The current section of the “Analysis” series covers Polycab India Ltd, India’s largest manufacturer of cables and wires. The company also manufactures fans, lights, switches, and optical fibre cables, as well as do engineering, procurement and construction (EPC) work for electricity and data transmission projects.

“Analysis” series is an attempt to share with all the readers, our inputs to the company analysis submitted by readers on the “Ask Your Queries” section of our website.

To benefit the maximum from this article, an investor should focus on the process of analysis instead of looking for good or bad aspects of the company. She should learn the interpretation of different types of data and transactions and pay attention to the parts of annual reports etc. used to get the information. This will help her in improving her stock analysis skills.

Polycab India Ltd Research Report by Reader

Sir,

I have analysed Polycab India Ltd and I am sharing my detailed analysis of it. It has been screened from Screener using some financial parameters. I hope that you will add your response and add it to the company analysis section of your website.

Thank you,

P Varun Kasyap

Financial Analysis:

Let us start with the financial analysis. I am using consolidated statements. Most of the ratios are comfortable enough for an investor to invest in the long term.

- Sales Growth: Past 5 years’ sales growth is 13.4%. Past 3 years’ sales growth is 17.1%

- EPS Growth: Past 5 years’ EPS growth is 34.3%. Past 3 years’ EPS growth is 45.7%

The main reason for this growth is an increase in net profit margin. OPM (operating profit margin) is growing good. Whereas NPM (net profit margin) has increased significantly from 3% to 9% in the last 5 years.

Operating Efficiency:

- Net Fixed Asset Turnover ratio declined significantly from 10.63 to 5.99 from Mar-14 to Mar-15. Then, it went to 6.55 till Mar-20.

- The inventory turnover ratio declined from 6.3 to 4.5 in the last 5 years.

- Receivable days decreased from 79 to 57.

- Most of the time, CFO is greater than its PAT.

By keeping these things, one can say that operating efficiency is average.

The margin of safety in business:

Self-sustainable growth rate (SSGR): SSGR of Polycab India ltd is 28%, which says that there are good chances of growth sustainability. It indicates that it has been able to manage its growth story without leveraging its balance sheet. It has a minuscule amount of debt on its book as reflected by its debt to equity ratio of 0.05.

Free cash flow (FCF) analysis: In the last 7 years, it has generated positive FCF 2 times. However, cash flow numbers indicate good FCF numbers in future. To generate positive FCF, either CFO should increase or capex should decrease. Once we see it keenly, most of the time, CFO is greater than PAT. If the CFO decreases, the FCF number would be negative. Therefore, we need to care for CFO numbers. In addition, depreciation is increasing every year. It will increase capex.

The margin of safety in market price:

Polycab India Ltd is trading at a P/E ratio of 24.4, which does not offer any margin of safety according to Benjamin Graham in the book, The Intelligent Investor. I do not use the discounted cash flow (DCF) model or any other models in the analysis process of valuation.

I do not say that it is undervalued. I can say that it is trading at some premium. One should remember that such a P/E ratio is ok. My experience says that, if a good growing company has a low P/E (less than 12.5), then we can understand that the business or the company has some issues. Such a P/E ratio is normal for a growing company. In addition, one should not make investment decisions only depending on the P/E ratio.

Next, we go with business analysis.

Business analysis:

Its main business is wires and cables. Copper and aluminium are the main raw materials needed. Change in copper and aluminium prices will affect its raw material costs. One needs to track copper and aluminium prices also.

We can understand that Polycab India Ltd has a major market share in the cables and wires sector and it is growing in market share in the electric components sector. One needs to track the market these metrics.

Let us have a look at credit rating reports: We have three credit rating reports from CRISIL. The short-term credit rating is the highest-rated (A1+) and the long-term rating upgraded from AA (stable) to AA (positive) in the last 3 years, which indicates that it is safe to give a loan to Polycab India Ltd.

Comment on management: I have no issues with the management. I did not find any kind of cases filed against management. In addition, I feel that the management’s integrity is good and they can take the company to higher positions. Moreover, the percentage of pledged shares is 0%.

Comments on the industry: The industry is growing very good and the demand for wires and cables is growing very good. Therefore, I have a very positive opinion of the industry.

Thank you,

P Varun Kasyap

Dr Vijay Malik’s Response

Dear Varun,

Thanks for sharing the analysis of Polycab India Ltd with us! We appreciate the time & effort put into the analysis.

Polycab India Ltd had come up with an initial public offer (IPO) in April 2019. Its red herring prospectus (RHP, click here) contained financial information from FY2014 onwards. Therefore, financial databases like Screener have financial data of Polycab India Ltd from FY2014 onwards on their websites.

While analysing the history of Polycab India Ltd, an investor notices that over the years, the company had many subsidiaries and joint ventures both in India and overseas to conduct its business. As per the Q3-FY2022 results announcement, pages 2-3, on December 31, 2021, Polycab India Ltd had eight subsidiaries and one joint venture (JV) company after excluding Ryker Base Private Limited, which it sold to Hindalco Industries Ltd during the quarter.

We believe that while analysing any company, an investor should always look at the company as a whole and focus on financials, which represent the business picture of the entire company including its subsidiaries, joint ventures etc. The consolidated financials of a company present such a picture.

Further advised reading: Standalone vs Consolidated Financials: A Complete Guide

Therefore, in the case of Polycab India Ltd, we have analysed consolidated financials from FY2014 onwards.

With this background, let us analyse the financial performance of Polycab India Ltd.

Financial and Business Analysis of Polycab India Ltd:

While analyzing the financials of Polycab India Ltd, an investor notices that the sales of the company have grown at a pace of 12% year on year from ₹3,986 cr in FY2014 to ₹8,927cr in FY2021. Further, the sales of the company have increased to ₹11,297 cr in the 12-months ended December 31, 2021, i.e. during Jan. 2021-Dec. 2021.

While analysing the sales growth of the company, an investor notices that the sales of the company increased every year since FY2014.

On similar lines, while analysing the profitability of Polycab India Ltd, an investor notices that the operating profit margin (OPM) of the company has also increased consistently from FY2014 until FY2021. The OPM of Polycab India Ltd increased from 7.5% in FY2014 to 13.1% in FY2021. The OPM of the company declined only on two occasions. First, during FY2017 when the OPM declined to 8.7% from 9.5% in FY2016 and second, during the 12-months ended December 31, 2021, i.e. during Jan. 2021-Dec. 2021 when the OPM declined to 10.7% from 13.1% in FY2021.

To understand the reasons for the financial performance of Polycab India Ltd, an investor needs to read the publicly available documents of the company like annual reports, conference calls, credit rating reports, red herring prospectus as well as its corporate announcements. Then she would understand the factors leading to the increase in its revenue and profit margins as well as the reasons for the decline in profitability in certain periods.

After going through the above-mentioned documents, an investor notices the following key factors, which influence the business of Polycab India Ltd. An investor needs to keep these factors in her mind while she makes any predictions about the performance of the company.

1) Intense competition with a continuous pricing pressure:

The cables and wires, as well as the electrical goods industry, are highly fragmented and competitive where the unorganized sector constitutes a significant part of the industry. Almost 50% of the wires segment is under unorganized players.

FY2020 annual report, page 41:

In segments like wires, where unorganised make nearly half of market.

Similarly, other segments of Polycab India Ltd. also have a significant presence of unorganized players as well as other organized players. All these players create intense competition in the industry, which dilutes the pricing power of companies.

Credit rating report for Polycab India Ltd. by CRISIL, July 2018, page 1:

Exposure to intense competition: The house wires and electrical cables segment is highly fragmented with a large number of unorganised players, constraining the pricing power of organised sector players. Apart from unorganised sector, PWPL also faces competition from organised sector players such as Havells India Ltd, Finolex Cables Ltd, and Kei Industries Ltd.

Polycab India Ltd acknowledged that for standardized/commoditised products, there is intense pricing competition and the company has to sell goods at a cheaper price to gain business.

RHP, April 2019, page 519:

For our more commoditized products, we compete primarily on price and our profitability depends on our ability to effectively manage our expenses, leverage economies of scale and secure large order volumes.

The price competition is so intense in some of the product segments like lighting that there has been price erosion over the last few years.

FY2020 annual report, page 42:

The lighting industry…is characterised as a very competitive market, particularly on the price front, due to aggressive pricing by some large players and subsequent retaliation by others.

Further advised reading: How to do Business Analysis of a Company

2) Very high dependence of Polycab India Ltd on basic commodities:

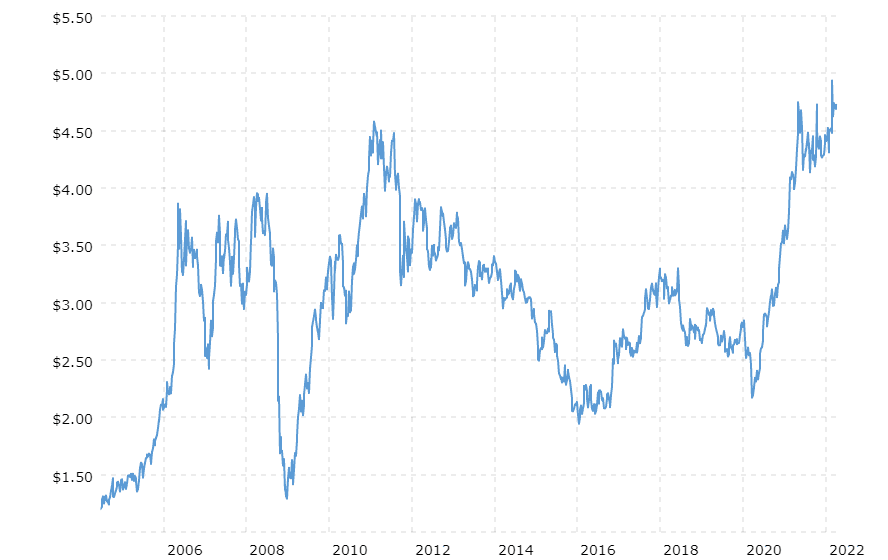

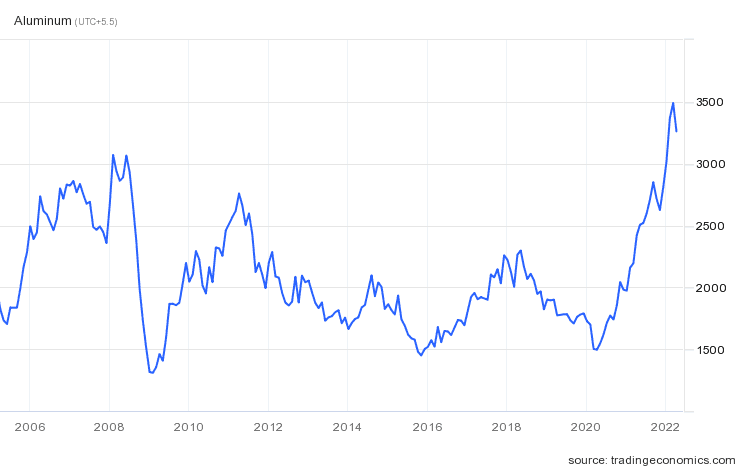

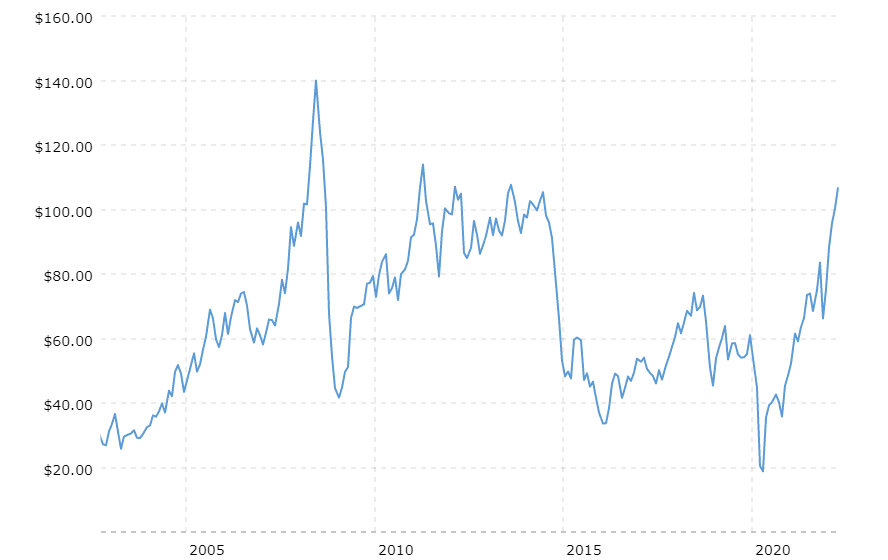

While analysing the financial performance of Polycab India Ltd, an investor notices that a major portion of its raw materials is basic commodities like copper and aluminium. In addition, it uses polyvinyl chloride (PVC), which is dependent upon crude oil.

The section “Details of Material Consumed” in the FY2021 annual report, page 199 shows that on a consolidated basis, copper (61.5%), aluminium (15%) and PVC (13%) constitute about 90% of overall raw material cost for Polycab India Ltd. Therefore, any change in the prices of these commodities puts a significant challenge for the company.

The prices of commodities like copper, aluminium as well as crude oil fluctuate significantly and follow a cyclical pattern of a rise and fall.

The following chart of copper prices from 2005 to 2022, taken from Macrotrends, shows a very high degree of cyclicity with prices fluctuating from $1.5 to $4.5 per pound.

Similarly, aluminium prices have also shown wide fluctuations from $1,500 to $3,500 per tonne from 2006 to 2022 (source: tradingeconomics).

During the same period, crude oil prices, which affect PVC prices, fluctuated from $20 to $110 per barrel while crossing $140 per barrel in 2008.

Therefore, an investor would appreciate that the input cost of almost 90% of Polycab India Ltd.’s raw material fluctuates wildly. Managing profitability with such sharply fluctuating input costs in an industry with intense competition becomes a challenge for any company.

However, when an investor notices the operating profit margin (OPM) of Polycab India Ltd., then she notices that the company has not only maintained its profitability; in fact, it has improved its OPM over the years.

Let us see how the company has been able to maintain its profit margin in the face of fluctuating input costs.

3) Flexibility to fix prices of inventory up to 90-days after purchase:

Polycab India Ltd. gets a period of 90-days from its suppliers after the purchase of copper and aluminium to fix the final price of purchase. This 90-day window/flexibility helps the company in reducing the impact of volatile copper and aluminium prices.

Red herring prospectus (RHP) of Polycab India Ltd., April 2019, page 210:

Since the selling prices of our products are affected by the prices of our primary raw materials, strong and rapid fluctuations in the prices of these raw materials and the inability to pass on the cost increase to our customers could negatively affect our operating results. To manage such risks, we have agreements with a majority of our suppliers, pursuant to which we typically have a 90-day window to price our products from the time of raw material procurement, primarily relating to our copper and aluminium products. This allows us to factor in the costs of the raw materials when we enter into any sales contracts and accordingly pass on any increase in the prices of raw materials to our customers.

Let us see how the flexibility window in pricing helps Polycab India Ltd.

For example, let us assume that Polycab India Ltd. buys copper on January 1 and the supplier ships the copper to the company without fixing the final price of copper. If on January 1, the price of copper on the LME (London Mercantile Exchange) is $3.00 per pound, then it becomes the provisional purchase price for Polycab India Ltd.

Now, let us assume that the shipment of copper would take about 2-months to reach the company. In the meanwhile, on February 20, Polycab India Ltd. gets an order from its customer when the price of copper on LME is $2.50 per pound. Then due to the flexibility window of 90-days in pricing, Polycab India Ltd. can fix the purchase price of copper at $2.50 per pound and use the same in determining the final price of cables/wires to the customer on February 20th.

In this way, Polycab India Ltd. can enter into contracts with its customers based on current prices on the date of the contract and change the price of its purchased raw materials. It helps Polycab India Ltd. maintain its profit margins. Otherwise, if the final price of copper were fixed at $3.00 per pound for Polycab India Ltd. on January 1 whereas the customer contract is dated February 25 when the copper price is $2.50 per pound, then the customer would be willing to pay a price according to the prevailing lower copper prices. In such a case, Polycab India Ltd. would have to incur a loss of $0.50 per pound on the sale transaction.

However, Polycab India Ltd does not have such pricing arrangements with all of its suppliers. About 90% of purchases are covered under such flexible pricing contracts.

Credit rating report of Polycab India Ltd by India Ratings, April 2016, page 1:

According to management, over 90% of its sales are via this mechanism, and it is hence protected from commodity and forex volatilities to a large extent.

For the remaining purchases, it buys commodities only when it has received an order from the customer so that the customer price as well as raw material buying prices, both represent current commodity prices and the company makes its expected profit margin.

Red herring prospectus (RHP) of Polycab India Ltd., April 2019, page 210:

For most of our other suppliers with whom we do not have such pricing windows, we tend to submit purchase orders for raw materials back-to-back at or around the same time as we receive orders from customers, to help minimize our open raw material positions.

For engineering, procurement and construction (EPC) business, Polycab India Ltd generally keeps price escalation clauses in the contracts, which protects it from raw material fluctuations after the project work has commenced.

Red herring prospectus (RHP) of Polycab India Ltd., April 2019, page 210:

For our EPC business, in which we tend to have longer-term contracts to supply products to our customers, we generally include price variation clauses in our contracts so that the sales price of our products gets adjusted periodically based on a formula that takes into account changes in raw material prices.

Therefore, in the case of large contracts where the company directly deals with the customers (B2B business), it is able to mitigate the variations in the raw material prices by way of flexibility in the pricing of purchased commodities whenever it enters into contracts with customers. For the remaining cases, it buys raw materials back-to-back from customer orders and keeps price escalation clauses in EPC contracts.

Let us see, how the company deals with raw material fluctuations for its B2C segment (retail wire sales and electronic goods), which constituted about 40% of its sales in FY2021.

Credit rating report of Polycab India Ltd by India Ratings, June 2021, page 1:

B2C segment grew by around 700bp yoy to 39.4% in FY21, led by the 20% yoy growth in the housing wires business

Advised Reading: Credit Rating Reports: A Complete Guide for Stock Investors

4) Ability to pass on the increase in raw material cost and foreign exchange variations to customers:

Polycab India Ltd intimated to its shareholders that it has a practice of adjusting the prices to its customers monthly where it passes on all the changes in the commodity prices as well as changes in the foreign exchange.

Conference call, October 2020, page 21:

Gandharv Tongia: Prashant, our business, in our case, it is a simple pass-through generally speaking. So whatever is the increase in copper, copper LME side as well as change in the foreign exchange rate in USD/INR, it generally passed on a monthly basis and that is what we have followed in this quarter as well.

When the changes in the raw material prices are sharp, then it changes the prices to the customers within a month as well.

Red herring prospectus (RHP) of Polycab India Ltd., April 2019, page 213:

When the fluctuation in prices of raw materials goes beyond a certain level during the period concerned, list prices of products are revised as and when required. In this way, any increase or decrease in the prices is passed on to end-customers by adjusting the percentage of discount or list prices with a maximum lag of one month.

Therefore, Polycab India Ltd could maintain its profit margins by regularly passing on the changes in the input costs to its customers. However, an investor notices that the OPM of the company has increased over the years.

One of the reasons for the increase in the OPM is that though the company increased its prices whenever its input costs increased; however when the costs declined, then it did not pass on all the benefits and instead retained some of the benefits, which led to an increase in profit margins.

For example, Polycab India Ltd retained some of the benefits of lower commodity prices in FY2019 due to which, its OPM increased from 10.8% in FY2018 to 11.9% in FY2019.

Conference call, May 2019, page 14:

Ramakrishnan R:…we do not retain the risk of commodity prices within our business. We pass it on. Sometimes it is quite likely for example in a period where commodity prices are coming down, it is possible that we may not pass on the benefit of the commodity price having come down adequately

Therefore, Polycab India Ltd increases its product prices when its input costs increase; however, at times, it did not decrease its prices enough when input costs declined. This practice has contributed to the increased profit margins of the company over the years.

The company has started to give up low margin business, which has contributed to an improvement in profitability.

Conference call, October 2020, page 4:

Gandharv Tongia:…On the domestic side, distribution channel performed better than the institutional business where we had to pass on some margin dilutive business.

In addition, in the electrical goods segment, the focus on the premium products in electrical goods, as well as a phased increase in electrical goods prices to bring them in line with the industry has added to the improved profitability. Initially, to gain a market share, Polycab India Ltd had offered its electrical goods at a discount to its competitors. It is now reducing the pricing gap.

Conference call, October 2020, page 4:

Gandharv Tongia: FMEG segment EBIT margin rose from 3.3% in Q2 FY2020 to 8% in the previous quarter, led by calibrated pricing action, premiumization, productivity improvement

Conference call, June 2021, page 19:

Gandharv Tongia: In the mature product categories within the FMEG, we have already reached to the industry level gross margin, which is give and take 2% points here and there around 30% or thereabout and in the product category which are comparatively smaller within the FMEG basket, there is some scope for improvement in margin.

Other factors leading to improving profit margins include improvement in the sales mix i.e. higher sales of high-margin retail wires and increasing operating leverage where fixed costs are spread across a higher volume of sales and in turn, increase profitability.

Conference call, October 2020, page 7:

Gandharv Tongia: In the Cable and Wire business, the B2C business which is a retail wire is more profitable than the regular B2B Cable Business

Credit rating report by India Ratings, September 2019:

PIL’s margins excluding other income improved -83bp yoy to 11.6% in FY19 owing to improved sales mix, expansion in contribution spread and growth in all segments.

From the above discussion, an investor may think that the pricing decisions are very easy for Polycab India Ltd. It can easily increase prices when the input prices increase and it can choose not to pass on full benefits when input prices decline. However, the cable and wires, as well as the electrical goods industry, are highly competitive where many unorganized and organized players compete for business.

As a result, there are times when despite an increase in raw material costs, it could not pass on the cost increase fully. This is because; the company could have lost business if it increased prices further. The company faced such a situation in the second half of FY2021.

Conference call, January 2021, pages 6 and 10:

Gandharv Tongia: all the raw material prices increased very significantly in the last three months, between September to December quarter. Copper and aluminium, both increased almost by 15%, and PVC has increased almost by 50%. So, what we did is, we took a conscious call not to pass on all the cost inflation, considering the market environment

The company confirmed that it could not increase prices due to high competition.

Conference call, January 2021, pages 6 and 10:

Aditya Bagul: I was just trying to link your comment earlier that you have not passed on the full impact of higher input cost to the customer. So I was just trying to wonder whether it was linked to a higher competitive intensity…hence, we have not passed on the input cost. Is there any truth to that?

Gandharv Tongia: Yes, I think we can attribute a part of it to that.

Once again, in FY2022, the company could not increase prices to its customers for the fear of losing the business.

Conference call, July 2021, page 6:

Gandharv Tongia: On a blended basis the raw material cost would have increased by in early teens whereas the price hike which we have taken is just touching the double digit so there is a bit of a negative delta there

The company accepted that if it increases the prices further, then its goods would become unaffordable for the customer. In addition, there is pricing pressure from competitors; therefore, if it had to gain a market share, then it would have to de-prioritize margin improvement.

Conference call, October 2021, page 4:

Gandharv Tongia: We are trying to cut a fine balance between managing profitability and customer affordability, but overall for this year we believe our main priority will be aggressive market share gains as against margin improvement

As a result, during the 12-months ended December 2021 (i.e. January 2021 to December 2021), the OPM of Polycab India Ltd declined to 10.7% from 13.1 % in FY2021.

As per the company, its operating margins in the core cables & wires business tend to sustain in the range of 11%-13%. An investor may keep the same in her mind while she projects its profit margins in the future.

Conference call, January 2020, page 3:

Gandharv Tongia: Historically, we have noted that our annualised sustainable margin in Wires and Cable business typically tends to hover in the range of 11% to 13%

Further advised reading: How to do Financial Analysis of a Company

5) Shifting of business from the unorganized sector to the organized sector:

Polycab India Ltd has managed to increase its revenue every year since FY2014. This is despite intense competition in the cable & wires as well as the electrical goods industry from the unorganized sector as well as other organized players.

One of the main reasons for it has been a continuous shift of the business from the unorganized sector to the organized sector.

Conference call, January 2020, page 7:

Gandharv Tongia: Almost five years back as you know unorganised sector was almost 39% of the total industry, last year it was almost 34% as per one independent study, and it appears that it would be close to 26% by 2023.

Apart from the better quality of products and the service from organized players, other factors like implementation of goods and services tax (GST) as well as policy measures like mandatory star rating of appliances have also contributed to the shift of business from the unorganized sector to the organized sector.

FY2020 annual report, page 42:

During the year, growth in unorganised sector was muted. Implementation of GST and star rating becoming mandatory further hampered the unorganised trade thereby reducing price pressure for organised players.

In addition, in recent times, the coronavirus pandemic has made it very difficult for the unorganized sector to sustain its business, which has increased the shift of business to the organized sector.

Conference call, January 2021, page 9:

Gandharv Tongia:…share of unorganized participant is reducing over the period and I think the rate of reduction has hastened in last few years. It started with demonization and then the GST, but particularly because of the pandemic, availability of capital, cost of capital and availability of labour probably pushed the unorganized sector to a point where recovery is very difficult for them. So that is where on the large players, including us, are gaining some market share.

As a result, Polycab India Ltd has seen its business increase in size over the years assisted by the shifting of business from the unorganized segment to the organized segment.

From FY2014 to FY2021, the company has improved its business by increasing both its revenue as well as its profitability. However, in recent times, it has faced challenges in maintaining its profit margins due to very high competition. Going ahead, an investor should keep a close watch on the profit margins of the company to assess whether the company continues to maintain its competitive advantages.

While analysing the tax payout ratio of Polycab India Ltd., an investor notices that from FY2014 to FY2020, the tax payout ratio of the company has been in line with the standard corporate tax rate prevalent in India. Until FY2019, it was above 30% and in FY2020; it was 24% in line with the reduced corporate tax rate in India. However, in FY2021, the company reported a tax payout ratio of 17%, which is much lower than the standard corporate tax rate.

The tax payout ratio in FY2021 is low because the company won a dispute against the Income Tax Dept. for a total consideration of about ₹100 cr.

FY2021 annual report, page 178:

During the year, the Parent Company had received a favourable order from Honourable Income-Tax Appellate Tribunal for AY 2012-13 to 2015-16 resulting into write back of income-tax provision of ₹839.52 million and recognition of interest on income tax refund of ₹163.89 million.

Advised Reading: How to study the Annual Report of a Company

Operating Efficiency Analysis of Polycab India Ltd:

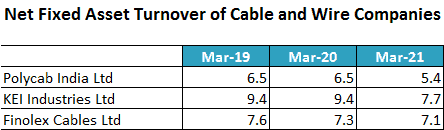

a) Net fixed asset turnover (NFAT) of Polycab India Ltd:

Over FY2015-FY2021, the net fixed asset turnover (NFAT) of Polycab India Ltd has stayed in the range of 5.2 to 6.5.

When comparing the NFAT of Polycab India Ltd with its peers, KEI Industries Ltd and Finolex Cables Ltd, an investor notices that the company’s NFAT is lower than its peers who have NFAT in the range of 7.0 to 9.5.

The key reason for a lower NFAT for Polycab India Ltd is the policy of the company to prefer to make most of its products in-house instead of outsourcing them. The company believes that it can produce the best quality of products when it makes them in-house.

Conference call, January 2020, page 7:

Gandharv Tongia: We as a company firmly believe in in-house manufacturing. Over the last few years, we have carried out several steps to ensure that we have adequate backward integration in place…The mindset and the thought process of the company is to ensure that we get the best quality

As per the company, field returns of its products i.e. the return of faulty products is the lowest in the industry.

Conference call, July 2021, page 18:

Gandharv Tongia:..third is in-house production which gives us confidence on the quality as well as the value for money for our consumers. You will be pleased to note that our field returns in fans are lowest in the industry because of the quality

As Polycab India Ltd prefers to manufacture its products in-house, it makes its operations relatively capital-intensive than its peers who may follow an asset-light strategy and outsource the production of goods. Therefore, Polycab India Ltd has a lower NFAT indicating a relatively asset-heavy business.

As a part of its in-house manufacturing strategy, Polycab India Ltd invested in a copper-rods manufacturing plant as a joint venture with Trafigura, which had a production capacity over Polycab’s requirements.

Credit rating report of Polycab India Ltd by India Ratings, May 2020:

PIL would consume about half of Ryker’s production capacity to meet its copper requirement while the balance would be sold through various tolling or partnership opportunities.

However, soon after the completion of this plant, Trafigura exited this business and Polycab India Ltd acquired its stake to own the whole plant.

Conference call, May 2020, page 6:

Gandharv Tongia: However, post Trafigura’s recent global strategic decision to exit from value added manufacturing businesses in India where it is a JV partner, their 50% stake was offered to us and we decided to acquire it making Ryker a wholly owned subsidiary of our company.

However, Polycab India Ltd could not sell the excess copper-rods capacity in the market. As a result, it became a pain point for the company because it was not able to run it to optimal capacity utilization resulting in very low profitability of the copper-rods plant.

Conference call, January 2021, page 10:

Gandharv Tongia: we have a small copper business which has significantly lesser contribution margin

Conference call, October 2021, page 10:

Gandharv Tongia: We are using broadly 1/3 of this total capacity and that is where this particular capacity is underutilized. We are exploring ways and means to either improve the capacity utilization by improving the internal consumption or looking for third party tie up through job work or other arrangement to improve the margins and cost of operation there.

As a result, the company had to sell the copper-rods business to Hindalco Industries Ltd.

Therefore, going ahead, an investor should monitor the capital allocation projects where the company may enter into projects where it may land up with a manufacturing capacity far more than its own consumption. This is because even though, it could sell the copper-rods plant at a profit to Hindalco, it may not find a profitable deal for the excess production.

Further advised reading: Asset Turnover Ratio: A Complete Guide for Investors

b) Inventory turnover ratio of Polycab India Ltd:

The inventory turnover ratio (ITR) of Polycab India Ltd has declined from 6.3 in FY2015 to 4.6 in FY2021. The ITR witnessed a sharp decline over FY2015-FY2017 when it reduced to 4.4 in FY2017. A declining ITR indicates that the inventory utilization efficiency of the company is declining over the years.

After its IPO in 2019, the company received strong feedback from market participants that it needs to work on improving its inventory utilization. The company acknowledged the same and even hired a consultant to work on improving inventory efficiency.

Conference call, July 2019, page 10:

Gandharv Tongia: Having said that, inventory is a focused area, we want to reduce it. We have started taking several management initiatives including hiring of the third-party management consultant

The company aimed to reduce its overall inventory holding and also increase the number of items it kept within that reduced inventory.

Conference call, May 2020, page 8:

Gandharv Tongia: The objective was twofold, one is reducing the absolute amount of inventory which we are carrying on our books so that we can reduce the working capital involved. The second is, within that reduced amount, increase the number of SKU. So, you increase the availability and you reduce the amount, so you get twin benefits. That project is progressing well. We have already achieved a bit of success

Even though the company claimed to achieve success, if a person measures the inventory turnover ratio (ITR), then she notices that the steps of the company are yet to produce a significant result.

Further advised reading: Why We cannot always Trust What Management Claims

One of the key reasons for a lower inventory turnover or maintaining a large amount of inventory by Polycab India Ltd is that the company prides itself on the quickest delivery of goods to its customers.

Conference call, July 2021, page 9:

Gandharv Tongia: The other thing is, generally speaking, we have ability to provide the required material just in time or within a day or two and that is a significant differentiator between us and our peers in the industry.

If a company has a very wide range of products and it aims to make quick delivery of goods, then it has to maintain a large amount of inventory in its warehouses and distribution channel, which makes its operations working capital intensive.

Credit rating report of Polycab Industries Ltd by CRISIL, April 2019:

Working capital intensity is higher than industry peers

The company has to balance the target of inventory reduction with ensuring quick availability of goods to the market, which is its key competitive advantage. The company seems to prefer quick delivery as it benefits the customers. Therefore, it may be a challenge for the company to sharply reduce the inventory holding.

Conference call, June 2021, page 14:

Gandharv Tongia: But to answer your question that whether the inventory can be further optimized or not I believe that yes certainly it can be further optimized but what we want to at the same time ensure is that we increase the availability because that is the clear differentiator for us at every market place. And the OTIF or on time in full delivery is generally between 95% and 98% as of now which has improved significantly I would say over the last three to four years and we as a company would like to reach to 100%.

Going ahead, an investor should keep a close watch on the inventory utilization efficiency of Polycab India Ltd to understand if it is able to bring any improvement in the same or if the cost of management consultants is an added financial burden for the shareholders.

Further advised reading: Inventory Turnover Ratio: A Complete Guide

c) Analysis of receivables days of Polycab India Ltd:

Receivables days of Polycab India Ltd have improved significantly from 79 days in FY2015 to 59 days in FY2021.

Polycab India Ltd has used channel financing to improve its receivables position in which it receives the money from the bank within 3 working days of supplying goods to the customers. In turn, the bank collects the money from the customers when it is due as per the payment terms. Otherwise, previously in FY2014 and FY2013, the receivables days were even higher at 86 days and 104 days respectively.

Credit rating report of Polycab India Ltd by India Ratings, January 2015:

Sustained Improvement in Working Capital: PWPL has been able reduce its working capital cycle significantly over the past three years…This is attributable to lower debtors days (FY14:86 days, FY13: 104 days) on account of higher use of the channel financing facility

A sharp improvement in the receivables days during FY2016-FY2018 was also due to the higher use of channel financing.

RHP, April 2019, page 537:

Our Debtor Days has decreased from 89 days in Fiscal 2016 to 72 days in Fiscal 2018, primarily due to our increased use of channel financing

Polycab India Ltd is encouraging its customers/dealers to opt for channel financing by giving incentives like cash discounts.

RHP, April 2019, page 211:

we offer a cash discount of up to 3% of the total invoice amount if the relevant dealer or distributor makes advance payment to us prior to dispatch or adopt channel financing.

As a result, the share of channel financing in its receivables has been consistently on the rise. As per the latest available data from the January 2022 conference call, channel financing has increased to about 70% in the cable & wire business and about 50% in the electrical goods business. The company aims to improve it further so that its working capital position becomes better.

Conference call, January 2022, page 9:

Gandharv Tongia:…advance plus channel finances put together in cable and wire we would be around 70% of our top line. In FMEG business, it has improved reasonably well and we are in late 40s, almost just shy of 50%. Theoretically speaking, this number can go right up to 80s and 90s

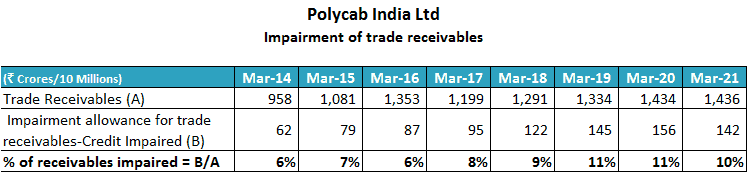

Apart from the early receipt of money, Polycab India Ltd seems to prefer channel financing for another important reason. Over the years, Polycab India Ltd seems to have faced challenges in collecting receivables from its customers/dealers. At any point in time, about 10% of its overall receivables are credit impaired i.e. there is a doubt that the company may not collect them.

In such a situation, the use of channel financing helps Polycab India Ltd avoid the credit risk associated with the collection of receivables. This is because in channel financing, the credit risk i.e. risk of loss of receivables is taken over by the bank.

RHP, April 2019, page 25:

we have increased our use of channel financing in recent years, whereby our customers enter into arrangements with banks through which we receive payment directly from the banks, who in turn take on credit risk and seek to collect outstanding dues from the customers. Channel financing reduces our risk of non-payment

Therefore, channel financing helps Polycab India Ltd to receive money fast and prevents the risk of non-payment by customers. As a result, the company is happy to provide cash discounts to any customer who starts using channel financing.

Polycab India Ltd does not disclose the ageing schedule of receivables in its annual reports; therefore, an investor is not able to ascertain the level of delays done by its customers in payments to the company.

One business segment of the company, which has a history of delays in receivables is the engineering, procurement and construction (EPC) segment. However, the company has stated that it does not want to grow this business. Instead, it wants this segment to support its business of cable & wires as it bids only for those EPC contracts, which have about 50% cable component.

Conference call, January 2020, page 7:

Gandharv Tongia: We know for sure that we are not an EPC company and we do not want to operate as such. The only thing is, we get operational advantage and leverage when we get into EPC for our main Cable and Wire business

Conference call, July 2019, page 14:

Ramakrishnan R.: What we try to do is pick up orders where the cable content is around 40% or 50%.

Therefore, the company has clearly stated that it is not going to grow the EPC business significantly.

Conference call, May 2019, page 6:

Ramakrishnan R.:…as a matter of our philosophy, EPC for us is a tactical business, we are not aiming to take that business to Rs. 1000 Crores – Rs. 2000 Crores, I think we will be ballpark in the vicinity of Rs. 200 Crores or thereabouts and that is where we will be.

Going ahead, an investor should keep a close watch on the credit-impaired receivables and the write-off of bad debt to assess whether Polycab India Ltd is able to collect its money on time.

Further advised reading: Receivable Days: A Complete Guide

When an investor compares the cumulative net profit after tax (cPAT) and cumulative cash flow from operations (cCFO) of Polycab India Ltd for FY2014-21, then she notices that over the years (FY2014-FY2021), the company has converted its profit into cash flow from operations.

Over FY2014-21, Polycab India Ltd reported a total net profit after tax (cPAT) of ₹3,170 cr. During the same period, it reported cumulative cash flow from operations (cCFO) of ₹4,052 cr.

It is advised that investors should read the article on CFO calculation, which would help them understand the situations in which companies tend to have the CFO lower than their PAT. In addition, the investors would also understand the situations when the companies would have their CFO higher than the PAT.

Further advised reading: Understanding Cash Flow from Operations (CFO)

Learning from the article on CFO will indicate to an investor that the cCFO of Polycab India Ltd is higher than the cPAT due to the following factors:

- Depreciation expense of ₹1,029 cr (a non-cash expense) over FY2014-FY2021, which is deducted while calculating PAT but is added back while calculating CFO.

- Interest expense of ₹729 cr (a non-operating expense) over FY2014-FY2021, which is deducted while calculating PAT but is added back while calculating CFO.

The Margin of Safety in the Business of Polycab India Ltd:

a) Self-Sustainable Growth Rate (SSGR):

Read: Self Sustainable Growth Rate: a measure of Inherent Growth Potential of a Company

Upon reading the SSGR article, an investor would appreciate that if a company is growing at a rate equal to or less than the SSGR and it can convert its profits into cash flow from operations, then it would be able to fund its growth from its internal resources without the need of external sources of funds.

Conversely, if any company attempts to grow its sales at a rate higher than its SSGR, then its internal resources would not be sufficient to fund its growth aspirations. As a result, the company would have to rely on additional sources of funds like debt or equity dilution to meet the cash requirements to generate its target growth.

An investor may calculate the SSGR using the following formula:

SSGR = NFAT * NPM * (1-DPR) – Dep

Where,

- SSGR = Self Sustainable Growth Rate in %

- Dep = Depreciation rate as a % of net fixed assets

- NFAT = Net fixed asset turnover (Sales/average net fixed assets over the year)

- NPM = Net profit margin as % of sales

- DPR = Dividend paid as % of net profit after tax

(For systematic algebraic calculation of SSGR formula: Click Here)

While analysing the SSGR of Polycab India Ltd, an investor would notice that over the years, the company had an SSGR in the range of 12%-18%, which has increased further in recent years as its NPM has improved. Over the years, the company has grown its sales at a rate of 10%-12%. Therefore, Polycab India Ltd has grown its sales within its SSGR. As a result, the company has managed to grow its business without raising a lot of external capital.

Polycab India Ltd came out with an initial public offer (IPO) in April 2019 and raised a total of about ₹1,345 crores. Out of it, ₹400 cr was a fresh issue of shares i.e. the money that was received by Polycab India Ltd and the remaining about ₹945 cr was an offer for sale i.e. existing investors sold the shares and received the money.

On a previous occasion, during FY2010, the company had raised about ₹400 cr by selling a 15% stake in the company by way of issuing equity shares and compulsory convertible debentures (CCDs). The CCDs were converted into equity shares in FY2013 (RHP, April 2019, page 227).

Even though, Polycab India Ltd raised an additional capital as equity; however, over FY2014-FY2021, it reduced its debt by ₹209 cr i.e. its total debt decreased from ₹458 cr to ₹249 cr (458 – 249 = 209). In addition, the company has increased its cash & investments by about ₹1,116 cr as its cash position increased from ₹50 cr in FY2014 to ₹1,166 cr in FY2021. Moreover, the company also paid out dividends (excluding distribution tax) of ₹355 cr over FY2014-FY2022.

Therefore, even though the company raised equity of ₹400 cr from IPO; however, it seems that the company did not need the money desperately and its business could generate sufficient cash to sustain its growth aspirations.

An investor arrives at a similar conclusion when she analyses the free cash flow (FCF) position of Polycab India Ltd.

b) Free Cash Flow (FCF) Analysis of Polycab India Ltd:

While looking at the cash flow performance of Polycab India Ltd, an investor notices that during FY2014-2021, it generated cash flow from operations of ₹4,052 cr. During the same period, it did a capital expenditure of about ₹2,265 cr.

Therefore, during this period (FY2014-2021), Polycab India Ltd had a free cash flow (FCF) of ₹1,787 cr (=4,052 – 2,265).

In addition, during this period, the company had a non-operating income of ₹478 cr and an interest expense of ₹729 cr. As a result, the company had a total free cash flow of ₹1,536 cr (= 1,787 + 478 – 729). Please note that the capitalized interest is already factored in as a part of the capex deducted earlier.

Polycab India Ltd has used this money in payment of dividends as well as reduction of debt. Moreover, the remaining money is available with the company as cash & investments of ₹1,166 cr at the end of FY2021.

Going ahead, an investor should keep a close watch on the free cash flow generation by Polycab India Ltd to understand whether the company continues to generate surplus cash from its operations.

Further advised reading: Free Cash Flow: A Complete Guide to Understanding FCF

Self-Sustainable Growth Rate (SSGR) and free cash flow (FCF) are the main pillars of assessing the margin of safety in the business model of any company.

Further advised reading: 3 Simple Ways to Assess “Margin of Safety”: The Cornerstone of Stock Investing

Additional aspects of Polycab India Ltd:

On analysing Polycab India Ltd and after reading annual reports, RHP, its credit rating reports and other public documents, an investor comes across certain other aspects of the company, which are important for any investor to know while making an investment decision.

1) Management Succession of Polycab India Ltd:

Polycab India Ltd is a part of the Jaisinghani family where until recently, three brothers Inder T. Jaisinghani, Ajay T. Jaisinghani and Ramesh T. Jaisinghani had been running the company.

RHP, April 2016, page 237:

Other than Inder T. Jaisinghani, Ajay T. Jaisinghani and Ramesh T. Jaisinghani being brothers, there is no family relationship among our Directors.

As a part of succession planning, the sons of all the three promoters, Bharat A. Jaisinghani, Kunal I. Jaisinghani and Nikhil R. Jaisinghani have joined the company in various positions.

RHP, April 2016, page 246:

Bharat A. Jaisinghani, Kunal I. Jaisinghani and Nikhil R. Jaisinghani are cousins, and sons of our Promoters, namely Ajay T. Jaisinghani, Inder T. Jaisinghani and Ramesh T. Jaisinghani, respectively.

In May 2021, two promoter brothers, Mr Ajay Jaisinghani and Mr Ramesh Jaisinghani resigned from the board and their sons Mr Bharat Jaisinghani (age 38 years), Mr Nikhil Jaisinghani (age 36 years) took over the board position.

Conference call, June 2021, page 8:

Gandharv Tongia: On the Executive directors’ side Mr Ajay Jaisinghani, Mr Ramesh Jaisinghani and Mr Shyam Lal Bajaj have stepped down from the board and Mr Bharat Jaisinghani, Mr Nikhil Jaisinghani and Mr Rakesh Talati have been appointed as Executive Directors…This change was a part of our larger succession planning. Bharat and Nikhil have been working in different areas of sales, marketing, production, IT etc. for nearly a decade now.

The third promoter-brother, Mr Inder T. Jaisinghani (age 68 years) is currently serving as the chairman & managing director of the company and his son Mr Kunal I. Jaisinghani is working as the head of agri-products in the company (FY2021 annual report, page 43).

Apart from the promoter brother and their sons, other members of the family are also working in the company like Mr Anil Hariani who is the nephew of the promoter brothers and is working as Director – Commodities in the company (FY2021 annual report, page 42).

RHP, April 2019, page 246:

Anil H. Hariani is a nephew of our Promoters and is a cousin of Bharat A. Jaisinghani, Kunal I. Jaisinghani and Nikhil R. Jaisinghani.

Therefore, an investor would note that currently, the next generation of promoter-brothers has also joined the company and been working for Polycab India Ltd for a significant amount of time.

The presence of younger family members at executive positions within the group, while the senior members are still handling responsibilities, looks like a good succession plan. This is because the young members can learn about the fine nuances of the business under the guidance of senior members until the seniors decide to take retirement.

Going ahead, an investor may keep a close watch on the relationships among the promoter’s family members to understand whether any ownership issues arise between them. An investor may contact the company directly for any clarifications in this regard.

Further advised reading: How to do Management Analysis of Companies?

2) Project execution by Polycab India Ltd:

In its annual reports, the company does not provide details with respect to each expansion project under execution in terms of the scope of the project, its total cost and expected time of completion. Instead, it only provides a broad overview like next year, it is going to spend say ₹300 cr in capex, out of which about two-third would be for cable & wires division and one-third would be for electrical goods division.

Conference call, June 2021, page 10:

Gandharv Tongia: On the capex, we anticipate that we would incur about Rs.300 Crores odd this fiscal, and around 35% will go for FMEG. This would include, say for example, new capex on fan factory, TPW factory as well as factories for pipes and all that. So that is around 35%. Balance would have a combination of a bit of a backward integration as well as cable and wire facilities…There would be some slight maintenance costs and all that but overall the capex would be around Rs.300 Crores thereabout.

Because of non-specific information, it is difficult for an investor to judge whether the company is completing its expansion projects on time or there are delays.

One project, where an investor could get specific information in terms of expected cost and completion time was the copper-rods manufacturing project established under a joint venture (JV) with Trafigura. An investor may assess the execution of this project to have a view of the project execution of Polycab India Ltd.

The company announced the project in the FY2017 annual report when it formed the JV in December 2016.

FY2017 annual report, page 8:

Ryker Base Pvt. LTD. (“Ryker”) a 50:50 Joint Venture between Trafigura PTE LTD. and Polycab Wires Pvt. LTD w.e.f 22.12.2016. The Joint Venture will set up a 225,000 tons copper wire rod plant with an investment of $25mln.

In an interview in October 2017 (source), the company disclosed that it would spend ₹167 cr on the project and commercialize it in Jan-March 2018 quarter.

total investment of about Rs 167 crore ($25 mn)…The manufacturing facility is expected to start commercial production in the first quarter of CY 18.

Thereafter, the project witnessed delays and the credit rating agency India Ratings highlighted that the project would be completed only in Q4-FY2019, indicating a delay of about one year.

Credit rating report by India Ratings, August 2018:

The JV expects the plant to become operational by 4QFY19.

However, the project was further delayed and in the RHP, the company said that it would complete the project in FY2020.

RHP, April 2020, page 195:

We expect the Ryker Plant to commence operations in Fiscal 2020 and once fully operational, the plant will have an annual capacity of 225,000 MT of copper wire rods

In the July 2019 conference call, while discussing the Q1-FY2020 results, Polycab India Ltd intimated to its shareholders that the plant started commercial production in the quarter.

Conference call, July 2019, page 11:

Ryker Plant has commenced production in the current quarter.

Moreover, the credit rating agency, India Ratings, highlighted that the project was completed with an investment of ₹250 cr.

Credit rating report of Polycab India Ltd by India Ratings, May 2020:

Ryker commissioned a 225,000MTPA copper wire rods manufacturing plant in FY20 by incurring capex of around INR2.5 billion which was funded by INR0.52 billion of equity and the balance by debt

Therefore, Polycab India Ltd could complete the copper-rod manufacturing project with a delay of about 15-months and a cost overrun of about 50% (₹83 cr = ₹250 cr – ₹167 cr).

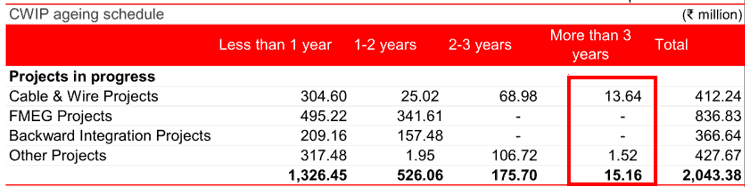

As per the capital work in progress (CWIP)-ageing schedule provided by Polycab India Ltd in its condensed financial statements, the company has expenses lying in CWIP for more than 3-years. Such prolonged continuation of CWIP may indicate time and cost overruns.

Going ahead, an investor may ask the company-specific details about its expansion project in the terms of scope of the project, its expected cost and completion timelines so that she may track whether it is completing its projects within cost and time estimates.

3) History of weak internal controls and compliance:

There have been numerous instances in the past when auditors of Polycab India Ltd and other regulatory authorities have highlighted weaknesses in its processes and decisions.

3.1) Auditor’s observations:

In FY2010, the auditor of the company highlighted that the company has not maintained proper cost records and its internal control system needs strengthening.

FY2010 annual report, page 5:

(vii) The Company has an internal audit system, the scope and coverage of which, in our opinion requires to be enlarged to be commensurate with the size and nature of its business.

(viii) The Company has not maintained the books of account required to be maintained by the Company pursuant to the rules made by the Central Government for the maintenance of cost records

In FY2015, the auditor of the company highlighted that the internal controls are weak and need strengthening.

RHP, April 2019, page 341:

The internal control system for purchase of inventory is adequate except documentation of quotation analysis for Engineering Procurement and Construction (EPC) Business and vendor selection, which needs strengthening in the Company

In addition, the auditor also questioned the inventory records of its work-in-progress.

RHP, April 2019, page 341:

The Company has maintained proper records of inventory except in respect of inventory of work-in-progress

In FY2016, the auditor could not opine about the strength of internal financial control of Polycab India Ltd, as the company could not provide enough documents/evidence to the auditor.

RHP, April 2019, page 273:

Since the company was not able to provide us with sufficient appropriate audit evidence on the system of internal finance control… we are unable to express an opinion on the adequacy or operating effectiveness of Internal Financial Controls over Financial Reporting as at March, 31, 2016.

In FY2017, the auditor could not confirm whether the revenue and receivables are accurate. Instead, the auditor highlighted that internal financial controls were not working properly and there could be over or under accrual of revenue and receivables.

RHP, April 2019, page 273:

The Company’s internal financial control over cut-off procedures for recognition of revenue at the year-end and review of invoices raised for certain category of customers were not operating effectively which could have potentially resulted in under or over accrual of revenue and receivables in the financial statements.

In addition, there have been numerous instances where the company did not deposit undisputed statutory dues like tax deducted at source, employee state insurance, professional tax, value-added tax and the provident fund from FY2014 to FY2018 (RHP, April 2019, pages 524-525). Such delays in the deposit of undisputed statutory dues were also present in FY2010 and FY2019.

3.2) Reserve Bank of India (RBI)’s observations:

In FY2017, RBI pointed it out to the company that it has not complied with FEMA guidelines in issuing shares and compulsory convertible debentures (CCDs) in 2009, 2010 and 2016 by not filing forms FC-GPRs. RBI cautioned the company in this regard and stressed that any future violations would be seen seriously.

RHP, April 2019, pages 51-52:

The acknowledgement letter however noted that the Form FC-GPRs was not filed within the stipulated period which is a contravention of 9(1) (B) of FEMA 20/2000-RB dated May 3, 2000 and further stated that any such failure by us in the future will be viewed seriously by the RBI and the RBI will take appropriate action under FEMA.

Later on, RBI highlighted violations of Overseas Direct Investment (ODI) regulations in the investment by Polycab India Ltd in its Italian subsidiary.

RHP, April 2019, page 30:

on May 5, 2017, RBI issued a memorandum of compounding of contraventions to our Company in respect of alleged violations of Regulation 16A(3) and 15(i) of the ODI Regulations in relation to our Subsidiary, Polycab Wires Italy SRL

4) Huge burden of advertising costs on the electronic goods division:

In 2014, Polycab India Ltd entered the electrical goods business (named FMEG: fast-moving electrical goods). In this segment, it competes with established players like Bajaj, Havells, V-Guard etc.

Electrical goods is a B2C business where the end-consumer directly buys goods in the shops. As a result, creating a brand and acquiring customers’ mindshare is essential in the electrical goods segment.

Polycab India Ltd aspires to be a top player in the electrical goods segment like it is in its other business divisions of cable and wires.

Conference call, January 2021, page 15:

Gandharv Tongia: We were no one when we entered this business, but slowly and gradually we became number one in cable business. Then in 1996, we started wires business, and now we are number one in wires business. So our DNA and our thought process is very clear that if we are in a particular business, we want to become number one

To create a brand in the electronic goods space, Polycab India Ltd has spent a significant amount of money on advertisement & promotions (A&P). Before the start of the electrical goods business, it used to spend about ₹5 cr to ₹10 cr on advertising; however, in recent years, it has to spend about ₹100 cr on advertising every year. The company acknowledges that it has no option but to continue to spend on advertising and that this spending will increase going ahead.

Conference call, October 2020, pages 16-17:

Gandharv Tongia: If I am not wrong, 6, 7 years where you used to spend only Rs.10 Crores on advertisement or probably Rs.5 Crores, but last year we would have invested almost Rs.100 Crores. So that is where we are cautious that for a B2C-oriented business, we have no option but to invest in A&P, and we will continue to do that. And this will only increase in terms of absolute amount in the coming years because the B2C revenue will increase.

However, despite being in this business for more than 7-8 years and spending significant money on advertising & promotions, it is still earning low margins. In Q1-FY2022, the company reported operating losses in the electrical goods division.

Conference call, July 2021, page 10:

Gandharv Tongia: As I mentioned to the earlier participant, it is primarily because of increase in fixed cost and that has also increase in the employee cost or the contractor cost…The second is the A&P spend has slightly increased and A&P predominantly is for our B2C business…So these are two major reasons because of which the EBIT margins have gone into negative trajectory

Going ahead, an investor should closely monitor the margins of the electrical goods division and its spending on advertising to assess whether the spending on advertisement and promotions is leading to any benefits for the business and shareholders.

Further advised reading: How to do Business Analysis of a Company

5) Key risk to the business of Polycab India Ltd:

5.1) Labour unrest:

Manufacturing cables, wires and electrical goods is a labour-intensive process and as a result, cordial labour relations are essential for the company. In the past, Polycab India Ltd had faced instances of labour strikes.

RHP, April 2019, pages 26-27:

Our manufacturing processes are labor intensive in nature…In Fiscal 2017, workmen at our Halol plant went on strike for a period of three weeks.

5.2) Workers’ safety:

The manufacturing process of Polycab India Ltd involves dangerous steps, where any lapses in security measures can lead to loss of property and life. There have been instances where workers lost their lives due to accidents in the factory of Polycab India Ltd.

RHP, April 2019, page 28:

we had an accident at one of our facilities at Daman, where the lid of an autoclave unhooked, resulting in two fatalities and injuries to three of our staff.

5.3) Non-patented, trade secret technology:

Polycab India Ltd has not patented its design and product technology. It is keeping most of it as confidential knowledge. As a result, it has to protect its knowledge on its own and does not have the institution of the patent office to help it.

The company is a large corporate and many employees have access to its confidential technology. Employees keep on leaving the company due to regular attrition. Therefore, the risk of the company losing its design and technology secrets to its competitors is high.

RHP April 2019, page 31:

Our technical knowledge is a significant independent asset, which may not be adequately protected by intellectual property rights. Some of our technical knowledge is protected only by secrecy… A significant number of our employees have access to confidential design and product information and there can be no assurance that this information will remain confidential…The potential damage from such disclosure is increased as many of our designs and products are not patented, and thus we may have no recourse against copies of our products and designs that enter the market subsequent to such leakages.

5.4) Environmental and pollution control regulations risk

The manufacturing processes of Polycab India Ltd involve steps, which are potentially damaging to the environment. The company needs to comply with environmental and pollution control regulations. In the past, the company has received notices for non-compliance with pollution control measures.

RHP April 2019, page 39:

In August 2016, we received a notice from the Gujarat Pollution Control Board in relation to the waste water management of one of our manufacturing facilities in Halol.

Going ahead, an investor needs to closely monitor the compliance of Polycab India Ltd with environmental regulations because any such non-compliance may lead to closure orders from Govt. authorities.

A live example of the closure of a factory due to environmental regulations is the copper manufacturing unit of Sterlite Copper at Thoothukudi, Tamil Nadu.

RHP April 2019, page 27:

in May 2018, one of our copper suppliers was ordered by the Government of Tamil Nadu to seal its copper smelter factory.

5.5) Lack of long-term agreements with suppliers:

Polycab India Ltd does not have long-term supply agreements with its suppliers. As a result, it runs the risk of a shortage of raw material when there is a disruption of the supply chain.

RHP April 2019, page 210:

while we enter into general purchase agreements with our suppliers, we typically do not enter into long-term agreements with our suppliers.

5.6) Land dealings with Govt. authorities:

In one of the instances, Karnataka Govt. allotted a parcel of land on which Polycab India Ltd has its factory, to some other party. The issue is currently under dispute.

RHP April 2019, page 550:

Our Company (“Petitioner”) filed a writ petition…The Petitioner had purchased the Land from a private vendor and subsequently, constructed a part of its industry on the Land. Karnataka Industrial Area Development Board (“KIADB”) has allotted 10 acres of Land including the three acres of the Land purchased by the Petitioner, to Sreedevi Power Industries (“Sreedevi”)…The matter is currently pending.

In another instance, the lease of the factory land at Daman has expired in 2012 and the Govt. authority had not renewed the lease agreement even in 2019.

RHP April 2019, page 40:

Daman and Diu for the lease of the Daman Land expired in the year 2012,…we paid an amount of ₹ 8.01 million as lease rent for the period from June 14, 2012 to January 30, 2015, and further requested the administration of Daman and Diu to grant lease to us. We also filed applications dated January 11, 2013, January 16, 2018 and May 9, 2018…the application for grant and renewal is pending

Moreover, title disputes of another land are under dispute and are pending resolution with Gujarat Govt.

FY2019 annual report, page 106:

title deeds of freehold land amounting to ₹10.48 million is in dispute and is pending resolution with the government authority in Gujarat

An investor may contact the company directly to know the status of these land-related issues.

5.7) Potentially speculative derivative transactions:

As per the condensed financial statements, Q3-FY2022, page 25, Polycab India Ltd has entered into derivative transactions, which are not hedging in nature.

The net value of such potentially speculative transactions was ₹269 cr in FY2021 and ₹32.3 cr on December 31, 2021.

Speculative derivative transactions, which are not hedging in nature, can lead to large losses. Therefore, usually, manufacturing organizations stay away from them.

Polycab India Ltd itself had suffered losses and defaulted against its obligations in a derivative transaction with one of its lenders in 2007-2008.

RHP, April 2019, pages 38-39:

during the years 2007 to 2008, there was a dispute with one of our lenders relating to derivatives transaction which was considered as a default on derivative transaction and working capital facility by the lender.

Going ahead, an investor should closely monitor the exposure of Polycab India Ltd to the derivative instruments, which are not like hedging.

Advised reading: Why Management Assessment is the Most Critical Factor in Stock Investing?

5.8) Contingent liability of commercial dispute:

In the past, Polycab India Ltd had entered into a contract manufacturing agreement with a supplier under which the company had to buy a minimum quantity of switches from the supplier. However, later on, the transaction went under dispute and the supplier sued Polycab India Ltd for an amount of ₹63.4 cr.

RHP, April 2019, page 548:

Sri Krishnashray (India) Private Limited…used the same designs for manufacturing switches (“Switches”) for the Defendant under the brand ‘Cleta’ and ‘Selene’…to affix the name of ‘Polycab’ in consideration of the Defendant purchasing an assured amount of Switches and giving a purchase guarantee of Switches. Subsequently, the Plaintiff filed a suit alleging non-purchase of Switches by the Defendant and thereby praying, inter alia, reimbursement of expenses amounting to an accrued amount of ₹634.21 million together with further interest of 18% per annum, in respect of loss suffered by the Plaintiff.

The matter was under litigation in the High Court of Bombay; however, in the FY2021 annual report, Polycab India Ltd removed this amount from its contingent liabilities stating that the possibility of an adverse decision against the company is remote.

FY2021 annual report, page 208:

A vendor filed a commercial suit against the Parent Company in relation to the alleged breach of three product sourcing agreements entered between the parties. The matter is currently pending in High Court of Bombay. During the current year, based on the legal evaluation, the likelihood of any liability arising on the Company from the outcome of the suit is reassessed from ‘possible’ to ‘remote’.

However, an investor should keep this contingent liability in her assessment and contact the company directly to know the status of the litigation.

6) Error in the annual report:

In its FY2019 annual report, Polycab India Ltd has made an error and disclosed a different number of warehouses at different places in the annual report.

On page 27, the company stated that it has 29 warehouses as a part of its distribution network.

Polycab’s distribution network across India consists of 3,300 authorised dealers and distributors and 29 warehouses across 20 states

Whereas on page 18, the company states that, it has 30 warehouses under its network.

It may be a simple typographical error on the part of the company or different people preparing different sections of the annual report may have been provided with separate data points by the company. Nevertheless, an investor may contact the company directly for any clarifications. This is because; such errors question the quality of the data included in the annual report.

Advised Reading: How to study the Annual Report of a Company

7) Related party transactions of Polycab India Ltd:

At times, Polycab India Ltd has entered into financial transactions with its promoters and their group companies. Some of the transactions are as below.

The company has taken on lease a few godowns from promoters and their entities.

RHP, April 2019, page 45:

rent agreement with our Promoter and Chairman and Managing Director, Inder T. Jaisinghani for the purpose of renting out a godown, situated at Coimbatore: yearly rental income accruing to ₹0.10 million.

rent agreement with A.K. Enterprises (“AK Rent Agreement”), a partnership firm, where our Promoters, godown owned by it pay a monthly rent of ₹ 2.06 million

Similarly, the company has entered into transactions for the sale of assets with promoters and their relatives including the son-in-law of promoters, Puneet Sehgal (FY2021 annual report, page 212).

In FY2021, the company paid commission to an Australian entity, EPMR Australia Pty. Ltd, owned by key management personnel (KMP) (FY2021 annual report, page 210).

An investor would appreciate that the related party transactions between the listed entity and the promoters/their entities provide opportunities for shifting economic benefits from the minority/public shareholders to the promoters. If the listed entity pays a price to the promoters, which is higher than the market price of those services/rent, then effectively, these transactions may benefit promoters at the cost of minority/public shareholders.

Advised reading: How Promoters benefit from Related Party Transactions

The Margin of Safety in the market price of Polycab India Ltd:

Currently (April 22, 2022), Polycab India Ltd is available at a price to earnings (PE) ratio of about 48 based on consolidated earnings of the last 12-months (January 2021 to December 2021).

However, we recommend that an investor may read the following articles to assess the PE ratio to be paid for any stock, which takes into account the strength of the business model of the company as well. The strength in the business model of any company is measured by way of its self-sustainable growth rate and the free cash flow generating the ability of the company.

In the absence of any strength in the business model of the company, even a low PE ratio of the company’s stock may be a sign of a value trap where instead of being a bargain; the low valuation of the stock price may represent the poor business dynamics of the company.

- 3 Principles to Decide the Ideal P/E Ratio of a Stock for Value Investors

- How to Earn High Returns at Low Risk – Invest in Low P/E Stocks

- Hidden Risk of Investing in High P/E Stocks

Analysis Summary

Overall, Polycab India Ltd seems a company, which has grown its sales at a moderate rate of 12% year on year for the last 8 years. Moreover, sales growth has been associated with consistently improving profit margins. This is a good achievement by the company in the light of the intense competition in the cable & wires as well as electrical goods industry from unorganized and organized players. For most of the products, players compete on pricing.

Polycab India Ltd has been able to consistently improve its profit margins despite depending on highly volatile commodities like copper, aluminium and PVC (crude oil). It has done so as it has the flexibility to price its raw materials up to 90-days after purchase when it enters into contracts with its customers. In addition, the company regularly passes on any changes in its raw material costs and foreign exchange changes to its customers.

At times, the company keeps the benefits of declining raw material prices with itself. In addition, the company has worked on improving its sales mix to sell more high-margin retail wires and premium electrical products. All these steps in addition to increasing operating leverage have led to an improvement in its profitability over the years. Nevertheless, in recent times, due to intense competition, Polycab India Ltd could not pass on the entire cost increase to its customers and its profit margins declined in the last 12-months (January 2021-December 2021).

The trend of shifting business from the unorganized to the organized sector has helped Polycab India Ltd grow its business continuously over the years.

The company believes in making most of its goods in-house to ensure the best quality. As a result, its business is relatively capital-intensive than its peers. In one such attempt, the company installed a copper-rod manufacturing plant for a higher capacity than what it could consume thinking that it would sell the excess capacity in the market. However, when the responsibility of selling copper rods fell on its shoulders after its JV partner, Trafigura, exited the project, then it could not do it successfully. As a result, it had to sell the plant to Hindalco Industries Ltd.

Polycab India Ltd keeps a relatively higher amount of inventory in its warehouses because it prides itself on quick delivery of goods to its customers. However, the inventory levels have increased to very high levels and the company has been engaging external management consultants to bring efficiency to inventory utilization. However, the financial data for the recent years do not indicate any major improvement in the inventory turnover ratio.

The company used to face a lot of delayed collection and impairment of trade receivables. As a result, it stressed that its customers use channel financing where it could receive the money quickly from the bank and the risk of loss of receivables is taken over by the bank. It started offering cash discounts to customers who opted for channel financing. With the increasing use of channel financing, now, its receivables days have improved significantly.

Polycab India Ltd is growing its sales within its sustainable growth rate. Therefore, it seems that the IPO done by the company in 2019 was more an attempt to provide an exit to the financial investor IFC than a desperate attempt to raise money for the business. Over the years, Polycab India Ltd has generated surplus cash, which it has used to repay debt, pay dividends and has built cash & investments.

The company seems to have a succession plan in place where the second generation of promoters has joined the company while the first generation is still active.