The current section of the “Analysis” series covers Lloyds Metals and Energy Ltd, jointly controlled by Mr B.L. Agarwal’s family and the Thriveni group. The company owns an iron ore mine and sponge iron plant in Naxal-affected areas of Maharashtra; Chandrapur and Gadchiroli districts.

The “Analysis” series is an attempt to share with all the readers, our inputs to the company analysis submitted by readers on the “Ask Your Queries” section of our website.

Please note that to benefit the maximum from this article; an investor should focus on the process of analysis instead of looking for good or bad aspects of the company. She should learn the interpretation of different types of data and transactions and pay attention to the parts of annual reports etc. used to get the information. This will help her in improving her stock analysis skills.

Lloyds Metals and Energy Ltd: Detailed Fundamental Analysis

On different occasions in the past, Lloyds Metals and Energy Ltd has created child entities (subsidiaries, joint ventures etc.). As a result, at times, it has published standalone as well as consolidated financials.

On Dec 31, 2022, the company had a joint venture (JV) company, Thriveni Lloyds Mining Private Limited with the Thriveni group. It formed the JV with the Thriveni group in FY2021 when the Thriveni group acquired equal promoter rights from the B.L. Agarwal family by infusing about ₹200 cr in the company.

FY2021 annual report, page 27:

pursuant to this MOU the Thriveni Earthmovers Private Limited and Lloyds Metals and Energy Limited has incorporated a Joint Venture Company namely “Thriveni Lloyds Mining Private Limited” on 28th May, 2020 in the ratio of 60:40, for doing Mining Operations only

As a result, of this JV, in recent times, Lloyds Metals and Energy Ltd started publishing consolidated financials from FY2021 onwards. Previously, the company had started publishing consolidated financials in FY2005 when it formed a wholly owned subsidiary (WOS) company, Gadchiroli Metals & Minerals Limited.

FY2005 annual report, page 6:

During the year, Company has floated a wholly owned subsidiary M/s. Gadchiroli Metals & Minerals Limited with a share capital of Rs. 10 Lacs.

However, from FY2014, it stopped publishing consolidated financials because Gadchiroli Metals & Minerals Limited did not remain its wholly owned subsidiary as the stake of Lloyds Metals and Energy Ltd was diluted when the subsidiary raised money from other parties.

FY2014 annual report, page 8:

M/s. Gadchiroli Metals and Minerals Limited, ceased to be wholly owned subsidiary of the Company due to dilution of shareholding during the year under review.

We believe that while analysing any company, an investor should always look at the company as a whole and focus on financials, which represent the business picture of the entire company including its subsidiaries, joint ventures etc. Consolidated financials of a company present such a picture. Therefore, if a company reports both standalone as well as consolidated financials, then in such a case, it is advised that the investor should prefer the analysis of the consolidated financials of the company, whenever they are present.

Therefore, while analysing the past financial performance of Lloyds Metals and Energy Ltd, we have analysed standalone financials until FY2004, consolidated financials from FY2005 to FY2013, standalone financials from FY2014 to FY2020 and again consolidated financials from FY2021 onwards.

Further advised reading: Standalone vs Consolidated Financials: A Complete Guide

With this background, let us analyse the financial performance of Lloyds Metals and Energy Ltd.

Financial and Business Analysis of Lloyds Metals and Energy Ltd:

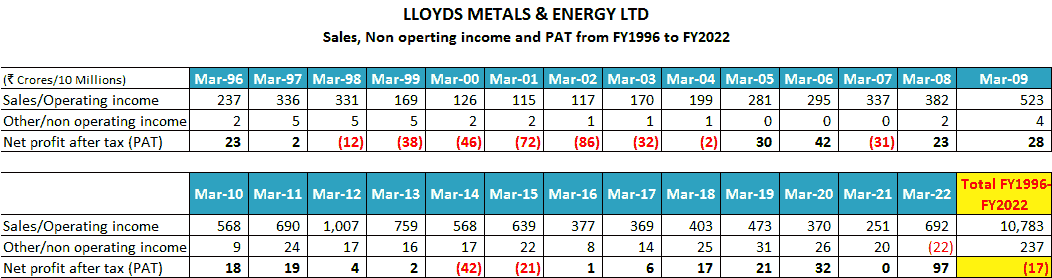

In the last 10 years (FY2013-FY2022), the sales of Lloyds Metals and Energy Ltd have declined from ₹759 cr in FY2013 to ₹692 cr in FY2022. The long-term decline in performance looks even sharper when looked at in the context of sales of ₹251 cr achieved by the company in FY2021, which is about 67% down from the sales of FY2013.

After FY2021, the company has been growing very fast. In FY2022, it reported sales of ₹692 cr, which is a growth of 175% over FY2021. In the last 12 months ending Dec. 2022 (i.e. Jan. 2022 to Dec. 2022), the company reported sales of ₹2,849 cr, which is a very significant growth.

However, if an investor looks at the financial performance of Lloyds Metals and Energy Ltd from FY1996 onwards, then she comes across an entirely different story. The performance of the company has been highly erratic.

The below table contains the data of sales, non-operating income and profit after tax (PAT) of Lloyds Metals and Energy Ltd from FY1996 to FY2022.

The first thing that an investor notices is that over the last 27 years (FY1996-FY2022), on a cumulative basis, the company has lost money because; over this period, it has reported a cumulative loss after tax of ₹17 cr. This is despite reporting sales of ₹10,783 cr over these 27 years.

Moreover, the business performance of Lloyds Metals and Energy Ltd had been highly volatile. From FY1998 to FY2004, the company reported losses for 7 consecutive years.

The sales of the company have been highly fluctuating. Sales reached a peak in FY1997 at ₹336 cr and thereafter started declining consistently. Sales bottomed out after declining 66% at ₹115 cr in FY2001 and then started increasing. Subsequently, sales peaked at ₹1,007 cr in FY2012. However, once again sales started declining and bottomed out after declining more than 75% at ₹251 cr in FY2021.

The sales of Lloyds Metals and Energy Ltd in FY2021, ₹251 cr were less than its sales of ₹336 cr achieved almost 25 years back in FY1997.

To understand the reasons for such a financial performance of Lloyds Metals and Energy Ltd, an investor needs to read the publicly available documents of the company like its annual reports from FY1997 onwards, credit rating reports by Brickwork, corporate announcements as well as other public documents. Then she would understand the factors leading to a highly fluctuating business performance along with the recent-most sharp improvement.

The above-mentioned documents indicate that the following key factors influence the business of Lloyds Metals and Energy Ltd, which are critical to understand for any investor analysing the company.

1) Major contributions from Iron ore mining operations:

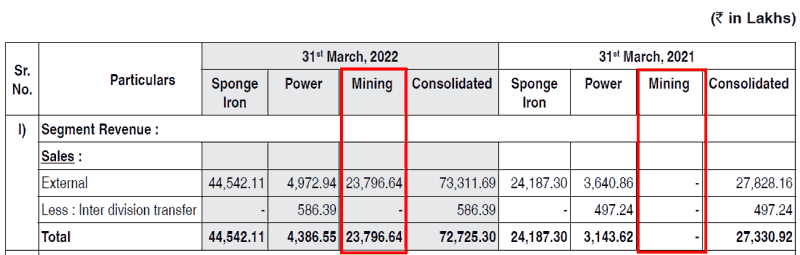

Sponge iron, power production and mining operations are the main revenue segments of Lloyds Metals and Energy Ltd. Out of these, the recent sharp increase in the business performance of the company is primarily due to a significant increase in revenue from its mining operations.

In FY2022, the company reported sales of about ₹238 cr from mining, which was nil in the previous year.

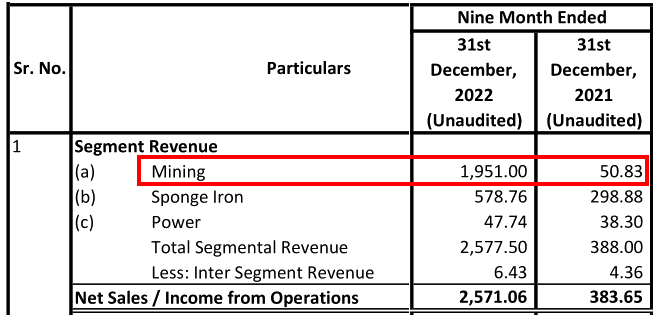

The same pattern in continuing in FY2023 as well. In 9M-FY2023 financials, the mining operations contributed ₹1,951 cr whereas, in 9M-FY2022, mining operations contributed ₹51 cr to sales.

The increasing size of the mining operations of the company has helped it on two fronts.

First, it is able to source all its iron ore requirements for sponge iron production from its own mine, which has significantly reduced its iron ore costs by up to 50% from earlier ₹7,000 per MT to now ₹3,000-3,500 per MT. It has led to a high-profit margin in sponge iron operations.

Credit rating report by Brickwork, August 2021, pages 2-3:

reduction in iron ore cost from Rs. 7000 per tonne to Rs. 3000~Rs. 3500 per tonne leading to healthy profitability of the company.

FY2022 annual report, page 39:

On account of captive consumption, the cost of sourcing raw material has come down leading to an increase of profitability of the Company.

In order to use more of its captive iron ore in-house, the company has announced major capacity expansions for manufacturing steel products.

Second, its iron ore production approval of 3 million tonnes per annum is much higher than its own requirement of about 0.5 million tonnes, until now. As a result, Lloyds Metals and Energy Ltd sells most of its iron ore production to other buyers.

Credit rating report by Brickwork, August 2021, page 3:

iron ore requirement for the company is around 0.50 million tonnes per annum hence any surplus iron ore production will be available for sale to third parties.

FY2022 annual report, page 14:

The Company could mine 2.9 million tons in 6 months of operation against an allowed capacity of 3 million tons per annum.

Selling iron ore in the open market is a highly profitable business because companies just need to dig the ore out from the earth and sell it without any value addition. The key factor leading to high-profit margins in this low-value-adding business is the license for mining.

It is difficult to get a mining license and at times, the steel industry has to face a shortage of iron ore e.g. in FY2021.

FY2021 annual report, page 46:

acute shortage of iron ore is prevailing due to the cancellation of the iron ore mines in March, 2020 and subsequent reduction in mining activities from the 19 auctioned mines in Odisha

Due to these regulatory hurdles, anyone who gets a license to mine iron ore can earn high-profit margins from digging the ore and selling it. In light of the same, it comes as no surprise to the investor that companies like NMDC Ltd, which rely primarily on iron ore mining enjoy operating profit margins of 50% to 70%.

Therefore, an increasing contribution of iron ore mining operations during FY2022 and FY2023 has led to a significant increase in the profit margins of Lloyds Metals and Energy Ltd from 4% in FY2021 (with nil mining sales) to 21% in FY2022 and 27% in 9M-FY2023.

1.1) Mining operations face a lot of uncertainty:

Mining operations are the mainstay of significant improvement in the performance of Lloyds Metals and Energy Ltd in recent years. The company tied up with Thriveni group, which is the largest mining operator in India for its iron ore mine. The decision seems to have worked well for the company because even during the rainy season, the mine could produce at near full capacity.

Q2-FY2023 results presentation, page 6:

Despite monsoons, the production run rate remained unaffected, indicating strong operational controls due to sufficient infrastructure in place.

However, if an investor takes a comprehensive view of the long-term history of the mining operations of Lloyds Metals and Energy Ltd, then she notices that its mining operations have faced many issues beyond simple operation matters. These are issues related to security threats, Naxals, regulators, approvals, litigations etc., which have played a bigger role in stopping its mining operations until now.

Lloyds Metals and Energy Ltd received the mining lease more than 15 years back in 2007.

FY2022 annual report, page 39:

The Company was awarded a lease for iron ore mines in 2007 at Surjagarh Village, Gadchiroli district (having Maharashtra’s richest iron ore reserve)

However, despite getting the lease in 2007, it could start its operations only in 2012.

FY2012 annual report, page 4:

company has received all statutory permissions…and the mining operations have commenced on trial basis.

However, mining operations were short-lived because Naxals opposed mining in the area. In the next year in July 2013, Naxals killed one of the employees of Lloyds Metals and Energy Ltd and the mining operations stopped.

FY2015 annual report, page 7:

due to insurrection by Naxals near Surjagarh Iron Ore Mine in which one of the official of the Company was killed, the Mining Operations…has been temporarily discontinued w.e.f. July, 2013

The mining activities could resume in FY2017 after security arrangements by the police.

FY2017 annual report, page 13:

mining of calibrated iron ore at captive mine at Surajagarh in Maharashtra has 1.01 Lakh MT as against previous year’s mining of Nil MT

The mining operations required heavy police protection of about 200 police personnel dedicated to the mine.

FY2018 annual report, page 9:

Due to Naxalites’ threat mining takes place under police protection at Surjagarh. Around 200 strong force is deployed in the area to ensure safe transport of iron ore from the mines.

Due to the deployment of a large police force dedicated to protecting mining operations, the police department has charged a hefty security bill to Lloyds Metals and Energy Ltd. (Source: Mining firm gets Rs 45 crore bill from Gadchiroli police for providing security to mine: Indian Express)

Gadchiroli police have given a bill of Rs 45 crore against to Lloyds Metals and Energy Limited Company for providing security to its iron ore mine

The area of the company’s mine has such a large security threat from Naxals that without continuous police protection, no mining can take place. The company has disclosed to its shareholders that it can expand mining operations only if the police provide it protection.

FY2019 annual report, page 14:

The Company is taking all the effective steps to double the iron ore production for the financial year 2019-20, and hopeful of achieving it provided the requisite security is provided by police.

Mining activities, which had started in FY2017, could only continue for 3 years because in FY2020 the mining operations stopped because the police could not provide it sufficient protection due to the deployment of police personnel in election duties.

FY2020 annual report, page 43:

The iron ore production for the financial year 2019-20 is nil due to political uncertainties as the Central and State elections have adversely impacted the security arrangements in the Naxal affected area.

Subsequently, Lloyds Metals and Energy Ltd could start its mining operations only after a gap of 2 years, in FY2022.

Therefore, on an overall basis, out of about 16 years since the allotment of its iron ore mine, Lloyds Metals and Energy Ltd could operate it only for about 5 years with frequent disruptions including the killing of one of its employees.

In light of such significant uncertainties related to mining operations due to security threats, an investor should be very cautious while projecting the performance of the mining operations of Lloyds Metals and Energy Ltd into the future. This is because, in this Naxal-affected area, any single security-related incident might put a complete stop to mining operations for many years.

Further advised reading: How to do Business Analysis of Mining Companies

2) Intense competition in sponge iron segment:

Apart from mining operations, the sponge iron segment is the next major contributor to the revenue of Lloyds Metals and Energy Ltd. The company started the production of sponge iron almost 27 years back in FY1996. FY1997 was the first full year of this segment’s operations.

FY1997 annual report, page 6:

The Sponge Iron Plant located at Ghugus…has reported its first full year of operation during the year under review.

Despite running the sponge iron division for more than 27 years, Lloyds Metals and Energy Ltd has not been able to make it a source of sustainable growth because the sponge iron industry in India is highly fragmented.

FY2019 annual report, page 34:

There are over 400 sponge iron units in India. Indian sponge iron industry is highly fragmented. Top 20 producers contribute about 60-65% of total production whereas rest contributes 35-40% of the production.

These numerous sponge iron units compete strongly with each other

Credit rating report by Brickwork, January 2019, page 2:

Intense competition: The sponge iron industry is largely a fragmented industry with numerous unorganised players, thus resulting in a highly competitive industry

Apart from domestic sponge iron producers, Lloyds Metals and Energy Ltd has to compete with cheaper imports of steel from foreign manufacturers as well.

FY2015 annual report, page 6:

Due to rising imports from countries like China, Japan and Russia, domestic steel industry is struggling to retain margins. Cost structure in these countries has significantly come down

In addition to other sponge iron producers and imported steel, Lloyds Metals and Energy Ltd also has to compete against scrap steel, which is a substitute for sponge iron in steel making.

FY2016 annual report, page 9:

Steel scrap becomes a direct substitute of sponge iron; since both of them are tradable commodities

The outcome of a fragmented sponge iron industry with intense competition from domestic players, cheaper imports as well as substitutes like scrap iron, is that Lloyds Metals and Energy Ltd does not have any pricing power over its customers.

Advised reading: How to do Business Analysis of Steel Companies

3) No pricing power of Lloyds Metals and Energy Ltd over its customers:

The company does not have pricing power over its customers. It is evident from the fact that over the last 27 years (FY1996-2022), Lloyds Metals and Energy Ltd had reported overall net losses. At one stretch (FY1998-FY2004), it reported losses for 7 consecutive years.

On multiple occasions, Lloyds Metals and Energy Ltd highlighted to its shareholders its inability to pass on the increase in costs to its customers.

For example, recently, during FY2014 and FY2015, when the company reported losses for two consecutive years, then it pointed out tough business conditions and the inability to pass on costs to customers as the reason for losses.

FY2014 annual report, page 6:

Margins of steel producers would continue to be under pressure, given the high cost of production on the back of higher input costs and their limited ability to pass on hikes in costs.

It is not only limited to recent times. Due to the commodity nature of the company’s products, it has always faced challenges in passing on increases in input costs to its customers.

At the same time, when steel prices fall, then the company is not able to do anything to prevent losses. There have been times when the manufacturing of the company’s products became financially unviable/uneconomical and it had to shut down production to restrict its losses.

FY1998 annual report, page 4:

The overall fall in the margin is mainly due to a slowdown in the industrial activities in general and the depressed market conditions which did not permit any increase in sales price to offset the rising input costs. Resultantly the company had to curtail production at CRCA and Pipe Division.

To sell its products, in addition to reducing the prices, it also had to give them a longer credit period.

FY1998 annual report, page 4:

in trying to be competitive had to suffer a fall in price realisation. The division has taken various measures to improve the sales target, like easing credit terms to the regular customers

In FY1999, the company had to shut down one of its steel processing divisions because cheaper imports made manufacturing its products unviable.

FY1999 annual report, page 3:

The recession in the user industry segments, availability of cheap imported Cold Rolled material from CIS countries and uneconomical scale of operation forced the Management to temporarily close down the CRCA Plant situated at Dombivli,

In FY2001, when the company continued to make losses, then it once again it highlighted that

FY2001 annual report, page 3:

The rising input cost without corresponding increase in realisation has put further squeeze on margins.

In FY2007, when the company once again reported losses, then it highlighted an increase in raw material costs as the reason for losses.

FY2007 annual report, page 4:

Company has incurred a Loss, before exceptional items, of Rs. 30.56 crores during the year…mainly due to increase in the cost of raw materials

In FY2007, the production of galvanized pipes by the company became economically unviable due to an increase in the prices of zinc, which it could not pass on to customers.

FY2007 annual report, page 4:

PIPE DIVISION: The production in the division was lower due to unexpected increase in the price of zinc, having more than doubled during the year under review, which has made the sale of galvanized pipes commercially uneconomical.

Moreover, even after one full year, the operating environment had not become conducive and Lloyds Metals and Energy Ltd was not able to produce pipes profitably.

FY2008 annual report, page 4:

Pipe division: The division has in second successive year, underperformed due to the reasons beyond the control of the company owing to its product becoming commercially uneconomical.

The poor bargaining position of the company is not limited to its sponge iron/steel products division. Even in the case of power generation, it faced situations where its buyers, which are large state distribution companies, are not willing to buy power. As a result, the company’s performance suffered as it could not produce sufficient power to sell.

FY2014 annual report, pages 6-7:

Reluctance of State Electricity Boards to buy power due to their financial weakness which has led many power producers to operate at sub-optimal capacities….production of the division was 17.05 MWH during the year under review as compared to 23.96 MWH for the previous year.

It seems that due to its poor negotiating position in its existing businesses of sponge iron and power, Lloyds Metals and Energy Ltd was feeling frustrated and even made plans to diversify into other business areas like infrastructure and trading.

FY2016 annual report, page 9:

Company is currently engaged in steel and steel related products activity and is looking for new avenues of business in various areas like infrastructure and trading.

Advised reading: How to do Business Analysis of a Company

4) Steps taken by the company to improve operations:

Due to the tough business environment and poor bargaining power of the company, Lloyds Metals and Energy Ltd undertook many steps to improve its operations.

4.1) Using low-cost Hospet iron ore to make sponge iron:

In FY1998, the company started using Hospet iron ore, which proved to be a cheaper source of raw material.

FY1998 annual report, page 6:

Sponge Iron Division has successfully used HOSPET Iron Ore. The landed cost of which is lower, resulting in saving in raw material cost.

As per the company, Hospet iron ore is not suited for its plants; however, it could improvise and make adjustments to use it in its plant.

FY2001 annual report, page 5:

Normally the Hospet ore is soft and not suitable for rotary kiln based Sponge Iron production process. By making necessary adjustments to the process, the plant has successfully used low grade Hospet ore.

By improvising the manufacturing process, Lloyds Metals and Energy Ltd could increase the proportion of Hospet iron ore to about 26% of total consumption. It reduced the raw material costs for the company.

FY2001 annual report, page 3:

During the year Hospet ore was used in larger proportion successfully. The total Hospet ore used was 45,961 MT accounting to 26% of the total feed.

4.2) Steps for efficient utilization of coal:

Coal is one of the key raw materials used by Lloyds Metals and Energy Ltd to produce sponge iron. It forms a major portion of input costs. As a result, the company focused on various steps to reduce the cost of coal like buying a cheaper variety of coal from Western Coalfield Ltd (WCL) and making suitable changes in its manufacturing process.

FY2002 annual report, page 6:

Further to save in raw material cost from this year company started using less costly EPROM coal from WCL mines. The process is under stabilization with this type of coal.

Subsequently, the credit rating agency, Brickwork, highlighted the long-term sourcing arrangement of the company with WCL as one of the key advantages for the company, which ensures raw material supply.

Credit rating report by Brickwork, May 2020, page 6:

The Company procures coal from Western Coalfields Limited under long-term linkages.

Advised reading: Credit Rating Reports: A Complete Guide for Stock Investors

However, despite such long-term linkages to buy coal, it is still difficult to get the required quantity of coal by the company. As a result, it has to look for various ways to efficiently utilize coal and reduce its wastage.

In FY2004, the company adjusted the manufacturing process to improve productivity.

FY2004 annual report, page 6:

We have reduced the distance to less than half i.e. about 7-8 mtrs from kiln discharge end for achieving better coal throw pattern particularly during monsoon season when coal is wet which used to jam. By this reduction of distance, coal throw pattern is achieved better and jamming problem is sorted out resulting better productivity.

In FY2006, the company started work on a coal-washing facility at its plant to improve the efficiency of coal usage.

FY2006 annual report, page 5:

Washed coal trials have been taken and is being continued to use as it gives better production and proper control of sulphur levels as desired by the customer. In pursuance to this coal washers design has been finalized and erection work is under progress to wash coal in our premises only.

In FY2009, the company started mixing domestic coal sourced from WCL with the imported high FC coal to improve efficiencies.

FY2009 annual report, page 8:

Imported coal with High F.C has been introduced to get a better coal mix with our WCL-coals, enhance the quality of fuel to achieve consistency in quality of the finished products, higher productivity and higher campaign life of kilns.

The company had to import high calorific value coal from outside India because in India sponge iron industry finds it difficult to get this coal. Moreover, in India, such coal is given to the power and cement sectors on priority.

FY2017 annual report, page 12:

The sponge iron sector in India faces major challenge of high calorific value domestic coal availability and more allocations to power and cement sector…The sponge iron manufacturers are facing this as the biggest challenge as most of the coals reaching sponge iron plants from domestic sources are usually of low calorific value.

In order to decrease the usage of coal, the company started using high-quality iron ore from its own captive mines.

FY2017 annual report, page 18:

By using high quality hematite iron ore from our captive mines we are able to reduce coal consumption by 10% in DRI manufacturing process with compare to sponge iron industry norms

Even though the company attempted a lot to reduce its costs of using coal. However, still, in FY2022, it had a large exception expense of coal cess for ₹51 cr (FY2022 annual report, page 99).

4.3) Captive waste-heat recovery power plant to reduce power costs:

Lloyds Metals and Energy Ltd established a waste-heat recovery (WHR) power plant to reduce its costs and stay competitive in the tough sponge iron industry. The company installed a 30 MW power plant out of which it could produce 17-18 MW of power using waste heat. It helped it in producing power at a low cost of ₹2/- per unit.

The company used only a part of it (5MW) in-house and could sell the remaining in the open market.

Corporate presentation, July 2022, page 14:

The cost of Generation is very low at less than Rs. 2.00 per Unit…17-18 MW is generated from Waste Heat & balance 12-13 MW is generated from Coal…company uses approximately 5 MW internally and sells the balance

The power plant got certified emission reductions (CERs) from the UNFCCC because it had an environmentally-friendly impact by recovering waste heat. The company could sell these CERs to make some additional money.

FY2014 annual report, page 4:

project shall be eligible for 109,660 Carbon Emission Reductions (CER) Certificates every year for 10 years duration from 2013-2023.

However, after completing the power plant, the company continued to face challenges in selling power because the power prices were not highly profitable in comparison to the high input costs.

FY2012 annual report, page 4:

High fuel prices and low merchant realization has put pressure on operating margins of the power companies.

4.4) Other steps to reduce operating costs:

In FY2009, Lloyds Metals and Energy Ltd even resorted to changing the technology to produce sponge iron so that it could use lesser raw material and power in its operations.

FY2009 annual report, page 8:

Sponge Iron Division: Operating technology of 500 TPD Kiln has been changed to LURGI based concept during the year 2008-2009. The conversion of technology has improved plant productivity with-substantial reduction of raw materials input and electrical power consumption per MT of DRI.

However, at times, intense competition from domestic as well as cheaper imports created conditions when manufacturing products became unviable. In such conditions, Lloyds Metals and Energy Ltd closed down its units.

For example, in FY2000, due to tough business conditions and the poor pricing power of Lloyds Metals and Energy Ltd, it became financially unviable to produce CRCA sheets. As a result, the company decided to shut down this division. The company gave the unit to a third party for operations.

FY2000 annual report, page 3:

CRCA Division has been given on conducting basis to an outside party for a period of three years, in order to offset the fixed costs.

Therefore, an investor may note that the intense competition and nil pricing power ensured that despite all the efforts by Lloyds Metals and Energy Ltd to reduce its costs and improve its profitability, it could not protect its business from suffering.

Advised reading: Operating Performance Analysis: A Simple & Complete Guide

5) Financial support by Govt. to Lloyds Metals and Energy Ltd due to operations in the Naxal affected area:

The company’s sponge iron plant and mine are located in a remote tribal area, which is Naxal-affected. In order to promote industrial development in such areas, govt. give various financial incentives to the companies like Industrial Promotion Subsidy refunds and other capital subsidies.

At times, the capital subsidies exceed the investment done by companies in such areas. For example, in 2022, Lloyds Metals and Energy Ltd got approval from the govt. of a subsidy of 125% of the capital that it plans to invest in its upcoming plant at Konsari, Gadchiroli.

Corporate presentation, July 2022, page 15:

Government Subsidy Letter Received of 125% of Capital Invested.

The other plant proposed by the company at Ghugus, Chandrapur, has received approval for an Industrial Promotion Subsidy of 110%.

FY2021 annual report, page 28:

incentives under Package Scheme of Incentives -2019 (PSI -2019 ) in the form of exemption on electricity duty, 100% exemption on Stamp Duty, Industrial promotion subsidy equivalent to 110% of the Fixed Capital Investment.

In the past also, almost every year, the company received a substantial sum of Industrial Promotion Subsidy (IPS) refund, which is reported under other income/non-operating income.

For example, in the last 4 years (FY2019-FY2022), it received an IPS refund of about 100 cr.

- In FY2022, it received an IPS refund of ₹27 cr and in FY2021: ₹19 cr (FY2022 annual report, page 100).

- In FY2020, it received an IPS refund of ₹25 cr and in FY2019: ₹28 cr (FY2020 annual report, page 86).

In the previous years, the company had continued to receive IPS refunds of about ₹12-15 cr every year.

Such subsidy support helped the company to sustain itself in the face of intense competition. However, it did not prove sufficient in the past.

6) Default to the lenders/bankruptcy and then high-interest rates:

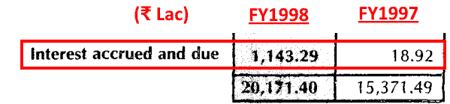

Due to the tough business environment of the steel industry, Lloyds Metals and Energy Ltd started reporting losses in FY1998 and defaulted to its lenders, as it could not make interest and principal repayments to them. As a result, its overdue started to accumulate from FY1998 onwards.

In FY1998, the company had about ₹11 cr of interest payments that it had to pay but it could not.

FY1998 annual report, page 13:

In FY1999, the overdue interest increased to ₹30 cr and in FY2000, it increased to ₹60 cr. (FY2000 annual report, page 12). In FY2001, the overdue interest increased to ₹89 cr and in FY2001, it increased to ₹137 cr. (FY2000 annual report, page 13). In FY2003, the overdue interest had crossed ₹150 cr. (FY2003 annual report, page 13).

In FY2004 annual report, the auditor of Lloyds Metals and Energy Ltd intimated to its shareholders that an amount of ₹352 cr is still overdue to different lenders since FY1998.

FY2004 annual report, page 9:

Amount of default aggregating to Rs.352 crores since 1997-98.

Due to continued losses and defaults in loan repayments, in FY2003, the company was admitted to the then bankruptcy court of India, Board of Industrial and Financial Reconstruction (BIFR).

FY2003 annual report, page 4:

Based on the Audited Balance Sheet for the year ended 31st March 2002, the Company has become a Sick Company…and reference has been registered during the year with Hon’ble Board- for Industrial and Financial Reconstruction (BIFR)

In FY2006, BIFR appointed IDBI as the operating agency for resolving the bankruptcy situation and rehabilitation of the company.

FY2006 annual report, page 5:

BIFR declared the Company as Sick…and appointed IDBI as the Operating Agency (OA) to prepare a Draft Rehabilitation Scheme (DRS) for the company.

In FY2008, as per the resolution of the BIFR-mandated debt restructuring, it was decided that Lloyds Metals and Energy Ltd would have to sell its pipe division, Murbad and then use the money for repayment of lenders.

FY2008 annual report, page 4

The CDR terms…stipulates that the company shall sell / transfer the entire assets along with employees of its pipe division at Murbad and utilize the sale proceeds for payment of settlement dues.

It was a second attempt by the lenders to recover their money from the company by making it sell its pipe division. Previously, in FY2000, the lenders had asked the company to sell its sheets division to repay loans.

FY2000 annual report, page 4:

your Company along with major creditors…As a part of the revival of the economic condition of the Company,…the de-merger of the C.R. Sheets Division into Incon Technologies Limited and amalgamation of rest of the Company thereafter with Insco Steels Limited is proposed

In FY2002, the lenders approached the debt recovery tribunal, which ordered Lloyds Metals and Energy Ltd not to sell/mortgage its assets.

FY2002 annual report, page 19:

In respect of the dues of some banks, Debt Recovery Tribunal (DRT, Mumbai) has issued an injunction order restraining the Company from transferring or creating third party right in the charged assets

However, these schemes did not work and the lenders had to take losses.

In FY2004, some lenders took a loss of 75% of their loan amount because they had to accept a payment of only ₹4.42 cr against their claims of ₹17.72 cr. The company reported the difference as an income/profit to its shareholders.

FY2004 annual report, page 20:

outstanding amount (Principal plus Interest) as per books of Rs.1772.96 lacs has been restructured and settled for Rs. 442.00 lacs. The difference amount of Rs. 1330.96 lacs has been written back to profit & loss account.

Next year, in FY2005, lenders had to accept a loss of about 60% of their money when they had to accept only about ₹83 cr against their loans of about ₹202 cr. Lloyds Metals and Energy Ltd reported the difference of ₹119 cr as an exception income/profit to its shareholders.

FY2005 annual report, page 18:

outstanding amount (Principal plus Interest) as per books is Rs.20279.51 lacs has been restructured and settled for Rs. 8316.90 lacs. The difference amount of Rs. 11962.61 lacs has been included in Exceptional Item in Profit & Loss account

Once again, in FY2006, lenders had to accept a loss of about 60% of their money when they had to accept only about ₹62 cr against their loans of about ₹146 cr.

FY2006 annual report, page 18:

total outstanding amount (Principal plus Interest) as per books of Rs. 14669.23 lacs has been restructured and settled for Rs.6226 98 lacs.

In FY2007, the company had lenders whose dues were not paid for almost the last 10 years as it had defaults of about ₹62 cr pending since FY1998.

FY2007 annual report, page 11:

Amount of default aggregating to Rs.61.98 crores is outstanding since 1997-98 & Rs.9.29 crores during the year.

In FY2008, lenders had to take a loss of 80% when they had to accept only about ₹14 cr against their loans of about ₹62 cr.

FY2008 annual report, page 19:

total outstanding amount (Principal Plus Interest) as per books of Rs.6197.72 lacs has been restructured and settled for Rs.1423.27 lacs.

In FY2009, lenders had to take a loss of 75% when they had to accept only about ₹20 cr against their loans of about ₹76 cr.

FY2009 annual report, page 20:

total outstanding amount (Principal) as per books of Rs. 7573.76 lacs has been restructured and settled for Rs. 1965.75 lacs

The company benefited from the loss taken by lenders and its reported profits increased as it wrote back the interest provisions as income/profits when lenders took a haircut under restructuring.

For example, in FY2006, the net profit of the company increased over the last year mainly due to writing back of interest expenses.

FY2006 annual report, page 5:

Company has reported a Net Profit of Rs. 42.11 crores as against a net Profit of Rs. 29.83 crores in the previous year mainly due to exceptional adjustments on account of write back of past interest provisions upon negotiated restructuring of debt.

It does not come as a surprise that when the company was continuously defaulting to lenders and forcing them to accept a loss on the money given by them to the company, then lenders will not be too eager to give to the company when needed.

As a result, on numerous occasions, the company faced a situation where lenders did not give its working capital loans and its business suffered.

For example, in FY2000-FY2002, lenders hesitated to give working capital loans to Lloyds Metals and Energy Ltd, which limited its ability to operate efficiently.

FY2000 annual report, page 3:

Constraints of working capital further eroded the operating capacity of the Company.

FY2002 annual report, page 4:

The ongoing working capital constraint & continuing slowdown in the user industry has affected the operations of the Company

During this period, the lenders were still trying to recover their money. However, by FY2008, the lenders had burnt their fingers and accepted losses of 60% to 80% on the money given by them to the company.

Advised reading: Can we Assess a Bank’s Financial Position from its Reported Financials

As a result, they were not willing to give any working capital loans to the company. The company had to take loans from outside parties other than banks etc. and therefore, it had to pay very high-interest costs for such loans, which has also led to a decline in profit margins.

FY2008 annual report, page 4:

higher Financial Charges incurred due to non-availability of working capital assistance from regular banking channel.

In terms of such a relationship of the company with lenders, it does not come as a surprise to the investors that the company had to do multiple rounds of equity dilution for raising money for working capital and capital expenditure. Whether it is by way of issuing warrants, preference shares, or convertible debentures to promoters or non-promoters and including raising money from the Thriveni group.

In addition, the company had to take debt from other promoter entities like Lloyds Steels Industries Ltd and Indrajit Properties Pvt. Ltd etc. (FY2019 annual report, page 86).

7) Breaking of contract by Lloyds Metals and Energy Ltd leading to a very large penalty leading to a very large loss in FY2023:

In Q1-FY2023, Lloyds Metals and Energy Ltd reported a very large non-operating loss of ₹1,194.40 cr leading to a net loss after tax of ₹930 cr.

Q1-FY2023 results, page 9:

The exceptional item has arisen pursuant to an arbitration award under which the company is liable to pay the amount…amount is being paid by way of 0% Optionally Fully Convertible Debentures (OFCD`s). The OFCD`s when converted will result in a dilution of equity capital to the extent of 6 crores equity shares.

Lloyds Metals and Energy Ltd had to pay this large sum of money because broke its contract with Sunflag Iron & Steel Company Ltd (Sunflag). Sunflag gave it money (₹312 cr) for the development of the iron ore mine; however, Lloyds did not supply iron ore to Sunflag.

FY2022 annual report, page 16:

Sunflag had advanced funds to the Company towards the operation and commencement of the mine. In the year 2016, the Company started mining operations with minimal production; however, the Company could not share the iron ore extracted with Sunflag for various reasons.

In the arbitration, Lloyds Metals and Energy Ltd was held responsible for breaking the contract and was asked to pay ₹900 cr to Sunflag.

FY2022 annual report, page 17:

The Company was liable to pay ₹900 crores to Sunflag (i.e., ₹312 crores on account of refund of advance along with accrued interest and the balance ₹588 crores as full settlement of all other claims).

Advised reading: How to study Annual Report of a Company

As Lloyds Metals and Energy Ltd did not have so much money to pay in cash; therefore, it gave 6 cr OFCDs for free to Sunflag, which give Sunflag an 11.89% stake in the company (Board meeting outcome, April 29, 2022, page 14).

The breach of contract with Sunflag by Lloyds Metals and Energy Ltd has further complicated the business position of the company. Over the last 27 years (FY1996-FY2022), Lloyds Metals and Energy Ltd has made a cumulative net loss of ₹17 cr and now it has reported its biggest loss of ₹930 cr in Q1-FY2023.

Going ahead, an investor needs to keep a close watch on the business performance of Lloyds Metals and Energy Ltd. She should closely track all the developments related to mining operations because any security failure can lead to the closure of mining operations for a couple of years. She should monitor the performance of the sponge iron segment to check if it is able to operate profitably in light of intense competition. She should check whether the power segment of the company is able to increase its production and sell it to distribution companies.

Over the last 10 years (FY2013-FY2022), the tax payout ratio of Lloyds Metals and Energy Ltd is nil indicating that the company has not paid any income tax during this period.

From the above discussion, an investor would remember that over the years, the company has made cumulative losses (a total net loss of ₹17 cr from FY1996 to FY2022). Due to such large losses, which are carried over the years, Lloyds Metals and Energy Ltd has not paid any income tax.

In addition, during FY2020 and FY2022, Lloyds Metals and Energy Ltd reported negative tax i.e. a profit after tax (PAT) higher than profit before tax (PBT). This is due to large brought forward losses, which the company has used to create tax assets i.e. it will use these losses against future profits when they happen.

In FY2020, Lloyds Metals and Energy Ltd recognized a negative tax payout (deferred tax assets) of about ₹19 cr as it utilized brought forward losses of about ₹80 cr.

FY2020 annual report, pages 96, 97:

sufficient profits will be available in future to recoup…carried forward losses and accordingly deferred tax has been recognized on those losses under Ind-AS provisions. The deferred tax asset has been recognized of ₹1,873.32 Lakhs as on 31.03.2020

Brought Forward Losses ₹7,949.68 lac

Similarly, in FY2022, the company recognized negative tax payout (deferred tax assets) of about ₹9.5 cr as it utilized brought forward losses of about ₹50 cr.

FY2022 annual report, pages 96, 97:

Deferred Tax recognized during the year in the P/L ₹950.68 lacs

Brought Forward Losses ₹4,950.87 lacs

Looking at the large loss of ₹930 cr in Q1-FY2023, it remains to be seen whether Lloyds Metals and Energy Ltd will pay income tax in the near future or not.

Nevertheless, it seems that the income tax department is not agreeing with the position of the company to pay nil tax. In FY2022, Lloyds Metals and Energy Ltd received a demand notice from the Income Tax Dept. for ₹32 cr, which it has disclosed under contingent liabilities without sharing any more details (FY2022 annual report, page 147).

An investor may contact the company directly for getting more information about this demand notice.

Advised reading: How to do Financial Analysis of a Company

Operating Efficiency Analysis of Lloyds Metals and Energy Ltd:

a) Net fixed asset turnover (NFAT) of Lloyds Metals and Energy Ltd:

Over the years, the NFAT of the company had declined from 2.3 in FY2015 to 0.7 in FY2021. Such declining NFAT indicates a deteriorating efficiency of utilization of fixed assets by the company.

NFAT has improved to 1.8 in FY2022 due to a sharp improvement in mining operations.

Going ahead, an investor should keep a close watch on the NFAT of the company to assess whether it can use its fixed assets and manufacturing capacity especially related to sponge iron and power production optimally.

This is especially important because, on many occasions, auditors of Lloyds Metals and Energy Ltd have highlighted that the company has not verified and taken the needed care of its fixed assets.

FY1998 annual report, page 9:

The fixed assets of the company have not been verified during the year

FY1999 annual report, page 8:

All the fixed assets have not been verified during the year

FY2001 annual report, page 6:

All the fixed assets have not been verified during the year

There have been instances where due to lack of proper care and required investments in the fixed assets, their quality deteriorated significantly and they had to be sold off in slump sale.

In FY2009, Lloyds Metals and Energy Ltd sold off its CRCA sheets division in a slump sale because its fixed assets had deteriorated due to a lack of investment in the last 10 years.

FY2009 annual report, page 6:

sale /transfer of its CRCA Unit at Dombivli on Slump sale basis as the conditions of the plant and machinery of the unit were deteriorated over the years. As the company could not make any investment in the unit since 1999 due to financial constraint

Therefore, an investor should keep a close watch on the signs that indicate whether the company is maintaining its fixed assets properly or not.

Further advised reading: Asset Turnover Ratio: A Complete Guide for Investors

b) Inventory turnover ratio (ITR) of Lloyds Metals and Energy Ltd:

In the past, the inventory turnover ratio (ITR) of the company had declined from 16.0 in FY2015 to 4.9 in FY2022. A decline in the inventory turnover ratio indicates that the efficiency of inventory utilization of the company has deteriorated over the years.

A decline in inventory efficiency increases the burden of working capital finance on the company. As a result, Lloyds Metals and Energy Ltd had to raise money from external parties (Thriveni group) to meet its working capital requirements by diluting its equity.

FY2021 annual report, page 19:

The proposed issue of 9,00,00,000 (nine crore) Equity Shares and 1,00,00,000 (one crore) 3% OFCDs…is being made for…meeting the short term and long term funding requirements of the Company including but not limited to working capital requirements

Going ahead, an investor should keep a close watch on the ITR of the company to assess whether it is using its inventory efficiently.

Further advised reading: Inventory Turnover Ratio: A Complete Guide

c) Analysis of receivables days of Lloyds Metals and Energy Ltd:

Over the years, the receivables days of Lloyds Metals and Energy Ltd have improved from 19 days in FY2014 to 8 days in FY2022. A trend of declining receivables days indicates that the company is able to collect its dues on time from its customers.

This comes as a welcome change from the history of Lloyds Metals and Energy Ltd when it could not collect its money from its customers who used to delay payments even by many years.

FY1997 annual report, page 6:

recovery from customers were delayed beyond the normal credit period.

In FY2000, the company had an overdue of more than ₹50 cr from customers who had not paid the money even after 6 months after the payment date.

FY2000 annual report, page 19:

Debtors outstanding for more than 6 months amounting to Rs.5249.88 Lacs

The company had to initiate court cases to recover its money.

FY2001 annual report, page 16:

Sundry Debtors exceeding six months includes Rs. 107.15 Lacs (Previous year Rs. 92.32 Lacs) for which the company has initiated legal proceedings

However, despite all its efforts, Lloyds Metals and Energy Ltd was not able to recover its money. In FY2003, the company had payments of about ₹23 cr due from its customers for more than 3 years since the payment date.

FY2003 annual report, page 19:

debtors outstanding for more than three years and aggregating to Rs. 2301.76 Lacs

In the next year, FY2004, Lloyds Metals and Energy Ltd had to write off ₹13.6 cr of receivables.

FY2004 annual report, page 16:

Bad Debts/ Provisions /Sundry Balance W/off (Net) ₹1,360.34 lac

Even in recent times, in FY2018, the company had some receivables where customers had not made payments even after more than 3 years.

FY2018 annual report, page 63:

More than 6 month receivables of 54.92 lac are pending since at least last 3 years.

Going ahead, an investor should monitor the trend of receivables days of Lloyds Metals and Energy Ltd to assess whether it continues to collect its receivables on time.

Further advised reading: Receivable Days: A Complete Guide

When an investor compares the cumulative net profit after tax (cPAT) and cumulative cash flow from operations (cCFO) of Lloyds Metals and Energy Ltd for FY2013-2022, then she notices that over the years (FY2013-FY2022), the company has not converted its profit into cash flow from operations.

Over FY2013-22, Lloyds Metals and Energy Ltd reported a total net profit after tax (cPAT) of ₹112 cr. During the same period, it reported cumulative cash flow from operations (cCFO) of ₹47 cr.

It is advised that investors should read the article on CFO calculation, which would help them understand the situations in which companies tend to have the CFO lower than their PAT. In addition, the investors would also understand the situations when the companies would have their CFO higher than PAT.

Further advised reading: Understanding Cash Flow from Operations (CFO)

Learning from the article on CFO will indicate to an investor that the cCFO of Lloyds Metals and Energy Ltd is lower than the cPAT due to a significant amount of money consumed by inventory, which as discussed above, is evident from the deteriorating inventory turnover ratio of the company.

Going ahead, an investor should keep a close watch on the working capital position of Lloyds Metals and Energy Ltd.

The Margin of Safety in the Business of Lloyds Metals and Energy Ltd:

a) Self-Sustainable Growth Rate (SSGR):

Read: Self Sustainable Growth Rate: a measure of Inherent Growth Potential of a Company

Upon reading the SSGR article, an investor would appreciate that if a company is growing at a rate equal to or less than the SSGR and it can convert its profits into cash flow from operations, then it would be able to fund its growth from its internal resources without the need of external sources of funds.

Conversely, if any company attempts to grow its sales at a rate higher than its SSGR, then its internal resources would not be sufficient to fund its growth aspirations. As a result, the company would have to rely on additional sources of funds like debt or equity dilution to meet the cash requirements to generate its target growth.

An investor may calculate the SSGR using the following formula:

SSGR = NFAT * NPM * (1-DPR) – Dep

Where,

- SSGR = Self Sustainable Growth Rate in %

- Dep = Depreciation rate as a % of net fixed assets

- NFAT = Net fixed asset turnover (Sales/average net fixed assets over the year)

- NPM = Net profit margin as % of sales

- DPR = Dividend paid as % of net profit after tax

(For systematic algebraic calculation of SSGR formula: Click Here)

Over the years, Lloyds Metals and Energy Ltd has reported an SSGR of negative to nil. SSGR has improved only in recent years due to a sharp improvement in the mining business. However, in previous years, the SSGR of the company has been very low.

As a result, to run and expand its capital-intensive business, the company has to rely on external capital in the form of debt and equity dilution.

The company has historically relied on debt to meet its capital requirements. However, from FY1998, it started to default to the lenders. As a result, lenders had to accept losses on their loans and they hesitated to give loans to the company.

Therefore, the company had to rely on equity dilution and loans from promoter companies to meet capital requirements. In the last 25 years, on many occasions, Lloyds Metals and Energy Ltd had to raise money via equity dilution.

- In FY1999, the company raised ₹23 cr by issuing Cumulative Redeemable Preference Shares to promoters (FY1999 annual report, page 11), which were converted into equity shares in FY2007 (FY2007 annual report, page 4).

- In FY2008, the company raised ₹9.2 cr by issuing warrants and then converting them into equity shares to non-promoters. (FY2008 annual report, page 4).

- In FY2020, the company issued warrants to promoters for ₹18 cr. (FY2020 annual report, page 4), which were converted into equity shares later (FY2021 annual report, page 28).

- In FY2021, the company issued further warrants for ₹62.5 cr to promoters (FY2021 annual report, page 29). These warrants were converted into equity shares in the board meeting on April 29, 2022.

- In FY2021, in another transaction, the company raised ₹20 cr by issuing Optionally Fully Convertible Debenture (OFCDs) to Clover Media Private Limited (CMPL) (FY2021 annual report, page 29). These OFCDs were later on converted into equity shares (FY2022 annual report, page 15). The conversion gave a 9.66% shareholding to CMPL (FY2020 annual report, page 13).

- In FY2022, the company raised ₹200 cr from Thriveni group (₹180 cr via allotting equity shares and ₹20 cr via Optionally Fully Convertible Debentures (OFCD’s) to Thriveni Earthmovers Private Limited (FY2022 annual report, page 15). Because of infusing ₹200 cr, Thriveni group became the joint promoters of Lloyds Metals and Energy Ltd along with the B.L. Agarwal family.

Therefore, over the years, the company has raised a total of ₹332 cr via equity dilution out of which ₹300 cr has been raised in the last 3 years.

Apart from this, the business also consumed about ₹320 cr during debt restructuring over FY2004-FY2009, which the lenders had to accept as a loss on their loans.

Therefore, an investor can notice that the business of Lloyds Metals and Energy Ltd has not generated sufficient money to run and expand its operations. The cost of the company’s operations and growth is borne by lenders via haircuts and shareholders by equity dilution.

Even during the Covid period, the company availed the moratorium on debt services provided by the Reserve Bank of India (RBI) for 5 months duration.

Credit rating report by Brickwork, August 2021, page 5:

company had availed moratorium period for the interest and principal payments towards the term loan from its lenders during March 2020 to August 2020 under the COVID-19 regulatory package.

Such incidents indicate the precarious cash flow condition of the company that with every stressful development in the business environment, the company faces a liquidity crunch.

An investor gets the same conclusion when she analyses the free cash flow position of Lloyds Metals and Energy Ltd.

b) Free Cash Flow (FCF) Analysis of Lloyds Metals and Energy Ltd:

While looking at the cash flow performance of Lloyds Metals and Energy Ltd, an investor notices that during FY2013-FY2022, it generated cash flow from operations of ₹47 cr. During the same period, it did a capital expenditure of about ₹326 cr.

Therefore, during this period (FY2013-FY2022), Lloyds Metals and Energy Ltd had a negative free cash flow (FCF) of (₹279) cr (=47 – 326).

In addition, during this period, the company had a non-operating income of ₹156 cr and an interest expense of ₹114 cr. As a result, the company had a net negative free cash flow of ₹237 cr (= – 279 + 156 – 114). Please note that the capitalized interest is already factored in as a part of the capex deducted earlier.

While looking at the overall cash-flow position of Lloyds Metals and Energy Ltd over the last 10 years (FY2013-2022), an investor notices that the company has primarily used the following sources to meet this cash shortfall:

- Raising equity by equity dilution, preferential issue of shares, warrants, OFCD etc. to promoters and non-promoters.

- Increase in debt by ₹51 cr as total debt has increased from ₹26 cr in FY2013 to ₹77 cr in FY2022.

Going ahead, an investor should keep a close watch on the free cash flow generation by Lloyds Metals and Energy Ltd to understand whether the company is able to generate surplus cash from its business and stop its frequent equity dilutions.

Further advised reading: Free Cash Flow: A Complete Guide to Understanding FCF

Self-Sustainable Growth Rate (SSGR) and free cash flow (FCF) are the main pillars of assessing the margin of safety in the business model of any company.

Further advised reading: 3 Simple Ways to Assess “Margin of Safety”: The Cornerstone of Stock Investing

Additional aspects of Lloyds Metals and Energy Ltd:

On analysing Lloyds Metals and Energy Ltd and after reading annual reports, credit rating reports and other public documents, an investor comes across certain other aspects of the company, which are important for any investor to know while making an investment decision.

1) Management Succession of Lloyds Metals and Energy Ltd:

Lloyds Metals and Energy Ltd is a part of the B.L. Agarwal family group in which Thriveni group has become a joint promoter in FY2022 by investing ₹200 cr.

As on date, Mr Babu Lal (B.L.) Agarwal (age 75 years) is leading the day-to-day operations of the company. Mr Balasubramanian Prabhakaran (age 49 years), the promoter of the Thriveni group is present on the board as a non-executive director.

Mr Mukesh Gupta, nephew of Mr B.L. Agarwal is currently the chairman of the company. Mr Rajesh Gupta, brother of Mr Mukesh Gupta is present on the board as a non-executive director.

Grandson of Mr B. L. Agarwal, Mr Madhur Gupta is also present on the board as a non-executive director.

FY2021 annual report, page 41:

Mr. Babulal Agarwal, Managing Director of the company is maternal uncle of Mr. Mukesh Gupta & Mr. Rajesh Gupta, Directors of the Company and Grandfather of Mr. Madhur Gupta, Additional Director of the Company.

It is important to note that the son of Mr Ravi Agarwal, son of Mr B. L. Agarwal is not a part of the board of directors.

FY2020 annual report, page 14:

Mr. Babulal Agarwal, the Managing Director of the Company is the father of Mr. Ravi Agarwal (belonging to Promoter/ Promoter Group of the Company)

Going ahead, an investor should keep a close watch on the relationship between the son and nephews of Mr B. L. Agarwal to understand more about the succession planning of the group.

Further advised reading: How to do Management Analysis of Companies?

2) Accounting issues pointed out by auditors of Lloyds Metals and Energy Ltd:

On numerous occasions, the auditors of the company have highlighted instances when Lloyds Metals and Energy Ltd did not follow proper accounting policies and as a result, it reported a higher profit or lower losses than what it actually should have.

At times, the amount of impact of these accounting changes was more than ₹100 cr.

2.1) Non-provision of interest expense in the P&L by Lloyds Metals and Energy Ltd:

In FY2004, the company did not provide for interest amounting to about ₹104 cr. As a result, the company, which should have reported a loss of about ₹105 cr for FY2004, reported only a loss of ₹1.5 cr.

FY2004 annual report, page 8:

The company has not provided interest amounting to Rs. 10378.09 lacs (till date Rs. 18177.47 lacs ) had the same been considered the loss for the year after taxation would have been Rs. 10535.27 lacs (as against the reported figure of loss of Rs. 157.18 lacs)

In FY2003, the company did not make provisions for interest expense of ₹68 cr and reported a loss of ₹32 cr whereas the actual loss was about ₹100 cr.

FY2003 annual report, page 9:

Note No 20 regarding non-provision of interest amounting to Rs. 6830.44 lacs (till date Rs. 7977.97 lacs)…had the observations…been considered the loss for the year after taxation would have been Rs. 10079.85 lacs (as against reported figure of loss of Rs.3241.41 lacs)

Lloyds Metals and Energy Ltd tried to show lower losses in FY2007 as well when it did not provide for interest expense of ₹34 cr and showed a lower loss of ₹30 cr instead of an actual loss of ₹64 cr.

FY2007 annual report, page 10:

The company has not provided interest amounting to Rs. 3351.25 lacs (till date Rs.11385.31 lacs), had the same been considered the Loss for the year after taxation would have been Rs. 6416.86 lacs (as against the reported figure of Loss of Rs. 3065.61 lacs)

In FY2006, the company inflated its profit by not providing for interest expense of ₹27 cr and showed a higher profit of ₹42 cr whereas the actual profit was only about ₹15 cr.

FY2006 annual report, page 10:

The company has not provided interest amounting to Rs. 2707.21 lacs (till date Rs. 8034.06 lacs), had the same been considered the Profit for the year after taxation would have been Rs. 1498.01 lacs (as against the reported figure of Profit of Rs. 4205.22 lacs)

Similarly, in FY2005, the company inflated its profit by not providing for interest expense of ₹25 cr and showed a higher profit of ₹30 cr whereas the actual profit was only about ₹5 cr.

FY2005 annual report, page 25:

The company has not provided interest amounting to Rs. 2476.68 lacs (till date Rs. 6162.53 lacs), had the same been considered the Profit for the year after taxation would have been Rs. 505.86 lacs (as against the reported figure of Profit of Rs. 2982.54 lacs)

Similarly, Lloyds Metals and Energy Ltd did not provide for interest expense of ₹3.8 cr in FY2000, ₹3.82 cr in FY2001, and ₹3.77 cr in FY2002.

Advised reading: How Companies Inflate their Profits

2.2) Non-provision of deferred taxes by Lloyds Metals and Energy Ltd:

In FY2002, the company did not provide for a deferred tax liability of about ₹35.5 cr in its books. As a result, it reported lower losses of ₹86 cr whereas the actual losses would have been higher by ₹35.5 cr.

FY2002 annual report, page 18:

The company has not created deferred tax liability in the books of account to the extent of Rs.3550.04 Lacs…As the company has not made any provision for the deferred tax liability the losses for the year after tax are lower to the extent of Rs.3550,04 Lacs.

It is not a case that Lloyds Metals and Energy Ltd did not follow proper accounting policies only in the past and now it has started following all the policies. Even in recent times, in FY2021, the company did not follow the accounting policies, as it did not create provisions for deferred taxes.

FY2021 annual report, page 105:

No provision has been made during the year ended on 31st March 2021 for Deferred Tax. Ind AS 12 requires recognition of tax consequences of difference between the carrying amounts, of assets and liabilities and their tax base. With reference to the above, the company has not adhered with measurement criteria as per Ind AS 12.

From the above points highlighted by the auditors of the company, over the years, Lloyds Metals and Energy Ltd did not provide for the interest and deferred taxes of about ₹304 cr over FY2000 to FY2022 and the cumulative profits declared by the company are elevated/losses are suppressed to that extent.

Keeping this in mind, the cumulative loss suffered by the company during the last 27 years (FY1996-FY2022) of ₹17 cr increases to ₹321 cr (= 17 + 304), which brings out the tough business journey of Lloyds Metals and Energy Ltd over the years.

The situation looks further grim if the investor adds the ₹930 cr of loss suffered by the company in Q1-FY2023 penalty on the company for breaking its contract with Sunflag even after receiving ₹312 cr from Sunflag for developing the mine and then not delivering the iron ore to Sunflag.

Advised reading: Deferred Tax Assets, Tax Payout (P&L vs. CFO): Queries Answered

3) Suboptimal capital allocation by Lloyds Metals and Energy Ltd:

In the past, on multiple occasions, Lloyds Metals and Energy Ltd did not put shareholders’ capital to its best use. At times, it invested money in projects but abandoned the project midway leading to large write-offs.

For example, in FY2005, the company wrote off ₹95 cr because of an abandoned project.

FY2005 annual report, page 19:

Exceptional items includes an amount of Rs. 9537.10 lacs on account of write off during the year of abandoned project.

Similarly, in FY2008, the company wrote off another ₹7.8 cr due to the impairment of its fixed assets.

FY2008 annual report, page 13:

Exceptional items includes an amount of Rs.777.09 lacs on account of impairment loss on fixed assets

FY2005 and FY2008, the years when Lloyds Metals and Energy Ltd recognized these write-offs were the years in which it recognised large gains due to the haircut/loss accepted by lenders. Therefore, effectively, lenders’ loss became the company’s gain and during the years when it had large exceptional gains due to debt restructuring, it recognized the write-offs on its fixed assets.

For example, the company recognized the write-off for ₹95 cr due to the abandoned project in FY2005 when it had an exceptional gain of ₹119 cr due to haircut loss taken by the lenders.

FY2005 annual report, page 18:

outstanding amount (Principal plus Interest) as per books is Rs.20279.51 lacs has been restructured and settled for Rs. 8316.90 lacs. The difference amount of Rs. 11962.61 lacs has been included in Exceptional Item in Profit & Loss account

Similarly, the company recognized the next write-off for about ₹8 cr on its fixed assets in FY2008 when it had another large exceptional gain due to haircut loss taken by the lenders.

FY2008 annual report, page 19:

the total outstanding amount (Principal Plus Interest) as per books of Rs.6197.72 lacs has been restructured and settled for Rs.1423.27 lacs. Principal amount of Rs 1135.22 lacs written back has been credited to Capital Reserve and the balance amount of Rs 3639.22 lacs has been credited to profit & loss account

It may seem like an attempt to mitigate the impact of large fixed asset write-offs by recognizing them in suitable periods.

Even in recent times, Lloyds Metals and Energy Ltd has taken decisions on capital deployment, which seem strange to an investor.

For example, in FY2021, the company purchased a land parcel for ₹15 cr from a promoter group entity, Snowwhite Realty Developers LLP. Lloyds Metals and Energy Ltd kept it as “held for sale”, which indicates that the company planned to sell it in a short period to gain some profits.

FY2021 annual report, pages 39, 71:

Related party transactions: Purchase of Property of the Value of ₹1,513.56 Lakhs from Snowwhite Realty Developers LLP.

The management estimates that the land so acquired is to be held for sale and not for use in the ordinary course of business.

In the next year, in FY2022, instead of selling the property to any third party for some profit, it transferred it back to Snowwhite Realty Developers LLP.

FY2022 annual report, page 28:

Related party transactions: Transferring back of Property of the Value of ₹1,513.56 to Snowwhite Realty Developers LLP

An investor may contact the company directly to understand the logic of this transaction and how it benefited the shareholders of the company.

Advised reading: How to Identify if Management is Misallocating Capital

4) Allegations of damage to the environment by the business activities of Lloyds Metals and Energy Ltd:

Media has reported a few instances, which indicate that the business activities of the company have caused damage to the environment.

For example, in February 2018, Maharashtra Pollution Control Board (MPCB) ordered the company to shut down its plant due to pollution (Source: MPCB orders closure of Lloyds’ Ghugus plant: The Times of India, February 9, 2018). As per the article, MPCB has termed the company as a habitual defaulter.

MPCB member-secretary Dr P Anbalagan has termed the company as habitual defaulter that knowingly and willingly violates the provisions of Air and Water (Prevention and Control of Pollution) Acts causing serious pollution in the surrounding.

In another instance in February 2021, the irrigation department cut the water supply to the company stating that it was stealing water from a govt. reservoir. (Source: Irrigation dept snaps water supply of Lloyd Metals: The Times of India, February 26, 2021)

Department has also discovered that the company was “stealing water” from the reservoir of a nearby WCL mine for the last few years. The department’s executive engineer (EE) has issued an order to file police complaint in the matter.

In light of such instances, it is advised that an investor should keep a close watch on the local developments in the region of the company’s plants so that she may get an idea about the perception of the company in the local population and if it may face local unrest in the future.

5) Remuneration to promoter-manager by Lloyds Metals and Energy Ltd:

While analysing the history of remuneration paid by the company to its promoter-manager and investor notices a few instances where the company paid a high remuneration in comparison to the performance of the company.

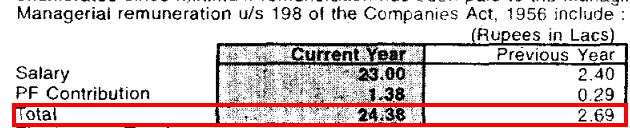

For example, in FY2002, when the company reported its highest loss of ₹86 cr, higher than the loss in the previous year of ₹72 cr, it increased the remuneration of its managing director, Mr B.L. Agarwal by more than 9 times. The remuneration of Mr B.L. Agarwal increased from ₹2.69 lac in FY2001 to ₹24.38 lac in FY2002.

FY2002 annual report, page 18:

Subsequently, due to the poor performance of the company, the remuneration of Mr B.L. Agarwal exceeded the statutory limits and therefore, the company had to take approval from the central govt. to pay his remuneration.

Lloyds Metals and Energy Ltd had to take such approval from the central govt. for paying remuneration to Mr B.L. Agarwal for FY2006, FY2007, FY2008 and FY2009.

FY2006 annual report, page 8:

The remuneration paid to Managing Director from 1st January, 2005 onwards is subject to the approval of the Central Government for which necessary application has been made.

FY2009 annual report, page 9:

For remuneration paid to Managing Director from 1st January, 2005 onwards necessary application has been made for approval of Central Government.

In FY2018, when the profit of the company was ₹17 cr, which is even less than the profit of ₹23 cr earned by the company; it increased the remuneration of its managing director, Mr B.L. Agarwal to ₹65 lac. (FY2018 annual report, page 22).

Advised reading: How to identify Promoters extracting Money via High Salaries

6) Dividend funded by equity dilution:

In FY2022, Lloyds Metals and Energy Ltd declared a dividend of ₹0.50/- per share (FY2022 annual report) and as a result, it paid out an amount of about ₹19 cr to its shareholders.

However, the decision to pay a dividend to shareholders seems strange in a situation when the company is raising money by diluting equity to meet its funds’ requirements. The company had raised ₹18 cr in FY2020, ₹82 cr in FY2021 and ₹200 cr in FY2022 by diluting its equity by way of preference shares, warrants, OFCDs etc.

Moreover, in FY2022, the company reported a negative cash flow from operations (CFO) of (₹78 cr) and in the previous year, FY2021, it had a negative CFO of (₹15 cr).

In such a financial situation, it seems that the money for the dividend payout has come from the funds provided by shareholders themselves, and it is not from the cash flow generated by the business of the company.

We believe that when dividends are not funded by the free/surplus cash flows generated by the business and instead are funded by debt or equity, then shareholders should not take comfort in such dividend yield because these dividends can stop at any time.

7) Long time taken in project execution by Lloyds Metals and Energy Ltd:

Due to one reason or another, almost always, the projects announced by Lloyds Metals and Energy Ltd have taken a very long time to get completed.

For example, the company had started work on the expansion of its sponge iron plant with a waste-heat recovery (WHR) power plant in FY1997.

FY1997 annual report, page 6:

Company has already taken up the work of the Second Phase to double the capacity of the Sponge Iron Plant and to install a Captive Power Plant of 12MW.

However, immediately in the next year, the work on the project became slow due to a change in the technology of the plant.

FY1999 annual report, page 5:

The work on sponge iron second phase to enhance production capacity alongwith captive power plant of 12 MW is progressing slow due to change in plant technology.

Finally, the expansion of the sponge iron plant was completed in FY2006 after 10 years after its commencement in FY1997.

FY2006 annual report, page 5:

SPONGE IRON DIVISION: Company has enhanced the capacity of its plant to 240000 TPA from the existing 150000 TPA. The additional capacity has become operational in a phased manner over the year.

The waste-heat recovery (WHR) plant, which was originally started in FY1997, was completed in FY2011 after about 15 years of commencement.

FY2011 annual report, page 4:

Company has commissioned its 30 MW co-generation Waste Heat Recovery Based (WHRB) Power Plant, at Ghugus, Maharashtra

Another project that witnessed a lot of delays in operationalization is the iron ore-mining project, which we have discussed above. The mine was allocated to the company in 2007; however, ore extraction from the mine commenced only in 2012 that too for a short period before the mining stopped again in June 2013 when Naxals killed one of the employees of the company.

In FY2018, the company announced a mineral-based steel plant at Konsari Village, Gadchiroli for ₹700 cr and expected to complete it by June 2020.

FY2018 annual report, page 9:

SETTING-UP MINERAL BASED STEEL PLANT:…at Konsari Village, Chamroshi Tehsil, Gadchiroli District for manufacturing of Sponge Iron, Electric Power Generation with Waste Heat Recovery Boiler… Company has agreed to make an investment of ₹700 Crores…expected date of commencement of initial production would be 30th June, 2020.

However, the progress of the plant is already delayed. The construction of the project has started in July 2022 after govt. approvals are received.

Corporate presentation, July 2022, page 15:

Work for this project is on in full swing with around 200 construction workers already employed at site…land has been procured and Environmental Clearance for the 1st phase has been received.

In FY2021, the company announced another steel plant, which is supposed to be a megaproject in Ghugus, Chandrapur. The project is expected to cost ₹1,200 cr and will be completed over 8 years in 3 phases.

FY2022 annual report, page 27:

The entire plan would be carried out over 8 years at a total cost of ₹1,200 Crores in 3 Phases.

The focus of the company will be on completing phase 1 costing about ₹185 cr first.

FY2022 annual report, page 27:

Board of Directors have approved the implementation at the earliest of the Phase 1 which consist of installing an Induction Furnace based steel Plant with a capacity to produce 2,50,000 MTPA at a cost of ₹185 Crores

As per the credit rating agency, Brickwork, phase 1 should commence production in July 2023.

Credit rating report by Brickwork, August 2021, page 4:

The construction for Phase I is expected to commence in November 2021 and the commercial operation shall commence from July, 2023. The total project outlay is estimated at Rs. 185.00 crores

An investor needs to closely track the developments related to these large projects announced by the company at Konsari, Gadchiroli and Ghugus, Chandrapur as well as other projects worth ₹20,000 cr for which it has received govt. approval.

Corporate announcement, BSE, December 14, 2022, page 1:

Maharashtra State’s cabinet sub-committee on industries on Tuesday, 13th December, 2022 cleared 13 projects worth Rs 70,000 crore…of which it has cleared a project worth Rs. 20,000 crores by Lloyds Metals and Energy Limited. The Company would first like to clarify that these approvals are preliminary and require a series of regulatory and internal approvals.