The current article covers the step-by-step calculation of cash flow from operations (CFO) from net profits (PAT) of a company.

In addition, the article covers responses to the common queries asked by readers about CFO.

Step-by-Step Calculation of Cash Flow from Operating Activities (CFO) from PAT

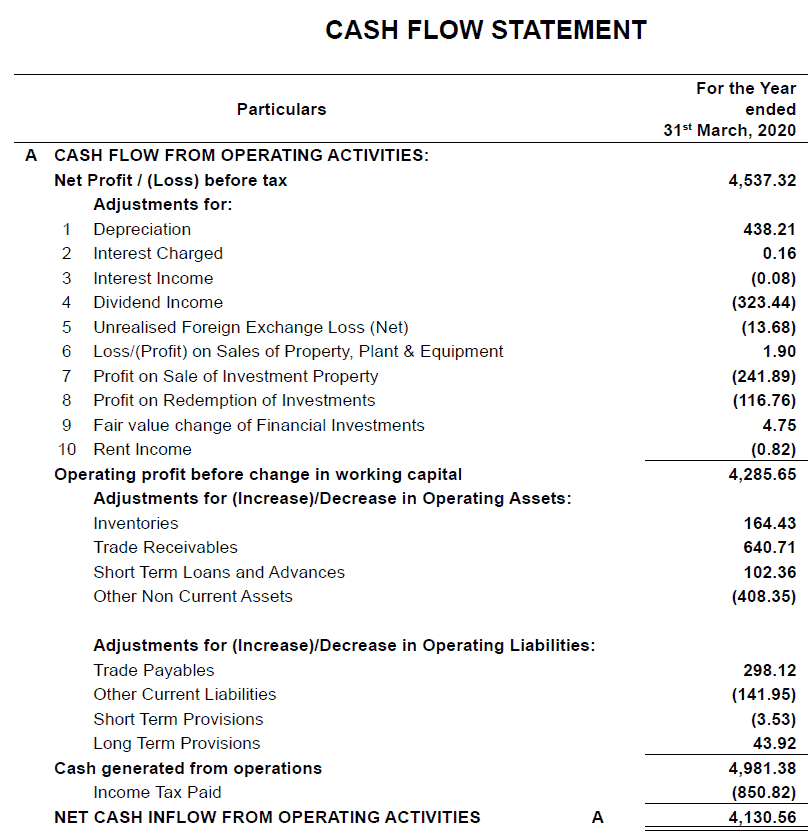

Let us see the steps used in the calculation of cash flow from operations from the profits of the company by taking examples of Paushak Ltd. It is India’s largest phosgene based speciality chemicals manufacturer. Paushak Ltd is a part of the Alembic Pharmaceuticals group.

(The figures are in ₹ Lakhs)

1) Depreciation of ₹3.48 cr is added. It creates a cash inflow in the statement, though practically it has no impact on cash generation.

Depreciation expense like amortisation is a non-cash expense. It is the adjustment of cash outflows, which happened in the past while creating fixed assets (plants, machinery etc.). At the time of the creation of plants, the cash outflow took place but the same was not deducted from the P&L as it was directly put on the balance sheet under fixed assets. The depreciation expense is the deduction of those past cash outflows from the P&L now. It is effectively to match the expense deduction of the cost of plants with the revenue being generated by them now.

Further Reading: Capitalization of Interest, Fixed Asset Turnover

As mentioned above, in the case of depreciation, the cash outflow has already happened in the past and now there is no cash outflow. However, the PAT of the company has been arrived at after deduction of depreciation (no cash outflow). Therefore, to derive at the actual cash position of the company from PAT/PBT, we add back the depreciation. Otherwise, the cash flow from operations (CFO) calculation will be erroneously lower whereas we will find that the company has excess cash, which is not accounted for.

2) Interest charged/paid is ₹0.16 lakh: It is added as cash inflow for CFO, whereas it is actually a cash outflow from the company.

Interest paid/expense is added back in profit before tax (PBT) as it is a financing item and therefore it should not reduce the cash flow from operating activities (CFO). We add the interest paid in PBT to arrive at CFO and the same interest paid is deducted as a cash outflow from financing in cash flow from financing activities (CFF). This is a mere reclassification of interest expense from CFO to CFF.

3) Various incomes like interest income, dividend income, rental income, profits on the sale of investment property, profit on the redemption of investments are deducted: actually, these are cash inflows to the company.

All these are non-operating incomes. Interest income, dividend income, rental income and profits on the sale of investments etc. are deducted from profits to derive CFO as these are income from investments in financial instruments and properties etc. and are not the core business operations of the company.

As CFO needs to represent only the operating activities; therefore, these are removed from the cash flow from operations (CFO) calculation and are put under cash inflow from investing activities (CFI).

4) Loss on Sales of Property, Plant & Equipment is added back to CFO whereas it is a loss?

This is a situation exactly opposite of the previous point. In the last point of non-operating income, we had deducted profits on the sale of investments because it was an investment income that has increased the profits. Therefore, to limit CFO only to operating activities, we had to deduct it from CFO. We show these non-operating incomes as inflow under cash flow from investing activities (CFI).

Similarly, the “loss on sales of property, plant & equipment” of ₹1.90 lakh is an investing item that has reduced the profits. Therefore, to limit CFO only to operating activities, we add it back to CFO.

Let us now see the adjustments done for working capital. First, let us understand the “Adjustments for (Increase)/Decrease in Operating Assets”:

5) Current assets like inventory, trade receivables and short-term loans & advances are added in the CFO of Paushak Ltd.

To understand the impact of current assets like inventory, trade receivables, and loans & advances on CFO and to understand when they are added and when they are deducted from CFO, we need to study it alongside changes in these items in the balance sheet. Let us see the current assets section of the FY2020 balance sheet of Paushak Ltd.

FY2020 annual report, page 54:

5.1) Inventories:

An investor notices that in FY2020, the inventories of the company have declined by ₹1.64 cr. It means that in FY2020, the company sold goods by using its existing inventories and received cash for the same. Therefore, a reduction in the inventories is a cash inflow and accordingly, ₹1.64 cr has been added in the calculation of CFO for FY2020.

If during FY2020, Paushak Ltd would have had an increase in inventories that would mean that the company bought and stored inventories. It would have led to cash outflow to purchase this excess inventory. Therefore, we would have deducted the increase in inventory as a cash outflow from the profits to calculate CFO.

5.2) Trade receivables:

An investor would notice that the trade receivables of Paushak Ltd have declined by ₹6.29 cr in FY2020. It means that during the year, the company collected money from its customers. Therefore, a reduction in the trade receivables is a cash inflow and accordingly, ₹6.40 cr has been added in the calculation of CFO for FY2020.

If during FY2020, Paushak Ltd would have had an increase in trade receivables that would mean that more money of the company is now stuck at the end of the customers, which is effectively a cash outflow. Therefore, we would have deducted the increase in trade receivables as a cash outflow from the profits to calculate CFO.

5.3) Short-term loans & advances and other similar items:

An investor notices that other current assets for Paushak Ltd have declined by ₹1.02 cr in FY2020, which is shown as a cash inflow in the CFO calculation. An investor would appreciate that a reduction in the assets is a cash inflow e.g. the company sells an asset and receives money for it.

If during FY2020, Paushak Ltd would have had an increase in other current assets or other similar items that would mean that it spent money to buy those assets, which is a cash outflow. Therefore, we would have deducted the increase in other current assets or other similar items as a cash outflow from the profits to calculate CFO.

An investor may read our complete analysis of Paushak Ltd in the following article: Analysis: Paushak Ltd

Let us move to the other major adjustment section for working capital changes. Now, let us understand the “Adjustments for (Increase)/Decrease in Operating Liabilities:”:

6) How to adjust for changes in trade payables, other current liabilities, provisions etc:

In the calculation of CFO for Paushak Ltd, trade payables of ₹2.98 cr are added and other current liabilities of ₹1.42 cr are deducted from the profits.

To understand the impact of current liabilities like trade payables and other current liabilities and other similar items on CFO and to understand when they are added and when they are deducted from CFO, we need to study it alongside changes in these items in the balance sheet. Let us see the current liabilities section of the FY2020 balance sheet of Paushak Ltd.

6.1) Trade payables:

An investor would notice that the trade payables of Paushak Ltd have increased by ₹2.96 cr in FY2020. It means that during the year, the company could get more goods from its suppliers for which it has not yet paid. It has effectively deferred/delayed payment for the goods to the future. While calculating cash flow changes in the indirect method that we are studying now, a payment deferred in future is considered as a cash inflow. Therefore, the increase in trade payables is added to the profits when we calculate the CFO.

The better way to understand the impact of trade payables on CFO is to look for the case where trade payables have declined during the year. If during FY2020, Paushak Ltd would have had a decrease in trade payables that would have meant that it had made payments to its suppliers. That means a cash outflow would have taken place. Therefore, we would have deducted the decrease in trade payables as a cash outflow from the profits to calculate CFO. Inversing this logic is an easy way to understand why we add an increase in trade payables as an inflow in CFO. Because, if a decrease in trade payables is a cash outflow, then an increase in trade payables is naturally a cash inflow.

6.2) Other Current Liabilities and other similar items:

An investor notices that other current liabilities for Paushak Ltd have declined by ₹1.42 cr in FY2020, which is shown as a cash outflow in the CFO calculation. An investor would appreciate that a reduction in the liabilities is a cash outflow e.g. the company settles a liability/a loan etc by making cash payments.

If during FY2020, Paushak Ltd would have had an increase in other current liabilities or other similar items that would mean that it has received money leading to an increase in the liabilities like a loan, which is a cash inflow. Therefore, we would have added the increase in other current liabilities or other similar items as a cash inflow in the profits to calculate CFO.

6.3) Provisions are added and deducted in CFO: whereas these are a non-cash expense.

While calculating the CFO for Paushak Ltd, in FY2020, short-term provisions of ₹3.53 lakh are deduced and long-term provisions of ₹43.92 lakh are added to the profits.

Provisions are a non-cash expense, where a company believes that it might have to pay something in future and therefore it recognises those expenses in P&L today itself. The cash outflow might not have happened in the current year. Therefore, just like in the case of depreciation, provisions, which are non-cash expenses, are added back to derive cash flow from operations (CFO) from PBT.

Moreover, to understand how changes in the provisions in the balance sheet impact the calculations of CFO, an investor needs to treat their changes just like current liabilities. If the provisions have increased, then it is a cash inflow in the CFO calculation just like trade payables and if the provisions have declined, then it is an outflow.

7) Income tax outflow:

The outflow of the income tax shown in the cash flow statement is the actual cash payment done by the company to the income tax department for its tax liabilities during the year.

An investor should appreciate that the tax payment shown in the cash flow statement may be different from the tax expense shown by the company in the P&L statement. This is because the tax expense in the P&L is prepared as per the Companies Act whereas the tax payment to the income department shown in the CFO calculations is paid as per the Income Tax Act. At any point in time, the Companies Act and Income Tax Act may treat different income and expenses differently. This creates deferred tax assets (DTA) and deferred tax liabilities (DTL).

To give a small example, the Companies Act under IndAS may ask the companies to include unrealized gains on their financial investments in the year as gains in the P&L and calculate tax expense accordingly. Whereas the Income Tax Dept may not demand a tax on the investments until they are sold and the gains are realized by the company. Therefore, during such a year, the tax expense in the P&L would be higher as unrealized gains on investments are included in the PBT whereas the tax paid to IT dept would be lower as the company needs to make tax payment only when the investments are sold and gains are realized in the future. This situation will create a deferred tax liability for the company.

An investor may read the following article to understand more about deferred taxes and how they are calculated: Deferred Tax Assets, Tax Payout (P&L vs. CFO): Queries Answered

Important note about the mismatch in the figures derived from the balance sheet and the figures in the cash flow statement:

In routine business, there are many transactions, which require subjective assessment whether they fall under operating or investing or financing, or under the current or non-current section. Therefore, investors would find that many times, the data derived from the changes in the balance sheet will only approximately match the figures in the cash flow statement. In case, the difference is large, then the investor may contact the company directly for clarifications.

Hope it answers your queries.

Also Read: How Companies Manipulate Cash Flow from Operating Activities (CFO)

All the best for your investing journey!

Regards

Dr. Vijay Malik

What does a negative cash flow from operations (CFO) mean?

Sir, what does a negative number in cash flow mean, under the head ‘cash from operations’? I read in your articles that one must compare PAT and Cash from operations of a company for the last 10 years and see that the difference is not much. However, for many companies, I have noticed that the number of cash from operations is negative for a few years (3 or 4 years out of 10). Why would that be and is it good or Bad?

Is it that these companies have invested in some capital expenditure (CAPEX) etc. and used internal accruals for the same? But that would still not impact ‘cash flow from operations’ right?

Author’s Response:

Hi Sunny,

Thanks for writing to me!

A negative number in CFO means that the company did not make cash from operations and on the contrary, it used up cash from other sources like investing (sale of assets) and financing (debt or equity) to meet its operating requirements.

To understand this relationship, I would suggest you read the cash flow statement in the annual report of any company, which would show step by step calculation of CFO from PAT/PBT.

This calculation would clearly show how the profits/funds get stuck in or get released working capital and the impact of depreciation. It would be a good learning exercise for you to understand in which cases PAT would be higher than CFO and in which cases it would be lower.

In case after reading and analysing the cash flow calculation of the company from its annual report, you have any query, then I would be happy to provide my inputs on your analysis and query resolution.

All the best for your investing journey!

Regards,

Vijay

Comparing cumulative cash flow from operations (cCFO) vs cumulative net profits (cPAT)

I tried to work on your suggestions but still, I have some confusion. Please help me in understanding the ratios below.

My queries are as below.

- CFO is always higher than the net profit in normal cases. Is it correct? When we calculate CFO, we add amortization, depreciation and finance cost with PBT. But when we calculate net profit, we subtract amortization, depreciation and finance cost.

- CFO lower than net profit means that cash is getting struck in working capital (inventory or trade receivables) and in some cases, higher payables may also reduce the CFO of the year. Am I correct?

- See the example of GSFC. Cumulative (10 Years) CFO is ₹4,367Cr and cumulative net profit ₹4,406Cr but still receivable are also high at ₹3,308Cr. How to relate all three in this case? Debtor days also very high.

Author’s Response

Hi,

Thanks for writing to us! It’s very pleasing that you are doing the hard work of interpreting the cash flow statement.

- It is right that normally CFO should be higher than PAT and it’s because of the reasons cited by you.

- It is right that CFO can be lower than PAT due to either working capital related factors or also due to high non-operating/other income, which would form part of CFI (dividend income etc.)

- As we have discussed CFO vs PAT for a single year, the same is true for 10 year period as well. In 10 years, the increase in receivables would reduce the CFO whereas cumulative depreciation/amortization and finance cost will increase the CFO. Rest for the real reasons, one would have to analyse the cash flow statements from the annual reports of each of the last 10 years and one would get to know the exact factors leading to a certain level of CFO.

Further reading: How to do Financial Analysis of Companies

Hope it answers your concerns.

All the best for your investing journey!

Regards

Dr. Vijay Malik

Related Query

Sir, I have been following your website since long and based on that, I feel this is one of the best websites for learning the intricacies of stock-picking. No other website matches the quality of this website. I would like to thank you for creating this masterpiece.

On another note, if for a stock, the other income is considerably high, then there are some chances of cumulative cash flow from operations (cCFO) being lesser than cumulative net profit after tax (cPAT). In those cases, what we should do to make sure that the company is not manipulating its P&L.

Please advise.

Thank you and best regards

Author’s Response

Hi,

Thanks for your feedback! We are happy that you found the articles useful!

We appreciate that you are spending time and effort to understand the cash flow dynamics of companies, which is an important tool to understand the investability of any company.

You are right that in the case of high other income, the CFO can be lower than the PAT. Such kind of assessment would indicate to an investor the ability of the company to generate a cash flow, which is sufficient to meet the fund’s requirements like capital expenditure (capex) or debt servicing etc.

Once an investor is able to identify that the CFO is lower due to other income, then she can take a case-specific investment decision depending upon the nature & amount of non-operating income as well as the nature and amount of funding requirements like capex or debt servicing etc.

Such decisions need to be taken on a case by case basis and there would not be any specific guideline applicable to all the cases.

Further reading: 7 Steps to Find out whether a Company is Cooking its Books

Hope it answers your concerns.

All the best for your investing journey!

Regards

Dr. Vijay Malik

Related Query: Why we compare CFO with PAT and not with Sales Revenue

Hello Vijay,

I know it is a very basic question but could you please explain to me:

Why we are considering CFO vs PAT? Why not Sales vs the money received from a customer?

We receive money from a customer against our sales not against profit then why we are comparing PAT vs CFO?

What is CFO?

As per your statement, the money is received from a customer, which means that we receive money against our sales then why we are comparing PAT that is only the profit.

I know I am confused a lot so please explain me to calculate CFO.

Also please explain, suppose the company sold 1000 INR worth of product but the company has not received the amount from the customer, is it still included in operating profit and net profit?

Thank you for your help and knowledge sharing.

Author’s Response:

Hi,

Thanks for writing to me!

We compare CFO to PAT, as the CFO just like PAT is after deduction of all the expenses incurred to earn the profits like the cost of raw material, employee salaries, advertisement expenses, fuel expenses etc. You can notice in CFO calculation in any annual report that it is calculated from PAT/PBT.

Read: Understanding the Annual Report of a Company

Comparing CFO to Sales would be comparing apples to oranges.

Hope it helps in the resolution of your query!

Regards,

Vijay

Readers’ Queries about Cash Flow from Operating Activities (CFO)

Can we compare cumulative EBITDA (instead of cumulative PAT) with cumulative CFO to decide whether a company is converting its profits into cash?

Dear Vijay,

I have one question related to comparing cumulative cash flow from operations (cCFO) to cumulative net profit after tax (cPAT). Consider a small company that operates in cash only and has only one asset, which is depreciating every year. Then, in this case, cPAT will always remain lower than cCFO. I believe that it will misguide the comparison. Because there are few other non-operating expenses that would always keep this difference. Here the company did not require any cash as its dealing in cash only.

My question is how can you remove this variance in order to compare cCFO to cPAT?

Below is a snapshot of an example I am talking about. Here, the company’s cash is increasing and does not require any loans to fund its growth. However, if we go through the comparison of cPAT vs cCFO, then we could conclude that the company is bad at converting their profit into cash. However, it is 100% converting its PAT into cash.

One correction in the above pic is for year 2 the CFO is 5 and not 10 and cCFO will be 15 and even net profit is -15 for year 1 and cPAT will be -25.

This is a simple example. Here, I have assumed that the company does the same-day purchase and sales. Therefore, there is no credit purchase or credit sales. Hence, the company is accumulating cash as it can be seen from the year-to-year comparison. However, the depreciation is higher and hence resulting in a net loss. This is all that I have assumed.

Therefore, my query is how to avoid such situations as there could be multiple scenarios where this could happen like finance expenses etc. I hope you got my query.

Well, my point here is simply that comparing cPAT with cCFO will not yield any conclusive evidence whether the company has been able to convert its profit into cash. An investor needs to deep dive into it.

Secondly, I have also assumed in my example that the plant was purchased and in the same year, operations were started. Therefore, on an overall basis, this company would never match cPAT with cCFO.

Therefore, can we instead compare cumulative earnings before interest, tax, depreciation & amortization (cEBITDA) to cCFO as this would be a better view I believe?

If you apply this concept in my example, then you will come to know that the company has been converting its profit fully into cash.

Let me know if you agree with me.

Author’s Response:

Hi,

Thanks for writing to us and elaborating on your query with clarifications.

In the case cited by you, the cumulative cash flow from operations (cCFO) will be higher than the cumulative net profit after tax (cPAT). The reason for the same is high depreciation, which has resulted in net losses. You may read further about the factors that may lead to CFO higher than PAT and the factors that may lead to CFO lower than PAT in the current article, which shows the step-by-step calculation of CFO from PAT.

We believe that an investor should always keep in mind that an investment decision is a result of a comprehensive analysis that includes an assessment of PAT as well as CFO. An investor should not be biased by good performance on either PAT or CFO alone. A company should have a good performance on PAT and the PAT should have been converted into CFO.

Regarding PAT being negative due to depreciation, an investor should remember that the depreciation is nothing but the deferred recognition of expenses done by the company on plant & machinery. The company spent money on plant & machinery in the past but it did not deduct these expenses in the profit & loss statement (P&L) as an expense when it constructed the plant.

Therefore, in a manner, in the past, when the company was spending to construct the plant, its profits were overstated because the money spent was not deducted as an expense. Whereas now, when the plant is complete, the profits are understated because the prior expense of plant creation is being deducted as depreciation even though there is no current cash outflow due to plant creation.

However, this is how the concept of capitalization operates. You may read more about how investors should understand capitalization in the following article: Understand the Capitalization of Interest and Other Expenses

As mentioned earlier, we do not attempt to take our final investment decision by looking at CFO alone and therefore, we would request investors to look at PAT, CFO as well as all other parameters of the following checklist before making any final investment decision about any company: Final Checklist for Buying Stocks

Moreover, investing & finance allows investors to use their preferred ratios and even tweak them to make their own custom ratios. We advise investors to keep experimenting with different ratios and use the ones, which they find to give good results. At end of the day, none of these ratios is an end in themselves.

As mentioned earlier in the case of PAT and CFO, in case of EBITDA vs CFO as well there are challenges like those that EBITDA is a pre-tax number and CFO is a post-tax number.

Therefore, we advise readers to use the ratios that they feel comfortable about and more importantly do not overly focus on any one ratio. A comprehensive analysis of all the aspects is important before taking a final investment decision.

Selecting Top Stocks to Buy – A Step by Step Process of Finding Multibagger Stocks

All the best for your investing journey!

Dr. Vijay Malik

How to calculate changes in trade receivables/payables for the cash flow statement?

Dear Doctor,

I have a doubt on Fund Flow Analysis. While analyzing the balance sheet with respect to the cash flow statement, the amount seems to be a bit different. Could you please assist me?

The change in the trade receivables, as well as trade payables in the balance sheet, is many times different from the changes mentioned in the cash flow statement.

Regards,

Author’s Response:

Hi,

Thanks for writing to us!

In the cash flow statement, many times, companies club the trade receivables and trade payables with certain other items under current assets and current liabilities respectively. Therefore, many times, investors would notice that the figures for changes in only “Trade receivables” and “Trade Payables” are not matching with the figures in the cash flow statement.

Moreover, you would notice that in the cash flow statement, the companies have started labelling these items as “Trade and other receivables” and “Trade and other payables”.

In the “Trade and other receivables”, most of the times, the items under “Short-term loans & advances” (STLA) are clubbed. You may go through the details of the items under “Short-term loans & advances” (excluding the changes in the tax-related items under STLA) and try to club their changes with trade receivables and in most of the cases, you would be able to approximate/tally it with the figures in the cash flow statement.

Similarly, in the case of “Trade and other payables”, many times, companies club other items under current liabilities, especially from section “Other current liabilities” and provisions along with trade payables. Therefore, there are differences in the changes in the “Trade payables” in the balance sheet and the cash flow statement. You may study the items under “Other current liabilities” and “provisions” and see their changes. They will provide you with an explanation for the differences observed by you.

Hope it will resolve your queries.

All the best for your investing journey!

Regards,

Dr. Vijay Malik

Can companies arbitrarily add depreciation in CFO calculation to inflate CFO?

Hi Sir,

I have a general query.

In cash flow from operations (CFO), we know that we have to add back the depreciation to know the cash flow. However, I saw cases where some companies arbitrarily add a huge amount of depreciation, which misleads the actual net cash flow from operations.

Sir, how can we assess the actual depreciation and at which level?

Regards,

Author’s Response:

Hi,

Thanks for writing to us!

An investor may get further details about the amount of depreciation by reading:

- The detailed schedule to financial statements contains details of fixed assets in the annual report.

- Moreover, the companies also disclose the assumption of life of different assets in the “key accounting policies” section in the annual report.

An investor may get a little bit more insights about the depreciation from combining the learning from the above two sections of the annual report. However, if still investor has doubts about the amount of depreciation, then she may contact the company directly for clarifications.

Advised reading: How should investors contact Companies/Management for clarifications or additional information?

All the best for your investing journey!

Regards,

Dr. Vijay Malik

Can Dividend & Interest Income be a part of cash flow from operations (CFO) instead of cash flow from investing (CFI)?

Hello Sir,

Recently I am reading a book, Creative Cash Flow Reporting by Charles W Mulford. On page: 15, it states that

Any income generated by those investments, such as cash revenue less cash expenses on investments in property, plant, and equipment, interest income on investments in debt securities, or dividend income on investments in equity securities, is included in the calculation of operating cash flow

We have learnt so far that any dividend income on investment is considered in Cash flow from investing (CFI), but this book contradicts here.

Kindly suggest.

Author’s Response:

Hi,

Thanks for writing to us!

As rightly mentioned by you, our understanding is the same that dividend income, interest income etc. are non-operating income and therefore, excluded while calculating cash flow from operations (CFO). Such income is included in cash flow from investing (CFI).

The only situation where such income (dividend and income) are included in CFO is for the companies whose main business is making investments like investment funds/NBFCs etc. This is because dividend and interest income is the operating revenue for them.

We do not have any views on why the said book has mentioned that dividend and interest income are included in CFO. You may read more about this topic in the said book. Probably reading more will provide you with the context in which the author has made this statement.

All the best for your investing journey!

Regards

Dr. Vijay Malik

Treatment of Profits from the sale of investment in Cash Flow from Operations

Hi,

I am trying to discuss Krishna Kumar’s question in the following article: Readers’ Queries: DHFL, KRBL, HMVL, Shilpi Cables & Others

(I may be completely wrong here because I am from non-finance background and hence have very limited knowledge.)

The way I would reason why interest and depreciation are added back is something like this:

- First, the company earns operating profit (OP).

- From that, they set aside money for meeting debt obligations (interest and principal repayments), money for replacing machinery (depreciation- I have oversimplified it a lot here), taxes, dividends and any others.

- So CFO should be ideally close to OP. if you look at the Cash Flow statement, CFO starts with adding back things to PBT. (I guess the P/L, BS and CF statements follow some accounting standards and that is what tweaks the picture a lot. Again I am guessing the auditing guys use some ledger entries to decide where each entry should go like CFO or CFF).

- The part that always trips me is fixed assets and investments. For e.g. look at the Cash flow statement of MUL in this article. Sale of Fixed assets: there is one entry that goes into CFO and one goes into CFF. Same is the case for Interest income which appears once in CFO and once in CFF. (The nature of the expense as differentiated by ledger entries decides which fixed assets go where? I don’t know. )

The way I look at CFO is: I try to see how close or far CFO is from OP. Again I am just a beginner, so you can completely ignore my reasoning

Author’s Response:

Hi,

Thanks for sharing your valuable inputs. I appreciate the time and effort spent by you while sharing your feedback with the readers and the author.

If you notice that in MUL’s cash flow statement, the sale of investments is shown as part of CFO as well as CFI. The reason is that profit from the sale of investments has been included in the calculation of PAT, whereas the sale of investment is not an operating activity, therefore, this profit has been deducted (negative entry) from PAT while arriving at CFO. As sale or purchase of investments is investing activity, the entire sum received from the sale of investment is shown as part of inflow (positive entry) under CFI.

Similarly, income from interest on the investments, which is included in the PAT, has been deducted to arrive at CFO as the interest income is not an operating income but an investment income. The same has been included in the CFI segment as a positive entry.

Hope it clarifies your query.

All the best for your investing journey!

Regards,

Vijay

Treatment of financial / interest expenses in cash flow statement

Read: Analysis – Premco Global Limited

Dear Dr. Vijay,

Thank you so much for all the wonderful analysis and in fact the whole website. I have learnt more in the last week reading your blog than what I learnt (and apply) during MBA days. I have read most of the articles and now feel much more confident in stock investing. My perspective has changed totally. For instance, Premco has been on my radar for many months now. I watch the stock price every week to see when I can buy it. Now, I have done a detailed analysis and feel much more confident in my decision.

I have one question on Premco Global.

I noticed in the cash flow statement, they have a line item called “Financial Expenses.” This particular line item appears both in CFO (as a positive figure) and CFF (as a negative figure). They have been consistently doing this from the beginning. Mathematically, it seems like the nullifying effect.

Just wanted to make sure this is not some accounting gimmick. I want to understand if this is “conceptually” correct. This reconciles correctly in the P&L as Finance expenses, though. So wanted to get your views.

Many thanks again for all your efforts.

Author’s Response:

Hi,

Thanks for your feedback & appreciation! I am happy that you found the articles useful!

Financial charges pertain to financial activities, therefore, these pertain to cash flow from financing activities (CFF). An investor would appreciate that companies need to deduct financial charges from profits before arriving at a net profit after tax (PAT).

As a result, while calculating cash flow from operations (CFO) from PAT/PBT, financial charges are added back to PAT (positive entry) and are deducted from CFF (outflow/negative entry) to classify them correctly in the cash flow statement.

Read: Understanding the Annual Report Of A Company

Hope this clarifies your query!

Regards,

Vijay

Can inventory losses (write-down) lead to inflated cash flow from operations (CFO)?

Hello sir,

I understand that while calculating cash flow from operations (CFO), we adjust for the working capital (WC) changes to arrive at CFO.

While analysing the CFO calculation of a commodity type business, I saw that the changes in the inventory led to the addition of a large amount of inflow in CFO and thus heavily inflated the CFO.

The company in question uses commodity as raw material (RM). The raw material/inventory was valued at very high prices last financial year inventory closing as the commodity was at its cyclical peak. However, in the recent year commodity prices has corrected to very lows (recent year inventory values). Therefore, the value of inventory at the end of the year has come down significantly. I understand that while adjusting for the working capital in CFO calculation, the reduction in the value of inventory on the balance sheet during a year is shown as cash inflow.

Therefore, I feel that the losses in the inventory held by the company due to a decline in the price of the commodity have the potential of inflating the CFO.

So while analysing the fund flow analysis from the balance sheet or cash flow analysis, how should we consider such changes, which may not be real?

Author’s Response:

Hi,

Thanks for writing to us!

We believe that in such cases of inventory write-down only a case to case based awareness is sufficient for investors and no change to the general method of CFO calculation is needed.

Let us see the impacts on both the balance sheet fund flow analysis as well as the cash flow from operations (CFO) calculation in the case of inventory write-down.

1) Calculation of cash flow from operations (CFO):

The positive entry of change in inventory in the CFO calculation under working capital changes nullifies the impact of loss recognised in the P&L due to inventory write down. This positive entry in CFO does not inflate CFO but cancels out the impact of reduction from loss due to inventory write-down in the profits.

If we do not add the positive change due to reduction of inventory in CFO, then the CFO will be unduly reduced from inventory write-down losses (which is a non-cash item).

2) Fund flow analysis from the balance sheet:

The decline in inventory will be factored in profit & loss statement as a loss/expense, which will reduce the profits and in turn will reduce the retained earnings (shareholders equity).

If we ignore all other transactions, then in the fund flow analysis, the fund inflow due to decline in the asset (inventory) will be matched with fund outflow due to decline in shareholders’ equity (reduction in retained earnings due to loss in P&L because of inventory write down).

Hope it answers your queries.

All the best for your investing journey!

Regards

Dr. Vijay Malik

Why is the amount of dividend declared in a financial year shown in the director’s report section different than the amount of dividend payment shown as an outflow in the cash flow statement?

Hi Dr Vijay,

Trust you are doing great.

I have a doubt regarding a company that I am analysing.

In a particular year (FY2005), this company’s director’s report mentioned that they declared a dividend of ₹1/share on 30 lac shares It means an outflow of ₹34 lacs including dividend distribution tax (DDT). However, the same year’s cash flow statement shows only an outflow for dividend plus DDT of ₹17 lac in the cash flow from financing activities.

How did this difference arise?

In addition, in the next year (FY2006) they declared the same dividend amount and correctly showed an outflow in CFF as ₹34 lacs.

Regards,

Author’s Response:

Hi,

Thanks for writing to us!

The cash flow statement contains the amount of dividend paid in cash during the year. If out of total dividend of ₹ 1, ₹ 0.50 is paid as an interim dividend within the financial year (e.g. FY2005). Moreover, the balance ₹0.50 is declared as a final dividend, which will be paid out in next year i.e. FY2006 after approval in AGM, then the cash flow statement for FY2005 will have cash outflow only for the interim dividend and not for the final dividend.

In the next year i.e. FY2006, the cash flow statement in the cash flow from financing section will contain the outflow for the final dividend of FY2005, which is paid after AGM in FY2006 and the outflow for any interim dividend for FY2006, which is declared and paid within FY2006.

Hope it will help.

All the best for your investing journey!

Regards,

Dr. Vijay Malik

Related Query

Sir, I have a query regarding dividend paid out and interest paid.

I came across a situation where the dividend paid out in balanced sheet (reserves and capital Note) and the dividend paid out in cash flow statement (CFF) with a different set of numbers. So, to find out a dividend per share which set of numbers should be used? Similar for interest paid out?

Author’s Response:

Hi,

Thanks for writing to me!

You may find different numbers for the dividend paid out as the number in cash flow statement includes all the dividends paid out during the year, whereas the number in the balance sheet might include only the dividend which remains to be paid out at the balance sheet date (March 31) and for which provisions have been done.

For interest, you should take the number from the cash flow statement as this includes the entire interest outgo during the year. Whereas the number in the P&L is only the amount of interest which is expensed during the year and excludes the interest which is capitalized during the year in the form of fixed assets or WIP. However, it is best to calculate the interest outgo on your own by taking an average of the debt outstanding at the start and the end of the year and by assuming a reasonable applicable rate as many a times companies do not give the actual interest data in either P&L or CF statement.

Read: Understanding the Annual Report Of A Company

Hope it clarifies your queries!

All the best for your investing journey!

Regards

Vijay

Can we find the amount of capital work in progress (CWIP) and the amount of capitalized interest from the cash flow statement?

Dear Sir,

I have two queries:

- While analysing the cash flow statement, how can we find what is the total amount of capital work in progress (CWIP) and where is it adjusted? This is because the capital work in progress might be in form of inventory, plants, etc.

- In addition, if any company is capitalising interest cost, can we find it in the cash flow statement?

Author’s Response:

Hi,

Thanks for writing to us!

Capital work in progress (CWIP) is a part of fixed assets. It constitutes those fixed assets, which are still under construction. Inventory is not classified under CWIP. Please note that the inventory, which is under process is classified under current assets >> inventory >> WIP.

The money spent on CWIP along with fixed assets is shown as an outflow in the cash flow from investing (CFI) under headings similar to: “Purchase of Fixed Assets”.

We have experienced that it is difficult to find out the exact amount of capitalization of interest from the cash flow statement. This is because companies show a lot of capitalized interest as part of outflow under “Purchase of fixed assets” under CFI instead showing it as a part of outflow in “Interest outflow” under cash flow from financing (CFF).

All the best for your investing journey!

Regards

Dr. Vijay Malik

Should we invest in Companies making Cash Losses?

Hi doc,

Today, I saw some scripts which are not good in their fundamentals like

Tata Metaliks Limited. The cash flow from operations (CFO) is negative in multiple years in the last ten year. Same is the case of Asian Granito Limited.

But these companies still manage to give multi-bagger results almost seven times within a year. So imaan dagmagane lagta hai.

Actually, CFO is the main factor to analysis as I have learned from you. So what should I do?

Should I invest in such type of companies, which produce almost nil or negative cash flow from operations (CFO) not only one but multiple in multiple years but still their share price increases multiple times within a year?

Please explain. Thanks

Author’s Response:

Hi,

Thanks for writing to us!

There are multiple approaches used by market participants to decide about the stocks which they would buy or sell. Our approach “Peaceful Investing” is one of such approaches.

If an investor believes that the stocks, which even though they do not have good fundamentals would give her good returns in future, then she can choose to follow her conviction.

However, stocks with weak fundamentals do not fit in our “Peaceful Investing” model and therefore, we tend to avoid them.

Read: Selecting Top Stocks to Buy – A Step by Step Process of Finding Multibagger Stocks

Hope it answers your concerns.

All the best for your investing journey!

Regards

Dr. Vijay Malik

When cash inflow from operations is equal to cash outflow from investing activities

In cash flow, many times we notice that the difference between cash flow from operation and the cash from investing is getting tallied or it is being met from cash flow from financing. Does it mean that the company is using all the cash from operation for investments?

Author’s Response:

Hi,

Thanks for writing to us!

The money is fungible, which means that it might be that finance is being used for investments and operations are being used partly for investment and partly to repay the finance.

Or both operations and finance are being used for investments.

But overall, if CFO inflow and CFF inflow are equal to CFI outflow that would mean that CFI requirements are being met through using both CFO and CFF.

Read: How to do Financial Analysis of Companies

Hope it answers your concerns.

All the best for your investing journey!

Regards

Dr. Vijay Malik

Should we deduct interest payment while calculating CFO?

Hi Dr Vijay,

I learnt from your blog that we should always look Net profit along with CFO.

While looking at the calculation of Cash flow from Operations in annual reports, I observe that interest paid and depreciation are added into the net CFO. I find that CFO in some high debt companies like Suzlon Energy Ltd is much greater than net profit since interest is included in CFO and not in net profit. This could seriously mislead our analysis.

Shouldn’t we remove these from CFO when we are comparing 10-year cPAT and cCFO? – Or, shall we compare (cCFO + tax paid) with cEBITDA.

Regards,

Krishnakumar.

Author’s Response:

Thanks for writing to me!

I am happy that you are doing your own stock analysis and are envisaging different scenarios/ratios/formulas which as per you represent the correct picture of the financial position of the company.

I congratulate you for questioning the set mindset of company analysis.

Krishna, the annual reports are prepared in a standard format as per the accounting rules of any country. Rules dictate that interest should be shown as CFF and not CFO, that’s why it is added back in net profit to arrive at CFO.

However, the analysis in finance by the investor is not bound by any rules. You may use any formula as you deem fit for gauging the correct situation of any company.

I would suggest that you try analysing companies on the tweaked formulas presented by you and take a call whether these new formulas are able to present the actual financial strength or weakness of the company, better than rule-bound CFO.

All the best for your investing journey!

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

This article was originally written and published during the period when I, Vijay Malik, was registered with SEBI as an Investment Adviser. I am currently registered with SEBI as a Research Analyst (Regn. No. INH100008364).

This article is for educational purposes only and should not be construed as investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.

16 thoughts on “Understanding Cash Flow from Operating Activities (CFO)”

If a company takes a loan against a fixed deposit (FD), is the FD amount still a cash asset?

How accounting is done for this?

Dear Sheela,

Thanks for writing to us!

We request you first do an independent search for the answer on Google and then think to come up with your own answer to whether an FD against which a loan is taken should qualify an asset. If yes, then how should simultaneous FD and loan against that FD be shown on the balance sheet?

Thereafter, please elaborate on your learning from such an exercise. We would be happy to provide our input on your line of thought on this issue.

Regards,

Dr Vijay Malik

What does income tax paid as negative mean? Some stocks have income tax paid as positive numbers in CFO. What does it mean?

Dear Sandeep,

We request you to think and provide your views about what one should call payment from Income Tax Dept to the company or an individual.

We request you to search independently and think of different scenarios where the money would flow from Income Tax Department to companies or individuals.

We will be happy to provide our input to your line of thought.

Regards,

Dr Vijay Malik

Oh. Got it, doc. So, basically, CFO is net profit+depreciation and changes in working capital. Is it so?

Dear Sandeep,

Apart from the items mentioned by you, other adjustments are done to arrive at CFO from PAT. The above article captures the step-by-step calculation of CFO from PAT. You may refer to that calculation to understand it further.

Regards,

Dr Vijay Malik

Dear Dr Vijay,

Thank you for your valuable insight on understanding cash flow from operational activities (CFO). I really admire all the hard work you have put forth and sharing the information with everyone.

I’m going through the consolidated balance sheet of “Grasim Industries Ltd” for the year 2018.

Inventories: ₹4,231 cr in 2017 and ₹5,860 cr on 2018

Trade receivables: ₹3,010 cr in 2017 and ₹5,213 cr on 2018

As per my understanding, an increase in inventories and trade receivables is cash outflow and the CFO statement should be adjusted for inventories as ₹1,629 cr (i.e. 5,860 – 4,231) and for trade receivables as ₹2,203 cr (i.e. 5,213 – 3,010).

However, the actual consolidated CFO statement for FY2018 contains inventories of ₹751 cr and trade receivables of ₹765 cr.

I’d highly appreciate it if you can throw some light on this.

Dear Bappa,

Thanks for sharing your feedback.

Bappa, many times, companies group multiple items and then show their impact in the cash flow statement. You may contact the company directly to understand the reasons for these figures. The company would be in the best position to answer why the changes in inventory and trade receivables in the CFO statement are different from the balance sheet data.

Regards,

Dr Vijay Malik

Sir, in many cases, I have seen that income tax deduction in cash flow statement is mismatched with p&l statement and that the gap is quite significant. How can I access this?

Dear Joyjit,

The following article will help you in this regard: Deferred Tax Assets, Tax Payout (P&L vs. CFO): Queries Answered

Regards,

Dr Vijay Malik

Sir, I am analysing Manali Petrochemicals Ltd and I found that the company has an inflow in operating cash flow statement from other current liabilities as 790 crores (decrease in liabilities). However, the company reduced their liabilities by 790 crores. How is it labelled under cash inflow?

Dear Satpal,

In case, an investor believes that the accounting done by any company is not in line with the normal practices, then she may contact the company directly for clarifications.

Regards,

Dr Vijay Malik

Hello Dr,

The cash flow from operations is negative for IRFC and Rail Vikas Nigam Ltd. When I looked up Screener, it says the company must be capitalizing its interest costs. Can this be true? how do I find it out in the balance sheet? In the excel template, only the past four years are available for analysing of few companies which got listed recently, can I depend upon this for analysing?

Thank you.

Dear Sowmiya,

You may the step-by-step calculation of cash flow from operations in the detailed financial statements of these companies in their annual reports. This exercise will help you understand why there CFO is negative. The following article will help you in this exercise: https://www.drvijaymalik.com/understanding-cash-flow-from-operations-cfo/

An investor would find that most of the recently listed companies would have limited data available for their historical performance. It depends on an investor how much data she needs to become confident about her analysis of any company. There is no fixed rule for it.

Regards,

Dr Vijay Malik

Hi Sir,

I have started learning market terminology from drvijaymalik.com. It is really nice content.

1. I have doubt in the below paragraph where you have mentioned that trade receivable declined by 6.29 Cr but mentioned the inflow as 6.40 Cr. Why additional 0.11 Cr in the inflow.

2. Does negative payable means that the company has paid an advance amount to its vendors?

“An investor would notice that the trade receivables of Paushak Ltd have declined by ₹6.29 cr in FY2020. It means that during the year, the company collected money from its customers. Therefore, a reduction in the trade receivables is a cash inflow and accordingly, ₹6.40 cr has been added in the calculation of CFO for FY2020.”

Dear Sonal,

1) Many times, the data between the balance sheet, profit & loss statement and cash flow statements do not show an exact match. It may be due to some assumptions, different grouping of expenses etc. We are ok if we can get approximate figures. An investor may contact the company directly for clarifications to get exact matching or for differences like the one highlighted by you.

2) Regarding negative payables, we would request you to do an independent search for an answer and then elaborate on your learning. We will be happy to provide our inputs to your line of thought.

Regards,

Dr Vijay Malik