The current section of the “Analysis” series covers Century Textiles & Industries Ltd, a B.K. Birla group company currently involved in the production of paper and textiles products, and real estate activities. The company has recently sold its large cement division.

“Analysis” series is an attempt to share with all the readers, our inputs to the company analysis submitted by readers on the “Ask Your Queries” section of our website.

In order to benefit the maximum from this article, an investor should focus on the process of analysis instead of looking for good or bad aspects of the company. She should learn the interpretation of different types of data and transactions and pay attention to the parts of annual reports etc. used to get the information. This will help her in improving her stock analysis skills.

Century Textiles & Industries Ltd Research Report by Reader

Hello Sir,

As requested, kindly provide an opinion on my analysis of the company: Century Textiles & Industries Ltd.

Thanks and regards,

Tanmay Ghate

Financial Analysis of Century Textiles & Industries Ltd:

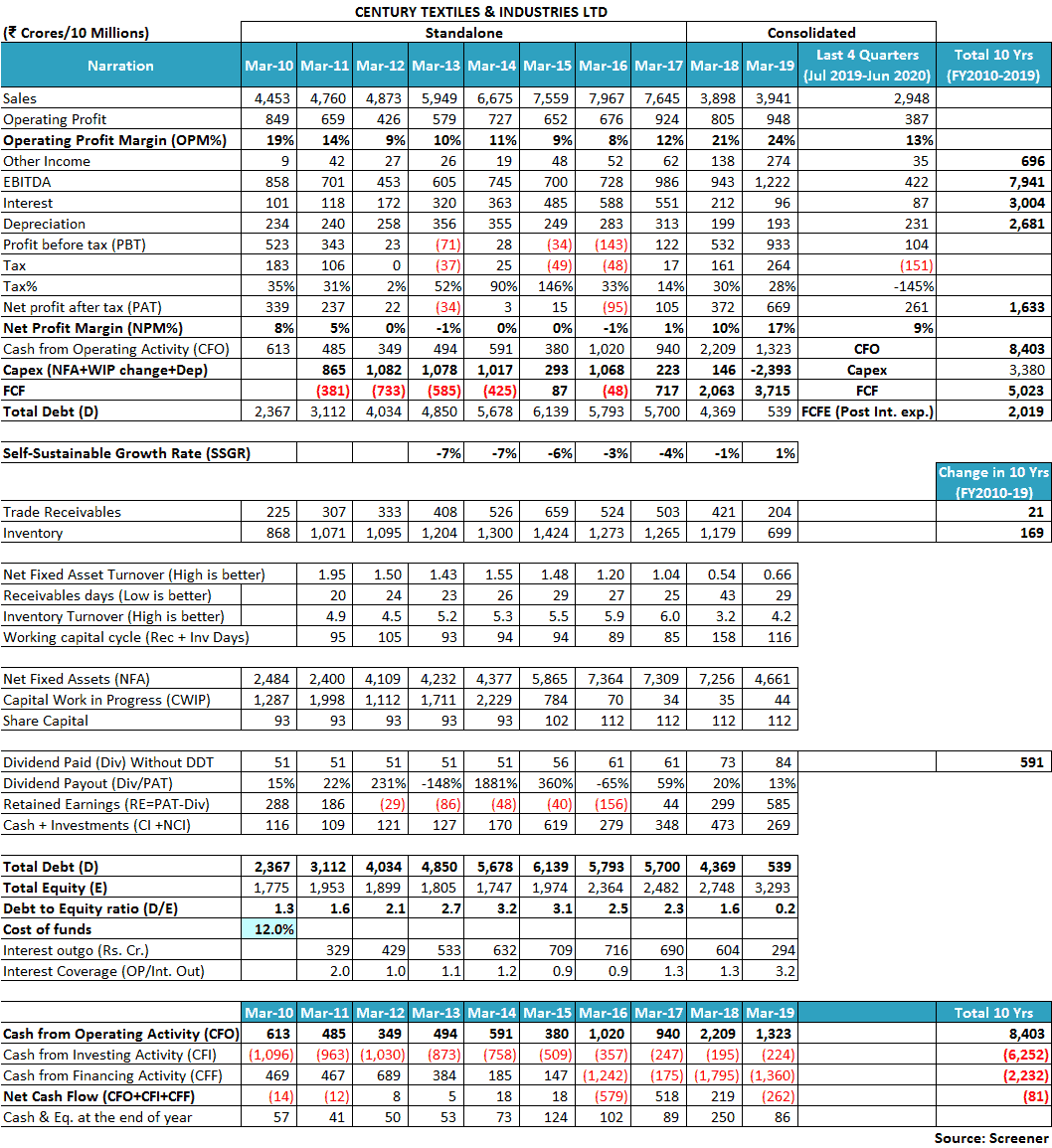

The company has not seen constant revenue growth in the last 5 years. In fact, there was a de-growth in sales for FY2017 as compared to the previous year. On the other hand, the company has undertaken cost optimization initiatives. During FY2018, the company entered into an agreement with Grasim Industries to operate VFY of its textile division against royalty. These measures have helped the company to reduce its debt and interest cost. Please note that figures for FY2019 in the image include revenue from the cement division, which has been demerged, hence not applicable.

As per 9-month financials for FY2020, there has been a de-growth in overall turnover for Century Textiles & Industries Ltd. Post demerger of cement division, major revenue comes from Century pulp and paper division.

Pulp and Paper Division of Century Textiles & Industries Ltd

In the recent past, the Indian paper industry faced short-term challenges due to structural economic changes like demonetization and GST. Being a capital-intensive industry, consolidation in the domestic market has happened. However, the industry is projected to grow at a CAGR of 5.5% between FY 20-23.

Previously papers were used for packaging purposes in FMCG, healthcare etc. sectors. However, with the growth of online shopping, the demand for papers has expanded immensely for wrapping and packaging purposes in India. Ban or reduction of plastic use by various state governments has influenced the use of paper more for the wrapping and packaging in India in the last few years. Higher spending by governments on education awareness programs and increasing literacy rates could lead to higher demand for paper in India.

Textiles Division of Century Textiles & Industries Ltd

To offset certain challenges, the company has been focusing on brand building via International quality standards like Made in Green tag and LEED certification (Leadership in Energy and Environmental Design), for the purpose of exports to USA/European markets, which give importance to such certification.

i) Restructuring of Century Textiles & Industries Ltd

During FY 2018, the company entered into an agreement with Grasim Industries to operate the Century Rayon segment for 15 years for a commuted royalty, interest-free refundable security deposit and transfer of Century Rayon’s working capital to GIL at actuals. The company has recognized a royalty income of INR 600 crores over the period of 15 years along with a security deposit of 200 crores. Pursuant to the agreement, Grasim Industries Ltd. shall incur all capex necessary for profitable operations of the Viscose Filament Yarn business.

While looking at the balance sheet items, Century Textiles & Industries Ltd has recognized this transaction under other non-current liabilities as a deferred revenue item. While reading note 33 for deferred revenue, Century Textiles & Industries Ltd mentions that it has received the money from Grasim Industries Ltd.

However, while going through the cash flow statement, the company has recognized this transaction under working capital changes, an item under the CFO segment. However, Century Textiles & Industries Ltd is in the business of textiles, cement, pulp and paper and real estate, each segment being a part of its core operations. Century Textiles & Industries Ltd is not in the business of giving its business division to operate on a lease basis to other companies. This type of recognition of the transaction has resulted in a significant shoot up of its CFO as well as operating profit and profit after tax for FY 2018 compared to the previous year.

This transaction has resulted in a decrease in interest cost and working capital requirement and repayment of high-cost debt, as a part of the cost control measure.

During FY 2018, the company also entered into Business Transfer Agreement (BTA) for its Century Yarn and Century Denim divisions, whose turnover was less than 5% of the total turnover of the company. Century Textiles & Industries Ltd recognized impairment loss on re-measurement of fair value amounting to INR 18.12 crores. This resulted in Profit before tax at INR -49.5 crores. Since the date of transfer of Y&D units, workers were on strike and challenged the sale of Y&D units by the Company. After objections of the workers in the court, the company terminated the sale and provided ₹25.49 cr as a restructuring cost.

Cement Division of Century Textiles & Industries Ltd

In June 2012, the Builders Association of India had filed a complaint before the Competition Commission of India (CCI) against certain cement manufacturers and the Cement Manufacturers Association (CMA). The accusations were imposed for using the CMA platform to fix cement prices, as well as control production and supply of cement in the market (cartel), thereby contravening the relevant provisions of the Competition Act 2002. Cement players like ACC, Ambuja, Ultratech, JK, Century, Binani, Lafarge cement etc. were involved in this case.

CCI had imposed a penalty (percentage of their net turnover) on cement manufacturers amounting to ₹6,300 crores. The penalty imposed on Century cement was INR 274 crores. Century along with other manufacturers had appealed this judgement before the Competition Appellate Tribunal (COMPAT). COMPAT had directed cement manufacturers to deposit 10% of the penalty amount. In December 2015, COMPAT ordered CCI to consider it as a fresh case and the interim penalty amount of INR 27.4 crores was refunded.

After rehearing arguments, CCI passed its judgment and once again held cement companies and CMA guilty in violation of Competition Act 2002, and imposed the same penalty as previously imposed in 2012. The order for cease and desist was also imposed. The company once again approached COMPAT, which stayed the CCI order in November 2016 subject to a deposit of 10% penalty amount within one month. The Company has accordingly deposited the said amount in December 2016 in the form of Fixed Deposit in favour of COMPAT on behalf of the Company.

Subsequently, the Government has made changes in the constitution and operations of Tribunals under which all matters with COMPAT have been transferred to the National Company Law Appellate Tribunal (NCLAT).

NCLAT has upheld the CCI order of imposing the penalty of INR 274 crores. Now the case is pending at Supreme Court for judgment.

i) Demerger of Cement Division:

During FY 2019, Century Textiles & Industries Ltd decided to demerge its cement division and sell to Ultratech Cement (Aditya Birla Group Company) for a share-swap deal. All assets/plants and liabilities including debt amounting to ₹3,000 crores of cement division were transferred to Ultratech cement. Contingent Liabilities amounting to ₹740 crores have also been transferred.

As per the valuation report uploaded at the exchanges, two entities were appointed as independent valuation agencies- Bansi S. Mehta & Co and Walker Chandiok & Co.

However, minority shareholders have expressed their concerns with respect to the methodology used by the Board of Century Textiles & Industries Ltd to sell off the cement division. Their opinion was competitive bidding system would have led to a higher realization on the sale off, unlike the market multiple approaches used in the case.

On the other hand, management was of the opinion that cement plants were more than 25 years old with an outdated system. In order to maintain the marginal Century Textiles & Industries Ltd.’s 3% market share in the Indian cement industry, it would have had to carry out capex to upgrade/modify at around 2500 crores. This would have led to higher leverage. Moreover, the profitability of the cement division is not comparable to the industry average. In addition, competitive bidding rounds eats up a lot of time, leading to further deterioration in the cement assets and further delay into the real estate segment.

Real estate division of Century Textiles & Industries Ltd:

Century Textiles & Industries Ltd has two commercial properties located at Worli, Mumbai viz. Birla Centurion and Birla Aurora, which are fully leased out. The annual rental income derived from these properties is around 150 crores.

In order to undertake real estate development projects, in December 2017, Century Textiles & Industries Ltd incorporated a wholly-owned subsidiary named Birla Estate Private Ltd. (BEPL) with an initial capital of INR 5 lakh. During FY 2019, the share capital of BEPL has further increased to INR 82.5 crores.

There was also one complaint filed in 2019 against BEPL.

As mentioned during concall in May 2018, management is more focused on NCR and Gurgaon, Pune (Talegaon), Mumbai (Worli and Kalyan) and Bangalore for residential projects development.

Out of these pockets, there is a certain land portion in Worli, which is under litigation with the Wadia family as disclosed in the call.

Management Analysis of Century Textiles & Industries Ltd:

Century Textiles & Industries Ltd is majorly owned by Aditya Birla Group companies with 50.21% since the end of FY 2018.

i) Warrants issued by Century Textiles & Industries Ltd:

The company had issued warrants to promoter group companies. As per the agreement, these were to be converted into equivalent no. of shares at INR 354.89 within 18 months from the date of allotment.

These warrants were exercised in two phases.

On 30th March 2015, 84,70,000 warrants were converted into equivalent no. of equity shares. As per the AR FY 2015 page 53, the lowest share price of Century Textiles & Industries Ltd in March 2015 was INR 529.65. If promoter group companies had increased their stake by buying shares from the open market, they had to pay at least INR 529.65 in the month of March 2015. However, shares were allotted to them at 354.89 per warrant, thus pocketing gains of INR 174.76 per share. The total amount is 148 crores. [(529.65-354.89)*84,70,000)]

Rest 1,01,80,000 warrants were exercised into equivalent no. of shares on 18th December 2015. As per AR FY 2016 page 48, the lowest share price of Century Textiles & Industries Ltd was INR 531.1. Thus, promoter groups have spent INR 179 crores less cost on the acquisition of shares through the exercise of warrants. [(531.1-354.89)*1,01,80,000], when compared to acquisition at market share price.

Century Textiles & Industries Ltd has sold its shares worth INR 530 (lowest market price in March 2015 and December 2015) at a price of ₹354.89 to promoter group companies.

This has also helped promoter group companies to increase their shareholding from 40.23% in April 2014 to 45.22% in March 2015 and further to 47.75% in December 2015. During FY 2018, promoters have acquired shares from the secondary market, which has helped to gain a majority stake in the company at 50.21%.

Regards,

Tanmay Ghate

Dr Vijay Malik’s Response

Hi Tanmay,

Thanks for sharing the analysis of Century Textiles & Industries Ltd with us! We appreciate the time & effort put in by you in the analysis.

While analysing the past financial performance of the company, an investor notices that until FY2017, the company used to report only standalone financials. However, in FY2018, the company formed its subsidiary Birla Estate Private Limited to focus on real estate development. As a result, the company started to report standalone as well as consolidated financials from FY2018.

We believe that while analysing any company, an investor should always look at the company as a whole and focus on financials, which represent the business picture of the entire company including its subsidiaries, joint ventures etc. Consolidated financials of any company, whenever they are present, provide such a picture.

Further advised reading: Standalone vs Consolidated Financials: A Complete Guide

Therefore, in the analysis of Century Textiles & Industries Ltd, we have used standalone financials up to FY2017 and consolidated financials from FY2018 onwards.

Business Structure of Century Textiles & Industries Ltd:

When reading about the business of Century Textiles & Industries Ltd, an investor notices that the company is a combination of different independent business segments. At the start of the decade, in FY2010, the company had the following segments:

- Cement division (59% of revenue)

- Paper & pulp division (21%)

- Textiles including Rayon man-made fiber division (Viscose filament yarn & related products) (18%)

Then in FY2010, the company entered the real estate business by starting construction of two commercial buildings at its mill land in Worli, Mumbai. The company completed the construction and leasing of the two commercial buildings in FY2016 and since then, it is getting an annual rental income of about ₹140-150 cr.

Credit rating report by CRISIL in July 2019:

Steady annual gross lease rental of Rs 140-150 crore from the commercial real estate assets is expected to support cashflows over the medium term.

Therefore, by FY2016, the company had four independent divisions:

- Cement division (52% of revenue)

- Paper & pulp division (24%)

- Textiles including denim, yarn and Rayon man-made fiber division (22%)

- Real estate division (0.4%)

Thereafter, from FY2018, the company started restructuring its businesses. In FY2018, Century Textiles & Industries Ltd did two business restructurings.

First, it sold its yarn & denim division. (FY2018 annual report, page 10):

During the year under review, the Company sold its Century Yarn and Century Denim Divisions, whose turnover was less than 5% of the total turnover of the Company.

Second, it leased out its Rayon man-made fiber division (Viscose filament yarn & related products) to a group company, Grasim Industries Ltd for 15 years.

FY2018 annual report, page 10:

With effect from 1 st February, 2018, the Company has granted Grasim Industries Ltd. (GIL) the right and the responsibility to manage and operate the Viscose Filament Yarn business…..which comprises of the manufacturing and sale of viscose filament yarn (including pot spun yarn and continuous spun yarn), rayon tyre cord and chemicals…..for a duration of 15 years…

Thereafter, in May 2018, Century Textiles & Industries Ltd proposed to demerge its cement division to a group company, Ultratech Cement Ltd., which was completed in Oct. 2019.

FY2020-Q3 results, page 2:

The Scheme of Demerger between the Company and UltraTech Cement Limited (“Resulting Company”) and their respective shareholders and creditors (“Scheme”) was approved by the National Company Law Tribunal (NCLT) on July 3, 2019 and on completion of all conditions precedent, as specified in the Scheme, the Scheme became effective on October 1, 2019. Pursuant to the Scheme becoming effective, the Cement Business Division is demerged from the Company and transferred to and vested in the Resulting Company with effect from May 20, 2018 i.e. the Appointed Date.

As a result, the company updated its financials from May 20, 2018, by excluding the performance of the cement division.

In addition, when the company reported its FY2019 financials in the FY2019 annual report, to provide relevant comparative financials for the previous period, Century Textiles & Industries Ltd provided its FY2018 financials adjusted after removing the performance of the cement division from its operating segments. Instead, the company reported the performance of the cement division under discontinued business segments.

FY2019 annual report, page 18:

Accordingly, the Cement business has been shown as discontinued operations in the financial statements.

In another development during, FY2019, the workers of the sold-out yarn and denim division disputed the sale in the court of law and Century Textiles & Industries Ltd had to cancel the sale process and take back the yarn & denim division that was sold in FY2018. However, the company kept the yarn & denim division as an “asset for sale”, therefore, it classified it under discontinued operations.

FY2019 annual report, page 10:

Pursuant to the objections raised in the Court, against the transaction by the workers of the Y&D units, during the year, the Company has terminated the Business Transfer Agreement and has taken back possession of the Y&D units. The Company is exploring various alternatives for disposal of the units. Accordingly, the assets and liabilities of the Y&D units are classified as assets held for disposal and the operations have been classified as discontinued operations.

Therefore, in light of all these business restructuring-related developments since FY2018, an investor needs to understand which business segments are included in the sales and profits of Century Textiles & Industries Ltd since FY2018.

While interpreting the numbers reported by different financial databases, an investor should keep in mind that the sales and the operating profit include the performance of business divisions, which are classified as continued operations. Moreover, the performance of discontinued operations is included in the net profits, cash flow statements and balance sheet.

Therefore, while interpreting the financial table of Century Textiles & Industries Ltd, an investor should read it as follows:

Up to FY2017, the sales, operating profit, net profit & all other financial parameters include the performance of the following four-business division:

- Cement division

- Paper & pulp division

- Textiles including denim, yarn and Rayon man-made fiber division

- Real estate division

Since FY2018, Century Textiles & Industries Ltd started business restructuring.

In FY2018 and FY2019, the financial performance in the operating income (sales) and operating profits include the performance of the following divisions:

- Paper & pulp division

- Textiles excluding denim, yarn and Rayon man-made fiber division

- Real estate division

Whereas the net profit, cash flow statement and the balance sheet of FY2018 and FY2019 include the performance of following additional business divisions, which are classified as discontinued operations by the company:

- Cement division

- Denim and yarn division

In FY2020 and ongoing FY2021, the operating income (sales) and operating profits include the performance of the following divisions:

- Paper & pulp division (72% of FY2020 revenue)

- Textiles excluding denim, yarn and Rayon man-made fiber division (22%)

- Real estate division (4%)

Whereas the net profit, cash flow statement and the balance sheet of FY2020 onwards, includes the performance of following additional business division, which is classified as discontinued operations by the company:

- Denim and yarn division

An investor would appreciate that understanding and comparing the financial performance of Century Textiles & Industries Ltd over the years, due to these business-restructuring exercises becomes difficult. However, an investor would have to keep these developments in her mind while she analyses the business performance of Century Textiles & Industries Ltd.

With this background, let us analyse the financial performance of the company since FY2010.

Financial and Business Analysis of Century Textiles & Industries Ltd:

While analyzing the financials of Century Textiles & Industries Ltd, an investor notices that the sales of the company were growing at a pace of about 8% year on year from ₹4,453 cr in FY2010 to ₹7,645 cr in FY2017. However, suddenly, in FY2018, the sales of the company declined to ₹3,898, which have further declined to ₹2,948 cr in the 12 months ended June 2020 (i.e. July 2019-June 2020).

From the above discussion about the business restructuring exercises undertaken by Century Textiles & Industries Ltd, an investor would appreciate that the decline in the operating performance from FY2019 is due to the demerger of the cement division, which used to constitute about 52% of the total sales of the company.

Moreover, when the company reported its FY2019 financials, then in the FY2019 annual report, in order to provide relevant comparative financials for the previous period (FY2018), Century Textiles & Industries Ltd provided its FY2018 financials adjusted after removing the performance of the cement division from operating segment and putting it in the discontinued segment.

As a result, it seems that financial databases like Screener have updated the FY2018 performance of Century Textiles & Industries Ltd by using the adjusted financials of the year from its FY2019 annual report. Therefore, the FY2018 operating performance of the company reported in the financial table above excludes the performance of the cement division even though the appointed date for the demerger was May 20, 2018.

Nevertheless, from the above discussion, an investor would appreciate that the performance of the cement division is included in the net profits, cash flow statement and the balance sheet as a part of discontinued operations. Therefore, while an investor analyses the net profit after tax (PAT) of Century Textiles & Industries Ltd, then she notices that there is no such sudden decline in the PAT of the company from FY2018 onwards.

While analysing the operating performance of Century Textiles & Industries Ltd over the years, an investor notices that the operating profit margin (OPM) of the company has witnessed very sharp movements.

The OPM of the company used to be 19% in FY2010, which declined sharply to 9% in FY2012. Thereafter, the OPM continued to remain suppressed until FY2016 when the company reported its lowest OPM of 8% in the last decade. From FY2017 onwards, the operating margin of the company started improving and it reached 24% in FY2019. Thereafter, the OPM of Century Textiles & Industries Ltd has declined to 13% in the 12 months ended June 2020 (i.e. July 2019-June 2020).

An investor would appreciate from the above cyclically fluctuating profit margins that the overall business of Century Textiles & Industries Ltd is highly cyclical. Such kind of fluctuating profit margin is a characteristic of businesses, which do not have any pricing power over their customers. Most of the time, these businesses deal in commodity products where the customer is indifferent to the source of the product. The customers of such products have the option of buying from multiple suppliers both from India and overseas without much difference in the quality of the product available to them.

As a result, the manufacturers of such non-differentiable commodity products are not able to increase the prices of their products when their input costs go up. If a supplier increases its prices, then the customer easily shifts to another supplier or starts importing the products. As a result, the manufacturers have to bear the impact of the increase in raw material products themselves and in turn, take a hit on their profit margins.

Almost all the business divisions of Century Textiles & Industries Ltd like paper, textiles, cement etc. are commodity products. As a result, the company finds it difficult to increase prices to its customers and had to take a hit on its profit margins when its input costs increase.

The credit rating agency, CARE had also highlighted this nature of business divisions of the company in its credit rating report in January 2019:

Cyclical and commoditized nature of business: All the three key businesses of CTIL viz. cement, textiles and pulp & paper are commoditized with intense competition and cyclical in nature makes it vulnerable to demand and supply dynamics and restricts CTIL’s pricing power.

Advised reading: Credit Rating Reports: A Complete Guide for Stock Investors

Nevertheless, in order to understand the business performance of the company, it is essential to understand the business dynamics and performance of each of these divisions individually.

1) Century Pulp & Paper:

As per the investor presentation of the company released in June 2020 (page 4), the pulp & paper division constitutes 72% of the operating revenue of the company. Therefore, in the current business position of the company, pulp & paper is the most important division for the company.

While reading the available annual reports of Century Textiles & Industries Ltd since FY2007, an investor gets insights that the pulp and paper business is a purely cyclical business where the industry undergoes periods of demand and supply mismatch.

At times, the demand for paper exceeds its supply in the market. As a result, the prices of paper products increase and the paper manufacturers increase their supply significantly. When the new manufacturing capacities start functioning, then the industry faces a situation of oversupply. This leads to price wars when manufacturers undercut prices to stay in the business. During this phase of decline of paper prices, many small & unorganized players find it difficult to survive and in turn, go out of business. The resulting shutdown of plants by these small & unorganized players reduces the supply in the market and the prices of paper products increase.

This seems to be a recurring phenomenon in the paper industry. While reading the developments of the paper industry over the years in the annual reports of Century Textiles & Industries Ltd, an investor can easily understand this cycle of the paper industry.

In FY2007-08, the paper industry in India was facing a shortage of supply. As a result, the country was importing a lot of paper and in addition, many Indian players were expanding their capacities.

FY2008 annual report, page 30:

The Indian paper industry is highly fragmented with numerous small players. The industry is witnessing a healthy demand and its financial performance has also improved. Most players are augmenting capacities, which are expected to come on stream over the next two to three years………With steady demand for paper in India and a surging requirement for higher quality paper, foreign players are exporting to India in a major way.

During this phase when the demand for paper exceeded the production, Century Textiles & Industries Ltd also announced capacity expansions. In FY2007, the company had completed one expansion project and simultaneously, it announced another expansion project to produce tissue paper.

FY2007 annual report, page 16:

The expansion of our paper unit for manufacturing paper from waste paper has been commissioned from 03.02.2007 with a capacity of 211 tonnes per day and the plant is now running smoothly.

It has been decided to set up a 100 tonnes per day Prime Grade Tissue Paper Plant at a total capital outlay of Rs.175 crore based on imported softwood and our own hardwood pulp as raw material…..is expected to be operative by about September, 2008.

The very next year in FY2008, Century Textiles & Industries Ltd announced its plans to establish a multi-packaging board plant along with a fibreline plant.

FY2008 annual report, page 09:

We are setting-up a Multilayer Packaging Board Plant, with a capacity of 500 tonnes per day. This development, requiring a total capital outlay of about Rs. 775 crore, is expected to be operational by December 2009. Additionally, we are planning to set up a Paper Grade Pulp Plant (Fibreline) to produce superior quality wood pulp. The plant demands a capital outlay of Rs. 495 crore and is anticipated to commence operations by December 2009.

An investor would expect that during good times, individuals, as well as companies, become very enthusiastic. As a result, the manufacturers see only the positives. An investor gets a similar feeling when in the FY2009 annual report, Century Textiles & Industries Ltd mentioned to its shareholders that the demand for paper would only go up from here.

FY2009 annual report, page 24:

Due to favourable Government policies such as the thrust on education, a growing economy and young population, increasing urbanization, a clear preference for print media and widespread interest in books and publishing, consumption of paper can only increase…

However, an investor would appreciate that paper is a cyclical industry where the demand rises and falls over time. In the very next year, FY2010, the upcycle phase of the paper industry was ending and Century Textiles & Industries Ltd saw a reduction in the demand for paper.

FY2010 annual report, page 20:

The Paper Business was under severe pressure due to a substantial increase in the prices of raw materials and reduced demand.

The intense competition in the industry did not allow the company to pass on the increase in raw material costs to its customers. As a result, the company had to take a hit on its profit margins in the paper division.

FY2010 annual report, page 23:

The prices of bagasse and wood which constitute major raw materials for pulp and other input costs have considerably increased without a sizable appreciation in selling prices. This has adversely affected the performance of this Division for a major part of the year.

By FY2012, almost all of the previously announced capacity expansion plants by the paper industry, including the expansion plants of Century Textiles & Industries Ltd were operational. As a result, the industry started facing a situation of oversupply. Century Textiles & Industries Ltd also acknowledged that the paper industry is cyclical in nature.

FY2012 annual report, page 25:

The output from several new manufacturing facilities has further increased finished product supply, flooding the market and it will take some time for demand to catch up with these additional quantities.

Being in the commodity sector, the paper industry is cyclical in nature and is strongly co-related with global economic factors.

The very next year in FY2013, Century Textiles & Industries Ltd reported net loss.

FY2013 annual report, page 23:

However, due to higher depreciation in the current year on account of commissioning of Multilayer Packaging Board and Fiberline Plant (Pulp plant) in the Pulp & Paper Division, the Company has incurred a net loss.

By 2014, the paper industry had so much oversupply that the situation of dependence on imports to meet the demand in FY2008 had now given way to exports of paper from India. Due to oversupply, the company was not able to pass on the increase in inputs costs to the customers and as a result, had to take a hit on its profit margins.

FY2014 annual report, page 24-25:

Further, apart from rising production and consumption, erstwhile import dependent India has achieved self-sufficiency and also has witnessed an increase in exports.

While raw material costs have been increasing, the selling prices could not be increased to offset entirely the rising costs which resulted in an adverse financial performance.

By FY2015, the oversupply situation in the paper industry had worsened to such an extent that the small, B-grade, unorganized players started to go out of business and a price war was prevalent in the market.

FY2015 annual report, page 21:

With new installed capacities coming online in the second half of the year, the demand supply equilibrium in the Indian market shifted towards excess supply. This led to players dropping prices to remain competitive…..

The biggest threat for the Indian paper industry is from imports of paper products from China and duty free paper products from the ASEAN region. Products from these regions have priced out many domestic manufacturers and this has resulted in a price war in the Indian market across all grades.

This impacted the profitability of the Indian paper industry, as well as economic viability of ‘B’ grade paper mills.

Soon enough, the newly started division by Century Pulp & Paper, the multilayer packaging board business also experienced oversupply.

FY2016 annual report, page 20:

…..two newly installed capacities becoming operational by other players in the Multilayer Packaging Board business. With new capacities, the demand supply equilibrium in the domestic market shifted towards excess supply.

By FY2017, the oversupply situation in the Indian paper industry has taken its toll on the paper manufacturers. A few of them had to shut down their business. Now, it was time for the demand to exceed supply and the future of the industry started to look bright.

FY2017 annual report, page 19:

Based on the recent shut down of some domestic capacities and expected growth in the country’s GDP, it is likely that the domestic paper industry will grow at a reasonable pace along with the economy, from a medium to long-term perspective.

By FY2019, the paper & pulp division of the company had started to contribute healthily to the company’s performance and became one of the key reasons for the improving operating profit margins of Century Textiles & Industries Ltd.

FY2019 annual report, page 18:

Pulp & Paper and Real Estates Divisions have primarily contributed to this growth.

The demand in the paper industry exceeds supply and in FY2020, India met about 20% of its paper demand from imports.

Investor presentation, June 2020, page 34:

Total Demand- 19.8 Million MT in FY 20-21

Total Supply:

- Domestic: ~15.8 Million

- Imports: ~4 Million

In FY2020, the paper division of the company operated with 100% capacity utilization. Press release for Q4-FY2020 results:

Pulp and Paper Business operated at 100% capacity for FY20.

In light of the same, it does not come as a surprise to the investor that the paper manufacturers have again started increasing the manufacturing capacities. Century Textiles & Industries Ltd announced its plans to expand the manufacturing capacity in FY2019.

FY2019 annual report, page 10:

The Company has undertaken a project to expand the Prime Grade Tissue Paper Plant capacity from 100 tonnes per day to 200 tonnes per day with an Anchor GSM of 19 grams at a total capital outlay of ₹100 crores at the existing Pulp and Paper Plant at Lalkua, District Nainital, Uttarakhand.

The credit rating agency, CRISIL, in January 2020, acknowledged that the paper division of Century Textiles & Industries Ltd has displayed significant improvement in performance over the last 3 years.

Paper segment’s revenue and profitability have consistently improved, backed by increased capacity utilisation and realisation over the last three fiscals. This is expected to continue over the medium term, with completion of capex in high margin tissue segment and de-bottlenecking, despite some headwinds in realisations.

From the above report, an investor would notice that CRISIL expects that the good performance of paper division will continue over the medium term.

The management of the company is also giving a positive outlook about the performance of the paper division.

FY2019 annual report, page 20:

With increased demand for value added products and an improved order booking position, in future, we are hopeful of having further improvement in the business.

However, from the above discussion about the development in the paper industry, an investor would appreciate that the paper industry is cyclical in nature where demand and supply undergo phases. In FY2007-2008, in the Indian paper industry, demand exceeded supply and many manufacturers announced expansion plans. In good times, Century Textiles & Industries Ltd said to the shareholders that the paper demand would only increase. However, soon thereafter, the industry turned into an oversupply situation where price wars broke out. Paper manufacturers started reporting losses and many players went out of business and shut down capacities. As a result, the oversupply corrected itself.

Since FY2017, the paper industry is witnessing another upcycle where demand has exceeded supply. The country is meeting excess demand from imports (just like FY2007-2008) and the manufacturers have announced capacity expansion.

Based on the insights about the cyclical nature of the paper industry, an investor should be cautious before she starts projecting the good performance of the paper division into the future. She should be aware that the paper industry is cyclical where the down-phase follows the upcycle phase and vice versa.

Moreover, while assessing the competition to any company in the paper industry, an investor should not limit her assessment only to other large paper manufacturers. This is because in the paper industry, many times, even the small players are able to produce good quality products and give tough competition to the large players. In the down-phase of the industry in FY2016, Century Textiles & Industries Ltd had disclosed this aspect of the paper industry to its shareholders.

FY2016 annual report, page 20:

Some smaller manufacturing set-ups, which enjoy lower cost of production due to advantageous levels of overhead expenses and taxes, have upgraded the quality of their products, and provide good competition to large units in terms of both, quality and price.

Therefore, an investor should always keep the cyclical and intensely competitive nature of the paper industry while she makes assumptions about the future performance of the paper division of Century Textiles & Industries Ltd.

Further advised reading: How to do Business Analysis of Paper Manufacturing Companies

To understand more about the nature of cyclical industries where supply and demand frequently exceed each other in phases, an investor should read our analysis of the following companies where manufacturers announce new capacities when demand exceeds supply; however, by the time, the new plants become functional, the demand cycle turns and the industry faces oversupply. As a result, many manufacturers shut down their businesses.

2) Century Textiles (Birla Century):

As per the investor presentation of the company in June 2020 (page 4), the textiles division contributed to 22% of revenue in FY2020. While reading the annual reports of Century Textiles & Industries Ltd, an investor realizes that the textile industry is highly competitive where it is not possible for the manufacturers to pass on the increase in input costs to their customers. As a result, whenever the raw material prices go up, the textile manufacturers end up taking a hit on their profitability margins.

FY2010 annual report, page 20:

the prices of all inputs had gone up which could not be passed on to the end users in view of adverse market conditions prevailing during the major part of the year coupled with low demand. Therefore, the performance of textile segment remained depressed.

FY2011 annual report, page 22:

However, due to the severe increase in the prices of cotton, wages, oil and gas, the cost of manufacturing has been steadily rising whereas the markets were under pressure due to demand recession and prevailing general inflation in consumer goods prices. It has not been possible to increase the selling prices commensurate with the increase in the input costs and therefore, the margins have been under severe pressure.

Moreover, an investor may think that the textile manufacturers might be facing the challenge in passing on the increase in input costs to their customers in the segments of yarn etc. She may think that in the case of the ready-to-wear segment where the manufacturers create brands and sell directly to the end customer, there the manufacturers might be able to increase prices to compensate for the increase in raw material costs. However, while analysing the business of Century Textiles & Industries Ltd, the investor notices that even in the ready-to-wear segment of branded clothes, the textile manufacturers are not able to pass on the increase in input costs to their customers.

FY2011 annual report, page 22:

The sales of our ready-to-wear garments marketed under the brand name ‘Cottons by Century’ have been adversely affected due to the demand recession and increase in costs. The recent introduction of excise duty on the manufacture of ready made garments will further increase the prices, which will be very difficult to pass on to customers.

In the textile industry, the position of players is very difficult. When the raw material prices go up, then they are not able to pass it on to their customers and therefore, have to take a hit on their profit margins. In addition, when the raw material prices go down, then the market prices of their products fall in line with the reduction in input costs. Therefore, they face large inventory losses.

FY2012 annual report, page 22:

Cotton prices reached at an all time high followed by a phase of correction. This left various mills with high cost inventories causing heavy losses as the selling prices of fabrics did not improve.

At present, the market is very reluctant to absorb increased costs in selling prices because of which margins are under severe pressure and we have to wait for markets to improve and costs to stabilize…

By FY2012, the competition in the textile market had become extremely severe from both the domestic manufacturers as well as from imports that many players realized that they could no longer compete in the market.

FY2012 annual report, page 22:

Textile products from Bangladesh permitted to be imported duty free are cheaper and have flooded the markets, pushing out Indian products with prices that cannot compete.

When the intense competition had taken its toll on the textile manufacturers, then the industry cycle showed some improvement in FY2013.

FY2013 annual report, page 23:

The sales at Birla Century have improved by about 65% as compared to last year due to better use of capacity and increasing demand in domestic and US markets.

However, soon enough, in FY2014, the industry again showed its tough face to the manufacturers where the inputs cost increased and they could not increase the prices to the customers. As a result, the profit margins of the players remained depressed.

…those with a presence in weaving, processing or even composite businesses are facing the heat due to increases in input cost without being able to pass on such higher costs to customers as the market is simply unable to absorb the same.

Moreover, an investor notices that the competition in the domestic market is not only from Indian manufacturers but also from international manufacturers like Bangladesh.

FY2019 annual report, page 18:

The duty free import of fabrics from China into Bangladesh and in return the Garments are being imported duty free into India from Bangladesh is hitting hard the Indian Textile Industry.

Nowadays, big brands manufacture their products overseas and then sell them in retail shops in India at cheaper prices.

FY2018 annual report, page 17:

The international brands like Marks & Spencer, IKEA, Zara, H & M, Walmart etc. who have multiple sources to cover fabrics and convert into garments in Bangladesh, Vietnam and Cambodia etc. for retailing in India at better prices will make it difficult for Indian textile industry to compete with them.

An investor learns that the smaller countries like Bangladesh, Vietnam etc. are not only contributing to competition in the Indian market, they are also beating India in competition in the developed markets.

FY2015 annual report, page 18:

Depreciation of the Euro against the Indian Rupee has adversely affected textile business, apart from the 9.6% tariff disadvantage Indian textile products suffer from the European Union. India has already started losing its markets and export orders, and countries like Pakistan, Bangladesh, Sri Lanka and Vietnam which have duty-free access, are now grabbing the market share.

FY2016 annual report, page 16:

Increasing competition from countries like Bangladesh, Vietnam, Pakistan and Sri Lanka due to favorable tariff structures on exports to developed markets like the US, EU, Canada, Australia, etc. poses a significant challenge to Indian exports.

Therefore, an investor notices that the tough business environment of the textile industry of the previous decade is still the same for the Indian manufacturers. In FY2010, the manufacturers were not able to pass on the increase in inputs costs to the customers. Even in FY2019, they are unable to pass on the increase in input costs to the customers. Moreover, nowadays, the shift from cotton to man-made fibers is increasing their challenge.

FY2019 annual report, page 19:

Due to the cash crunch and weak demand in the Indian and Export markets, it is difficult to pass on the cost to end customers, hence the margins are under pressure. Further, globally consumer shifting preference from cotton fibre to man-made fibre, which are available at lower prices, is also putting pressure on prices.

Read: How to do Business & Industry Analysis of a Company

i) Yarn & denim unit of Century Textiles & Industries Ltd

While reading about the performance of different segments within the textile division, an investor notices that certain segments like yarn and denim have had a tough time throughout the available period under analysis.

In FY2009, the company had to cut production, as it did not have enough demand.

FY2009 annual report, page 21:

The domestic and export markets for cotton yarn and denim remained quite depressed. We are making every possible effort to develop new varieties of denim to suit the fast changing fashion trends as also regulating the production as per market needs.

Again, in FY2013, when the situation of the denim market did not improve, then Century Textiles & Industries Ltd had to make its denim production plant to produce other materials.

FY2013 annual report, page 23:

However the market for denim is depressed. We have, therefore, re-engineered the product line to produce the items that customers prefer, to overcome the slackness.

In FY2015, the company faced severe pricing pressure in the denim segment.

Further, the cotton yarn market remained depressed for a major part of the year under review, which adversely impacted our yarn unit near Indore in M.P. Similarly, the denim market also remained dull and domestic sales and exports from India were facing a severe price crunch.

As a result, it does not come as a surprise to the investor when she reads in the FY2018 annual report that Century Textiles & Industries Ltd has sold off its yarn & denim unit that too at a loss of ₹18.12 cr.

FY2018 annual report, page 122:

Pursuant to the Business Transfer Agreement (BTA) the Company has sold its Yarn and Denim (Y&D) units (included in Textile Segment) during the year and has recognized loss on disposal amounting to ₹18.12 Crore. The operations of Y&D units has been classified as discontinued operations (Refer note 35).

As the company reported the performance of the yarn & denim unit separately in the FY2018 annual report, under the discontinued operations, therefore, an investor could get to know the financial performance of this unit for FY2017 and FY2018. Otherwise, the financial performance of the yarn & denim unit was clubbed with other units under the section “textiles” in the segmental results. As a result, an investor could not know the financial performance of individual units.

As per the FY2018 annual report, page 119, the yarn & denim unit had made a net loss of ₹18.9 cr in FY2017, which increased to a net loss of ₹36.8 cr in FY2018.

It is unfortunate for the shareholders that the dissenting workers stalled the sale process of the yarn & denim unit and Century Textiles & Industries Ltd had to take back the unit from the buyer and even suffer a restructuring cost of ₹25.5 cr.

FY2019 annual report, page 128:

Pursuant to the objections raised by the workers of Y&D units against the said business transfer, during the year the Company has terminated the BTA, refunded the sale consideration and has obtained back the possession of the Y&D units. The Company is currently exploring various alternatives including sale to other buyers and accordingly has classified the operations as Discontinued operations. Further, during the year Company has recognized a provision for restructuring cost relating to the units amounting to ₹25.49 crores.

As per the performance of the yarn & denim unit disclosed under discontinued operations in the FY2019 annual report, page 128, the yarn & denim unit suffered a net loss of ₹48.56 cr in FY2019.

Therefore, the decision of the company to keep looking for other buyers for the yarn & denim unit does not come as a surprise to the investor. The yarn & denim unit seems like a continuous drain on the resources of the company.

ii) Rayon (man-made) fiber & chemicals unit of Century Textiles & Industries Ltd:

Rayon unit of the company primarily comprises man-made fibers like viscose filament yarn (pot spun yarn and continuous spun yarn), rayon tyre yarn and various other chemicals.

From the above discussions on business restructuring, an investor would remember that currently, Century Textiles & Industries Ltd has given this unit on lease from FY2018 to Grasim Industries Ltd for 15 years and has already received all the lease payments for the next 15 years.

Therefore, this unit may not be very relevant from the perspective of business performance. However, we believe that an understanding of this unit is essential for investors because of two reasons. First, after the end of the contract with Grasim Industries Ltd, the company would receive this unit back. Second, the decisions taken by the management of Century Textiles & Industries Ltd with respect to the Rayon unit provide insights into the quality of the management of the company.

Century Textiles & Industries Ltd used to be one of the largest manufacturers of rayon in Asia and the largest manufacturer in India. It had a 40% market share in India.

Credit rating report of Century Textiles & Industries Ltd by CRISIL in February 2015:

the company is one of the largest manufacturers of rayon in Asia and is a market leader in India (40 per cent market share).

Such a position may indicate to an investor that the company might enjoy a lot of negotiating and pricing power over its customers. However, it was not true. Century Textiles & Industries Ltd did not command any pricing power and its profit margins were hit when input costs increased as it could not pass on the increase in raw material prices to the customers.

While reading about the rayon unit, an investor notices that right from the first available annual report of FY2007, Century Textiles & Industries Ltd has faced challenges while running its rayon unit.

In FY2007, the company highlighted that there is immense competition in the viscose filament yarn (VFY) segment and many producers are selling it at a discount. Therefore, the company is unable to increase prices to cover higher input costs.

FY2007 annual report, page 26-27:

Producers like us could not increase prices due to yarn being sold at a discount by a few producers.

Higher cost of raw-materials, particularly Wood Pulp and Sulphur may have to be absorbed, as it would be difficult at this stage to pass on this increased burden to consumers.

The situation continued to be grim over the years as cheaper imports from China continued to provide intense competition.

FY2012 annual report, page 22:

the industry in general, in both the PSY and CSY segments, faced pressure on off-take due to substantial arrivals from China,

The excess supply situation in the viscose filament yarn (VFY) segment continued over the years and Century Textiles & Industries Ltd did not expect any respite in the near future.

FY2014 annual report, page 22:

It is expected that the existing trend of excess supply affecting sales volumes as well as prices will continue for some time.

When an investor attempts to understand the reasons for such continued situation of oversupply in the VFY industry (at least since FY2007, the first publicly available annual report of the company), then she notices that the viscose filament yarn is facing substitution from polyester yarn, which is cheaper.

FY2008 annual report, page 28:

Substitution of VFY by Polyester Yarn in a few cases and cheaper prices of Polyester Yarn continue to affect the off-take as well as the prices of VFY.

In addition, the polyester yarn manufacturers seem to do good research and development to produce newer varieties of polyester yarn, which made the situation further difficult for VFY producers.

FY2011 annual report, page 25:

The threat from cheaper polyester yarn continues. Due to continuous research being undertaken by the polyester industry, new varieties of polyester yarn are being introduced, making it suitable for alternative use and compete better against rayon yarn.

Soon, the research efforts of polyester industry borne fruit and it launched Recosilk yarn, which further hit the demand of viscose filament yarn (CFY).

FY2014 annual report, page 22:

The launch of ‘Recosilk’ yarn by the polyester industry for embroidery, weaving and knitting has also made a dent in the market share of viscose filament yarn and could lead to a reduction in VFY consumption.

Soon, the polyester industry introduced new products, which hit the demand for another key product of the rayon unit, rayon tyre yarn (RTY).

FY2016 annual report, page 18:

Efforts by Tyre manufacturers to replace rayon tyre yarn with HMLS Polyester continues to pose a long term threat,

This other key segment of the rayon unit, the rayon tyre yarn (RTY) had been facing oversupply and intense competition since long. In fact, the competition increased to such an extent that in FY2009, Century Textiles & Industries Ltd had to stop its production plant.

FY2009 annual report, page 22:

This has resulted in high inventory due to which production of rayon tyre yarn had to be suspended from end February 2009.

The situation in the rayon tyre yarn (RTY) segment stayed worse for years to come. In FY2010, 50% of the manufacturing capacity was kept shut.

FY2010 annual report, page 21:

High inventory of rayon tyre yarn continues to remain a major concern and 50% of the production capacity remains suspended from February 2009.

The high inventory in the RTY segment improved only after about four years of curtailed production. In FY2012, the company could finally use its full capacity of RTY production.

FY2012 annual report, page 23:

Efforts by the unit to provide quality products have yielded positive results and it is pertinent to mention that for the first time in the last 4 years, full manufacturing capacity is being used

However, the very next year, in FY2013, the company again had to suspend 35% of its manufacturing capacity.

FY2013 annual report, page 24:

Continuing recession in Europe has adversely affected the off-take of rayon tyre yarn which forced our unit to curtail its production by about 35%.

Century Textiles & Industries Ltd could use its full manufacturing capacity again only after two years in FY2015.

FY2015 annual report, page 18:

After a prolonged period, increased demand and consumption of Rayon Tyre Yarn in Europe and Japan have led to full capacity utilization of our Rayon Tyre Yarn production capacity.

However, the full capacity utilization of RTY capacity did not mean that it has got its pricing power back. Instead, in FY2016, the company intimated to its shareholders that it is not able to get any price increase for the last four years.

FY2016 annual report, page 18:

The unit could procure orders for Rayon Tyre yarn for the year 2016 and is expected to operate at its full capacity. However, it could not get any increase in the price for about four years, which is a matter of concern.

Just when the company was able to get some order to use its manufacturing capacity of rayon tyre yarn (RTY), it realised that the customers are now asking for a new product, dipped fabric instead of Rayon Tyre yarn, which Century Textiles & Industries Ltd is not able to manufacture.

FY2016 annual report, page 18:

Tyre manufacturers are demanding dipped fabric instead of Rayon Tyre yarn, which the unit is not able to supply as it does not have a conversion facility. In the long run, this may threaten our presence in the International market.

FY2017 annual report, page 17:

In Rayon Tyre Yarn, the unit may face the threat of losing its market share due to not having an integrated manufacturing unit for dipped fabrics.

Further advised reading: Understanding the Annual Report of a Company

From the above discussion about the key product segments of the rayon unit, viscose filament yarn (VFY) and rayon tyre yarn (RTY), an investor would notice that these businesses are very tough. In addition, the manufacturing process of these man-made fibers is polluting. As a result, these companies face tough environmental regulations. These tough operating conditions along with intense competition due to oversupply and substitution by polyester make their plants economically unviable. While reading the annual reports of Century Textiles & Industries Ltd, an investor notices many instances where the multiple manufacturers of viscose filament yarn closed their plants and shut down their business.

FY2007 annual report, page 26:

Due to environmental and other problems, one major yarn producing unit in Europe had to close down a couple of years back.

FY2009 annual report, page 22:

During the year, overall demand for viscose filament yarn (VFY) has reduced. However, in view of closure of two Rayon producing units in the country, industry was able to utilize its full capacity and also reduce inventories.

FY2010 annual report, page 21:

The world over, due to stringent environment control, rayon manufacturing units are closing their operations, including one having so well-known a name as Enka Elsterberg, Germany.

FY2013 annual report, page 24:

Production of VFY by domestic producers has dropped by about 23% in the last 5 years and the gap thus created has been met through higher imports as there have been no significant additions to capacities within India.

FY2015 annual report, page 18:

While some additional capacities have been commissioned in China, non viable plants were shut down in Europe & C.I.S. countries due to shift of manufacturing operations away from the western to emerging markets.

Until now, the environmental norms were getting stringent only in western countries. Therefore, VFY manufacturers in countries like China and India were happy to get additional business. However, in FY2016, the VFY manufacturers in China faced closure when the country tightened its environmental norms to reduce pollution.

FY2016 annual report, page17:

New stringent environmental policy norms adopted by China have led to the closure of 2 VFY plants in China, having a capacity of 29000 Tons per annum.

In FY2016, Century Textiles & Industries Ltd also realized that India is also considering tighter environmental norms for VFY production. The company realised that tougher environmental norms are going to create many challenges for it. As a result, the company along with other players requested the authorities to reconsider new environmental norms.

FY2016 annual report, page 18:

A representation made by the unit through Association of Man-Made Fibre Industry of India (AMFII) for reconsideration of the proposed new environmental norms for the man-made fibre industries, are at the hearing stage. If imposed, it would be difficult for the industry to meet the new environmental norms without huge capital investment.

Therefore, from the above discussion, an investor would appreciate that the rayon unit faced multiple challenges like intense competition, oversupply, cheaper imports, substitution by cheaper polyester products, and tougher environmental norms. In addition, the company was not able to keep up with the changing demands of its customers.

As a result, despite being the largest manufacturer of rayon in India and one of the largest in Asia, Century Textiles & Industries Ltd decided to get rid of its rayon unit by handing it over to Grasim Industries Ltd.

It remains to be seen whether Grasim Industries Ltd would be able to run the rayon unit profitably or it would hand it back over to the company before completion of 15 years. In any case, the business of the rayon unit has proved to be a tough challenge for Century Textiles & Industries Ltd, which it finally quit in FY2018.

Moreover, it seems that the company has learnt its lesson from the tough business conditions of the textile industry and now, it has decided not to invest any big money in the textile unit.

Conference call transcript, May 2018, page 14:

Management:….we do not want to go for big expansion in textiles because the profits we expect are more in paper and real estate.

Further advised reading: How to do Business Analysis of Textile Companies

3) Real estate division of Century Textiles & Industries Ltd:

As per the investor presentation of the company in June 2020 (page 4), the real estate division contributed to 4% of revenue in FY2020.

At present, Century Textiles & Industries Ltd has two completed and leased out commercial buildings at Worli, Mumbai, which provide it with an annual rental income of about 140-150 cr.

Credit rating report by CRISIL in January 2020:

Steady annual gross lease rental of Rs 140-150 crore from the commercial real estate assets is expected to support cashflows over the medium term.

In addition, the company has launched sales in three residential projects at Kalyan, Bengaluru and Gurugram.

Investor presentation, Q1-FY2021 results, July 2020:

Strong uptick in demand enquiries and conversions at our launched projects (Birla Vanya, Kalyan and Birla Alokya, Bengaluru) despite the nationwide lockdown

Gurugram project – Birla Navya (JV with Anantraj Ltd) project which is presently in a prelaunch stage, received a strong response. Sold inventory worth around INR 28 Crs (INR 14 Crs in Q1 FY 21) and collected 2.8 Crs, so far.

There are many uncertainties pertaining to the future of the real estate industry due to excessively high prices that many times, are out of reach for the common person, and the associated execution risk of real estate projects. These factors have led to the bankruptcy of many established and well-known real estate players and almost all remaining players including the industry leaders are facing a tough time. Therefore, it remains to be seen whether Century Textiles & Industries Ltd is able to complete its projects on time and within the estimated cost.

Also read: How to do Business Analysis of Real Estate Companies

4) Cement division of Century Textiles & Industries Ltd:

An investor would remember from the above discussion on the business restructuring of Century Textiles & Industries Ltd that the company has demerged its cement division to Ultratech Cement Ltd. Therefore, going ahead, the dynamics of cement are not going to affect the business performance of the company. Nevertheless, a brief discussion about the business unit, which the management controlled and operated during the major part of the analysed financial history, provides the investors with insights about the decisions taken by the management with respect to business. Such analysis, now, provides more insights about management quality instead of business quality.

However, an investor would appreciate that cement is an intensely competitive, cyclical industry, which has always faced a situation of oversupply over the last decade. As a result, the cement division of the company has contributed significantly to the fluctuating profit margins of Century Textiles & Industries Ltd until FY2018 when it was a part of the company.

In FY2007, the cement industry position was very attractive where demand exceeded supply. As a result, many foreign players entered the Indian market.

FY2007 annual report, page 28:

Four of the top five cement companies in the world have entered India through mergers, acquisitions or joint ventures. These include Lafarge, Holcim, Italcementi and Heidelberg. These companies have already garnered about 28% of Indian industry capacity.

In the subsequent years, there was a race among the players to increase capacity. By FY2013, the capacity installed by cement manufacturers in India had exceeded the targets estimated by the planning authorities. As a result, the industry faced a situation of oversupply.

FY2013 annual report, page 27:

The cement industry had surpassed the target set by the working group on this industry for the XIth five year plan (2007-2012). The installed capacity was over 340 million tonnes against a target of 298 million tonnes at the end of the terminal year of the XIth five year plan, resulting in surplus capacity.

By FY2015, the surplus capacity started to have a serious impact on the manufacturers and the capacity utilization of the industry declined to 69%.

FY2015 annual report, page 19:

Cement industry’s capacity utilization during the year 2014-15 was about 69%. Capacity utilization is gradually coming down on account of the mismatch in capacity addition and demand.

By FY2018, the capacity utilization level of the industry declined further to 68%.

FY2018 annual report, page 20:

The Indian Cement industry is grappling with lower capacity utilisation while operating at levels of about 68 per cent.

At one end, an investor may think that the cement industry was grappling with over-enthusiasm shown by the cement manufacturers where they added large capacity initially and thereby faced a situation of oversupply. However, an investor would appreciate that in such situations, the manufacturers stop creating more supply and wait for the demand to recover so that their capacities reach optimal utilization levels before they start additional expansion projects.

However, in the cement industry, it seemed that these normal fair-market principles did not apply and the industry witnessed significant capacity additions even when the utilization levels of existing plants were very low.

The following analysis of Heidelberg Cement India Ltd would indicate to an investor that the cement industry increased its manufacturing capacity from 296 MTPA in FY2011 with 73% capacity utilization to 495 MTPA in FY2019 with 68% capacity utilization.

Further advised reading: Analysis: Heidelberg Cement India Ltd

As a result, the Competition Commission of India (CCI) initiated a probe in the working of the cement industry. CCI found that the cement manufacturers were working as a cartel to produce less cement deliberately even when there was a demand in the market. As a result, CCI imposed a penalty of ₹6,300 cr on leading cement manufacturers including Century Textiles & Industries Ltd.

The continuous subdued performance of the cement division due to either genuine oversupply or deliberate under-production had led to the fluctuating profit margins of the cement division of Century Textiles & Industries Ltd.

To understand more about the cement industry, an investor may read the analysis of the following article where we discuss the business analysis of cement companies in detail: How to do Business Analysis of Cement Companies

From the above discussion about the business performance of Century Textiles & Industries Ltd over the years, an investor would understand that the company is a mix of a few entirely independent business divisions. Therefore, in order to understand the company or to make any assumptions of the future business performance of the company, an investor needs to understand each of the business divisions individually.

As per the current business structure of Century Textiles & Industries Ltd, the business divisions of paper, textile and real estate are important. Nevertheless, from the above discussion, an investor understands that each of these divisions is intensely competitive. In paper and textile divisions, the competition is so intense that routinely many manufacturers shut down their plants and businesses as they become economically unviable.

In real estate, even though at the surface, it may look like that demand exceeds supply and the business has excessive profitability margins. However, if an investor studies the experience of different real estate players, including the leading, well-known names, then she gets to know that it is very difficult to stay continuously relevant in this industry. There have been numerous examples of leading players going bankrupt, unable to complete and deliver their projects and even instances of promoters going to jail. Therefore, an investor should be cautious while she starts projecting supernormal profits in the real estate division into her assumptions in order to justify any high valuation.

Going ahead, an investor should monitor the profitability margins and the capacity utilization of paper and textile divisions of Century Textiles & Industries Ltd. In addition, she should track the execution progress of the real estate projects launched by the company. She should also monitor whether, in future, the company resorts to launching many projects in quick succession without focusing on the completion of existing projects. This is because launching more real estate projects than what one can complete in time is the stage where problems start to appear for real estate developers. The greed of getting a lot of money from the homebuyers at a very initial stage of the project when the real estate developer has hardly spent any money on construction makes the projects cash surplus right from its launch stage. As a result, the greed to get more and more money from homebuyers leads to the developers launching more & more new projects without focusing on completing existing projects.

Therefore, the investor should keep a close watch on the new launches of real estate projects by the company. If she notices that the company has launched many projects in quick succession, then instead of becoming very happy, she should become cautious. She should increase her monitoring level of execution of existing real estate projects. By staying cautious and with close monitoring, she would be able to avoid negative surprises from the real estate division of the company.

While looking at the tax payout ratio of Century Textiles & Industries Ltd., an investor notices that for most of the last 10 years (FY2010-2020), the tax payout ratio of the company has been highly fluctuating. Over the years, the tax payout ratio has varied from 2% in FY2012 to 146% in FY2016.

An investor may appreciate that the many products of the company like textile, paper etc. are exported, which have tax incentives from the government for its manufacturing operations focused on exports. These incentives would tend to decrease the tax payout ratio. In addition, the cement plants of the company have fiscal benefits.

Moreover, due to frequent business restructuring exercises, the company’s profits, as well as tax payout, tends to fluctuate significantly.

An investor may contact the company directly for any further clarifications about its tax payout ratio and the incentives available to the company.

Further advised reading: How to do Financial Analysis of a Company

Operating Efficiency Analysis of Century Textiles & Industries Ltd:

a) Net fixed asset turnover (NFAT) of Century Textiles & Industries Ltd:

When an investor analyses the net fixed asset turnover (NFAT) of Century Textiles & Industries Ltd in the past years (FY2010-19), then she notices that the NFAT of the company has consistently come down from 1.95 in FY2011 to 0.66 in FY2019.

Declining NFAT over the years indicates that the company efficiency of utilization of assets by the company has deteriorated over the years.

If an investor takes the case of cement division, which used to be a part of the company’s financials until FY2017 and used to constitute more than 50% of sales, then she notices that the company faced deteriorating performance of the division due to two factors.

First, the cement industry faced oversupply leading to lower capacity utilization.

Second, the cement plants of Century Textiles & Industries Ltd were old, inefficient and effectively of poor quality. The management of the Century Textiles & Industries Ltd disclosed this aspect of the cement plants of the company in its conference call with investors in May 2018 while discussing the deal with Ultratech Cement Ltd.

As mentioned earlier, the discussion of the business units hived off by the company now provides more insights about the management quality and their strategic decisions that the quality of the business of the hived off units.

First, the management highlighted that its cement plants are inefficient and their profitability is less than the industry average.

Conference call, May 2018, page 2:

Moreover, the profitability of cement division is currently not comparable to the industry average.

The company highlighted that the old plant at Manikgarh, Maharashtra of about 2 MTPA capacity is currently shut down as it is highly inefficient and is effectively an economically unviable plant.

Conference call, May 2018, page 8:

Rajesh Shah: Out of the existing capacity of 4.8 million tonnes at Manikgarh, 2 million is the old capacity and shutdown. It’s an old plant and it has lot of inefficiencies relating to power consumption, heat consumption and to upgrade that it needs a huge investment.

Similarly, another cement plant of the company in Chhattisgarh is very old and is nearing the end of its life. As a result, an investor would appreciate that the plant would have many inefficiencies in its operations.

Conference call, May 2018, page 8:

Management: Again about the Chhattisgarh Plant that is the oldest plant that is a 44 year old plant. And the current life of the plant left is around 6-7 years’ time and maybe after 7 years it need complete new line will have to be put up so that will again call for huge investment…

Moreover, the management highlighted that the utilization of the new cement capacity created in West Bengal depends on transporting clinker from Manikgarh, Maharashtra, which is a very expensive and inefficient method.

Conference call, May 2018, page 17:

Gunjan Prithyani: I just have one clarification there is this grinding unit in West Bengal from where was you feeding the clinker to that grinding unit?

Management: So in that grinding unit clinker was largely getting supplied from Manikgarh unit incurring a huge logistic cost.

In addition, the management clarified that even though it had put up a significant 2.8 MTPA new cement capacity at Manikgarh, Maharashtra, the region has immense competition with low demand. The management highlighted that even if they increase the production of cement in the Manikgarh plant, then they do not know how to sell it.

Conference call, May 2018, page 8:

Management: I will just come to the power efficiency, but basically demand is also not there in that area. There is huge competitive intensity in that area and we are not able to sell that. That is why that utilization level is low.

Further reading: How to identify if Management is Misallocating Capital

From the above discussion, an investor notices that the cement division led to deteriorating NFAT for Century Textiles & Industries Ltd due to many factors. First, significant cement capacity was old, inefficient and even economically unviable. Therefore, these assets produced lower sales leading to lower NFAT. Second, the new capital expenditure for the creation of new cement manufacturing plants was also done in a manner, which resulted in new capacity in the region where the company is either not able to sell (Manikgarh, Maharashtra) or it needs to transport clinker from halfway across the country from Maharashtra to West Bengal to run the new plant there. All these decisions add to the inefficiency in the utilization of the assets leading to lower NFAT.

In addition, an investor would remember from the above discussion that the other business divisions like textile and paper have continuously faced a tough business situation with oversupply, poor pricing power etc., which leads to poor asset utilization and a decline in NFAT.

Moreover, an investor would notice that the absolute level of asset turnover of Century Textiles & Industries Ltd is low in the range of 1.00 and the average net profit margin (NPM) for the last 10 years is in the range of 4%.

Please note that as discussed above, the NPM of the company for FY2018 and FY2019 is high because the sales (operating income) excludes the impact of discontinued operations (primarily cement division) whereas the net profit after tax (PAT) includes the profit of discontinued operations. As per the FY2019 annual report, page 129, the cement division (discontinued operations) had a profit of ₹129 cr in FY2018 and a profit of ₹222 cr in FY2019. The addition of this profit in PAT without the related revenue in the sales increases the NPM.