The current section of the “Analysis” series covers AIA Engineering Ltd, an Indian manufacturer of grinding equipment used in the mining, cement and power industries. AIA Engineering Ltd specializes in grinding media, liners and diaphragms containing chrome and is among the two largest players in this segment in the world along with Magotteaux of Belgium.

The “Analysis” series is an attempt to share with all the readers, our inputs on the company analysis submitted by readers on the “Ask Your Queries” section of our website.

To benefit the maximum from this article, an investor should focus on the process of analysis instead of looking for good or bad aspects of the company. She should learn the interpretation of different types of data and transactions and pay attention to the parts of annual reports etc. used to get the information. This will help her in improving her stock analysis skills.

AIA Engineering Ltd Research Report by Reader

Sir,

My report for AIA Engineering Ltd is attached for your perusal.

With best regards,

Shreyas Nevatia

About AIA Engineering Ltd

It is a company, which makes grinding media for cement, and mining companies. We can call it an FMIG (Fast moving Industrial Goods) company comparable to FMCG companies. The cost is low compared to the total costs but the company needs it to function, hence there is customer stickiness.

The company is into the production of high chrome mils for major plants, hence, there will be customer stickiness as existing customers would like to stick with a quality supplier and the demand is mostly replacement so no one will change suppliers, as the costs are a small part of their overall costs. In addition, the lack of comparable industries also perhaps explains their high ROCE.

Business Analysis of AIA Engineering Ltd

The market is oligopolistic indicating a high competitive advantage.

Marketing strategy: the business always has to go for aggressive capacity expansion.

Inherent cyclicality: The business is somewhat cyclical because its end users are cyclical. From its credit rating report, apparent that the company is cyclical as raw material volatility is higher. Further, it is working capital intensive; also, it has not been able to convert its PAT into CFO.

Further, if we see the OPM on the Screener it is fluctuating over 5 %, which indicates limited pricing power.

There is a lack of continuity of demand when a downturn in the mining industry led to disruption for the company in FY2010.

The company states that it is able to pass on the price fluctuations then why it buys raw materials during low price cycles.

The company has dependability on China for raw material prices.

The prospects of the company are closely linked to the prospects of the cement and mining industry. Further, due to limited pricing power, there is fluctuation in operating margins.

Related Party Transactions of AIA Engineering Ltd:

The purchase of goods is ₹26 cr in 2020 and ₹36 crores in 2019, which is not big compared to the size of the company. In addition, if we analyse various other years, then there have been no significant dealings with private related parties controlled by management entities. The transaction with subsidiaries is in the normal course of business, as exports require transactions to be done across geographies.

Management Remuneration of AIA Engineering Ltd:

Given the size of the company, management remuneration is reasonable. In FY 19, it was ₹1.27 crore which is reasonable. Further, Mr Shah is an IIT graduate, which also brings great technocratic skills to the table.

Ratio Analysis of AIA Engineering Ltd:

The business is working capital intensive as stated in its credit report. Hence, the company has not been able to convert its Profits into CFO. (₹3789 cr PAT vs ₹3089 cr CFO).

The company has a fixed asset turnover ratio ranging from 3 to 5. This is explained by the aggressive capacity expansion that the company has to take constantly to maintain customer relations.

Receivable days have increased from 68 in March 2014 to 78 in March 2019. (March 2020 excluded for Covid). It is a sign of working capital-intensive operations.

The inventory turnover ratio has also remained in a range from 6 to 4.

The company has been able to generate free cash flows of ₹1862 crores until date, which is proved by the low debt and high cash on its books.

Special mention: 31 crores was spent on settling a patent infringement suit with a key competitor.

Reason for no R&D expense: “All work that we work is at the client side all the trial and error all the operating conditions are things we learned and we go to mines and we just have the good trial at the client-side. We do work at our own end but it is difficult to spread through the whole system so it is difficult to hive off and create a system and R&D.”

Valuation: The current valuation is 32 times earnings, which does not offer a margin of safety.

Summary:

The company is a quality company with an established track record and high customer stickiness due to network effects. The company also has a good runway for growth given the opportunity to convert the grinding media to Ferro-chrome. Further, the cost reduction brought into the customers’ operation and it being FMIG good gives the company a competitive advantage. However, it is somewhat constrained by the cyclicality of its end customers which also exposes it to raw material fluctuation. The company has a clean track record of corporate governance. Hence, the company can surely be bought at reasonable valuations, as it will have a high rate of reinvestment of incremental capital generated.

Regards,

Shreyas Nevatia

Dr Vijay Malik’s Response

Dear Shreyas,

Thanks for sharing the analysis of AIA Engineering Ltd with us! We appreciate the time & effort put in by you in the analysis.

While analysing the history of AIA Engineering Ltd., an investor notices that throughout the last 10 years (FY2011-2020), the company has had many subsidiaries within India as well as in foreign locations. As per the FY2020 annual report, pages 166, the company has 2 Indian subsidiaries and 9 foreign subsidiaries in its corporate structure. As a result, throughout the last 10 years (FY2011-2020), AIA Engineering Ltd has reported both standalone as well as consolidated financials.

We believe that while analysing any company, an investor should always look at the company as a whole and focus on the financials, which represent the business picture of the entire group. Consolidated financials of any company, whenever they are present, provide such a picture.

Further advised reading: Standalone vs Consolidated Financials: A Complete Guide

Therefore, in the analysis of AIA Engineering Ltd, we have used consolidated financials in the assessment.

With this background, let us analyse the financial performance of the company.

Financial and Business Analysis of AIA Engineering Ltd:

While analyzing the financials of AIA Engineering Ltd, an investor notices that the sales of the company have grown at a pace of about 11% year on year from ₹1,160 cr in FY2011 to ₹2,970 cr in FY2020. Further, during the 12 months ending December 2020 (i.e. January 2020-December 2020), the sales of the company have declined to ₹2,878 cr.

While doing a detailed analysis of the sales growth and the profitability of AIA Engineering Ltd, an investor notices that the company’s growth journey has not been smooth and it has faced years of declining sales as well as fluctuating profit margins.

AIA Engineering Ltd witnessed a decline in its sales in FY2016 when the sales declined to ₹2,097 cr from ₹2,182 cr in FY2015. Thereafter, in FY2020, the sales of AIA Engineering Ltd declined to ₹2,970 cr from ₹3,070 cr in FY2019. Thereafter, in the 12 months ending December 2020 (i.e. January 2020-December 2020), the sales of the company further declined to ₹2,878 cr.

When an investor notices the profit margins of AIA Engineering Ltd, then she notices that the operating profit margin (OPM) of the company has seen significant fluctuations over the years. During FY2011-2014, the OPM declined consistently to 14% from about 27% in FY2009 and FY2010 (as per the FY2010 annual report, page 8).

Thereafter, during FY2015-2017, the OPM recovered to the levels of 28-29%. However, the recovery was short-lived and in FY2018, the OPM declined sharply to 22% and has been at similar levels until the 12 months ending December 2020 (i.e. January 2020-December 2020). The net profit margin (NPM) of AIA Engineering Ltd has followed a similar trend over the years.

An investor needs to analyse the business model of AIA Engineering Ltd in detail to understand the reasons behind the periodic decline in sales and the fluctuations in the profit margins of the company over the years. Only after understanding the reasons behind the fluctuating performance of the past, an investor would be able to make an educated guess about the future performance of the company.

Advised reading: How to do Business Analysis of a Company

While reading the annual reports of AIA Engineering Ltd, its credit rating reports, red-herring prospectus for IPO in FY2006 as well as various corporate announcements, an investor notices that the business model of the company has the following characteristics, which influence its performance significantly and bring in the volatility in its business performance.

A) The prices of raw materials of AIA Engineering Ltd are very volatile:

In the terms of raw materials, AIA Engineering Ltd uses metal scrap (primarily steel) and ferrochrome as primary raw materials, which forms more than 40% of its total cost.

FY2006 annual report, page 24:

The key raw materials for our company include Scrap and Ferro Chrome constituting more than 40% of the total costs.

In the case of both raw materials, AIA Engineering Ltd finds it difficult to have fixed-price contracts.

The company buys metal scrap and other recyclable inputs from the shipbreaking industry.

FY2018 annual report, page 33:

Over 65% of input material is sourced from scrap, which is in turn sourced from the ship breaking industry

In the case of metal scrap, the suppliers are from the unorganized sector and the company is not able to enter into fixed-price contracts.

FY2006 annual report, page 26:

Suppliers of scrap are scattered and unorganized and hence, it is difficult to enter into fixed price contracts.

Moreover, an investor would appreciate that the prices of metal scrap (primarily steel) move along with the prices of steel, which is very fluctuating as the steel industry is a cyclical industry where periods of high demand follow periods of low demand. This brings volatility in all the industries that are influenced by steel production.

From the above graph, an investor would notice that historically, steel prices have been very volatile. As a result, an investor would appreciate that the prices of scrap steel would naturally follow the steel prices and in turn, the raw material costs for AIA Engineering Ltd would vary significantly over this period.

AIA Engineering Ltd sources ferrochrome from companies like Tata Steel Ltd.

FY2018 annual report, page 34:

Ferro alloys are sourced from well established players such as Tata Steel, Dipak Ferro alloy, Essel mining and Team Ferro alloys.

The prices of ferrochrome are dependent on the decisions of China regarding the production of steel and the stocking of ferrochrome. An investor would appreciate that the cyclical nature of steel production would make ferrochrome prices very volatile.

FY2019 annual report, page 85:

Ferro Chrome pricing is linked to Chinese actions on production of steel and stocking decisions on this raw material, which in turn brings volatility in pricing. We expect Ferro Chrome to remain volatile going forward.

Advised reading: How to do Business Analysis of Steel Companies

Moreover, AIA Engineering Ltd is a very small player when compared to suppliers like Tata Steel Ltd. Therefore, ferrochrome suppliers seem to have a higher negotiating power on AIA Engineering Ltd and therefore, are able to push on any increase in their costs to AIA Engineering Ltd.

An investor may notice the extent of volatility in the raw material prices borne by AIA Engineering Ltd from the following chart of ferrochrome import prices in India from January 2010 to December 2020.

In the above chart, an investor would notice that ferrochrome prices have been very volatile frequently doubling and then becoming half.

From the above discussion on the prices of steel and ferrochrome, an investor would appreciate that AIA Engineering Ltd faces a very volatile pricing situation in its raw materials where the prices routinely double and then frequently decline by half.

B) The customers of AIA Engineering Ltd belong to cyclical industries:

While reading the annual reports of AIA Engineering Ltd, an investor notices that the company supplies to customers belonging to the mining, cement and power sectors. FY2020 annual report, page 30:

The Company serves the cement, power, mining and aggregates markets both national and international.

Out of these industries, mining constitutes more than two-thirds of the sales for AIA Engineering Ltd. As per the presentation of the Q3-FY2021 results, page 6, the mining sector constituted 66% of the sales in FY2020 and 70% of sales in 9M-FY2021 (April 2020-Dec 2020).

An investor would appreciate that industries like mining, cement etc. are cyclical in nature. These industries witness periods of good performance followed by periods of poor performance. As a result, the cyclical nature of these industries also influences AIA Engineering Ltd where its products witness periods of good demand followed by periods of poor demand by its customers in the mining and cement industries.

In FY2010, when the commodity sectors like iron ore, cement etc. witnessed a decline, then the business of AIA Engineering Ltd was impacted.

FY2010 annual report, page 35:

The countries, which were particularly worst hit, include North America, South America, European Subcontinent as well as CIS countries. Since your Company is strongly present in the Cement segment in all these major markets, it has witnessed a temporary impact of this slow down in the Cement replacement demand from the above markets.

On the Mining front, since your Company had focused strongly on Iron Ore for its worldwide foray into Mining business, significant slow down in the Iron Ore production world wide resulted into a sizeable destocking activity by the major Iron Ore mines, which affected your Company’s plan to ramp up its production for servicing this segment in First Half of FY 2010.

Therefore, an investor would appreciate that the demand for the products of AIA Engineering Ltd is linked with the cyclical nature of the mining and cement industries, which are its key customers.

C) Exposure to volatile foreign exchange/currency movements:

While analysing AIA Engineering Ltd, an investor notices that more than 75% of the sales of company come from exports where the company get money in foreign currency.

FY2020 annual report, page 84:

In Fiscal Year 2019-20, 77.39% of its total sales came from outside India while balance 22.61 % came from sales from India.

An investor would appreciate that foreign exchange (currency) markets are very volatile and prices keep changing due to numerous parameters like economic, political, social, and technological factors. A high contribution of exports in the revenues of AIA Engineering Ltd brings volatility in the performance of the company.

Therefore, when an investor tries to explain the fluctuating sales and profit performance of AIA Engineering Ltd over the last 10 years, then she should look at the above parameters of raw materials (metal-scrap and ferrochrome), customers (mining sector forming 65-70% of sales), and exports as major sources of revenue, working together to influence the business of the company.

For example, during FY2010-2013, when AIA Engineering Ltd saw its operating profit margins (OPM) decline from about 27% in FY2010 to 18% in FY2013, it was a combined impact of an increase in raw material prices, the pressure to offer lower prices to make an entry into the mining industry and volatility in the foreign currencies.

FY2012 annual report, page 28:

In terms of costs, there was significant increase in input costs including main raw materials like melting scrap and ferro chromium. Further, the company has also faced certain entry level pricing pressure in the Mining Segment. In addition, major currencies where the Company has an exposure, viz. Euro and USD also went through volatility. All these factors have affected the margin to an extent.

Again, in FY2018, the OPM of the company declined sharply to 22% from 28% in FY2017. From the above charts showing historical prices of steel and ferrochrome, an investor would notice that over FY2017-2018, the prices of both these commodities increased sharply, which led to a decline in the profit margins of AIA Engineering Ltd.

While reading its past annual reports, an investor notices that in FY2006, AIA Engineering Ltd realised that the fixed price contracts with its customers have hurt its profit margins whenever raw material prices increase. Therefore, it started to incorporate variable pricing in its contracts with the customers, which could help it seek an increase in prices when the raw material prices go up.

FY2006 annual report, page 24:

Also, annual fixed price contracts with customers and substantial increases in scrap prices impacted the company’s margins adversely. However, we have now entered into variable price contracts, which will enable us to pass on any spikes in raw material costs

Therefore, an investor is a little surprised to notice that despite entering into variable price contracts with its customers since FY2006, why the company’s profit margins are impacted in FY2011-2013 and FY2018 when the raw material prices increased sharply.

Here, an investor would appreciate that two important factors come into play. The first is that not all customers accept variable-price contracts. Certain customers like Govt. might prefer fixed-price contracts, and most of the sales of the company to power producers in India are to public sector companies. In addition, the company may be forced to offer fixed-price contracts to new customers to start a relationship with them.

Secondly, even in the cases where AIA Engineering Ltd has variable price contracts, the increase in the prices does not seem to happen automatically. In these cases, the company starts a discussion with the customers about increasing prices when the raw material prices have already increased significantly. Moreover, many times, when the negotiations reach the stage of determining new prices, by that time, the raw material prices may have already stabilized leading to AIA Engineering Ltd bearing the full impact of the transient increase in raw material prices and thereby affecting its margins.

Therefore, an investor would appreciate that the company gets an increase in prices only after a delay of a few quarters that is taken up in negotiations and many times; it may not get a price hike if the raw material prices come down during this period. The company highlighted this aspect of business negotiations in its conference call with the investors in February 2021.

Kunal D. Shah: But how do you deal with pricing when prices are very erratic, right? When prices are going up, we started all the conversations. But by the time it can crystallize, we’re seeing some level of retrenchment back towards mean prices. So I mean, as prices stabilize, it’s a natural conversation that will come up. Raw material is never sitting as cost, any increases or decreases do not sit on our profit and loss. It’s a pass-through and pass-through takes a few quarters.

However, due to variable price contracts, when the raw material prices go down, then the company has to give the pricing benefits to the customers by reducing the price of its goods.

From the above charts on the history of steel and ferrochrome prices, an investor would notice that in FY2015-2016, the prices of both steel and ferrochrome declined sharply. As a result, the company had to give the benefit of price reduction to the customers and its revenue declined in FY2016.

In FY2010, when the commodity prices were down as an aftereffect of the global financial crisis, AIA Engineering Ltd intimated to its shareholders that its sales have declined due to a fall in the prices of its raw materials.

FY2010 annual report, page 10:

During the year under review, your Company has registered a Turnover of Rs.80419.50 Lacs as compared to Rs.92285.95 Lacs in the previous Financial Year on account of decrease in Raw Material prices and consequently decrease in Sales Realization.

Therefore, when an investor understands the business model of AIA Engineering Ltd, then she notices that its business performance has been volatile as the company deals in raw materials whose prices keep fluctuating sharply, its customers are from cyclical industries and it has high exposure to foreign exchange volatility.

Advised reading: How to do Business Analysis of a Company

Despite an attempt by the company to incorporate variable price clauses in the contracts with its customers, it is still exposed to the risk of an impact on profit margins when raw material prices go up. The credit rating agency, CRISIL, has highlighted this aspect of the business of AIA Engineering Ltd in its credit rating report on February 26, 2021:

Operating margin remains susceptible to fluctuations in raw material prices (particularly, steel scrap and ferrochrome) and foreign exchange rates, with exporting account for 75% of sales.

Therefore, despite variable price clauses in the contracts with the customers, an investor may keep in mind that the profit margins of AIA Engineering Ltd may fluctuate significantly in line with the changes in the prices of its raw materials.

As a result, whenever an investor attempts to extrapolate the sales or the profit margins of AIA Engineering Ltd in the future, then she should keep in mind the fluctuating nature of its raw material prices, the cyclical nature of its customers’ industries, and the forever changing foreign exchange prices. These factors have led to fluctuating profit margins for AIA Engineering Ltd in the past and they may lead to significant fluctuations in its profit margin in the future as well. Therefore, an investor should keep a close watch on the profit margins of the company.

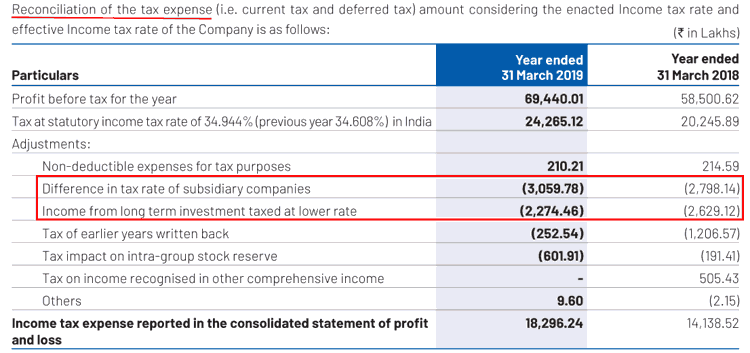

While looking at the tax payout ratio of AIA Engineering Ltd., an investor notices that in most of the last 10 years (FY2011-2020), the tax payout ratio of the company has been lower than the standard corporate tax rate prevalent in India.

An investor would notice that AIA Engineering Ltd earns a significant portion of its revenues from exports. As per the FY2020 annual report, the company generates more than 75% of its sales from exports.

FY2020 annual report, page 84:

In Fiscal Year 2019-20, 77.39% of its total sales came from outside India while balance 22.61 % came from sales from India.

In the consolidated financials of AIA Engineering Ltd, a large portion of the business is generated by its subsidiaries, which are based in foreign locations and are taxed at a lower rate than the business activities based in India.

In addition, due to the large cash & investments surplus, AIA Engineering Ltd earns a significant amount of money from returns on its long-term investments, which are taxed at a lower rate.

In the recent annual reports, AIA Engineering Ltd has provided the reconciliation of income tax paid by it and the standard corporate tax rate applicable in India. The reconciliation table highlights that the key factors leading to the lower tax payout ratio for AIA Engineering Ltd are the differential tax rate applicable to its subsidiaries and on the returns of its long-term investments.

As an illustration, an investor may note the income tax reconciliation section from the FY2019 annual report, page 198, which provides reasons for the tax payout ratio of 24% in FY2018 and 26% in FY2019.

Moreover, an investor would appreciate that in India, exporting companies get various tax incentives from the govt. As a result, the lower tax payout ratio of AIA Engineering Ltd seems to be due to its exports oriented business and returns from its long-term investments.

Further advised reading: How to do Financial Analysis of a Company

Operating Efficiency Analysis of AIA Engineering Ltd:

a) Net fixed asset turnover (NFAT) of AIA Engineering Ltd:

When an investor analyses the net fixed asset turnover (NFAT) of AIA Engineering Ltd in the past years (FY2011-20), then she notices that the NFAT of the company has declined from 4.4 in FY2012 to 3.4 in FY2020. A decrease in the NFAT over FY2012-2020 indicates that the utilization efficiency of the assets by the company is deteriorating over the years.

When an investor analyses the year-on-year trend of NFAT, then she notices that by FY2014, the NFAT of AIA Engineering Ltd had increased to 5.4. However, since FY2015, the NFAT started declining and by FY2017, the NFAT had declined to 3.3. Thereafter, the NFAT of AIA Engineering Ltd stayed at the lower levels.

When an investor analyses the capacity addition by AIA Engineering Ltd, then she notices that in FY2015, the company increased its manufacturing capacity to 260,000 MTPA from the earlier existing 200,000 MTPA.

FY2015 annual report, page 8:

The Company’s effective capacity reached 260,000 Metric Tonnes after successful commission of Moraiya brownfield expansion project during 2014-15.

An investor would appreciate that whenever any company does a new capacity addition, then it takes some time to use the new plant to optimal utilization. This is because it takes some time to get additional orders from new/existing customers to sell the additional production capacity. Therefore, normally, after a new capacity addition, the NFAT of a company would decline until the time it reaches optimal utilization levels.

Moreover, the next year, in FY2016, AIA Engineering Ltd increased its capacity from 260,000 MTPA to 340,000 MTPA, which further reduced its NFAT to 3.4 in FY2016 from 4.6 in FY2015.

FY2016 annual report, page 9:

During 2015-16, the Company increased its installed capacities to 340,000 TPA through effective commissioning of greenfield expansion at GIDC – Kerala, Phase-I and brownfield expansion at Trichy.

In addition, another factor that affected the NFAT of AIA Engineering Ltd after the new capacity addition was that the company had to sell its products at a lower price to get the business of new customers, which again lowered its NFAT because the sales from the plant were generating comparatively lower revenue.

While reading the credit rating reports of AIA Engineering Ltd, an investor gets to know that at times, the offer of low pricing to access newer markets has been the reason for the decline in the profit margins of the company.

Credit rating report by CRISIL, May 2018:

Margins contracted during fiscal 2018 due to steady input prices and competitive pricing in newer markets.

Therefore, an investor would appreciate that addition of the new capacities in FY2015 and FY2016 along with an offer of lower prices to get new customers has led to a decline in the NFAT after FY2015. As the plants of the company started to reach optimal utilization by FY2019, the NFAT of AIA Engineering Ltd increased to 4.1 in FY2019.

Thereafter, AIA Engineering Ltd increased its manufacturing capacity to 390,000 MTPA in FY2020 from 340,000 MTPA, which has led to a decline in the NFAT of the company to 3.4 in FY2020 from 4.1 in FY2019.

FY2020 annual report, page 19:

The Company has completed its first phase of Greenfield expansion of Grinding Media of 50,000 MT in August 2019. The Company’s current capacity now stands at 3,90,000 MT of annual production of high chrome mill internals.

Therefore, an investor would appreciate that the NFAT of AIA Engineering Ltd has declined over the last 10 years due to two factors; first, frequent capacity additions that took time to reach optimal utilization levels and second, reduction of the price of its products to get new customers.

Further advised reading: Asset Turnover Ratio: A Complete Guide for Investors

b) Inventory turnover ratio of AIA Engineering Ltd:

While analysing the efficiency of inventory utilization by AIA Engineering Ltd, an investor notices that over the last 10 years, the inventory turnover ratio (ITR) of the company has declined from 5.3 in FY2012 to 3.8 in FY2020. The ITR reached a high of 5.5 in FY2014 and has been on a decline since then.

A decline in the inventory turnover ratio indicates that the efficiency of utilization of inventory by the company is coming down over the years. It means that the company is using comparatively more inventory to run its business.

While analysing the business of AIA Engineering Ltd, an investor gets to know that the company has to keep inventory at many warehouses located in different places across the world near its customers so that it can quickly supply products to its customers. This arrangement increases the amount of inventory of finished goods that it needs to keep with itself all the time to meet customers’ requirements at a short notice. The company has followed this strategy for a long time.

FY2006 annual report, page 24:

Our products are very critical for the user industry and delay in supply can stop the grinding process and which can affect the whole plant. As a result, our customers require products at a short notice. To service this requirement, AIAE maintains inventory in strategic locations across the world.

The credit rating agency, CRISIL, highlighted this aspect of inventory management by AIA Engineering Ltd in its report for the company in August 2019.

AIA has to maintain high inventory due to stocking requirement across several geographies to ensure timely supplies to customer given the criticality of the product.

Therefore, an investor would appreciate that as the company has grown over the years, it has started selling in more and more countries. In FY2010, AIA Engineering Ltd had customers in about 60 countries, which increased to more than 120 countries in FY2020.

FY2010 annual report, page 34:

Worldwide presence in more than 60 countries, being directly in front of the customers through a network of overseas marketing Subsidiaries in the Middle East, Europe and USA and warehouse facilities.

FY2020 annual report, page 6:

AIA engages with customers in more than 120 countries.

An increase in the number of countries where AIA Engineering Ltd has its customers increases the requirements of the company to keep more inventory in overseas locations leading to a decline in its inventory turnover ratio over the years.

An investor may think that holding inventory in warehouses spread across the world has tied up the capital of the company; however, last year due to the coronavirus pandemic, when international shipping declined, then it could serve its customers from the stock held by it in these overseas warehouses and its business could continue to function.

FY2020 annual report, page 84:

As a strategy, we maintain stock at many locations closer to customers’ plants, which allows us to service customers from these warehouses.

Therefore, every strategy has its tradeoffs. Holding inventory in overseas warehouses used to consume a lot of capital of AIA Engineering Ltd; however, it proved very useful for the business during the coronavirus pandemic.

Going ahead, an investor should monitor the inventory turnover ratio of AIA Engineering Ltd to check whether the company is able to make any improvements in its inventory utilization.

Further advised reading: Inventory Turnover Ratio: A Complete Guide

c) Analysis of receivables days of AIA Engineering Ltd:

Over the last 10 years, AIA Engineering Ltd has had its receivables days in the range of 70-85 days. The receivables days reached a low of 68 days in FY2014; however, since then it has increased to 83 days in FY2020.

The increase in receivables days is due to offering a higher credit period to customers to gain new/additional business from foreign customers.

The credit rating agency, CRISIL, highlighted this aspect in its report for AIA Engineering Ltd in August 2019:

Besides, debtors are moderately high due to extended credit cycles to overseas clients.

Moreover, the receivables days are also high because AIA Engineering Ltd gives a guarantee to its customers for an assured performance of its products. To back the guarantee by a financial commitment, the customers retain/block a portion (about 10-20%) of the final payment to AIA Engineering Ltd as retention money.

FY2006 annual report, page 24:

Retention money for new products: For many new products introduced to the market, the company offers guarantees for the performance. For such supplies, the customer retains part of the payment (which is typically 10-20%).

AIA Engineering Ltd also highlighted the aspect of guarantee for an assured performance of its products to the customers and a resultant monetary penalty in its prospectus for the IPO in 2005 (click here).

DRHP 2005, page iii:

We guarantee the performance of our products; in terms of number of hours or in terms of wear rate in grams per tonne of product ground; to some of our domestic/overseas clients. We may have to may have to incur pecuniary liability in case the actual guaranteed performance of the products is not commensurate to the guaranteed performance.

Therefore, an investor would appreciate that the customers of AIA Engineering Ltd block about 10-20% of the total payment and release it to the company only after its products have performed to a satisfactory level. Such a blockage of money by the customers tends to increase the receivables days for AIA Engineering Ltd.

Further advised reading: Receivable Days: A Complete Guide

When an investor compares the standalone receivables position of AIA Engineering Ltd with its consolidated receivables position, then it notices that the company has a higher level of receivables outstanding for the standalone entity than its consolidated position (including all the subsidiaries). This indicates that the subsidiaries of the company are able to collect money from their customers in foreign countries; however, they delay payment of their dues to the Indian parent entity (AIA Engineering Ltd standalone financials).

AIA Engineering Ltd has highlighted to its potential shareholders in its IPO prospectus (2005) that the company gives a higher credit period to its subsidiaries because, it takes into account a long shipping period, stocking period and then the normal credit period that its subsidiaries have to give to their overseas customers.

DRHP 2005, page 117:

The debtors include the debts due from our Vega Subsidiaries to whom we have to extend higher credit up to 150-180 days. This is because this credit includes the shipment period to various destinations outside India of around 30-45 days; average stocking period of around 30 days in relation to the stocks maintained outside India; and the normal credit period of around 60 days in respect of sales effected by Vega subsidiaries to the customers outside India

This arrangement between AIA Engineering Ltd and its subsidiaries has led to higher receivables outstanding in the standalone entity when compared to the consolidated financials.

Further advised reading: Standalone vs Consolidated Financials: A Complete Guide

When an investor analyses the working capital position of the company that takes into account both the inventory and receivables position of the company, then she notices that the business of AIA Engineering Ltd is working-capital intensive, which requires a high inventory in overseas warehouses and a higher credit period to foreign customers.

The credit rating agency, CRISIL, highlighted this aspect of the business of AIA Engineering Ltd in its report in August 2019:

Operations are working capital intensive, marked by large inventory and debtors; 121 days and 87 days respectively as on March 31, 2019. AIA has to maintain high inventory due to stocking requirement across several geographies to ensure timely supplies to customer given the criticality of the product. Besides, debtors are moderately high due to extended credit cycles to overseas clients.

An investor would appreciate that if the business of any company were working capital intensive that requires a lot of investment in its inventory and receivables, then the company would face challenges to convert its profits into cash flow from operations. This is because a significant amount of profits would be stuck in working capital and would not be available as cash flow to the company.

When an investor compares the cumulative net profit after tax (cPAT) and cumulative cash flow from operations (cCFO) of AIA Engineering Ltd for FY2011-20 then she notices that the company is not able to convert its profits into cash flow from operating activities.

Over FY2011-20, AIA Engineering Ltd reported a total cumulative net profit after tax (cPAT) of ₹3,789 cr. During the same period, it reported cumulative cash flow from operations (cCFO) of ₹3,039 cr.

It is advised that investors should read the article on CFO calculation, which would help them understand the situations in which companies tend to have the CFO lower than their PAT. In addition, the investors would also understand the situations when the companies would have their CFO higher than the PAT.

Further advised reading: Understanding Cash Flow from Operations (CFO)

Learning from the article on CFO will indicate to an investor that the cCFO of AIA Engineering Ltd is lower than the cPAT due to the following factors:

- Increase in the inventory by ₹541 cr, from ₹237 cr in FY2011 to ₹778 cr in FY2020, which is deducted from PAT while calculating CFO.

- Increase in the receivables by ₹294 cr, from ₹354 cr in FY2011 to ₹648 cr in FY2020, which is deducted from PAT while calculating CFO.

- Non-operating/other income of ₹745 cr during FY2011-2020, which is included in PAT; but is deducted from PAT while calculating CFO.

The above factors led to a CFO, which is lower than the PAT of the company during FY2011-2020.

The Margin of Safety in the Business of AIA Engineering Ltd:

a) Self-Sustainable Growth Rate (SSGR):

Read: Self Sustainable Growth Rate: a measure of Inherent Growth Potential of a Company

Upon reading the SSGR article, an investor would appreciate that if a company is growing at a rate equal to or less than the SSGR and it can convert its profits into cash flow from operations, then it would be able to fund its growth from its internal resources without the need of external sources of funds.

Conversely, if any company attempts to grow its sales at a rate higher than its SSGR, then its internal resources would not be sufficient to fund its growth aspirations. As a result, the company would have to rely on additional sources of funds like debt or equity dilution to meet the cash requirements to generate its target growth.

An investor may calculate the SSGR using the following formula:

SSGR = NFAT * NPM * (1-DPR) – Dep

Where,

- SSGR = Self Sustainable Growth Rate in %

- Dep = Depreciation rate as a % of net fixed assets

- NFAT = Net fixed asset turnover (Sales/average net fixed assets over the year)

- NPM = Net profit margin as % of sales

- DPR = Dividend paid as % of net profit after tax

(For systematic algebraic calculation of SSGR formula: Click Here)

While analysing the SSGR of AIA Engineering Ltd, an investor would notice that the SSGR of the company has been more than 40% over the years. This is more than the sales growth of 11% achieved by the company during FY2011-2020.

Therefore, an investor would appreciate that the company has grown at a rate, which is well supported by its business profits. As a result, the company has been net-debt-free throughout the last 10 years. Net debt indicates a position of total debt – cash & investments.

AIA Engineering Ltd had a total debt of ₹21 cr and cash & investments of ₹303 cr in FY2011. In FY2020, the company had a total debt of ₹112 cr and cash & investments of ₹1,573 cr. Therefore, an investor would notice that AIA Engineering Ltd was net-debt free in FY2011 as well as in FY2020. This indicates that the company has grown its business at a rate, which was supported by its business profits and therefore, the company did not need any additional capital like debt or equity dilution.

An investor arrives at the same conclusion when she analyses the free cash flow (FCF) position of AIA Engineering Ltd.

b) Free Cash Flow (FCF) Analysis of AIA Engineering Ltd:

While looking at the cash flow performance of AIA Engineering Ltd, an investor notices that during FY2011-2020, it generated cash flow from operations of ₹3,039 cr. During the same period, it did a capital expenditure of about ₹1,177 cr.

Therefore, during this period (FY2011-2020), AIA Engineering Ltd had a free cash flow (FCF) of ₹1,862 cr (=3,039 – 1,177).

In addition, during this period, the company had a non-operating income of ₹745 cr and an interest expense of ₹88 cr. As a result, the company had a net free cash flow of ₹2,519 cr (= 1,862 + 745 – 88). Please note that the capitalized interest is already factored in as a part of the capex deducted earlier.

An investor notices that the company has used the surplus cash of ₹2,519 cr over FY2011-2020, primarily in the following manner:

- Paid dividends excluding dividend distribution tax of about ₹886 cr during FY2011-2020. On this, the company would have paid about 20% (about ₹175 cr as the dividend distribution tax).

- The remaining amount seems to be present with the company as a part of the cash & investments of about ₹1,573 cr in FY2020. The company used to have cash & investments of about ₹303 cr in FY2011

Further advised reading: Free Cash Flow: A Complete Guide to Understanding FCF

Self-Sustainable Growth Rate (SSGR) and free cash flow (FCF) are the main pillars of assessing the margin of safety in the business model of any company.

Further advised reading: 3 Simple Ways to Assess “Margin of Safety”: The Cornerstone of Stock Investing

Additional aspects of AIA Engineering Ltd:

On analysing AIA Engineering Ltd and after reading its past annual reports since FY2005, its IPO prospectus, credit rating reports and other public documents, an investor comes across certain other aspects of the company, which are important for any investor to know while making an investment decision.

1) Management Succession of AIA Engineering Ltd:

The promoter of the company, Mr Bhadresh K. Shah, is currently the managing director of the company. Mr Shah is currently, 69 years of age (FY2016 annual report, page 6).

While reading the annual reports of AIA Engineering Ltd, an investor does not come across any information that may indicate that any other member of the promoter family is a part of the active management of the company.

As per this article in Business Today, dated December 21, 2014, Mr Shah says that his daughters would join the board of directors. However, the article also mentions that none of them is interested in an active role in the business as one of them is a fashion designer and the other daughter is interested in chocolate making.

“At the board level, my daughters would join,” says Shah. He has two daughters – one is a fashion designer and another has interest in chocolate making.

It is advised that an investor may contact the company directly to know about the succession planning of promoters. This is because if the next generation of promoters joins when the elder generation is still around, then they get to learn the business in-depth under the active guidance of founding members. This provides for a seamless transition in leadership.

Further advised reading: How to do Management Analysis of Companies?

2) Remuneration of the promoter of AIA Engineering Ltd:

While analysing the company, an investor notices that in FY2020, the founder promoter of the company, Mr Bhadresh K. Shah took home a remuneration of ₹1.11 cr (FY2020 annual report, page 202), which is about 0.18% of the consolidated net profit after tax of ₹590 of the company in FY2020.

An investor notices that the remuneration taken by the promoter of the company as a percentage of the net profits of the company is lower than the average remuneration taken by many other promoters of different listed companies, which we have found to be in the range of 2-4% of net profits.

When an investor notices the historical trend of the remuneration taken by Mr Shah, then she notices that in the past, in FY2006, he took home a remuneration of ₹0.65 cr (FY2006 annual report, page 35), which was about 1.2% of the consolidated net profit after tax of ₹54.32 cr of the company in FY2006.

Therefore, an investor would notice that first, the promoter of the company Mr Shah has kept his remuneration at a low level of the proportion of the net profits of the company. Secondly, she would notice that over the last 14 years, FY2006 to FY2020, the remuneration of Mr Shah has increased at a rate of 3.9% per year from ₹0.65 cr in FY2006 to ₹1.11 cr in FY2020. During the same period, the consolidated profit after tax of AIA Engineering Ltd has increased at a rate of 18.6% from ₹54.32 cr in FY2006 to ₹590 cr in FY2020.

It is not to say that Mr Shah is not making money while the company is growing its business. In FY2020, Mr Shah took home a dividend of about ₹149 cr on his 58.45% shareholding in the company.

Advised reading: How to identify Promoters extracting Money via High Salaries

3) Project execution by AIA Engineering Ltd:

While reading the historical financial performance of the company, an investor notices that AIA Engineering Ltd has frequently increased its manufacturing capacity after an interval of a few years every time. The manufacturing capacity of the company used to be about 65,000 MTPA in 2005 when it launched an IPO to raise money for a planned capacity expansion. At that point in time, the company was facing a severe capacity crunch and it intimated to its shareholders that the company is not able to undertake new clients due to a lack of spare manufacturing capacity.

FY2006 annual report, page 32:

your Directors would like to place on record that the present capacities are fully booked for virtually next six to nine months, and your company is currently facing a severe capacity constraint, which would be partly relieved once the ongoing Greenfield expansion project is implemented in full.

Thereafter, the company increased its total manufacturing capacity in the following manner.

- 2007: 115,000 MTPA

- 2008: 165,000 MTPA

- 2011: 200,000 MTPA

- 2014: 260,000 MTPA

- 2016: 340,000 MTPA

- 2020: 390,000 MTPA

However, at times, the company faced some delays in completing its projects on time. On some occasions, the delay was due to outside factors involving the suppliers like in FY2018, when the expansion project of AIA Engineering Ltd was delayed due to financial troubles faced by one of its equipment suppliers. AIA Engineering Ltd could resolve the issue in 2019 and the project could be commissioned in FY2020.

FY2019 annual report, page 21:

The first phase of 50,000 Mt has been delayed on account of financial issues faced by one important equipment supplier thereby delaying supply of that equipment. We have now resolved this and expect to commission this first phase by September 2019.

Moreover, while analysing the company, an investor notices that AIA Engineering Ltd had initially planned to increase its capacity to 440,000 in FY2014 with a completion date of March 31, 2016.

FY2014 annual report, page 7:

The Company is on target in implementing its Capex plans for FY 2014-15 and 2015-16 so as to effectively augment the total available capacity from the exiting level of 2.60 Lac TPA as on 31.03.2014 to 4.40 Lac TPA by 31.03.2016.

Advised reading: Understanding the Annual Report of a Company

However, an investor realizes that after more than 5 years of its announcement, in FY2020, AIA Engineering Ltd has reached a capacity of 390,000 TPA.

Nevertheless, looking at the record of the company frequently adding to the manufacturing capacity of the company by brownfield and greenfield expansions, an investor would appreciate that the company has good project execution skills.

At times, the company intimated to shareholders about some expansion plans, which never came up. For example, in FY2007, AIA Engineering Ltd intimated to its shareholders that it is planning backward integration by putting up a ferrochromium plant and a captive power plant. However, these plants never came up.

FY2007 annual report, page 29:

The Company is also contemplating certain backward integration opportunities including setting up of a Captive Power Plant and a Ferro Chromium plant of a suitable size.

The ferrochromium plant and the captive power plant announced in FY2007 did not materialize. The company invested in power production after more than 10 years when it put up windmills for about ₹104 cr in FY2019.

FY2019 annual report, page 21:

Company has now successfully purchased and commissioned 8 windmills at a total cost of ₹104.19 crore.

Going ahead, an investor should keep a close watch on the developments related to the expansion projects and capital expenditure by the company.

4) Rivalry of AIA Engineering Ltd with Magotteaux:

While analysing AIA Engineering Ltd, an investor gets to know that the high chrome grinding media (mill internals) market is dominated by two companies globally: AIA Engineering Ltd and Magotteaux. The investor also notes that both these companies are fighting hard to prove their superiority over each other for many years. However, reading about the history of AIA Engineering Ltd brings these two companies had deeply collaborated with each other in the past.

The history of the relationship between AIA Engineering Ltd and Magotteaux forms an insightful reading for any investor attempting to analyse the company. It is a typical love-hate relationship. The following article about Mr Bhadresh Shah in Business Today provides a good insight to the investor: Casting the net wider, December 21, 2014

The article states that Mr Shah first approached Magotteaux for a tie-up in the 1980s; however, he could not succeed. As a result, Mr Shah had to collaborate with another Belgian company, Slegten SA.

In the mid-1980s, Shah approached the Belgium-based industry equipment supplier Magotteaux International for a tie-up aimed at improving his company’s technological expertise. But he didn’t succeed as Magotteaux was already in talks with a Tata group company and engineering giant Larsen & Toubro for a partnership. Shah finally joined hands with a Belgian consultancy, Slegten SA, in 1988 for design expertise.

The tie-up of Mr Shah with Slegten SA proved very successful and then, Magotteaux approached Mr Shah for a joint venture to which he agreed and the current company took shape in 1991 as AIA Magotteaux Ltd with 51% with Magotteaux and 49% stake with Mr Shah.

The tie-up with Slegten was so successful that Magotteaux approached Shah to form a joint venture. In March 1991, the new company was incorporated as AIA Magotteaux with a majority 51 per cent equity with the Belgian company and the remaining with Shah.

Around 1996, Mr Shah worked out of Magotteaux headquarters in Belgian as an employee for 1.5 years before he realized that Magotteaux and his vision about the future of AIA Magotteaux do not align with each other. Mr Shah came back to India and since then the rivalry between the two companies started.

“The new management asked me to join the parent in Belgium as an executive,” says Shah, who was also offered a minority stake in the parent company. In 1996, Shah landed in the Magotteaux headquarters. “But somehow it didn’t work out. There were a lot of differences,” says Shah, who worked in Belgium for one and a half years before coming back to India. That was possibly the worst phase of Shah’s career. After he returned to India the Magotteaux management started putting restrictions on exports from the Indian unit.

A legal battle between the two JV partners followed. Mr Shah filed a case in the Company Law Board complaining of oppression in the affairs of the company (click here).

Bhadresh Kantilal Shah vs Magotteaux International And … on 16 December, 1999

1. The petitioner hereinabove, holding 49 per cent, shares in AIA Magotteaux Ltd. (“the company”), has filed this petition under Section 397/402 and Section 403 of the Companies Act, 1956 (“the Act”), alleging oppression in the affairs of the company.

The legal disputes ended in 2000 when Magotteaux sold its 51% stake in the JV to Mr Shah by way of a settlement agreement dated February 16, 2000. This agreement allowed the company to use the technology of Magotteaux in its products; however, it put many conditions like Mr Shah has to be in control of the company always, the company cannot sell the technology and none of the two companies, AIA and Magotteaux, can buy a stake in one another for next 15 years.

IPO prospectus 2005, page 56:

Under the terms of this settlement deed, for such period of time as the Promoter owns effective majority control of our Company, our Company has the right to use in India the know how…without the payment of any fees or royalty…The Company may not disclose, sell, transfer or license the know-how to any third party. The Promoter is restricted, for a period of fifteen years from the consummation of the settlement deed from acquiring any shares of Magotteaux International S.A…

Mr Shah acquired the 51% stake of Magotteaux in the company for ₹40 cr.

IPO prospectus 2005, page 56:

Mr. Bhadresh K. Shah acquired 51% Shares of AIA Magotteaux Ltd. held by M.I. through signed Bid at a total aggregate price of Rs.400 Million.

During IPO, the company highlighted to the potential shareholders, the restrictive condition of the settlement agreement that Mr Shah should always have the majority control of AIA Engineering Ltd as a risk that can limit growth opportunities that require Mr Shah to let go of the control of the company.

IPO prospectus 2005, page ii:

The restrictions placed may have an adverse impact on the company in the event of succession in terms of royalty payment. It may also restrict our ability to enter into strategic partnerships where the Promoter is required to cede the control over management and thereby hamper our growth prospects.

Nevertheless, after the settlement agreement of February 2000 and the sale of the stake by Magotteaux, an investor would think that the issues between the two companies would end. However, it looks like it was only a start because since then, the two companies have been fighting battles in courts around the world for patents, royalties, anti-dumping duties and damages.

In 2004, AIA Engineering Ltd opposed a patent application by Magotteaux in the European Patent Office.

IPO prospectus 2005, page 144:

The Company has filed an application of opposition in the European Patent Office to the grant of Patent No. EP 0 998 353 B1 on December 22, 2004 to Magotteaux International S.A. in respect of ‘broyuer tubulaire,’ rotary mill having internal armour plating.

Thereafter, Magotteaux filed a patent violation case against AIA Engineering Ltd in the USA and the company had to pay a penalty of about ₹31 cr to Magotteaux in FY2014.

FY2014 annual report, page 48:

During the year out of the above, Company has paid US $ 6000000 (₹ 3111 Lacs) to Magotteaux International (MI), Belgium towards the Settlement of US Patent case as per the Settlement Agreement entered by the Company with the MI

However, it was not the end of disputes between the two companies. In FY2018, Magotteaux, once again, started another litigation against AIA Engineering Ltd in London asking for damages of $60 million.

FY2018 annual report, page 121:

Under the arbitral mechanism provided in Settlement Deed, Magotteaux has initiated arbitral proceedings against Mr. Bhadresh K. Shah and the Company before the International Chamber of Commerce, London (ICC) claiming the reliefs of injunction and damages inter alia alleging infringement of its Patent by the Company (in relation to the Company’s Sintercast Product) and breach of the Settlement Deed (in relation to Company’s Sintercast product). The amount involved in the said arbitral dispute is approximately US $ 60 Mn

However, Magotteaux did not succeed and had to enter into a full and final settlement agreement with AIA Engineering Ltd and Mr Shah stating that no further dispute would be raised in any other forum. As per the corporate announcements by AIA Engineering Ltd to the Bombay Stock Exchange (BSE) on October 9, 2020, the company does not have to make any payment to Magotteaux as a part of this settlement.

We are very happy to CLARIFY that the settlement does not involve any payment or make AlA Engineering Limited (AlAE) and/or Mr Bhadresh Shah liable for any payment to MI against its claims.

All claims made by MI in, arising out of, or in connection, with the Arbitration Proceedings & Challenge Proceedings (Proceedings), are permanently waived and abandoned and forever discharged with no liberty to reinstate any such claims in any forum.

Now, after about 20 years of the initial settlement agreement of February 2000, an investor may think that the issues between the two companies would have finally been settled. However, on December 18, 2020, AIA Engineering Ltd intimated to the stock exchanges that Magotteaux has complained to the trade regulator of Canada, the Canada Border Services Agency (CBSA) requesting it to put an anti-dumping duty on the products of the company (exports from India).

The Canada Border Services Agency (CBSA) announced on December 17, 2020 has initiated investigations with respect to the alleged dumping and subsidizing of certain grinding media from India the subject matter. This investigation is initiated on a complaint filed by Magotteaux Limited, located in Magog, Quebec.

Therefore, an investor would appreciate that the relationship between Mr Shah and Magotteaux, which started in the mid-1980s when Mr Shah initially approached Magotteaux for a tie-up has seen many ups and downs. However, currently, the relationship seems to be a bitter rivalry, which has affected the business of AIA Engineering Ltd in terms of sales as well as monetary penalties.

Going ahead, an investor should keep a close watch on the developments between AIA Engineering Ltd and Magotteaux, as these seem to have the potential of seriously affecting the business of the company.

Moreover, an investor should also keep a close watch on any other litigation involving patent violations about AIA Engineering Ltd. This is because, as per the learnings during the analysis of the company, an investor notices that the technology is one of the key business strengths. Established companies attempt to protect this barrier by any means whereas newcomers attempt to gain access to the technology by any means.

While reading the IPO prospectus of AIA Engineering Ltd in 2005, an investor comes across a case where the company filed litigation against M/s Balaji Industrial Products stating that it hired two employees from AIA Engineering Ltd and copied its product designs with their help.

IPO prospectus 2005, page 144:

The Company had filed a civil suit against M/s Balaji Industrial Products on the ground that it had copied designs of certain products like grinding media for zinc ore and of inserted rolls and ball sorting machine acting in concert with two former employees of the Company.

Therefore, tracking developments on these aspects is an essential part of an investor of AIA Engineering Ltd.

5) AIA Engineering Ltd could not grow in China despite more than 15 years of efforts:

While reading about AIA Engineering Ltd, an investor notices that the company is attempting to sell its products in China since at least FY2005.

FY2005 annual report, page 3:

The Company is actively pursuing penetrating Chinese market through a strategic alliance where potential for Vertical Mill spare parts is huge.

Finally, after about 5 years of efforts, in FY2010, AIA Engineering Ltd could achieve some sales in China.

FY2010 annual report, page 2:

Similarly, your Company has also started supplies to the Chinese markets.

Enthused by the initial sales in FY2010, the company formed a subsidiary in China in FY2011 named Wuxi Weigejia Trade Co. Limited.

FY2011 annual report, page 6:

During the year under review, a step-down Subsidiary Company in the name of Wuxi Weigejia Trade Co. Limited, China has been incorporated which is a Wholly-owned Subsidiary of Vega Industries (Middle East) FZE, UAE.

In FY2016, after more than 10 years of initial plans of FY2005, AIA Engineering Ltd intimated to its shareholders that it has achieved only a limited presence in the Chinese market.

FY2016 annual report, page 22:

In China, the Company currently maintains a limited presence by marketing specific products.

In FY2020, after about 15 years since the initial plans to enter China in FY2005, the Chinese market does not feature as a large source of revenues for AIA Engineering Ltd. An investor may appreciate that despite prolonged efforts, the company could not make a mark in the Chinese market, which is one of the biggest markets for mining and cement industry in the world.

6) Curious incidences of diluting stakes in subsidiaries by AIA Engineering Ltd:

When an investor reads the annual reports of the company, then she comes across a few instances when AIA Engineering Ltd diluted its stake in its subsidiaries. However, the investor is not able to understand the reasons behind the stake dilution as AIA Engineering Ltd has always been a cash-rich company and did not face any financial crunch that might have been the reason for stake dilution in its subsidiaries to outside investors.

6.1) Reclamation Welding Limited (RWL):

While analysing AIA Engineering Ltd, an investor notices that Reclamation Welding Limited (RWL) was a subsidiary of the company that owned a manufacturing plant in Ahmedabad.

IPO prospectus 2005, page 42:

RWL our subsidiary is located in plot no. 129, 130 at GVMM Estate, Odhav, Ahmedabad. The main product it manufactures is big sized mill internals individually ranging from 1.5 tons to 16 tons.

AIA Engineering Ltd used to own a 98.13% stake in RWL. However, in FY2008, the company diluted its stake in RWL to 40% by issuing shares to the other shareholders.

FY2008 annual report, page 14:

With the allotment of 64286 Equity Shares of Rs.100 each by Reclamation Welding Limited (RWL), a Subsidiary of the Company, to non-promoter Shareholder group, the Shareholding of the Company in RWL has reduced to 70% from 98.13% w.e.f. 14.03.2008.

When an investor analyses the cash position of AIA Engineering Ltd, then she notices that in FY2008, the company had about ₹120 cr of cash & investments, which included more than ₹90 cr of unutilized money raised in a qualified institutional placement (QIP) (FY2008 annual report, page 85). The company had done the QIP in December 2006.

Therefore, an investor can appreciate that AIA Engineering Ltd was not facing any financial crunch that might have forced it to sell a stake in its subsidiary, RWL.

Interestingly, after a short period of time, in FY2010, AIA Engineering Ltd merged RWL with itself, effectively, buying out/taking over the stake of the other shareholder group in RWL when it amalgamated RWL in itself.

FY2010 annual report, page 11:

During the year under review, the Company has allotted 336430 Equity Shares of Rs.2 each to the Shareholders of erstwhile Reclamation Welding Limited pursuant to the Scheme of Amalgamation

When an investor attempts to find a rough guide to the valuation of RWL in FY2008 when AIA Engineering Ltd sold the stake in RWL and the valuation at which it took over the stake of other shareholders in FY2010, then she comes across the following data points.

The FY2008 annual report does not mention at what valuation, the company diluted its stake from 98.13% to 70% in FY2008. However, an investor notices that in FY2008, the RWL had a book value (equity + reserves) of ₹10.82 cr. Therefore, the 30% stake of the other shareholder group in RWL had a book value of about ₹3.25 cr. Unfortunately, the FY2008 annual report does not mention what amount was infused by the other shareholder in RWL to increase its stake from 1.87% to 30%.

In FY2010, when AIA Engineering Ltd amalgamated RWL with itself, then it allotted 336,430 shares of AIA Engineering Ltd to the other shareholder group of RWL. At the closing share price on March 31, 2010, of ₹403 on the National Stock Exchange (NSE), these 336,430 shares were valued at ₹13.56 cr.

AIA Engineering Ltd had always been a cash-rich company and during FY2008-FY2010 when these transactions related to RWL took place, it was not short of cash & investments. Therefore, an investor is not able to understand the reasons for the dilution of its stake in RWL. Moreover, when the investor attempts to find out how much money was put in by the other shareholder group in RWL to increase its stake to 30% for which it got about ₹13.56 cr worth of shares of AIA Engineering Ltd in FY2010.

An investor may contact the company directly to understand what was the reason for the dilution of its stake in RWL in FY2008, who were these other shareholders, and the amount of money invested by them in RWL. Once she gets a firm answer to these questions, then she may make an informed opinion from this incident.

6.2) Vega Steel Industries (RSA) Proprietary Limited (3) South Africa:

Vega Steel Industries (RSA) (Proprietary) Limited (VSIRPL) was acquired by AIA Engineers Ltd in FY2010 to serve as a marketing subsidiary in South Africa.

FY2010 annual report, page

Vega Industries (Middle East) FZE, UAE, a Wholly-owned Subsidiary of the Company has acquired 100% Shares of Tuffsan Trading 295 (Proprietary) Limited, South Africa (Tuffsan). The name of Tuffsan was later changed to Vega Steel Industries (RSA) (Proprietary) Limited, South Africa.

While reading the FY2018 annual report, an investor gets to know that VSIRPL has issued additional shares during the year due to which the shareholding of AIA Engineering Ltd in VSIRPL has declined from 100% to 74.63%.

FY2018 annual report, page 154:

(3) Subsidiary of Vega Industries (Middle East) F.Z.C., U.A.E. During the year, the subsidiary had issued additional shares, which resulted in decrease of group’s shareholding.

An investor would note that in FY2018, AIA Engineering Ltd had cash & investments of about ₹1,350 cr where it had a debt of ₹123 cr on consolidated levels. Therefore, an investor would appreciate that AIA Engineering Ltd was under no pressure to sell a stake in the subsidiary to raise money.

Therefore, an investor may contact the company directly to understand the reasons for the sale of a stake in VSIRPL.

7) Overstating of profits by AIA Engineering Ltd:

While reading the annual reports of AIA Engineering Ltd, an investor comes across multiple instances where the company did not include the unrealized/mark-to-market losses on the derivatives in its profit & loss statement; thereby, overstating its profit to that extent. On multiple occasions, the auditor of the company pointed it out in the auditor’s report.

In FY2010, the company did not include losses of about ₹25 cr in its profit and loss statement and the auditor pointed it out in its report.

FY2010 annual report, page 39:

Note 9 of Schedule 17 regarding derivatives contracts entered into by the Company to hedge Foreign Currency Risk. The notional Marked – to – Market loss on these unexpired contracts as on 31 st March 2010 amounting to Rs.2537.78 Lacs has not been considered in the Financial Statements.

In the next year, FY2011, the company did not include losses of about ₹14.3 cr in its profit and loss statement and the auditor pointed it out in its report.

FY2011 annual report, page 55:

Note 9(a) of Schedule 19 regarding derivatives contracts entered into by AIA Group to hedge foreign currency risk, the notional marked-to market loss on these unexpired contracts as on 31-03-2011 amounting to ₹ 143.42 Millions has not been considered in the financial statements.

Again, in FY2012, the company did not include losses of about ₹8.3 cr in its profit and loss statement and the auditor pointed it out in its report.

FY2012 annual report, page 29:

Note No.33 regarding derivatives contracts entered into by the Company to hedge Foreign Currency Risk, the notional Mark – to – Market loss on these unexpired contracts as on 31st March, 2012 amounting to ₹829.86 Lacs has not been considered in the Financial Statements.

Advised reading: How Companies Inflate their Profits

8) Related party transactions of AIA Engineers Ltd:

While analysing the company, an investor comes across a few transactions done by AIA Engineers Ltd with its related parties that gain attention. Let us discuss a few of them below.

8.1) Purchases from Harsha Engineers Ltd:

Harsha Engineers Ltd (HEL) is one of the related party companies of AIA Engineers Ltd because the chairman of the company, Mr Rajendra Shah is the CMD (Chairman and Managing Director) of HEL.

FY2017 annual report, page 12:

NAME Mr. Rajendra S. Shah (DIN 00061922)

EXPERTISE IN SPECIFIC FUNCTIONAL AREAS: Chairman and Managing Director of Harsha Engineers Limited, manufacturers of Bearing Cages.

AIA Engineers Ltd has been purchasing a significant amount of goods from HEL over the years.

- FY2015: ₹30 cr (FY2016 annual report, page 126)

- FY2016: ₹26 cr (FY2016 annual report, page 126)

- FY2017: ₹70 cr (FY2018 annual report, page 187)

- FY2018: ₹87 cr (FY2018 annual report, page 187)

- FY2019: ₹68 cr (FY2020 annual report, page 202)

- FY2020: ₹03 cr (FY2020 annual report, page 202)

Therefore, an investor would notice that from FY2015 to FY2020, AIA Engineers Ltd purchased a total of ₹159.84 cr worth of goods from Harsha Engineers Ltd (HEL), where its chairman Mr Rajendra Shah is the CMD.

Whenever an investor comes across such instances where a company is making purchases or selling goods to the companies owned by related parties, then she should do a thorough due diligence on these transactions. This is because such transactions have a high probability of shifting the economic benefits from the minority shareholders to the related parties.

An investor would appreciate that in case a company purchases goods from the companies owned by the related parties at a price higher than the market price or it sells goods to the companies owned by the related parties at a price lower than the market price, then such transactions effectively transfer economic benefits from the minority shareholders to the related parties. This is because, in such transactions, the gains to the related parties come at the cost of the minority shareholders.

Therefore, an investor may do an in-depth analysis of the transactions of AIA Engineers Ltd with HEL. She may contact the company directly in case she wishes to get more information and clarifications about these transactions.

In the case of transactions with HEL, an investor also notices that the name of HEL is missing from the FY2015 annual report completely whereas in the FY2016 annual report, on page 126, AIA Engineers Ltd disclosed that it did purchases of ₹20.26 cr from HEL in FY2016 and purchases of ₹24.30 cr from HEL in FY2015.

Therefore, an investor is confused about whether AIA Engineers Ltd knew that HEL was a related party when it prepared its FY2015 annual report and chose not to disclose these purchases. Alternatively, it was buying goods from HEL every year; however, HEL became a related party only in FY2016 and as a result, AIA Engineers Ltd included it in the list of related parties only in FY2016. An investor may note that the CMD of HEL, Mr Rajendra Shah is a member of the board of directors of AIA Engineers Ltd for more than 15 years, even before its IPO in 2005. (FY2005 annual report, page 2)

An investor may seek clarifications from the company in this regard.

Advised reading: How Promoters benefit themselves using Related Party Transactions

8.2) loans to a minority shareholder:

While analysing the consolidated balance sheet of AIA Engineers Ltd, an investor notices that from FY2018, the company has disclosed that it has given a loan to a minority shareholder.

- FY2018: ₹37 cr (FY2019 annual report, page 186)

- FY2019: ₹15 cr (FY2019 annual report, page 186)

- FY2020: ₹93 cr (FY2020 annual report, page 181)

An investor notices that this loan to the minority shareholder only appears in the consolidated financials and not in the standalone financials. Therefore, it might indicate the loan has been given by any subsidiary of AIA Engineers Ltd to one of its minority shareholders.

Nevertheless, an investor may contact the company to get more details about the loan in terms of the name of the subsidiary and the minority shareholder, the reasons why the company has to support its minority shareholder with the loan and what are the terms like interest rate or repayment period of the loan. In case, an investor finds out that the company has offered terms, which are more lenient than the market terms like low-interest rate, then the transaction may be a favour to the minority shareholder.

9) Foreign exchange fluctuation risk management by AIA Engineers Ltd:

While analysing the annual reports of AIA Engineers Ltd, an investor notices that very frequently, the company has reported large exchange rate fluctuations losses as well as large foreign exchange fluctuation gains. The following table contains the foreign exchange gains and losses reported by AIA Engineers Ltd from FY2006 to FY2020.

An investor would note that frequently, the company has reported foreign exchange rate fluctuation gains as well as losses of large amounts in the range of ₹50 – 70 cr as well. Overall, during FY2006-2020, AIA Engineers Ltd reported a total foreign exchange gain of ₹228 cr and a total foreign exchange loss of ₹253 cr i.e. effectively a loss of ₹25 cr (= 253 – 228).

An investor may note that if a company enters into a hedging transaction using derivatives, then if the hedge is an effective/perfect hedge, then the gains and losses due to foreign exchange fluctuations do not show up in the profit and loss statement. It is only when the hedge is imperfect or ineffective hedge; the gain or losses appear in the P&L statement.

As in the case of AIA Engineers Ltd, large gains and losses appear in the P&L statement on account of foreign exchange fluctuations; therefore, it might be a case where either the hedge created by the company using derivatives is inefficient. Alternatively, the company is not creating a perfect hedge voluntarily and leaving some part of the foreign exchange risk uncovered in order to gain from the fluctuations. The second situation where a company voluntarily does not cover up its entire risk may be equal to taking a speculative position on the foreign exchange movement where a company may believe that the foreign exchange will move in its favour and it will make money.

We believe companies should avoid taking speculative positions based on their expectations of foreign exchange movements as such speculative positions may hurt the business of the company. This is because the companies should focus on the areas of their core strength and in the past, there have been many instances where manufacturing organizations had to face bankruptcy when their positions in the foreign exchange did not work in their favour.

An investor may seek clarifications from the company to understand its hedging policy in a better manner.

The Margin of Safety in the market price of AIA Engineering Ltd:

Currently (March 18, 2021), AIA Engineering Ltd is available at a price-to-earnings (PE) ratio of about 31 based on consolidated earnings for 12 months ending December 2020 (i.e. January 2020-December 2020).

However, we recommend that an investor may read the following articles to assess the PE ratio to be paid for any stock, which takes into account the strength of the business model of the company as well. The strength in the business model of any company is measured by way of its self-sustainable growth rate and the free cash flow generating the ability of the company.

In the absence of any strength in the business model of the company, even a low PE ratio of the company’s stock may be sign of a value trap where instead of being a bargain; the low valuation of the stock price may represent the poor business dynamics of the company.

- 3 Principles to Decide the Ideal P/E Ratio of a Stock for Value Investors

- How to Earn High Returns at Low Risk – Invest in Low P/E Stocks

- Hidden Risk of Investing in High P/E Stocks

Analysis Summary

Overall, AIA Engineering Ltd is a company that has grown its sales at a rate of 11% year on year for the last 10 years. However, the company faced many challenging times during this journey. The company had periods of high-profit margins followed by low-profit margins. Similarly, the company also faced years of sales decline.