The current section of the “Analysis” series covers Linde India Ltd, a company of Linde-Praxair group in India making industrial gases like Oxygen, Argon, Nitrogen etc. The company was previously known as BOC India Ltd.

To benefit the maximum from this article, an investor should focus on the process of analysis instead of looking for good or bad aspects of the company. She should learn the interpretation of different types of data and transactions and pay attention to the parts of annual reports etc. used to get the information. This will help her in improving her stock analysis skills.

Linde India Ltd: Detailed Fundamental Analysis

Until 2015, Linde India Ltd did not have any subsidiary, joint venture etc.; therefore, it used to report only standalone financials. In 2016, it formed a joint venture (JV), Bellary Oxygen Company Private Limited with Inox Air Products Private Ltd. As a result, from 2016 onwards, it started reporting both standalone as well as consolidated financials.

In the latest results reported by the company for the quarter ended Dec. 31, 2023, it has reported two JVs and three associates in its consolidated financials (Q3-FY2024 results, page 4).

Joint Ventures:

- Bellary Oxygen Company Private Limited

- Linde South Asia Services Private Limited

Associates:

- Avaada MHYavat Private Limited

- FP Solar Shakti Private Limited

- FPEL Surya Private Limited

We believe that while analysing any company, an investor should always look at the company as a whole and focus on financials, which represent the business picture of the entire company including its subsidiaries, joint ventures etc. Consolidated financials of a company present such a picture. Therefore, if a company reports both standalone as well as consolidated financials, then the investor should prefer the analysis of the consolidated financials of the company.

As a result, while analysing the past financial performance of Linde India Ltd, we have analysed the standalone financials of the company until 2015 and consolidated financials from 2016 onwards.

Further advised reading: Standalone vs Consolidated Financials: A Complete Guide

With this background, let us analyse the financial performance of Linde India Ltd.

Financial and Business Analysis of Linde India Ltd:

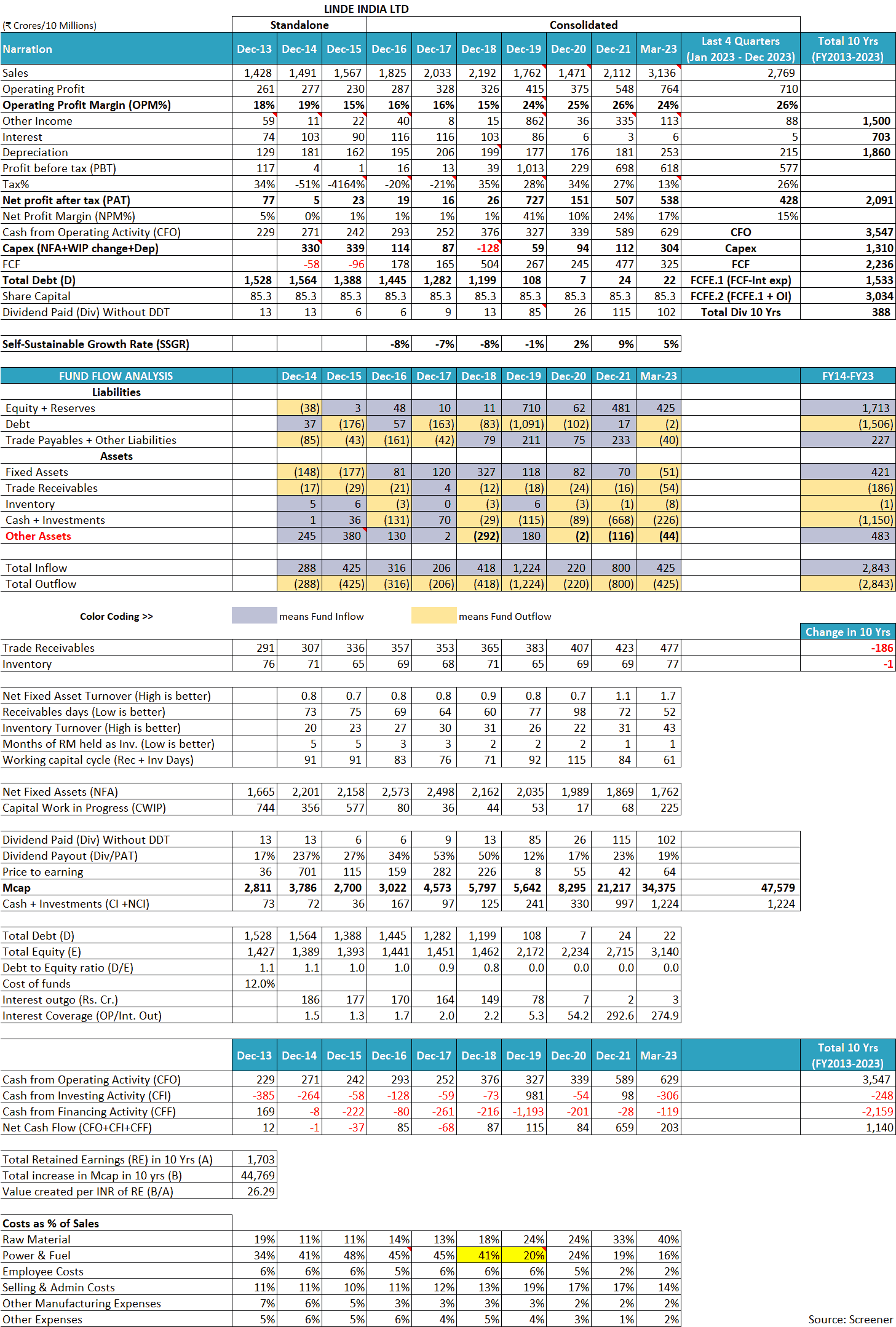

In the last 10 years, Linde India Ltd has increased its sales from ₹1,428 cr in 2013 to ₹2,769 cr in 12 months ended Dec. 2023 at an annualized growth of 7%.

The reported profit margins of the company have changed significantly over 2013-2023. Linde India Ltd had an operating profit margin (OPM) of 18% in 2013, which declined to 15% in 2015 and 2018. From 2019, the reported OPM increased significantly and is currently in the range of 24-26%.

The financial picture of the company’s historical performance presents more insights if an investor extends her analysis to the earliest available financial information from 1987 onwards present in its historical annual reports available on the website of BSE Ltd.

In the below table, we have presented the data of sales, net profit before exceptional items, net profit margin before exceptional items and the data of exceptional items each from for last 37 years (1987-2023) for Linde India Ltd.

In the 37-year historical performance of Linde India Ltd, an investor comes across many periods where its sales and profit margins declined significantly. The company reported a sharp decline in sales in 1992, 1995, 2001, 2007 and 2020. At times, the company even reported losses e.g. in 1998, 2000. On other occasions, its profitability (net profit margin before exceptional items) declined sharply e.g. in 1990, 1995, 2001, 2007, and 2012 to 2018. Overall, its profit margins have fluctuated between 17% to losses of (20%).

To understand the reasons for such fluctuations in the business performance of Linde India Ltd over the years, an investor needs to read the publicly available documents of the company like annual reports from 1997 onwards, credit rating reports, as well as its corporate announcements.

After going through the above-mentioned documents, an investor notices the following key factors, which influence the business of Linde India Ltd. An investor needs to keep these factors in mind while she makes any predictions about the performance of the company.

1) Intense competition in the industrial gases business from multinational companies (MNCs) as well as the unorganized segment:

Many large MNC players, numerous medium-sized domestic players, as well as a large number of small-sized players from the unorganized sector, provide each other with intense competition for business in the Indian industrial gases segment.

Credit rating report by CRISIL, July 2014:

Linde India faces significant competition from both the organised (other international players present in the Indian market) and unorganised sectors.

Due to a large number of players, the Indian industrial gases business has continuously faced overcapacity leading to players strongly competing with each other to keep their plants running. This was especially true during the FY2012-FY2018 period when Linde India Ltd saw its net profit margin (NPM) before extraordinary items significantly fall to the 0%-3% range.

FY2016 annual report, page 15:

The Gases business in India continues to be impacted by overcapacity in the market…which led to lower plant loading with adverse impact on specific power.

FY2015 annual report, page 14:

There has been significant product oversupply in the markets with number of new ASUs coming on-stream while demand continued to be weak.

FY2014 annual report, page 16:

over supply position in the markets resulted in significant under utilisation of installed capacities, further impacting the financial performance.

The intensely competitive position of the industrial gas business in India has been a continuous issue for players like Linde India Ltd. Even at the start of the current century, the company faced intense competition from both large and small players.

FY2002 annual report, page 18:

Indian economy has seen the entry of all the major international gas companies in the country and presently the industry is organised around six big players with an all India presence, twelve medium sized companies and about two hundred small scale regional players. The industry is likely to see greater consolidation in future with increasing competitive pressure.

FY2000 annual report, page 5:

With two new bulk tonnage plants, our own at Jamshedpur and a competitor’s plant at Hospet, having come on stream within six months of each other, the supply of industrial gases exceeded demand substantially.

As a result, going ahead, the competitive intensity in the industry is expected to remain severe.

Also read: How to do Business Analysis of Chemical Companies

2) Non-differentiable, commodity products make the industrial gases market extremely price sensitive. Linde India Ltd does not have pricing power over its customers:

Linde India Ltd makes industrial gases like oxygen, nitrogen, argon etc., which are non-differentiable from such gases produced by its competitors. Therefore, any customer can easily use gases produced by any manufacturer as long as they meet the same purity and concentration specifications.

Credit rating report by CRISIL, July 2014:

domestic industrial gases industry remains intensely competitive because of the commodity nature of products.

The ability of customers to replace one supplier of gases with another without any significant impact on business provides them with a higher negotiating power over industrial gas suppliers. This coupled with the overcapacity in the gas segment and intense competition takes away pricing power from gas manufacturers.

As a result, industrial gas manufacturers face intense price-based competition where competitors tend to undercut profit margins of each other.

FY2023 annual report, page 20:

Intense competition is observed…with a lot of overseas players willing to compromise on margins for newer markets…Predatory pricing with compromising margins is dominating the commercial discipline to load new capacity.

The company has faced intense price-based competition continuously in the past as well. For example, in 2010, it intimated its shareholders about the pricing pressure due to overcapacity in the industry.

FY2010 annual report, page 13:

The gases market in India has witnessed significant addition to capacities by almost all gas majors…As a result, the gases market which is already competitive, is expected to remain so with ongoing pricing pressures

In 2003, the company highlighted the highly price-sensitive nature of the market.

FY2003 annual report, page 19:

The competitive scenario as well as large scale capacity additions over the last few years have made the market extremely price sensitive

In FY1998 and FY2000, when the company reported losses, then it highlighted that depressed prices due to competition has led to losses.

FY1998 annual report, page 11:

Additionally, competitive pressures have also severely depressed prices of the Company’s products during the year adversely impacting the revenues for the year.

FY2000 annual report, page 5:

the state of heightened competition with the entry of other multinationals, the price of gases in the merchant market could not be increased adequately and margins remained under severe pressure.

As a result, of intense price-based competition, the company could not pass on an increase in input costs like power to its customers and had to take a hit on its profit margins. For example, in FY2007 and FY2012, it mentioned that it could not recover increased costs from its customers.

FY2007 annual report, page 19:

power tariff in Maharashtra which increased by approximately 27% over last year’s rates, also impacted the profitability as the entire cost increase could not be passed on to the customers.

FY2012 annual report, page 11:

The power cost increase in West India was quite significant and the sluggish market situation made it difficult to fully recover such increased costs, thereby putting margins under pressure.

The lack of pricing power of Linde India Ltd is visible in two other instances. First, in FY2003, when the power cost of the company declined, then it had to immediately pass on the benefit to its customers leading to lower prices and thereby a lower revenue, which was in sharp contrast to the case of an increase in power prices, which it could not recover from its customers.

FY2003 annual report, page 19:

Gases and Related Products: The turnover, however, remained flat as the increase in volume was neutralised by revenue de-escalation as a result of reduction in power rate by the power supplier

In FY2001, the company received a substantial demand of ₹52.4 cr from its power supplier, which the company stated was substantially recoverable from its customers.

FY2001 annual report, page 2:

Company has received…demands…on account of fuel surcharge…amounting to Rs. 524 million with retrospective effect from 1995-96…a substantial part of the arrear power fuel surcharge will become recoverable from its contracted customers by your Company.

However, in FY2002, the company intimated that it had to bear a loss of ₹13 cr as out of ₹52.4 cr, it could only recover ₹39.4 cr from its customers, which indicated its lower pricing/negotiating power over its customers and suppliers.

FY2002 annual report, page 42:

demands…amounting to Rs. 524,067 thousand…out of which Rs. 393,768 thousand is recoverable from contracted customers…The net amount of Rs. 130,299 thousand…has been charged as an extraordinary item

Therefore, an investor should always keep in mind that Linde India Ltd produces commodity products in an intensely competitive market where its customers can easily replace products of one supplier from another. As a result, it bears very low pricing power over its customers and faces intense price-based competition from its peers, which has impacted its profit margins in the past even leading to losses.

Also read: Why We cannot always Trust What Management Claims

3) Cyclical business of Linde India Ltd in industrial gases as well as project engineering division:

The main business activity of Linde India Ltd is to produce & sell industrial gases to manufacturing companies in its Gases & Related Products division and to create industrial gas plants for captive use by manufacturing companies in its Project Engineering division.

Both these divisions primarily service customers in the steel & fabrication and automobile sectors. Therefore, the business performance of Linde India Ltd is linked primarily to the prospects of steel, and automobile sectors.

Moreover, both steel and automobile sectors are highly cyclical in nature, which in turn, brings cyclicity in the business performance of Linde India Ltd with alternating boom and bust periods of performance.

Credit rating report by CRISIL, July 2014:

steel and other metallurgical industries account for around two-third of its revenue from the gases segment, leading to end-user industry concentration. The inherent cyclicality in this segment exposes the company to sluggish growth during economic downturns

The business of the project engineering division (PED) is also highly dependent on the steel and oil refinery sector, which are highly cyclical.

FY2014 annual report, page 16:

PED’s business is primarily driven by capacity expansion in steel and refinery segments.

As a result, whenever these sectors (steel, automobile, oil refining etc.) do well, then Linde India Ltd also reports good performance e.g. in FY2023 when on a 12-month basis, the company reported a revenue growth of about 18%.

FY2023 annual report, page 15:

growth in Gases revenue was driven by higher merchant liquid demand in line with economic recovery, increase in gas consumption by steel sector…Our Project Engineering business continues to perform strongly with healthy order book position supporting mainly steel, refineries, and electronics sectors

Similarly, in FY2021, when Linde India Ltd reported a 43% increase in revenue, then apart from excessive demand for medical oxygen due to the Covid pandemic, a strong recovery in the steel and oil refining sectors played a huge role.

FY2021 annual report, page 17:

growth in the Gases revenues during the year 2021 was mainly driven by liquid and compressed medical oxygen…during the 2nd wave of Covid-19…growth in the Project Engineering business was driven by…strong performance of the engineering business across steel and refinery sectors…significant demand for gases from customers mainly Tata Steel, SAIL and Jindal Stainless.

Similarly, in FY2014, when its major customers in the steel industry were not doing well due to the economic downturn, Linde India Ltd reported poor performance with almost 0% profit margin.

FY2014 annual report, page 16:

Company recorded a subdued performance during the year under review, amidst weak economic conditions and contraction of demand in most of the end user industry segments.

The company had faced similar headwinds leading to poor performance in FY2012 when its end user consumer industries did not perform well.

FY2012 annual report, pages 11-12:

Company had to contend with significant headwinds, which among others included lower demand from major customers, delay in major projects related to customer delays…demand landscape from some of the major customers forced some of our tonnage plants to operate at lower than full capacity

During FY1998 and FY2000 when the company reported losses, it was primarily due to a slowdown in the sectors like steel and automobile.

FY1998 annual report, page 12:

slowdown began towards the end of 1996…Infrastructure industries like steel, automobiles, petrochemicals, fabrication and metal working, etc. have borne the brunt of this recession. Since your Company is essentially in the business of being a preferred vendor to the bulk of these industries, it could not escape the beating

FY2000 annual report, page 5:

The loss of Rs 794 million in the 18 months period is the cumulative result of several factors…given the sluggish growth in the steel fabrications, ship making and scrap cutting sectors, which constitute the largest part of the Company’s customer base

As a result, an investor should always see the performance of Linde India Ltd as linked to the performance and prospects of its key consumer industries of steel, automobile, electronics, oil refinery etc. She should not get carried away by the good performance of the company during upcycles in these industries because when these industries undergo a downcycle, then the performance of Linde India Ltd would also be impacted.

Also read: How to analyse New Companies in Unknown Industries?

4) Attempts by Linde India Ltd to diversify its customers’ industry base:

Over the years, Linde India Ltd has taken multiple steps to reduce the impact of cyclicity due to the concentration of its customers’ industries.

It attempted to find customers in industries other than steel and automobiles. In FY2012-FY2014, it won customers in the cement and aluminium industries.

FY2014 annual report, page 18:

your Company was successful in converting a number of its gases application leads into business with customers including wins in new sectors like cement and aluminium

During FY2017-FY2018, it won customers in the refineries sector, quick freezing application (food storage) and tyre sector.

FY2018 annual report, page 1:

we have won our first major customer in the refinery sector…a key customer has invested in our Instant Quick Freezing application, cryogenic freezing with liquid nitrogen, and we have acquired our first nitrogen application for tyre curing

In FY2011, the company diversified into the production of CO2 by making an acquisition.

FY2011 annual report, page 12:

Company completed acquisition of a merchant CO2 business. This business has added CO2 as a new product line and caters mainly to the beverage and engineering segments

In FY2021, it expanded its presence in the “Packaged Gas and Micro Bulk” market of Western India by acquiring business from HPS Gases Ltd.

FY2021 annual report, page 120:

Company has acquired from HPS Gases Ltd., Vadodara its entire packaged gases business…The aforesaid acquisition will help expand Linde’s presence in Packaged Gas and Micro Bulk market in Western India.

Linde India Ltd also started serving export orders in its project engineering division by contributing to overseas projects undertaken by Linde group companies.

FY2016 annual report, page 15:

The Division is continuing its efforts to get orders in the overseas markets and has received an order for a nitrogen plant from JGC Japan for their project in Indonesia and another order for a merchant ASU for one of The Linde Group companies in Malaysia.

In the past, the company focused on diversifying its revenue base by selling oxygen concentrators and nebulisers of Air-Sep of USA in India in FY2000 and FY2001.

FY2001 annual report, page 18:

As per the agreement with Air-Sep of USA, and following a good market response to the Oxygen Concentrator, your Company has recently introduced Nebuliser to supplement its home care equipment product range.

In FY2006, the company also diversified its business by re-entering welding equipment and medical engineering services that it had exited in the past.

FY2006 annual report, page 11:

Some of our recent offerings include the re-entry into the welding equipment and Medical Engineering Services

In FY2001, the company even proposed to enter into the LPG distribution business; however, it seems that this initiative did not work out properly as the company never focused on it in the subsequent annual reports.

FY2001 annual report, page 20:

Company is also exploring the possibility of entering the LPG distribution business and is currently in advanced stage of discussions with an oil major.

As per its latest disclosures, Linde India Ltd is planning to serve customers of the semiconductor segment and is setting up a nitrous oxide plant.

FY2023 annual report, page 3:

For strengthening our presence in the semiconductor segment, the Company is setting up a high purity Nitrous Oxide facility at its existing Hyderabad plant.

An investor needs to monitor how this initiative by Linde India Ltd turns out as previously the initiative by the company in FY2008 to enter into the solar photovoltaic business did not turn out well for the company.

In FY2008, the company made significant investments to enter into the solar photovoltaic business.

FY2008 annual report, page 11:

Company made strategic investments focusing on the solar photovoltaic business…also setting up infrastructure for manufacturing, storing and pipeline distribution of high value electronic gases in a Special Economic Zone in the State of Andhra Pradesh to customers in photovoltaic space.

However, soon, in FY2011, this business witnessed a significant slowdown.

FY2011 annual report, page 12:

electronic gases business serving the solar photovoltaic industry witnessed a significant slowdown as compared to last year.

In the next year, FY2012, the company suffered a significant setback when one of its major customers from the solar photovoltaic industry shut down its business as its technology became unviable/uncompetitive. As a result, Linde India Ltd had to write off its investments in the solar photovoltaic business.

FY2012 annual report, page 13:

one of the major electronic gases customer discontinued operations in view of their thin film photovoltaic cell technology becoming uncompetitive…Company had to take a significant hit by way of impairment of assets at the customer’s plant

Therefore, investors need to keep a close watch on the entry of the company into new industry segments.

Also read: How to analyse New Companies in Unknown Industries?

5) Focus of Linde India Ltd on improving cost competitiveness:

As Linde India Ltd operates in a commoditised products business facing intense price-based competition; therefore, the key way to increase profitability and earn a competitive advantage over its peers is to be the lowest-cost producer of goods. As a result, over the years, Linde India Ltd has undertaken various measures to enhance its cost efficiencies.

5.1) Economies of scale:

Over the years, Linde India Ltd has created numerous plants for producing industrial gases, both for selling gas in the open/merchant market as well as dedicated plants in customers’ premises with take-or-pay arrangements.

Credit rating report by CRISIL, January 2017:

significant proportion of revenue in the gas segment comes from installation/tonnage, where the company enters into long-term (15-20 years) take or pay contracts with customers, which provide stable cash flow and profitability and prevent significant decline in revenues during downturn.

Numerous large-sized tonnage plants as well as air separation units (ASUs) have helped the company in lowering its cost of operations as the company can spread its fixed expenses over a larger production base.

FY1997 annual report, page 16:

Due to economies of scale arising out of this project, your Company would have the critical advantage of a low-cost product source for meeting the merchant demand

As a result, the company significantly increased the size of its operations both by installing new gas plants as well as acquiring plants from other companies. In FY2010, it acquired three plants of 1,050 TPD from Tata Steel (FY2010 annual report, page 10). In FY2012, it acquired the gas business of Uttam Gases (FY2012 annual report, page 13).

As the company’s scale of operations increased, it implemented steps like a new logistics organization for economies of scale benefits.

FY2003 annual report, page 19:

setting up of a new logistics organisation focusing on customer service, fleet and asset utilisation and achieving overall economies of scale in the supply chain.

In FY2010, the company commissioned a national scheduling centre for efficient utilization of its transportation fleet from a common centre.

FY2010 annual report, page 13:

commissioning of the national scheduling centre and the fleet control room at Kolkata.

In the same year, it also operationalized a remote operating centre in Singapore, which helped it schedule the production of gases in various plants for their most efficient utilization.

FY2010 annual report, page 12:

to drive improved safety, efficiency and reliability in operations of the tonnage plants, the Group had earlier set up Remote Operating Centre (ROC) in Singapore, which is already operational and successful.

In addition, Linde India Ltd also undertook measures like removing low-capacity tankers from its transportation fleet so that it may economically move more gas using higher-capacity tankers.

FY2018 annual report, page 11:

several measures to improve efficiency of the distribution function such as phasing out of low capacity tankers, introduction of 7KL tankers with flow meter for medical supplies

FY2019 annual report, page 12:

Company continued its focus on improving efficiency of the distribution function by phasing out of old 3 and 5 KL VITTs…improving delivered quantity per trip by about 9%, reducing product loss in distribution by 10%

Advised reading: How to study Annual Report of a Company

5.2) Reuse/shifting of plants from one location to another to extract maximum value from these assets:

Over the years, Linde India Ltd has ensured that it derives maximum value from it manufacturing plants.

In FY2000-02 when its existing 120 tonnes per day (TPD) plant at Jamshedpur was lying unutilized because it had installed a new, larger 1,290 TPD plant in 1998, then it refurbished the old plant and relocated it from Jamshedpur to Dolvi in Maharashtra for Ispat Industries Ltd. Due to this reuse, the company could extract more value from its plant.

FY2000 annual report, page 5:

relocation of the refurbished 120 tpd plant from Jamshedpur to Maharashtra for an attractive medium term contract is another step in the right direction

FY2003 annual report, page 9:

successful commissioning of the Company’s idle 100 tpd plant at Dolvi which was relocated from Jamshedpur

Subsequently, in FY2014, Linde India Ltd relocated its other air separation unit (ASU) plant from Taloja in Maharashtra to Dahej in Gujarat to extract maximum value from it.

FY2014 annual report, page 19:

PED is also engaged in dismantling and relocating the 110 tpd ASU from Taloja and its commissioning at a new site at Dahej.

5.3) Closing down unviable plants, selling down business units and properties to monetize idle assets:

Linde India Ltd closed down multiple manufacturing units that had become economically unviable to operate. In some cases, it could revive the units after making significant changes in manpower etc. whereas in a lot of cases, it sold the land, and plant & machinery.

For example, around FY2000, it closed multiple units in Kanpur, Guwahati, Asansol and Ghatkopar.

FY2000 annual report, page 5:

Over the past decade, BOC India has taken several steps to make itself a more focussed and lean organisation…unviable units at Kanpur, Guwahati, Asansol and Ghatkopar (Mumbai) were closed and where possible, idle assets were disposed off.

Out of these, the company revived the Asansol unit by getting rid of its surplus labour and reopening the unit with reduced manpower.

FY2004 annual report, page 4:

The re-opened Asansol unit commenced production with reduced manning and has been able to build-up production quickly to serve the local markets.

For the remaining units, it sold off the land/properties. Interestingly, over the years, Linde India Ltd has disposed of so many assets that “exceptional items” from the sale of assets have become almost a regular feature in its financial statements.

- FY1997: ₹1.1 cr from sale of land and factory at Kanpur, UP.

- FY1998: ₹30.7 cr from sale of Ohmeda healthcare business.

- FY2001: ₹15.5 cr from sale of Delhi factory

- FY2002: ₹10.6 cr from the sale of the property at Bandra, Mumbai

- FY2003: ₹13.5 cr from sale of property at Delhi

- FY2004: profit of ₹25.4 cr from sale of property at Ghatkopar, Mumbai

- FY2005: profit of ₹3.5 cr from sale of the factory in Ranchi and a flat in Mumbai

- FY2006: ₹49 cr from sale of plant at Bangalore. In addition, flats in Chennai and Jamshedpur were also sold.

- FY2007: ₹61 cr from the sale of the plant at Sanatnagar, Hyderabad and ₹24 cr from the sale of land at Tondiarpet, Chennai.

- FY2008: ₹24.6 cr from sale residual interest in land and building in Hyderabad

- FY2011: sale of land in Joka, Kolkata

- FY2012: profit of ₹72 cr from sale of land at Vizag and Bangalore.

- FY2013: ₹50 cr from sale of land in Ahmedabad and profit of ₹4.3 cr from sale of right of use asset in Kolkata

- FY2014: profit of ₹6.6 cr from sale of the right to use of flat in Kolkata

- FY2016: profit of ₹15.6 cr from sale of factory in Tarapur, Maharashtra.

- FY2019: ₹1,380 cr from sale of “South Region Divestment Business” as per directions of Competition Commission of India (CCI) for the merger of Linde Group and Praxair Group.

- FY2020: ₹300 cr from sale of land and building of factory in Kolkata. In addition, ₹55 cr from the sale of a stake in “Belloxy Divestment Business” to Inox Air Products Pvt. Ltd to meet CCI requirements.

Over the last 37 years (1987-2023), the company reported a total exceptional profit of ₹1,092 cr, which is comparable to net profit after tax and before exceptional items of ₹1,707 cr over this period.

5.4) Relieving excess employees via voluntary retirement schemes (VRS):

Over the years, Linde India Ltd did multiple rounds of VRS in many plants to reduce its manpower costs and increase its operating efficiency.

For example, in the 1990s, the company removed almost 90% of its workforce.

FY2000 annual report, page 5:

In the process, during the decade, the workforce has come down from 5124 employees in 1990 to 660 in March this year.

Thereafter, in the slowdown of 2008-2009, the company froze all recruitment and focused on reducing manpower using VRS.

FY2009 annual report, page 14:

to minimize the impact of the slow down on the Company’s business, your Company had to initiate a freeze on recruitment and also launched a voluntary separation scheme

Thereafter, in FY2015, the company again spent a significant amount to relieve employees via VRS.

FY2015 annual report, page 14:

incurred an amount of Rs.95 million towards a voluntary retirement scheme

5.5) Attempts to reduce power costs by Linde India Ltd:

The production of industrial gases is a very energy-intensive process. As a result, power and fuel cost is one of the major input costs for Linde India Ltd.

As a result, over the years, the company has undertaken many steps to reduce its power cost.

In FY1998, the company replaced it Jamshedpur plant with a newer technology plant with almost 50% specific power consumption than the older plant.

FY1998 annual report, page 13:

Jamshedpur 120 tonnes-per-day (tpd) plant was closed and an energy efficient 1290 tpd plant of latest technology was commissioned… Specific power consumption of this plant is less than 50% of the old plant.

The company streamlined its operations and focused on running its plants maximum during non-peak energy tariff periods.

FY2002 annual report, page 22:

Operations of the Tonnage Plants at Taloja and Tarapur were optimized to have maximum benefit of non-peak energy tariff.

By FY2016, the company started sourcing power from open access mechanism to benefit from lower spot prices to reduce its power costs.

FY2016 annual report, page 12:

Alternative sourcing of power through open access mechanism resulted in reduction in power cost, thereby making the gases business more competitive.

In the recent period, FY2023, the company has made significant investments in captive solar power to reduce its power costs.

FY2023 annual report, page 1:

The primary objective of these investments is to gain access to renewable power procurement under a captive mechanism. By utilising this mechanism, we aim to secure renewable power at lower tariffs, leading to significant cost savings for our operations.

5.6) Focus on reducing finance/interest costs:

Over the years, Linde India Ltd has expanded its capacity at a fast pace for which it had to raise a lot of debt.

Credit rating report by CRISIL, July 2014:

moderation in the company’s financial risk profile over the last 3 years on account of large debt funded capital expenditure

High debt on the balance sheet of Linde India Ltd had continuously put pressure on its profit margins due to high finance costs.

Over the years, the company has taken multiple steps to control its finance cost and improve its profit margins like refinancing high-cost debt with low-cost debt.

In the early 2000s, the company refinanced a large portion of its debt and saved about ₹4-5 cr of interest costs each year.

FY2001 annual report, page 2:

replacing high cost borrowings with lower cost debentures. In addition, better working capital management and tighter controls have generated a savings of Rs. 53 million in interest cost over the previous year

FY2002 annual report, page 1:

cost saving of approximately Rs.44 million has been achieved by way of a reduction in interest charge as a result of substitution of high cost loans with lower cost borrowings.

In FY2004, it achieved further savings of ₹4.4 cr.

FY2004 annual report, page 21:

reduction in borrowings together with the continuing restructuring of high cost borrowings resulted in a significant reduction of Rs. 44.32 million in interest charges.

In 2007-2008, Linde Group acquired BOC Group and thereafter, Linde Group infused about ₹600 cr in Linde India Ltd (then named BOC India Ltd), which the company used to repay its entire debt and became a debt-free company leading to substantial interest cost savings.

FY2008 annual report, page 13:

During the year, the Company received a sum of Rs.5973 million from the promoter Group…Company utilised a sum of Rs.2190 million towards repayment of its existing borrowings, thus becoming a ‘zero debt’ company at present.

Thereafter, the company raised more debt including debt from its promoter Linde Group to expand its manufacturing capacity. However, in 2020, when the company had to sell its southern region business to comply with conditions put by CCI for approving the merger with Praxair group, then it used the sale proceeds to repay its entire debt and reduce its interest cost.

FY2020 annual report, page 13:

steep reduction in the interest cost from Rs.862.50 million during 2019 to Rs. 62.43 million during the year…result of repayment of all the outstanding borrowings from the proceeds of divestment of South Region Divestment Business.

Therefore, even though the company had to raise debt to create manufacturing plants, it tried to reduce its interest costs by repaying debt whenever it could raise cash from promoters or the sale of assets. These steps helped in improving the profit margin of the company.

Also read: How to do Financial Analysis of a Company

6) Regulatory/govt. policy risk faced by Linde India Ltd:

On numerous occasions, Linde India Ltd’s business was impacted by regulatory steps. For example, in FY1997, it had to close down its factory in Delhi after the Hon. Supreme Court directed the closure of all hazardous factories within Delhi.

FY1997 annual report, page 4:

businesses were adversely affected by the closure of your Company’s Delhi unit at Kirtinagar from end November last year, following the Hon’ble Supreme Court’s order of 8 July 1996.

In FY2014, the pricing power of Linde India Ltd was impacted when govt. put a ceiling on the price of medical oxygen and nitrous oxide gases as emergency drugs.

FY2014 annual report, page 18:

Government of India, fixed a ceiling price for medical oxygen and nitrous oxide by classifying them as emergency drugs.

However, it is not a case that all the regulatory interventions have impacted the company adversely. At times, the company benefited as well. For example, in FY2000, the govt. exempted medical gases from excise duty, which helped it compete with the unorganized sector.

FY2000 annual report, page 11:

Understanding the importance of medical gases, the Government of India has now exempted it from levy of excise duty enabling your Company to compete aggressively with the unorganised sector.

In FY2010, when govt. of India provided various incentives to industries to aid in recovery from the global financial meltdown, and then Linde India Ltd benefited from the recovery of demand from its consumer industries.

FY2010 annual report, page 10:

improvement over the previous year following consistent revival in the various end user industry segments driven by fiscal stimulus packages put in place by the Government

In FY2016, to protect the domestic steel industry, govt. of India put in place policies like minimum import price for steel. It reduced low-priced import competition for domestic steel producers, which in turn increased demand for Linde India Ltd.

FY2016 annual report, page 12:

Minimum import price restriction put on import of steel, last year, has helped Indian steel industry and thereby gas industry.

As discussed earlier, in FY2021, Linde India Ltd benefited significantly from the humungous demand for medical oxygen due to the Covid pandemic. However, realizing the shortage of medical oxygen, govt. mandated and supported pressure swing adsorption (PSA) oxygen-generating plants in hospitals, which impacted the demand for medical oxygen produced by Linde India Ltd.

FY2023 annual report, page 20:

With impetus from government financing & NGO’s approx. 3,756 PSA plants are currently operational in the country, impacting liquid medical oxygen sales.

Therefore, an investor should always keep a close watch on regulatory and policy developments related to Linde India Ltd.

7) FY2019’s sharp reduction in revenue and increase in profit margins:

In FY2019, the revenue of Linde India Ltd declined sharply by about 20% to ₹1,762 cr from ₹2,192 cr in FY2018. At the same time, the operating profit margin (OPM) of the company increased sharply to 24% in FY2019 from 15% in FY2018.

The main reason for such a sharp change in the reported financial performance of Linde India Ltd was the adoption of Ind AS 115 on “Revenue from Contracts with Customers.” As a result of the new accounting standard, that power & fuel cost for onsite plants, which was earlier a pass-through as per the contract with customers and was included both in the revenue and in the power & fuel cost is now removed from the revenue as well as power & fuel costs.

As a result, both the revenue as well as power & fuel costs declined by the amount of pass-through power cost whereas the amount of profit stayed the same.

This changed treatment of power cost resulted in a decline in revenue by the amount of now-removed power cost whereas the profit margin increased sharply due to the profit amount staying stable whereas the revenue amount declined in the ratio calculation.

The actual gas revenue of the company during FY2019 net of this accounting impact had actually increased by 3.1%.

FY2019 annual report, pages 8-9:

decline of about 19.6% in the total revenue from operations is mainly on account of adoption of Ind AS 115 on “Revenue from Contracts with Customers”…power and fuel cost in respect of onsite plants, which in the previous year was disclosed gross has now been shown net of sales related costs reimbursed by the customer. This has resulted in reduction in revenue and a reduction of an equal amount in power and fuel cost to the tune of Rs.4,976.61 million…gases revenue for the year 2019 without the adjustment as per Ind AS 115, however, recorded a growth of about 3.1%.

This however, had a positive impact on the operating margin, though operating profit from the gases business remained unaffected.

Therefore, an investor needs to keep in mind this change in accounting policy when assessing the sharp reduction in revenue in FY2019 and the sharp increase in OPM from FY2019 onwards.

Going ahead, an investor should keep in mind the intense, price-based competition faced by Linde India Ltd due to the commodity nature of its products and its low pricing power due to its customers being very large steel players like Tata Steel, JSW Steel, SAIL etc. She should factor in the cyclical nature of its business and acknowledge that in the past, periods of increasing profit margins have been followed by periods of declining performance even leading to losses.

Therefore, the investor should be cautious before she extrapolates any period of good performance of Linde India Ltd in the future.

For many years, the tax payout ratio of Linde India Ltd had been in sharp variation than the prevailing corporate tax rate in India.

For example, in FY2015, the company reported a profit before tax (PBT) of ₹1 cr; however, it reported a profit after tax (PAT) of ₹23 cr. This was because, during the year, the company availed tax benefits on its ASU plant in Kalinganagar, Odisha leading to benefits of about ₹25 cr.

FY2015 annual report, page 14:

During the year, your Company availed tax benefit…its Air Separation Units at Kalinganagar, which has resulted in deferred tax release of Rs.253.26 million.

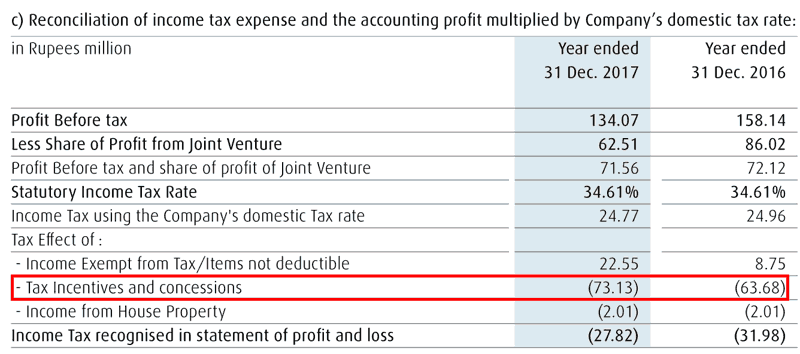

Similarly, in both FY2016 and FY2017, the company reported its PAT higher than PBT due to income tax incentives and concessions.

FY2017 annual report, page 148:

In FY2019, the company reported a lower tax payout ratio of 28% because the profit on the sale of its southern business attracted long-term capital gains, which was lower than the business income tax rate (FY2019 annual report, page 161).

In FY2023, the company reported a lower income tax rate of 13% because it decided to switch to a new lower corporate tax rate, which led to a reduction in deferred tax liabilities and hence a lower tax payout ratio.

FY2023 annual report, page 14:

Company has elected to exercise the lower tax rate of 22% (effective rate of 25.168%) permitted under the new tax rate regime…beginning 1 April 2022 resulting in lower tax expense and re-measurement of deferred tax liabilities.

Recommended reading: How to do Financial Analysis of a Company

Operating Efficiency Analysis of Linde India Ltd:

a) Net fixed asset turnover (NFAT) of Linde India Ltd:

The net fixed asset turnover (NFAT) of Linde India Ltd in the past years (FY2013-23) has improved from 0.8 in FY2014 to 1.7 in FY2023. The improvement of NFAT in recent years FY2021 and FY2023 is due to high medical oxygen demand during the Covid pandemic and due to the sharp recovery of the steel industry post-pandemic. Nevertheless, the NFAT of the company at levels of 1 or below indicates that the business of manufacturing industrial gases is very capital-intensive.

Credit rating report by CRISIL, July 2014:

business of onsite sales is highly capital intensive, involving large capex, long gestation period, and lengthy payback

The company also acknowledged the capital-intensive nature of its business to its shareholders in the FY2010 annual report highlighting large investments in setting up ASUs and distribution assets.

FY2010 annual report, page 11:

The gases business is capital intensive by nature as it requires large investments in setting up of air separation units. The supply chain in the gases business also requires significant investments in the form of distribution assets and storage networks

Moreover, despite large capital investments, when technology changes, then the company has to write off its assets leading to a loss of investments as the assets may not be put to any alternate use.

FY2005 annual report, page 21:

Company has provided for impairment losses of Rs. 64 million on certain fixed assets which due to changing market and technology could not be put to any alternative use at present

Similarly, in FY2012, the company had to write off ₹8.5 cr when a customer shut down its business and the company could not reuse its assets for any other purpose.

FY2012 annual report, page 12:

The depreciation includes impairment provision of Rs. 84.52 million relating to assets at an electronic gases customer’s site, arising from the discontinuance of their operations.

Recently, in FY2021 when the company sold its interest in the Bellary plant to JSW Steel Ltd, then it recognized an impairment of about ₹19 cr on its investment.

FY2021 annual report, page 157:

The exceptional items also include impairment of Belloxy Investment (refer note 16) of Rs 189.74 million

As a result of the capital-intensive nature of the business, which also experienced multiple instances of impairment, the asset turnover of Linde India Ltd had been low. Going ahead, an investor should keep a close watch on the fixed asset turnover levels of the company to assess if it can efficiently utilize its plants.

Further advised reading: Asset Turnover Ratio: A Complete Guide for Investors

b) Inventory turnover ratio of Linde India Ltd:

The inventory turnover ratio (ITR) of the company has improved from 20 in FY2014 to 43 in FY2023. An increasing ITR indicates an improvement in the efficiency of the company in the utilization of its inventory.

Over the years, there have been only limited instances of inventory write-offs by Linde India Ltd. In FY2000, the company provided for about ₹1.1 cr of obsolete inventory on its books.

FY2000 annual report, page 27:

Company has provided for…sIow/non-moving and obsolete inventories including adjustment for net shortage of Rs 11,046 thousand

Going ahead, an investor should keep a close watch on the inventory position of the company to understand whether it can maintain the efficiency of its inventory utilization.

Further advised reading: Inventory Turnover Ratio: A Complete Guide

c) Analysis of receivables days of Linde India Ltd:

Over the years, the receivables days of Linde India Ltd have decreased from 73 days in FY2014 to 52 days in FY2023. It indicates that overall, the company has been able to collect its money from customers in time.

However, in the past, there have been instances where Linde India Ltd had to write off debts/receivables, which it realized that it could no longer collect from its customers.

For example, in FY2000, it provided about ₹40 cr. in doubtful debt and other current assets.

FY2000 annual report, page 5:

considered it appropriate to provide Rs 402 million towards obsolete assets and unrecoverable debts

Thereafter, almost every year, the company had to provide for about ₹5-7 cr of unrecoverable trade receivables.

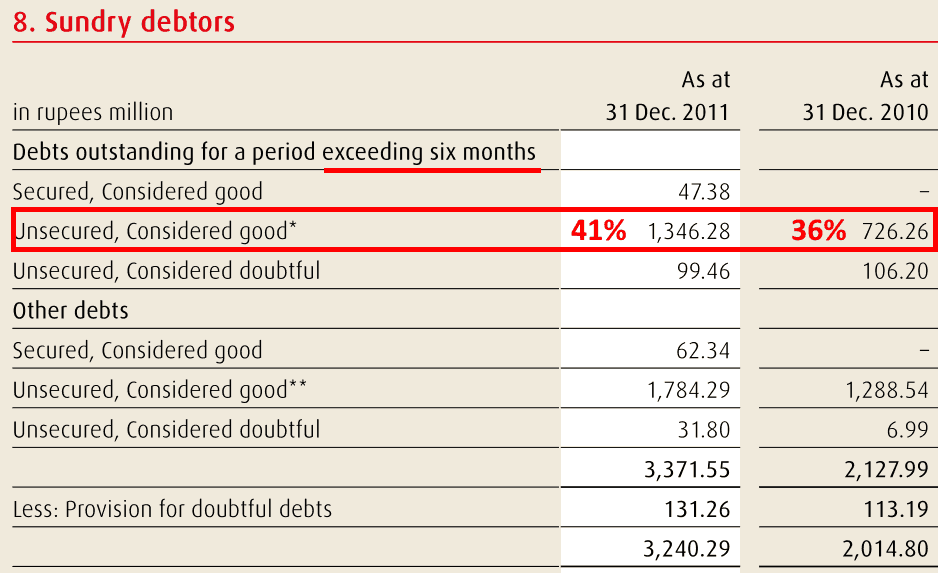

At one point in time, in FY2010-FY2011, it seems that the company faced challenges in the timely collection of receivables because it had more than 35-40% of its trade receivables outstanding for more than 6 months.

FY2011 annual report, page 45:

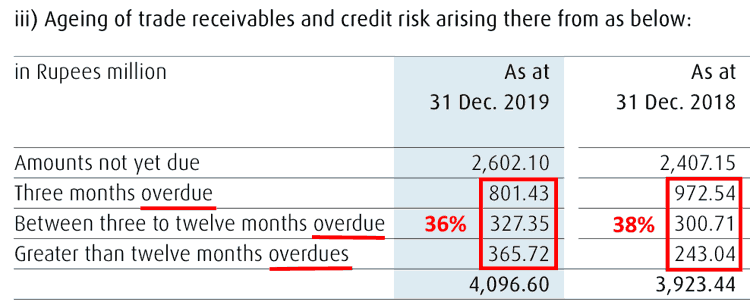

The situation stayed the same over the years, as in FY2019, almost 36-38% of overall trade receivables were overdue for at least 3 months or above.

FY2019 annual report, page 153:

As per the FY2023 annual report, page 171, on March 31, 2023, more than ₹21 cr of trade receivables were overdue for more than 3 years for Linde India Ltd. This number was about ₹20 cr on December 31, 2021.

Going ahead, an investor must keep a close watch on the receivables position of the company to check if it can collect its money on time from its customers.

Further advised reading: Receivable Days: A Complete Guide

When an investor compares the cumulative net profit after tax (cPAT) and cumulative cash flow from operations (cCFO) of Linde India Ltd for FY2013-23, then she notices that over the last 10 years (FY2013-FY2023), the company has converted its profit into cash flow from operations.

Over FY2013-23, Linde India Ltd reported a total net profit after tax (cPAT) of ₹2,091 cr. During the same period, it reported cumulative cash flow from operations (cCFO) of ₹3,547 cr.

It is advised that investors should read the article on CFO calculation, which would help them understand the situations in which companies tend to have the CFO lower than their PAT. In addition, the investors would also understand the situations when the companies would have their CFO higher than the PAT.

Further advised reading: Understanding Cash Flow from Operations (CFO)

Learning from the article on CFO will indicate to an investor that the cCFO of Linde India Ltd is higher than the cPAT due to the following factors:

- Depreciation expense of ₹1,860 cr (a non-cash expense) over FY2013-FY2023, which is deducted while calculating PAT but is added back while calculating CFO.

- Interest expense of ₹703 cr (a non-operating expense) over FY2013-FY2023, which is deducted while calculating PAT but is added back while calculating CFO.

The Margin of Safety in the Business of Linde India Ltd:

a) Self-Sustainable Growth Rate (SSGR):

Read: Self Sustainable Growth Rate: a measure of Inherent Growth Potential of a Company

Upon reading the SSGR article, an investor would appreciate that if a company is growing at a rate equal to or less than the SSGR and it can convert its profits into cash flow from operations, then it would be able to fund its growth from its internal resources without the need of external sources of funds.

Conversely, if any company attempts to grow its sales at a rate higher than its SSGR, then its internal resources would not be sufficient to fund its growth aspirations. As a result, the company would have to rely on additional sources of funds like debt or equity dilution to meet the cash requirements to generate its target growth.

An investor may calculate the SSGR using the following formula:

SSGR = NFAT * NPM * (1-DPR) – Dep

Where,

- SSGR = Self Sustainable Growth Rate in %

- Dep = Depreciation rate as a % of net fixed assets

- NFAT = Net fixed asset turnover (Sales/average net fixed assets over the year)

- NPM = Net profit margin as % of sales

- DPR = Dividend paid as % of net profit after tax

(For systematic algebraic calculation of SSGR formula: Click Here)

Over the years, Linde India Ltd had an SSGR in negatives to a low level of 2-5%. In comparison, the sales growth achieved by the company over the last 10 years (FY2013-23) is 9-10%. Therefore, the company has grown beyond what its business model can sustain from inherent cash flows.

As a result, over the years, Linde India Ltd had to rely on debt as well as equity dilution from its promoters be it BOC Group or Linde Group.

For example, in 1997, it raised about ₹130 cr for the construction of a 1,290 TPD plant at Jamshedpur.

FY1997 annual report, page 36:

In FY2008, the company raised about ₹600 cr when Linde Group acquired BOC Group. The company used this money to repay the debt it had raised to construct various plants in the past.

FY2008 annual report, page 13:

During the year, the Company received a sum of Rs.5973 million from the promoter Group…Company utilised a sum of Rs.2190 million towards repayment of its existing borrowings, thus becoming a ‘zero debt’ company at present.

Thereafter, Linde India Ltd, primarily relied on its holding company to raise debt to fund the construction of its plants. For example in FY2012, it raised ₹555 cr from Linde AG for construction of projects for Tata Steel at Kalinganagar and Asian Peroxide.

FY2012 annual report, page 15:

for financing the Tata Steel Kalinganagar project and Asian Peroxide’s project, the Company has finalized funding arrangement of EUR 77.6 million (Rs. 5,553.83 million) by way of a new ECB facility from the parent Company, Linde AG.

Linde India Ltd continued to raise debt from Linde group entities to meet its funding requirements. For example, in FY2015, it raised ₹50 cr from Linde Engineering India Ltd as an inter-corporate loan.

FY2015 annual report, page 16:

Company has also availed an inter corporate loan of Rs. 500 million from Linde Engineering India Private Ltd.

Currently, the company has very low debt because CCI asked the company to sell its southern business and the company used proceeds from this sale to repay its debt.

Credit rating report by CRISIL, February 2020:

Linde has divested assets in southern region at total consideration of Rs. 1380 crore, the proceeds were utilized to prepay the debt to the tune of Rs. 866.8 crore.

Therefore, an investor should note that over the years, Linde India Ltd has grown its business beyond what its internal cash flows could support. As a result, it had to rely on equity infusion as well as debt from its promoters. The company could keep its debt position under control by using equity dilution and asset sales to raise funds for debt repayment.

b) Free Cash Flow (FCF) Analysis of Linde India Ltd:

While looking at the cash flow performance of Linde India Ltd for the last 10 years (FY2013-FY2023), an investor notices that it generated cash flow from operations of ₹3,547 cr. During the same period, it made a capital expenditure of about ₹1,310 cr.

Therefore, during this period (FY2013-FY2023), Linde India Ltd had a free cash flow (FCF) of ₹2,237 cr (=3,547 – 1,310).

In addition, during this period, the company had a non-operating income of ₹1,500 cr and an interest expense of ₹703 cr. As a result, the company had a total free cash flow of ₹3,034 cr (= 2,237 + 1,500 – 703). Please note that the capitalized interest is already factored in as a part of the capex deducted earlier.

Linde India Ltd used its free cash flow for debt repayments of about ₹1,503 cr, paying dividends of about ₹388 cr, and has increased its cash & investment balance by about ₹1,150 cr to ₹1,224 cr on March 31, 2023.

Going ahead, an investor should keep a close watch on the free cash flow generation by Linde India Ltd to understand whether the company continues to generate surplus cash from its business.

Further recommended reading: Free Cash Flow: A Complete Guide to Understanding FCF

Self-Sustainable Growth Rate (SSGR) and free cash flow (FCF) are the main pillars of assessing the margin of safety in the business model of any company.

Further advised reading: 3 Simple Ways to Assess “Margin of Safety”: The Cornerstone of Stock Investing

Additional aspects of Linde India Ltd:

On analysing Linde India Ltd and after reading annual reports, its credit rating reports and other public documents, an investor comes across certain other aspects of the company, which are important for any investor to know while making an investment decision.

1) Related party transaction of Linde India Ltd with its promoter group, shareholders’ rejection and SEBI investigation:

Over the years, Linde India Ltd has entered into numerous transactions with its holding company as well as other promoter group companies. These transactions vary from taking interest-bearing loans, sale of goods, purchase of goods and services from promoter entities etc.

When the company was a part of the BOC group, then the amount of related party transactions was moderate and primarily included supervisory services ranging from about ₹5-10 cr each year. However, after the takeover by Linde Group and post the merger with Praxair Group, the size of related party transactions of Linde India Ltd with its promoter group companies has increased significantly.

In 2020, Linde India Ltd and Praxair India Pvt. Ltd formed a JV company (50:50), LSAS Services Private Ltd. for handing over numerous administrative, sales & marketing, procurement and consulting functions to the JV company.

FY2019 annual report, page 10:

Joint Venture Company will render Operation and Management Services to both the joint venture partners for their respective functions including Procurement, SHEQ, Human Resources, Finance, IT, Legal, Administration, Business Development, Onsite account management, Sales & Marketing, Product Management on an arms’ length basis.

In FY2023, Linde India Ltd purchased goods/equipment of about ₹375 cr and availed services of about ₹222 cr from its promoter group entities. (FY2023 annual report, page 196).

In FY2022, it purchased goods of about ₹214 cr and services of about ₹187 cr from related parties (FY2021 annual report, page 172).

In the past, it spent large sums of money on buying capital goods from its holding company, Linde AG. For example, in FY2012, it purchased fixed assets for about ₹558 cr from its related parties (FY2012 annual report, page 72).

In the annual general meeting (AGM) held on June 24, 2021, shareholders rejected the company’s proposal of entering into related party transactions with Praxair India Private Ltd. and Linde South Asia Services Private Ltd. with 93.9486% of shareholders voting against the resolution. (Source: click here, page 10).

Result: The above resolution was not passed as the votes cast against the resolution were greater than the votes cast in favour.

In FY2023, the company breached its pre-approved limit for related party transactions and the secretarial auditor highlighted as non-compliance with regulations in its report dated May 26, 2023, page 5 (Source: click here).

value in case of two transactions were exceeded the pre-approved amounts and were ratified subsequently by the Audi Committee.

Later, shareholders raised objections to the related party transactions being entered by the company with promoter group entities and as a result, the Securities and Exchange Board of India (SEBI) started an investigation into the matter and summoned the managing director (MD) and secretary of the company in Oct. 2023 along with relevant information. Later on, in January 2024, SEBI also summoned independent directors of the company. Now, the company has filed a writ petition in the Hon. Bombay High Court to stop the investigation by SEBI (Source: click here, pages 2 and 9)

An investor should keep a close watch on the development related to the SEBI investigation as any adverse outcome can have a significant impact on the company. She should also monitor all related party transactions by Linde India Ltd with its promoter group entities. This is because related party transactions provide an avenue for promoters to shift economic benefits from public shareholders to themselves by selling goods or services to the company at prices higher than market prices or buying goods or services from the company at prices lower than market prices.

Also read: How Promoters benefit from Related Party Transactions

It seems that the holding company of Linde India Ltd wishes to run it like a privately held company with the freedom of deciding about the movement of money and material across promoter group companies. As a result, in the past, twice, it came up with delisting proposals. Once in January 2011 (FY2010 annual report, page 14) and again in January 2019 (FY2018 annual report, page 13). However, on both occasions, the delisting proposals failed and Linde India Ltd continues to be a publicly listed company.

2) Management Succession of Linde India Ltd:

Linde India Ltd is an Indian entity, which has seen multiple changes in its holding companies over the years.

It was previously named BOC India Ltd and was a part of the BOC Group, UK. In 1999, Air Products and Chemicals of USA and Air Liquide of France attempted to buy BOC Group UK; however, the takeover bid failed as the Federal Trade Commission of USA did not grant its permission (FY2000 annual report, page 12-13).

In 2006, Linde AG acquired BOC group and in Feb. 2013, the name of the company was changed to Linde India Ltd.

Thereafter, in 2017, Linde Group and Praxair Group did a merger of equals and as a result, Linde India Ltd became an entity under the combined Linde-Praxair group.

The company is run by professional management where holding companies have provided leadership to the company. In 2023, Mr M J Devine joined the company as its new chairman.

Therefore, over the years, holding companies have provided continuity in leadership and it does not depend on any promoter family for succession planning.

Further advised reading: How to do Management Analysis of Companies?

3) Remuneration paid by Linde India Ltd to its managing director:

Linde India Ltd had paid remuneration to its managing director, which was more than legal limits. The secretarial auditor of the company highlighted it in its report.

FY2014 annual report, page 27:

The remuneration paid to the Managing Director for financial year ended 31 December 2014 was in excess of limits…Company is seeking the shareholders’ approval by way of a special resolution, for waiver of such excess.

Subsequently, the company pointed out to its shareholders that there is no limit on the remuneration that it can pay to its managing director as he is working in his professional capacity.

FY2018 annual report, page 37:

Pursuant to para B of Section II of Part II of Schedule V of the Companies Act, 2013, no ceiling limit is applicable to Mr Moloy Banerjee, Managing Director since he is functioning in a professional capacity

An investor should always monitor the remuneration paid by the company to its senior management. This is because, many times, professionals running the company tend to prioritise their interests by rewarding themselves via higher remunerations whereas shareholders might suffer due to subdued performance of the company.

Also read: Are professionally managed companies safer for shareholders?

4) Weakness in internal controls and processes of Linde India Ltd:

Certain instances indicate that internal controls and processes at Linde India Ltd have a scope for improvement.

4.1) Fraud by employees on Linde India Ltd:

In FY2019, the company identified that some employees had committed fraud of about ₹3.6 cr on the company.

FY2019 annual report, page 132:

The management of the Company has detected…misappropriation of Company’s fund, which was committed by employees in connivance with some contractual employees and vendors. The amount of misappropriation of funds involved in the fraud over last four years amounted to Rs 36 million approx.

Such fraud/misappropriation of funds indicates the requirement for strengthening of processes at the company.

4.2) Non-compliance with legal requirements by Linde India Ltd:

On multiple occasions, Linde India Ltd failed to comply with statutory guidelines.

In the FY2014 annual report, page 27, the secretarial auditor pointed out that the company did not comply with legal limits while payment of salary to its MD. In addition, the auditor also pointed out that the company was yet to finalize a whistleblower policy, remuneration policy and policy on related party transactions. In addition, the company was yet to file a return for a change of 2% in the shares held by promoters and top 10 shareholders.

As per the secretarial audit report dated May 26, 2023, the company exceeded the pre-approved limit on transactions with related parties.

In addition, in FY2023, the company did not deposit TDS (tax deducted at source) to income tax authorities on time.

Moreover, the statutory auditor of the company highlighted in the FY2023 annual report, page 146 that the company did not provide it internal audit report for January 1, 2023, to March 31, 2023.

As per the FY2020 annual report, page 46, Linde India Ltd delayed the transfer of shares to the Investor Education and Protection Fund Authority.

4.3) Presentation of data in the annual report by Linde India Ltd:

As mentioned earlier, the statutory auditor of the company in its report signed on May 23, 2023, which was submitted by the company to stock exchanges on May 26, 2023 (Source: BSE), highlighted that the company exceeded pre-approved limits for related party transactions in case of two transactions. However, in the secretarial audit report included in the FY2023 annual report, pages 36-37, which was also signed by the auditor on May 23, 2023, this observation is excluded.

An investor may approach the company directly to understand why the observation about exceeding the limit of related party transactions, which was there in the audit report filed with stock exchanges was absent in the audit report included in the annual report.

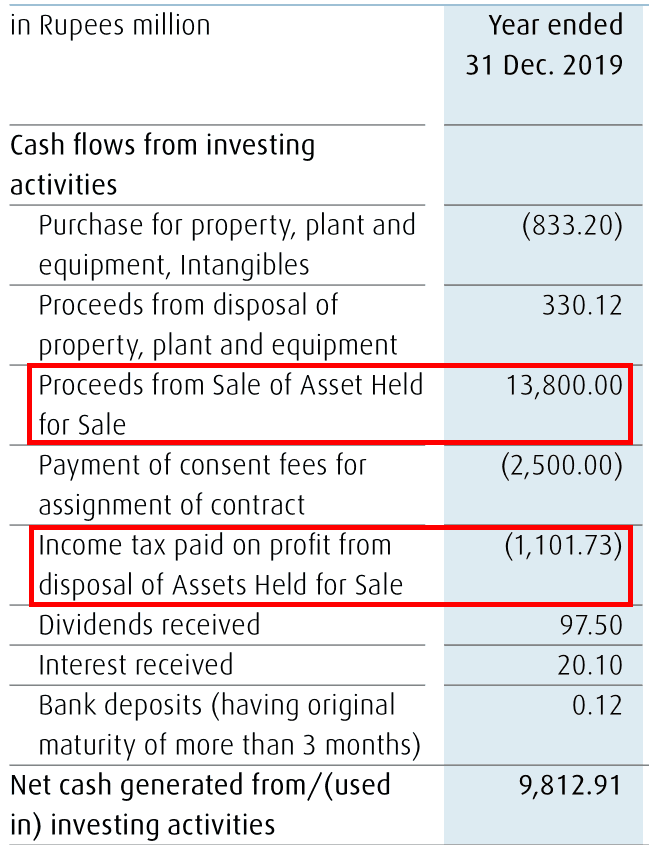

In multiple annual reports, while disclosing cash inflow from the sale of properties/land/factories in the cash flow statement, Linde India Ltd has included both the overall cash inflow as well as tax outflow in the section cash flows from investing activities.

For example, in FY2019 annual report, page 137, showed an inflow of ₹1,380 cr from the sale of assets held for sale as well as the tax paid on this transaction, the outflow of ₹110 cr in the cash flows from investing activities.

Generally, all the tax payments are shown as outflow under cash flow from operating activities.

Shifting tax outflows from operating activities to investing activities increases the cash flow from operating activities shown in the annual report.

Also read: How Companies Manipulate Cash Flow from Operating Activities (CFO)

On some occasions, Linde India Ltd has disclosed significant amounts as “Miscellaneous Expenses” under “Other Expenses” without providing details about what these expenses pertain to. For example, in FY2017, miscellaneous expenses were about ₹79 cr, in FY2016, these were ₹93 cr, in FY2014, these were ₹76 cr and in FY2013, these were ₹62 cr.

An investor may approach the company directly to get a further breakup of miscellaneous expenses.

Additionally, over the years, the company has changed its financial year multiple times, which forces an investor to be extra attentive while analysing the year-on-year financial data of the company. For example, the company presented 15-month results in FY2023, 9-month results in FY2007, and 18-month results in FY2000, FY1994 and FY1989.

It is advised that an investor keeps it in mind while analysing the financial performance of Linde India Ltd.

5) Project execution by Linde India Ltd:

Over the years, the company has executed numerous projects for its tonnage plants, and air separation units (ASUs) as well as for other customers under its project engineering division, which indicates good execution skills by the management.

For example, it executed a 1,290 TPD plant at Jamshedpur in 1998, which was completed three months ahead of schedule.

FY1998 annual report, page 14:

the project was completed in 15 months, three months before schedule. The plant is designed to meet the additional gases requirements of Tata Steel (TISCO)

In FY2004, it completed a new plant of 225 TDP at Jamshedpur before time and budgeted costs.

FY2004 annual report, page 20:

commissioned the 225 tonnes per day plant at Jamshedpur before time and significantly below cost.

Some of the other major plants executed by the company include 855 TPD ASU at Bellary in Karnataka, a 1,260 TPD plant at Dolvi in Maharashtra, 1,800 TPD ASU at Bellary, 1,700 TPD ASU at Rourkela for SAIL, 2,550 TPD ASU for Tata Steel at Jamshedpur, 418 TPD ASU for Jindal Stainless in Kalinganagar in Odisha, 330 TPD merchant ASU in Taloja in Maharashtra, 2,000 TPD project in Indonesia for POSCO, 2,400 TPD ASU at Tata Steel in Kalinganagar etc.

Nevertheless, on many occasions, the plants run by the company faced operational challenges impacting production.

For example, in FY2000, the Jamshedpur plant faced issues due to power equipment (FY2000 annual report, page 14). The same plant again faced technical problems in April 2001 (FY2001 annual report, page 18). Once again, in FY2005, this plant faced a major breakdown.

FY2005 annual report, page 20:

the 1290 tonnes per day (tpd) plant at Jamshedpur could not be operated at full production capacity in the month of August 2004 due to a major breakdown in the plant

Once again, in FY2007, this plant faced issues and was shut down for multiple weeks in Dec. 2006 and May 2007.

FY2007 annual report, pages 18, 20:

technical problems faced at the Company’s 1290 tpd air separation plant in Jamshedpur which led to its shutdown for a period of 20 days during the month of December 2006

On the basis of…root cause analysis carried out by the global team of experts…Company has taken a planned shutdown of the plant in the first week of May 2007 for major repairs,

In FY2010, the Taloja and Bellary plants of the company faced problems.

FY2010 annual report, page 12:

The plant outage in Taloja was caused by a transformer failure and the outage of the 1800 tonnes per day plant at Bellary was caused due to failure of the Siemens main air compressor

In FY2011, another ASU in Jamshedpur faced challenges in operations and production was shut down (FY2011 annual report, page 12).

In FY2018, once again a large ASU in Jamshedpur faced a breakdown and production was hampered from January 2018 until June 2018.

FY2018 annual report, page 10:

breakdown of certain critical equipment at a large air separation unit at a customer site in Jamshedpur, which occurred in the third week of January 2018….the ASU operated at a turned down capacity, which continued till the 1st week of June 2018

Going ahead, an investor should keep a close watch on the progress of the construction of its new projects as well as the operations of its existing projects.

While assessing project dynamics, an investor should also keep in mind the contingent liability on the company of Asset Restoration Obligation to dismantle the plant installed at the customer’s location after the contract is over.

FY2023 annual report, page 163:

Asset Restoration cost:…amount that it may have to incur towards liabilities related to restoration of soil and other related works, which are due upon the closure of certain of its onsite plants.

On March 31, 2023, the company estimated these liabilities at about ₹42 cr (FY2023 annual report, page 176).

6) Certain decisions taken by the company:

In the past, the company has made some decisions, which demand the attention of investors.

For example, in FY1998, the company decided to pay rent for the next 20 years as an advance to the counterparty.

FY1998 annual report, page 25:

Prepaid expenses in Schedule 9 include Rs 28,080 thousand towards rent adjustable over a period of 20 years from April 1998

An investor would appreciate that it is uncommon for any entity to pay advance rent for 20 years for any property especially due to two main reasons. First, if the company invests the amount of advance rent of 20 years and generates a return of about 5% on it, then it can easily pay the annual rent from the returns without utilizing the corpus. Second, over 20 years, rental markets may change and rent might decrease as well like during the 2000 and 2008 recessions.

In FY2007 (April 2006-March 2007), the company used short-term funds of ₹77 cr for long-term investments and during April 2007-Dec. 2007 period, it used ₹216 cr of short-term funds for long-term purposes. Such practices had the potential to generate cash flow mismatches for the company (FY2007 annual report, page 64 and April 2007-Dec. 2007 report, page 67).

In FY1998, the company acknowledged that its human resource practices had made a mistake as it did not recruit enough managers, which now has led to a talent crunch hurting the company.

FY1998 annual report, page 13:

slowdown in recruitment of managers in the past has depleted the human resource capital of your Company and your Board believes that the total implications of this depletion are only now beginning to be felt.

Similarly, the company also showed inefficiency in utilizing its assets as at one point of time it had more than 9,000 cylinders lying unused.

FY2001 annual report, page 6:

Since 1998 more than 9000 idle cylinders have been put into productive use.

Therefore, an investor should read between the lines to understand various decisions taken by the company and their impact on its performance.

The Margin of Safety in the market price of Linde India Ltd:

Currently (March 7, 2024), Linde India Ltd is available at a price-to-earnings (PE) ratio of about 113 based on consolidated earnings of the last 12 months (January 2023 to December 2023).

Moreover, we recommend that an investor read the following articles to assess the PE ratio to be paid for any stock, which takes into account the strength of the business model of the company as well. The strength in the business model of any company is measured by way of its self-sustainable growth rate and the free cash flow generating the ability of the company.

In the absence of any strength in the business model of the company, even a low PE ratio of the company’s stock may be sign of a value trap where instead of being a bargain; the low valuation of the stock price may represent the poor business dynamics of the company.

- 3 Principles to Decide the Ideal P/E Ratio of a Stock for Value Investors

- How to Earn High Returns at Low Risk – Invest in Low P/E Stocks

- Hidden Risk of Investing in High P/E Stocks

Analysis Summary

Overall, Linde India Ltd has grown its sales at a rate of about 9% over the last 10 years (FY2013-2023). Its operating profit margins seem to have increased from about 15% until FY2018 to 25% from FY2019 onwards; however, it is due to the adoption of Ind AS 115, which excludes power costs reimbursable by customers from revenues as well as expenses.

Linde India Ltd produces commodity gases and faces intense, price-based competition from many large MNC players as well as other large domestic players and numerous small unorganized players. Its customers are primarily very large steel companies, which do not give it a lot of pricing power. As a result, the business of Linde India Ltd is impacted by the cyclical nature of its customer industries like steel, automobile, oil & gas etc.

To reduce the impact of cyclicity, Linde India Ltd has attempted to diversify its business into cement, aluminium, packaged merchant gas segment, healthcare etc. However, it faced challenges when its investments for a photovoltaic customer had to be written off when the customer shut down its business.

Due to a lack of pricing power, in the business of industrial gases, a company has to be as cost-efficient as possible. Therefore, Linde India Ltd has attempted to benefit from economies of scale by growing its business size; both by organic and inorganic (acquisitions) route. The company has tried to make the best use of its plants by refurbishing, relocating and reusing them in different customers’ premises one after another.

The company has shut down its economically unviable plants, selling them, monetizing idle properties, relieving excess manpower via VRS and attempting to be as power efficient as possible because power cost is the major input cost.

Linde India Ltd faces regulatory challenges as its and its customers’ operations are considered hazardous and impact the environment. As a result, it continuously invests in technologically advanced machinery and at times, it had to write off its old machinery that could not be put to any alternate use.

The business of Linde India Ltd is highly capital intensive and it continuously needs to raise debt as well as equity to fund its growth plans. As a result, after every few years, it ends up laden with significant debt.

Over the years, it has kept its financial position under control by refinancing high-cost debt with low-cost ones, repaying debt by raising money from its promoting companies and using money from asset sales.

The company faces issues in the collection of money from customers as at times, overdue receivables form a large part of its overall debtors. At times, the company had to write off significant sums of money as non-collectible.

It seems that the MNC holding companies of Linde India Ltd want to run it like a private company with the freedom to move resources between their group companies. As a result, twice, they attempted to delist the company; however, each time, they failed. As a result, Linde India Ltd stayed publicly listed.

However, the holding companies have engaged in large-sized related party transactions with Linde India Ltd, which, at times, have exceeded approved limits. As a result, shareholders have objected to these large related party transactions by the company and rejected a board resolution on related party transactions by the company.

Currently, the stock market regulator, SEBI, is investigating the company for its related party transactions and has summoned its MD, secretary and independent directors. The investigation is still going on. The company has approached the Hon. Bombay High Court with a writ petition to stop the investigation by SEBI in this matter.

In the past, Linde India Ltd has given excessive remuneration to its managing director, which was pointed out by its auditors.

Some instances like fraud by employees who misappropriated funds from the company, non-compliance with legal requirements, data presentation in its annual reports etc. indicate that the company has a scope for improvement in its internal controls and processes.