it paid a remuneration of ₹1.20 cr each to the sons of the founding promoters (whole-time directors): Mr Udit Singla, Mr Shivom Singla and Mr Raja Singla.

Overall, in FY2025, Titan Biotech Ltd paid a total remuneration of ₹4.56 cr to promoter family members, in contrast to its net profit after tax of about ₹22 cr, indicating that promoters’ remuneration was more than 20% of its profit after tax.

FY2025 annual report, page 179:

Moreover, in the FY2025 annual general meeting (AGM), the company has proposed a significant increase in remuneration for all the promoters’ family members:

Remuneration of founding promoters/managing directors is proposed to increase up to a maximum of ₹2.4 cr per year, which is 5 times the remuneration of ₹0.48 cr each paid by the company to them in FY2025 (Source: FY2025 annual report, pages 17-18).

Similarly, remuneration of the sons of founding promoters/whole-time directors, Shivom and Udit Singla, is also proposed to be increased to a maximum of ₹2.4 cr each, which is double the remuneration of ₹1.2 cr each paid by the company to them in FY2025 (Source: FY2025 annual report, pages 20-21).

If these proposals are approved by shareholders, then the amount of remuneration that Titan Biotech Ltd would be able to pay to the promoters’ family will increase substantially in absolute terms as well as in proportion to its profits.

We believe that an investor should keep a close watch on the remuneration provided by the company to its promoters and seek clarifications from the company directly, if any.

Also read: How to identify Promoters extracting Money via High Salaries

3) Related party transactions of Titan Biotech Ltd with its promoter-group entities:

3.1) Sales, purchases and loans to promoter-group entities:

Over the years, the company has been involved in multiple transactions with its promoter-group entities, such as sales, purchases, giving and taking loans, purchase of assets etc.

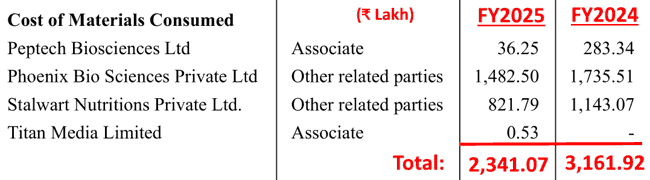

For example, in FY2025, Titan Biotech Ltd purchased goods of more than ₹23 cr from its related parties. In FY2024, it had purchased goods for more than ₹31 cr from related parties.

FY2025 annual report, page 179:

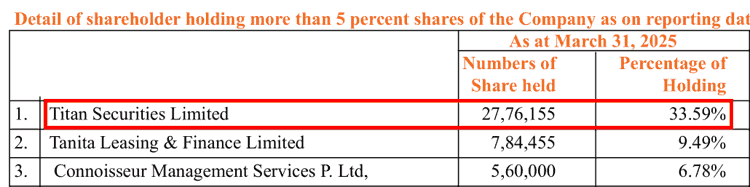

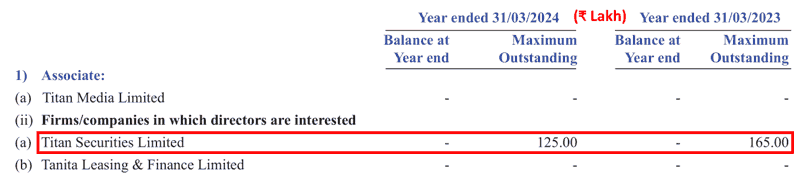

In addition, there have been instances where promoter group companies have used Titan Biotech Ltd as a lender and have used the financial resources of the publicly listed company for their benefit. For example, take the case of a company, Titan Securities Limited, through which promoters hold a 33.59% stake in Titan Biotech Ltd.

FY2025 annual report, page 120:

At times, Titan Securities Limited has taken a loan during the year and has repaid it before the year-end in one year and repeated the same process the next year while leaving the year-end balance as nil. In FY2023 and FY2024, Titan Biotech Ltd gave loans of ₹1.65 cr and ₹1.25 cr, respectively, to Titan Securities Ltd.

FY2024 annual report, page 180:

An investor may note that each of such sale/purchase/lending transactions provides an opportunity for shifting of economic benefit from public shareholders to promoters if the listed company buys goods/services from promoter entities at a price higher than their market price or sells goods/services to promoter entities at a price lower than their market price. Therefore, an investor should always do deeper due diligence of such sale/purchase transactions with related parties.

Also read: How Promoters benefit from Related Party Transactions

3.2) Curious case of Peptech Bioscience Limited (PBL):

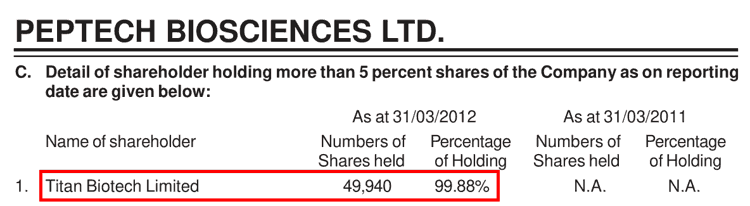

In FY2012, Titan Biotech Ltd created a new subsidiary named Peptech Bioscience Limited (PBL) with 99.88% shareholding, to transfer its manufacturing plant situated at Chopanki.

FY2011 annual report, pages 2-3:

company do incorporate subsidiary named Peptech Biosciences Limited or such other name as may be made available by the Ministry of Corporate Affairs

As the company intends to sell/dispose off the Chopanki Unit of the Company…approve sale/disposal of the unit/undertaking of the Company at Chopanki to its proposed new subsidiary

FY2012 annual report, page 30:

A subsidiary in the name of Peptech Biosciences Limited was incorporated on 15th, November, 2011.

FY2012 annual report, page 99:

By FY2022, PBL has grown its business and started reporting healthy revenue and profits. As per the statutory audit report of Titan Biotech Ltd for FY2022, PBL reported a revenue of about ₹34 cr and a net profit of about ₹7 cr.

FY2022 annual report, page 149:

one associate, namely Peptech Biosciences Limited whose…total revenues of Rs.3471.37 Lakhs, net profit of Rs. 723.84 Lakhs

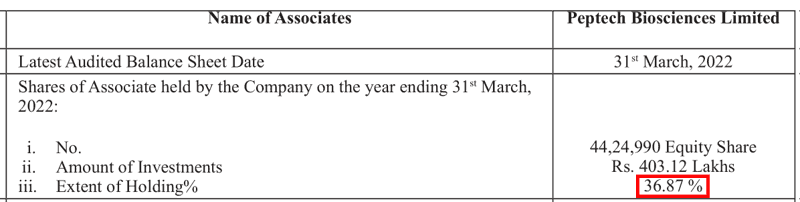

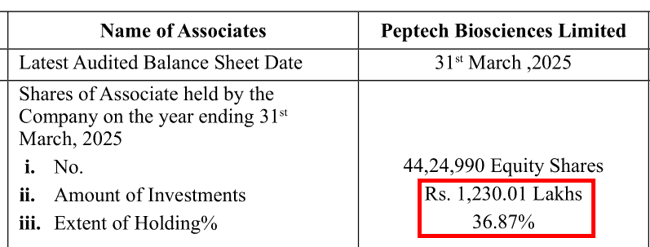

However, by this time, Titan Biotech Ltd had reduced its shareholding in PBL to 36.87% and other shareholders had gained control.

FY2022 annual report, page 69:

The annual report of Titan Biotech Ltd also provides some glimpses into who these other major shareholders of PBL are. As per the FY2022 annual report, pages 23-24, the sons of the founding promoters, Mr Udit Singla, Mr Raja Singla and Mr Shivom Singla, own 5% each, and the daughter of the founding promoter, Ms Supriya Singla, holds 4.99% of the shareholding in PBL.

The above information indicates that over the years, as PBL started making good revenue, promoters started increasing their stake in the company in their personal capacity, and the shareholding of Titan Biotech Ltd in PBL declined from 99.88% to 36.87%.

Thereafter, by FY2025, Titan Biotech Ltd has invested more money via partly paid shares (about ₹8 cr) and given more debt (₹3 cr, FY2025 annual report, page 178) to PBL. However, its shareholding in the company is stable at 36.87%.

FY2025 annual report, page 70:

An investor may do her due diligence about the change of control of PBL from Titan Biotech Ltd to its promoters over the years, as PBL’s business started performing. In case of any clarifications, she may contact the company directly.

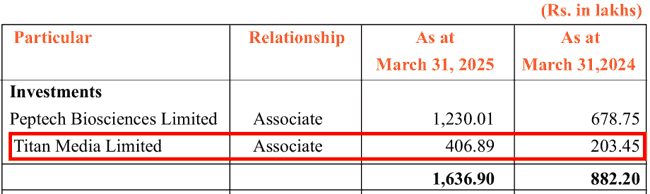

3.3) Purchase of stake in promoter-group entity Titan Media Ltd by Titan Biotech Ltd:

In FY2024, the company agreed to purchase a 64.58% stake in its promoter-group company, Titan Media Ltd (TML), over the years by making a total investment of ₹8.13 cr spread in multiple tranches with a similar increase in shareholding with each payment. This transaction values TML at about ₹12.58 cr (= 8.13/0.6458).

FY2024 annual report, page 67:

Company has acquired 33,90,510 partly paid up equity shares of Rs 24/- each at par aggregating to Rs. 8,13,72,240…out of which Rs. 2,03,43,060/-…had paid on application…Company agreed to acquire equity shares equivalent to voting rights of 64.58%

In this regard, Titan Biotech Ltd paid ₹2.03 cr in FY2024 and an additional ₹2.03 cr in FY2025, taking the total investment up to ₹4.06 cr at the end of FY2025.

FY2025 annual report, page 180:

In FY2025, TML made a profit of ₹0.12 cr (₹11.70 Lakh) (Source: FY2025 annual report, page 71).

A valuation of ₹12.58 cr for a company making a profit of ₹0.1170 cr values TMP at a price to earnings (P/E) ratio of about 114 (=12.58 / 0.1170).

An investor may do her due diligence to assess whether taking control of a company from its promoters at a PE ratio of about 114 is a value-adding step by Titan Biotech Ltd.

Whenever an investor comes across transactions between any publicly listed company and its promoters/promoter-controlled entities, then she should be cautious because each such transaction has the potential to shift economic benefits from minority/public shareholders of the listed company to promoters.

Also read: Why Management Assessment is the Most Critical Factor in Stock Investing?

4) Weakness in internal controls and processes at Titan Biotech Ltd:

On multiple occasions, an investor notices instances indicating a scope for improvement in the internal controls and processes at Titan Biotech Ltd.

For example, in FY2019, when the company issued 525,000 equity shares on a preferential basis, its secretarial audit report mentioned that there were no instances of any preferential issue of shares in the year.

FY2019 annual report, page 157:

The above table clearly shows that Titan Biotech Ltd issued 525,000 shares in FY2019. Whereas the section below from the secretarial audit report from the FY2019 annual report, page 82 of the company, denies any preferential issuance of shares during the year.

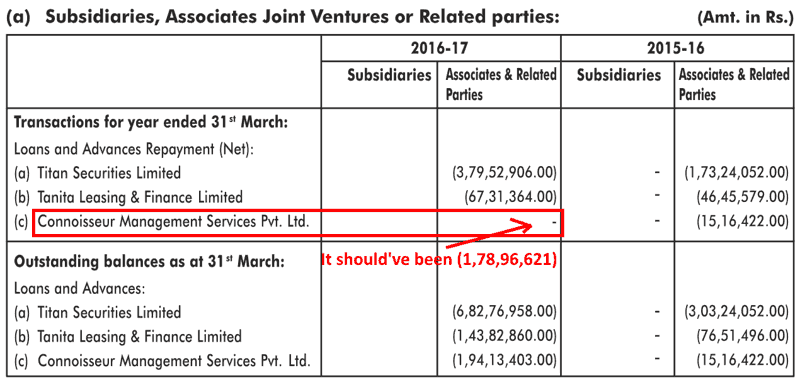

On a separate occasion, in FY2017, in the related party transactions section of its annual report, Titan Biotech Ltd did not disclose any transaction of loans & advances during the year with Connoisseur Management Services Pvt. Ltd.; however, its year-end outstanding balance increased from ₹0.15 cr (₹15.16 lakh) in FY2016 to ₹1.94 cr in FY2017, indicating that Titan Biotech Ltd had taken loans of about ₹1.79 cr (₹1,78,96,621 = 1,94,13,403.00 – 15,16,422.00) from Connoisseur Management Services Pvt. Ltd.

FY2017 annual report, page 114:

In the same table, an investor may note that the transactions with Titan Securities Limited and Tanita Leasing & Finance Limited are disclosed properly with the sum of the year-end balance at FY2016 and the amount of transactions during FY2017, summing properly to the year-end balance with each entity at the end of FY2017.

- Titan Securities Limited: 3,03,24,052.00 + 3,79,52,906.00 = 6,82,76,958.00

- Tanita Leasing & Finance Limited: 76,51,496.00 + 67,31,364.00 = 1,43,82,860.00

In the FY2010 annual report, in the related parties transactions table, it did not disclose the remuneration/salary paid to its promoters.

FY2010 annual report, page 35:

Whereas in the FY2010 annual report, it paid a remuneration of ₹1,740,000/- to each of its founders/managing directors, Mr Naresh Kumar Singla and Mr Suresh Chand Singla (Source: FY2010 annual report, page 3). However, its related party transactions table did not include this information.

In light of such issues, an investor is advised to be extra cautious while analysing the information provided by Titan Biotech Ltd and its auditors in its public disclosures, including annual reports.

From April 1, 2023, i.e. FY2024, every company in India is required to use accounting software with an audit trail feature (Source: Audit Trail feature in accounting software from 1st April, 2023: Taxguru).

However, Titan Biotech Ltd has not yet enabled the audit trail feature in its accounting software. Both in FY2024 and FY2025, the company mentioned in its annual report that it is in contact with the vendor regarding this.

FY2024 annual report, page 190:

The ERP used by holding company and one of the associates company the feature of audit trail log has not been enabled…This is being taken up with the vendor.

FY2025 annual report, page 187:

The ERP used by the Company has not been enabled with the feature of audit trail log…This is being taken up with the vendor.

Also read: How to study Annual Report of a Company

An investor may contact the company directly to understand the reasons for the delay in enabling the audit trail feature in its ERP/accounting software.

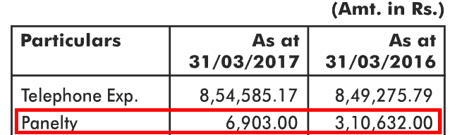

In the past, Titan Biotech Ltd has faced penalties, probably due to non-compliance, for example, in FY2016, FY2017 and FY2018.

FY2017 annual report, page 110:

In FY2010, Titan Biotech Ltd faced a penalty on account of sales tax (Source: FY2010 annual report, page 30).

On numerous occasions in the past, Titan Biotech Ltd has delayed filing of forms and information related to the Companies Act and Rules.

FY2024 annual report, pages 82-83:

except some forms or information or documents under the Companies Act and Rules or made thereunder have been filed late

there were few instances of delay in filing of forms with the Ministry of Corporate Affairs/Investor Education & Protection Fund Authority which were regularized by payment of late filing fee.

The company had similar delays in filing in FY2023 (annual report, page 91), FY2022 (annual report, page 79), FY2021 annual report, page 101), FY2020 (annual report, page 81) etc.

In one of its corporate announcements on August 13, 2025, while intimating about its annual general meeting (AGM), it mentioned its book closure date from September 21, 2025. However, soon, the company realised that it had made a mistake and on August 25, 2025, it had to file a revised notification rectifying the book closure date from September 20, 2025.

Corporate announcement to BSE, August 25, 2025:

The date was inadvertently mentioned as 21st September 2025 instead of 20th September 2025.

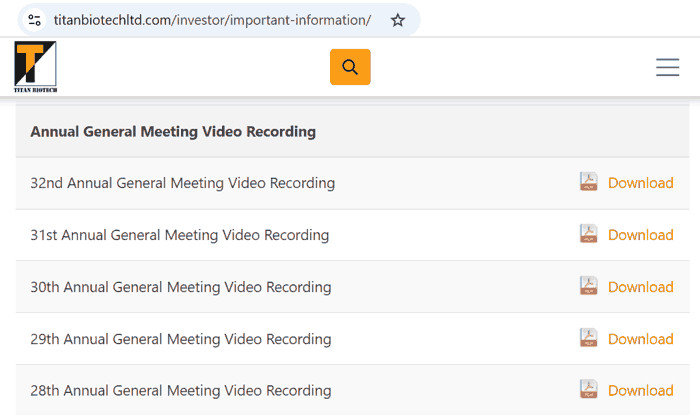

On its website, Titan Biotech Ltd has provided links to video recordings of its 28th (FY2020), 29th (FY2021), 30th (FY2022), 31st (FY2023) and 32nd (FY2024) AGMs on the following page: https://titanbiotechltd.com/investor/important-information/

The page links to the following pages on YouTube:

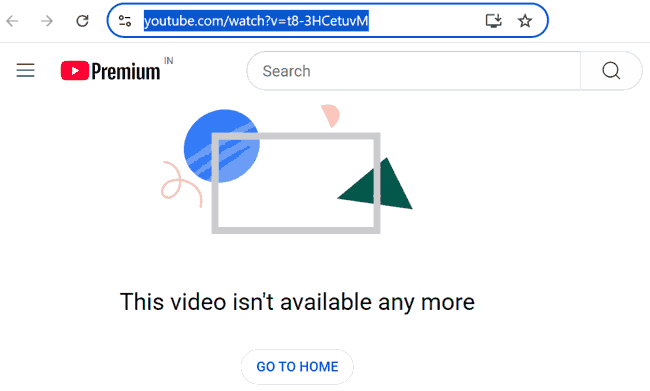

- 32nd AGM (FY2024): https://www.youtube.com/watch?v=t8-3HCetuvM

- 31st AGM (FY2023): https://youtu.be/yEIH9FpG6ec

- 30th AGM (FY2022): https://youtu.be/nFp_BkEHikc

- 29th AGM (FY2021): https://youtu.be/tpZug9mc5IY

- 28th AGM (FY2020): https://www.youtube.com/watch?v=FvBpXhEZgMw

However, out of these, only the link for the 29th AGM (FY2021) works, and the rest of the videos do not exist.

An investor may contact the company directly to seek access to the video recordings of remaining AGMs.

Similarly, annual reports of multiple years are not available in the important public domain sources like the company’s own website (Source) and the website of BSE (Source), which has annual reports of companies from FY1997 onwards.

Annual reports of FY1998, FY2001, FY2004, FY2006, and FY2009 are missing from the above-mentioned sources (the company’s website and BSE).

An investor may contact Titan Biotech Ltd directly to seek annual reports for these missing years.

The above instances indicate that the company needs to improve its internal controls and processes, including the maker-checker arrangement for its public disclosures. As a result, investors should be cautious while analysing the data of the company.

The Margin of Safety in the market price of Titan Biotech Ltd:

Currently (September 22, 2025), Titan Biotech Ltd is available at a price-to-earnings (PE) ratio of about 36 based on consolidated earnings of the last 12 months (July 2024-June 2025).

We recommend that an investor read the following articles to assess the P/E ratio to be paid for any stock, which considers the strength of the business model of the company as well. The strength in the business model of any company is measured by its self-sustainable growth rate and the free cash flow generating ability of the company.

In the absence of any strength in the business model of the company, even a low PE ratio of the company’s stock may be a sign of a value trap, where, instead of being a bargain, the low valuation of the stock price may represent the poor business dynamics of the company.

- 4 Principles to Decide the Ideal P/E Ratio of a Stock for Value Investors

- How to Earn High Returns at Low Risk – Invest in Low P/E Stocks

- Hidden Risk of Investing in High P/E Stocks

Analysis Summary

Over FY2016–2025, Titan Biotech Ltd grew its sales at a 15% CAGR; however, this growth has been uneven with revenue declines in FY2022 and FY2025. Both operating and net profit margins have also been very volatile. These swings indicate a business lacking consistent pricing power, benefiting temporarily from extraordinary events like Covid pandemic, but unable to sustain high profit margins.

Titan Biotech Ltd operates in a highly competitive industry facing pressure from unorganised domestic players who compete aggressively on price as well as from much larger multinational companies with deeper resources. The company finds it difficult to pass through rising raw material costs to customers due to this competition. The sharp fall in profitability after FY2021, when demand for COVID-related products declined, shows the vulnerability of its business. Its profit margins have been on a declining trend since then, showing weaker negotiating power with customers.

The company’s business has been working-capital-intensive. Titan Biotech Ltd has a history of delayed receivables and write-offs. In FY2024, disputed receivables of over ₹1 crore had remained unresolved for a couple of years. In the past, it faced severe liquidity problems, and it could not run its business properly nor could it pay listing fees on time. Such pressures have often forced it to go for multiple equity dilutions to fund its operations.

Its operating efficiency parameters, like NFAT, inventory turnover ratio etc. indicate sub-optimal utilisation of assets. Receivable days worsened from 42 in FY2017 to 51 in FY2022, though they later improved modestly to 44 days.

Investors notice some concern regarding the remuneration paid by Titan Biotech Ltd to its promoter-family members. In FY2025, total remuneration to promoters and family members was ₹4.56 crore, more than 20% of the reported net profit. Moreover, it plans to increase the amounts substantially.

The company has extensive related-party transactions with promoter-owned entities. It makes purchases of about ₹23–31 crore annually from promoter-linked entities. It extended loans to Titan Securities Ltd, a promoter-controlled entity, which were repaid before year-end but repeated across years.

The case of Peptech Biosciences Ltd is notable. Originally a 99.9% subsidiary into which Titan transferred a manufacturing unit, PBL became profitable by FY2022 with ₹34 crore in revenue and ₹7 crore profit. Over the years, Titan’s stake was diluted to 36.9% while promoter family members gained direct ownership. Despite this, Titan continues to invest funds into PBL through partly paid shares and loans, raising questions about shifting benefits away from minority shareholders.

Similarly, the acquisition of Titan Media Ltd, another promoter-group company, at a valuation implying a price-to-earnings multiple of about 114, requires deeper due diligence by investors to assess whether it represents value for the public shareholders of Titan Biotech Ltd.

The company shows weaknesses in internal controls and compliance. There have been inconsistencies in disclosures, such as preferential shares issued in FY2019 but not reflected in the secretarial audit, loans not disclosed in related party transactions in FY2017, and promoters’ remuneration missing from related party disclosures in FY2010.

Titan Biotech Ltd has repeatedly delayed statutory filings, faced penalties in multiple years, and has still not enabled the mandatory audit trail feature in its ERP system despite regulatory requirements since April 2023. Some routine matters have shown lapses, such as errors in AGM notices, missing annual reports on public platforms, and non-functional AGM video links. These suggest inadequacies in internal processes and disclosure practices, increasing the risk that minority shareholders may not always have reliable information.

Management succession appears better planned, with the next generation already inducted into executive roles alongside the founding promoters. However, with control concentrated in two promoter families, investors should be cautious about any potential dispute among promoter families.

Going ahead, investors should monitor whether Titan Biotech Ltd can stabilise its operating and net profit margins, manage its receivable days, bad debts, and cash flow conversion. She should keep a close watch on its asset utilisation and inventory turnover, which also needs scrutiny to assess whether recent capacity expansions deliver adequate returns. She should monitor promoters’ remuneration, related-party transactions, and acquisitions so that she can be alert about any early red flags.

Further recommended reading: How to Monitor Stocks in your Portfolio

These are our views on Titan Biotech Ltd. However, investors should do their own analysis before making any investment-related decisions about the company.

You may use the following steps to analyse the company: “Selecting Top Stocks to Buy – A Step by Step Process of Finding Multibagger Stocks”

I hope it helps!

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

I, Vijay Malik, am a SEBI-registered Research Analyst (Regn. No. INH100008364). This article is for educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.

{kind=link}