Apollo Micro Systems Ltd is an electronics and electromechanical systems manufacturer focusing on the defence industry. In the recent past, the company has witnessed a significant growth in business due to the increased focus of the Indian government on domestic purchases of weapons and equipment. The Indian government wishes to create a large ecosystem of local defence manufacturers to increase self-sufficiency and reduce dependence on other countries for defence. As a result, almost all companies catering to the defence sector have witnessed a significant increase in their order books.

Apollo Micro Systems Ltd has significantly increased its manufacturing capacity to execute the current order book and, in anticipation of large orders from the transition of current developmental projects into production phases.

This seems to have enhanced investors’ interest in Apollo Micro Systems Ltd, leading to a significant increase in its share price.

However, in our experience of about two decades in stock markets, we have noticed that during the times of euphoria of increasing sales and profits, at times, investors might overlook and underestimate key risks that might be of concern to long-term investors.

Therefore, in the current article, we focus on aspects, like the ability of Apollo Micro Systems Ltd to convert profits into cash, funding of its growth only through external capital, and the impact of promoter-level leverage on incentives and governance.

Please note that this analysis is not about arriving at a buy or sell conclusion on the company. Instead, it focuses on identifying commonly overlooked aspects that tend to get ignored during periods of strong growth narratives but play a critical role in determining whether reported growth can translate into long-term shareholder value creation.

Key Aspects Long-Term Investors Should Not Miss

Key Risk Areas That Deserve Closer Scrutiny:

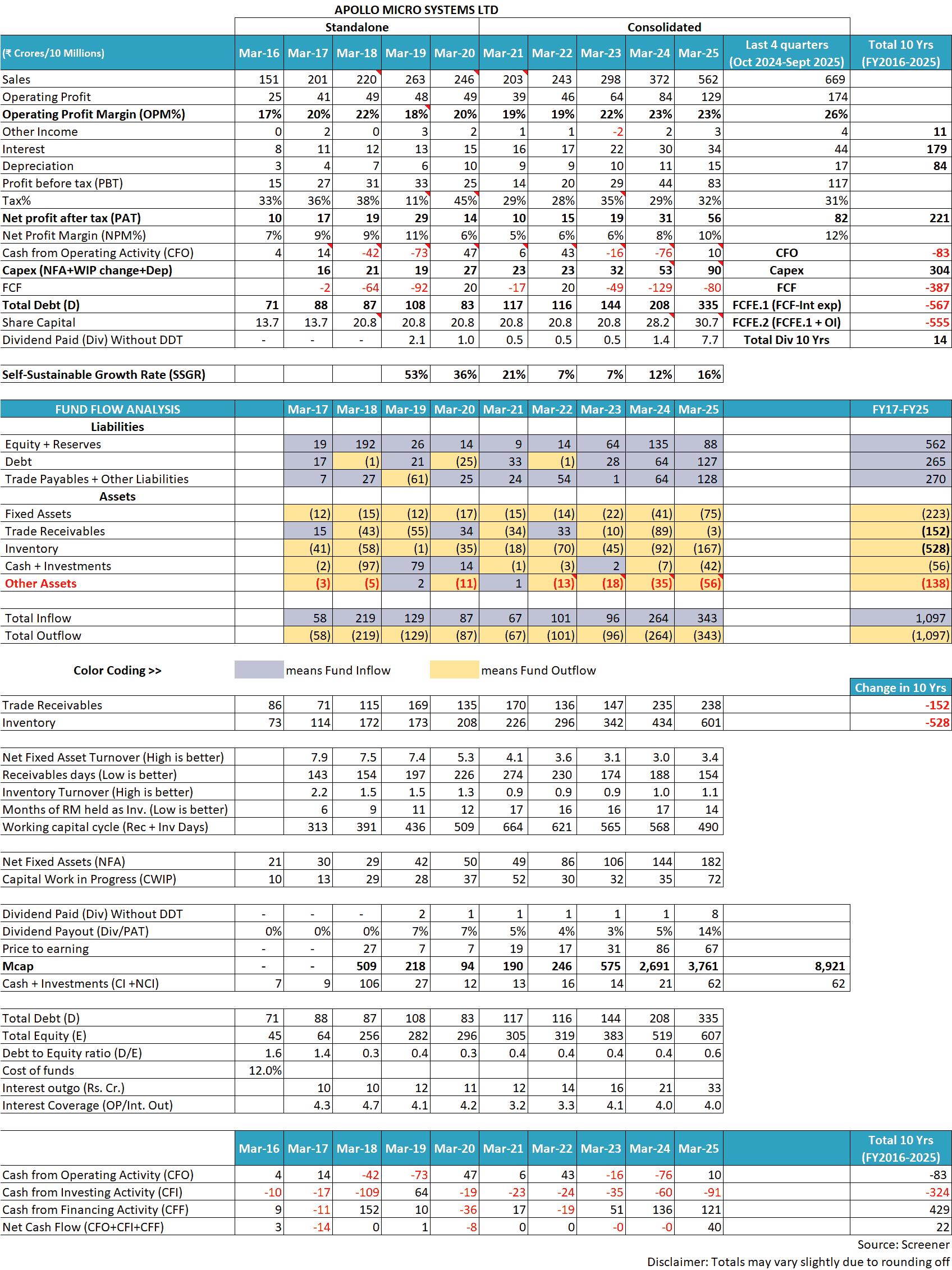

A snapshot of the financial performance of Apollo Micro Systems Ltd over the last 10 years is provided below to set the context for the discussion that follows:

1) No cash flow generation by Apollo Micro Systems Ltd from its business:

Over the last 10 years (FY2016-FY2025), the company reported a cumulative net profit after tax (cPAT) of ₹221 cr. However, during this period, it reported a negative cumulative cash flow from operations (cCFO) of (₹83) cr, indicating that Apollo Micro Systems Ltd could not convert its profits into cash.

The key reason for all its profits and much more money getting stuck in business is its high working-capital-intensive business model, where a large amount of money gets stuck in trade receivables and inventory.

Credit rating report by Acuité Ratings & Research Limited, July 2025, page 4:

AMSL’s working capital cycle remains significantly elongated…primarily driven by stretched receivables and elevated inventory levels

Apollo Micro Systems Ltd has to keep a significant amount of inventory because, on the one hand, some of its raw materials need a lead time/advance-booking time of up to 2 years, and on the other hand, it needs to keep sufficient inventory to give uninterrupted, prompt supply to its customers.

Conference call transcript, February 2025, page 11:

Krishna Sai Kumar:…The existing lead times of certain raw material are as small as a couple of weeks to as big as 2 years actually

Presentation, Q4-FY2025 results, May 2025, page 42:

our working capital cycle tends to be high. This is primarily driven by the need to maintain adequate inventory levels for defence-critical and mission-critical systems, ensuring uninterrupted supply in line with the Ministry of Defence’s requirements and operational readiness standards.

No wonder that during FY2016-FY2025, when the sales of Apollo Micro Systems Ltd increased to 3.72 times from ₹151 cr in FY2015 to ₹562 cr in FY2025, its inventory levels increased to 8.23 times from ₹73 cr in FY2015 to ₹601 cr in FY2025. During this period, its inventory turnover ratio declined from 2.2 in FY2016 to 1.1 in FY2025.

This indicates a significant deterioration in the efficiency of inventory utilisation and also points to the fact that, as Apollo Micro Systems Ltd has grown its business, its inventory requirements have grown at a much faster pace, requiring it to keep infusing significantly more and more money in its business/working capital.

Readers interested in understanding how reported profits can diverge from operating cash flows over long periods may refer to the detailed discussion here: Understanding Cash Flow from Operating Activities (CFO).

In addition to inventory, the business of Apollo Micro Systems Ltd also suffers from very elongated receivables, leading to a stretched liquidity position.

The company is not in a situation where once it has delivered the goods, then simply after a fixed period of time (30/45 days), it will get its money from customers. Instead, its customers take a significant amount of time to thoroughly test its products after delivery, and only upon satisfactory performance of the products are its payments released.

Credit rating report by Acuité Ratings & Research Limited, July 2025, page 4:

systems supplied by the company are subject to post-delivery testing by customers, and payments are released only upon successful completion, contributing to elevated debtor day

Due to such delays, at times, Apollo Micro Systems Ltd has faced large delays in getting money. For example, its receivables days deteriorated to about 274 days in FY2021, indicating that it received its money almost 9 months after delivering the goods.

Even on March 31, 2025, Apollo Micro Systems Ltd had significant receivables (more than ₹27 cr) outstanding for more than 3 years from the date they became due for payment.

FY2025 annual report, page 262:

Due to such delayed payments by customers and continuous requirement to purchase raw material for uninterrupted supply, Apollo Micro Systems Ltd has to rely on various methods, like delaying payments to their suppliers.

Credit rating report by Acuité Ratings & Research Limited, July 2025, page 4:

To partially fund its working capital needs, the company stretches creditor payments

However, as it cannot delay payments to suppliers beyond a point, therefore, it has to rely on loans to fund its business, even though it has to pay very high interest rates for such loans.

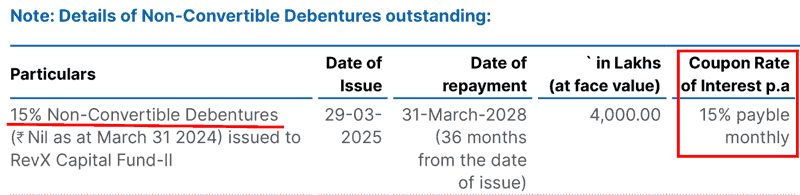

For example, in FY2025, it had to raise ₹40 cr by issuing non-convertible debentures at an interest rate of 15% per year.

FY2025 annual report, page 267:

As the payments from customers do not come on time, therefore, its banks’ loan limits are almost fully utilised.

Credit rating report by Acuité Ratings & Research Limited, July 2025, page 4:

reliance on working capital limits stood high marked by average 92 percent utilization of the fund-based limits used over the past six months ending in Mar 2025.

At times, such liquidity constraints have directly constrained business growth. Due to such liquidity problems, Apollo Micro Systems Ltd was forced to go for an initial public offer (IPO) in January 2018. In the IPO, almost the entire money was to be used for working capital and running business expenses.

RHP for IPO, January 2018, page 87:

However, even the significant equity raise in FY2018 could not fulfil the cash-guzzling nature of its business, and continued liquidity shortage led to ICRA downgrading its credit rating.

Credit rating report by ICRA, July 2019, page 1:

The ratings revision factors in the significant deterioration in Apollo Micro Systems Limited’s (AMSL) working capital cycle in FY2019 owing to an increase in debtor days, high inventory holding, and low creditors, leading to faster-than-expected deployment of funds raised through the company’s IPO in January 2018.

Large negative free cash flow leading to frequent equity dilutions and debt raising:

Cash flow-related problems of Apollo Micro Systems Ltd do not end with its working capital position. The company had to do a lot of capital expenditure as well to create additional manufacturing capacity, leading to a deeply negative free cash flow (FCF), which demanded even more capital.

During FY2016-FY2025, Apollo Micro Systems Ltd generated a negative cumulative cash flow from operations (cCFO) of (₹83) cr. However, during this period, it made a capital expenditure of ₹304 cr. Therefore, during this period, it had a negative free cash flow (FCF) of (₹387) cr (= -83 – 304).

In addition, during this period, the company had a non-operating income of ₹11 cr and an interest expense of ₹179 cr. As a result, the company had a total negative free cash flow of (₹555) cr (= -387 + 11 – 179). Please note that the capitalised interest is already factored in as part of the capex deducted earlier.

Readers who want to deepen their understanding of how cash flow differs from reported profits may refer to: Free Cash Flow: A Complete Guide to Understanding FCF for a detailed conceptual explanation.

Apollo Micro Systems Ltd funded this cash flow gap by raising equity (₹1,108 cr) and incremental debt (₹265 cr).

- In FY2018, the company raised equity of about ₹182 cr. by issuing shares in IPO (₹156 cr), preferential allotment (₹5.8 cr) and compulsory convertible debentures (CCDs) (₹20 cr).

- In FY2023, the company raised equity of about ₹184 cr by issuing warrants that were exercised in FY2024 and FY2025),

- In FY2026, the company has raised about ₹742 cr by issuing shares in preferential allotment (₹308 cr) and warrants (₹434 cr), which are being exercised at regular intervals.

- Additionally, Apollo Micro Systems Ltd raised an additional debt of ₹264 cr over FY2016-FY2025 because its total debt increased from ₹71 cr in FY2016 to ₹335 cr in FY2025.

Therefore, investors should note that the business of Apollo Micro Systems Ltd is highly cash-intensive, where incremental sales require a substantial infusion of external capital through equity dilution and debt.

Key learning for long-term investors:

When a growing company reports rising profits but consistently fails to generate operating cash flow, growth itself becomes a source of risk. In such cases, every additional rupee of sales increases dependence on external funding rather than strengthening the business. Long-term investors should always examine whether growth is self-funded or externally financed, because only the former supports sustainable compounding.

2) Promoters of Apollo Micro Systems Ltd have relied on pledging of existing shares to subscribe to new equity shares:

Investors should note that every new equity infusion by new investors in a company leads to a reduction/dilution of the shareholding of existing shareholders, including promoters.

As Apollo Micro Systems Ltd is not generating any cash flow from operating activities, it has to continuously rely on equity dilution to run its business.

In this process, the shareholding of promoters has declined from 96.79% in FY2017 (Source: FY2017 annual report, page 47) to 50.33% as of September 30, 2025 (Source: BSE).

As the promoters are barely clinging to a majority shareholding at 50.33%, they seem under a lot of pressure to keep subscribing to new shares by way of warrants etc., to maintain control of the company.

However, due to a significantly large amount of funds required by Apollo Micro Systems Ltd (over ₹1,100 cr of equity raised since FY2018), promoters also have to raise large money at a personal level to infuse in the company. Otherwise, they are on the verge of losing majority control of the company.

Due to this urgent need for significant money, promoters have relied on taking loans against their shareholding in Apollo Micro Systems Ltd by mortgaging these shares to lenders. This is reflected in a significant share of promoters’ shareholding pledged to lenders.

Conference call transcript, February 2025, page 12:

Krishna Sai Kumar: Promoter has pledged his shares because he was sourcing funds to subscribe to the warrants.

As per BSE, on September 30, 2025, 35.55% of promoters’ shareholding (i.e. 6,00,45,500 shares) were pledged to lenders (click here). At the closing share price of ₹325.60 at September 30, 2025, the value of pledged shares exceeds ₹1,950 cr.

Investors who want to understand how promoter share pledging can affect incentives and governance over business cycles may read: Share Pledge by Promoters: A Complete Guide.

Lenders usually agree to lend up to 50% of the value of shares (loan-to-value, LTV) in “loan against shares”. So, on September 30, 2025, promoters might have under debt of up to ₹975 cr (maximum value at 50% loan to value). If the lenders had asked for a higher security value, then the loan amount would be lower.

Nevertheless, as of September 30, 2025, promoters have given shares of about ₹1,950 cr to lenders, and additionally, considering that Apollo Micro Systems Ltd has raised more than ₹1,100 cr in equity in recent years, it becomes clear that promoters have raised a very large amount of money via loans against their shareholding in the company.

Such a large pledging of shares by promoters raises multiple concerns.

2.1) Promoters’ continuous focus on the share price of the company:

As the security provided for the loan amount is shares, whose prices are highly volatile, therefore, to reduce their risk, lenders continuously adjust the loan and security value as per updated prices, i.e. if share price declines, then to maintain their security cover (loan to value, LTV), lenders would ask for either additional shares or part repayment of loan.

These “mark-to-market” are highly stressful for the borrowers because they are hardly in a position to make part repayments because their financial position is already under strain for commitments to subscribe to warrants to maintain their majority shareholding in the company. If they had other large sources of money, then they would not have pledged their shares in the first place.

Therefore, the only option to get LTV at the required levels is to pledge more shares to lenders. This is seen as highly negative by the markets, which, due to increased risk, punishes the share price further, forcing promoters to pledge more shares, leading to a negative spiral.

Therefore, when a large portion of promoters’ shareholding is pledged, then promoters fear any decline in share price.

Investors should note that in such situations, promoters’ significant focus remains on increasing or at least maintaining the share price.

Such a focus on share price usually leads to behaviour like frequent release of positive news about the company. For example, the release of unaudited results just a few days after the end of the quarter (on Oct. 10, 2025), even before quarterly results are formally announced (on Nov. 4, 2025) as per SEBI timelines.

When under tremendous pressure to keep up the share price, companies tend to release announcements of every order win (however small it might be), of every memorandum of understanding (MoU) etc. In such situations, an investor should be very cautious. This is because, in the past, there have been instances where companies influenced their share price by making positive corporate announcements, which later on, SEBI found to be false.

Such pressure to keep up the share price is one of the major factors forcing companies to manipulate financial performance, also by way of aggressive accounting, accelerating revenue recognition and at times, falsifying financial statements and even fraud. For example, the following research paper at the American Economic Association: Share Pledging and Corporate Securities Fraud (Source)

We find a positive, causal relation between share pledges by controlling shareholders and detected corporate fraud.

2.2) Why pledging to subscribe to new shares weakens promoter commitment:

When promoters pledge their existing shares to raise funds for subscribing to new equity, their increased stake does not reflect additional personal capital at risk. Economically, the value of their ownership has already been monetised through borrowing.

As a result, higher promoter shareholding achieved through such mechanisms can create an illusion of commitment, while the underlying financial risk has merely shifted to lenders. Long-term investors should therefore evaluate how promoters fund their subscriptions, not just whether they participate.

Key learning for long-term investors:

Share pledging is not merely a financing decision; it reshapes promoter incentives. When personal leverage becomes significant, promoters’ priorities can shift from long-term value creation to short-term share price stability. Investors should therefore treat high pledging as a signal to scrutinise all subsequent corporate actions more closely.

3) Promoters trying to get money from Apollo Micro Systems Ltd by high remuneration and dividends:

Investors should note that when promoters raise a large loan by way of pledging of stake, then it puts a big pressure on them to make regular interest payments to lenders.

If the only source of money for promoters is their stake in the company, then promoters have to rely on it to generate more and more money for interest and principal repayments.

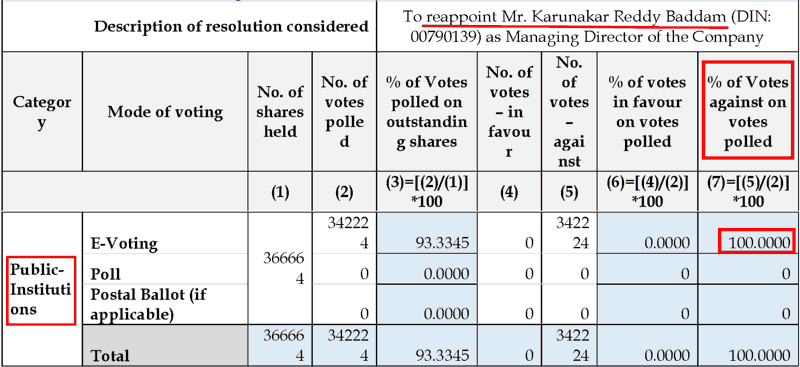

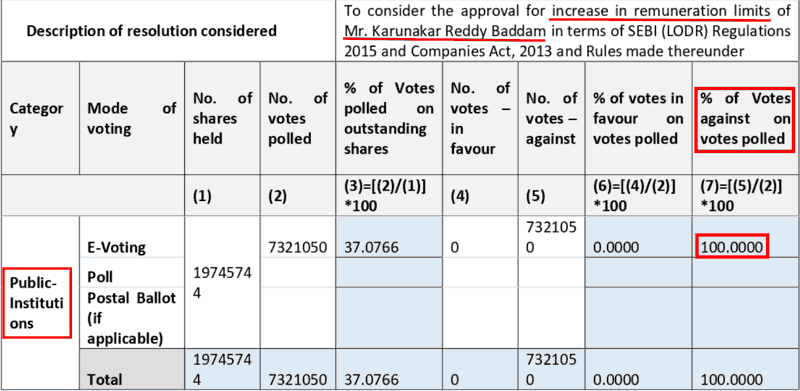

In the past, the promoters have attempted to take the maximum possible remuneration that could be allowed under the law and considering the risks of extraction of value from the company, the public shareholders, especially institutional shareholders, have voted heavily against such resolutions.

For example, in May 2022, when Apollo Micro Systems Ltd put up a resolution to increase the remuneration of promoter, Mr Karunakar Reddy Baddam to ₹1.8 cr per annum and an additional bonus of 5% of net profits (click here), then in the postal ballot ending May 11, 2022 (Source), 100% of public institutional shareholders voted against it.

However, the proposal was passed because it was an ordinary resolution, and promoters’ self-voting in its favour led to its passing.

Subsequently, in the 2023 AGM, once again, the company put up a resolution for increasing promoters’ overall remuneration to exceed ₹5 cr.

FY2025 annual report, page 49:

The remuneration of Managing Director is proposed to exceed ₹5 Crores in the coming financial year(s) and hence seeking approval of shareholders by way of special resolution

This time, again, all the public institutional shareholders voted against the resolution; however, it was passed due to self-voting by the promoters (Source).

Therefore, over the years, the promoter of Apollo Micro Systems Ltd has continuously tried to take a high remuneration, where public shareholders (especially institutions) are completely against it.

The continuous pressure from lenders to make interest and principal repayments of large loans taken by pledge of shares is likely to add to the desire of promoters to take more and more money as remuneration to make payments to lenders.

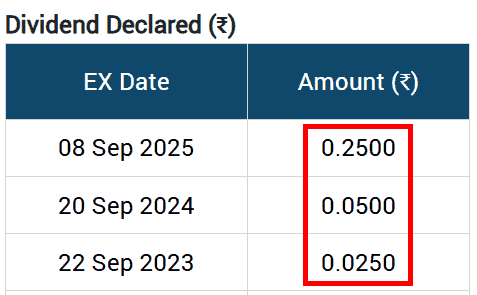

In addition to remuneration, another major source of funds for promoters from the company is dividends. Even though dividends are distributed to all the shareholders, promoters, being the largest beneficiaries due to their large shareholding and controlling position, usually influence the timing and amount of dividends.

As per the earlier discussion, an investor would note that Apollo Micro Systems Ltd has continuously suffered from negative cash flow from operations (CFO) and negative free cash flow (FCF). Therefore, the company does not have any surplus cash to pay dividends to shareholders, as all its business-generated cash is consumed in working capital and capital expenditure.

In such a situation, any dividend payment to shareholders is funded by either debt or equity dilution and not by operating cash flows.

For example, in each of the last three years, Apollo Micro Systems Ltd has reported negative free cash flow and a continuously increasing debt. However, it has declared increasing dividend amounts in 2023, 2024 and 2025 (Source: BSE).

We believe that in such a situation, dividends might be a drain on the previous resources of the company, which might be influenced by promoters’ liquidity crunch for making large interest and principal repayments to their lenders.

Moreover, investors should not take any comfort from the dividend yield in such cases, because such dividends may be stopped at any time by the lenders of the company whenever the cash flow position of the company deteriorates.

The pressure to extract cash from the company becomes more pronounced when promoters are servicing large personal liabilities arising from pledged shares. In such situations, remuneration and dividends should not be viewed in isolation, but as part of a broader liquidity stress ecosystem involving the company, its promoters, and external lenders.

The broader framework to analyse how promoters extract value from listed companies is discussed here: How to identify Promoters extracting Money via High Salaries

4) Complex group structure and related party transactions of Apollo Micro Systems Ltd:

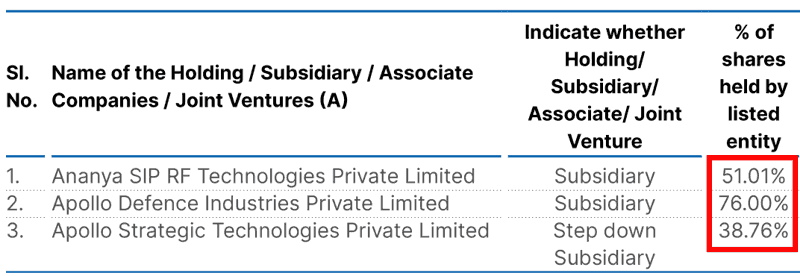

The company has multiple subsidiaries/child entities, including a step-down subsidiary, which are consolidated in its financial performance. However, all these entities are only partly owned by Apollo Micro Systems Ltd.

FY2025 annual report, page 130:

The company owns 51.01% of Ananya SIP RF Technologies Private Limited and 76% of Apollo Defence Industries Private Limited. Apollo Strategic Technologies Private Limited is 51% owned by Apollo Defence Industries Private Limited (51% * 76% = 38.76%).

The annual reports of the company do not provide complete details about who the external shareholders are owning stakes in these companies.

The presence of external shareholders in subsidiaries creates tricky situations. On account of majority shareholding, Apollo Micro Systems Ltd has to put in most/all of the efforts and funding burden, give guarantees for loans etc., for these subsidiaries. Whereas, there remains a possibility that external shareholders get a free ride along the way.

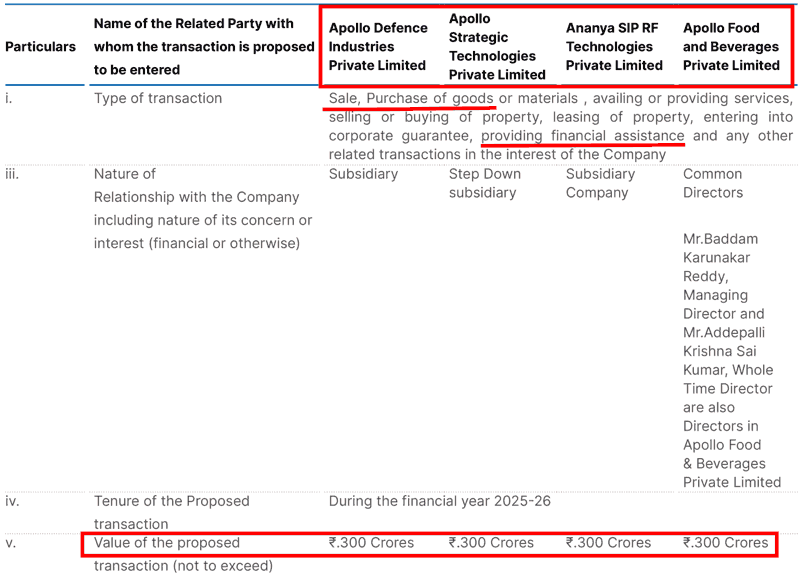

Moreover, in the corporate world, there have been multiple instances where promoters of the listed companies themselves are present directly/indirectly as external shareholders in partly owned child entities and, in turn, benefit at the cost of minority shareholders via related party transactions.

Related party transactions of listed companies with such partly-owned child entities, like sale/purchase/rent/loan/professional fees etc. provide an opportunity for shifting of economic benefit from public shareholders to external shareholders/promoters if the listed company buys goods/services from such entities at a price higher than their market price or sells goods/services to such entities at a price lower than their market price.

Therefore, public investors are always cautious of such transactions with related parties/partly-owned child entities.

Over the years, Apollo Micro Systems Ltd has attempted multiple times to get approval from shareholders to enter into related-party transactions with the above-mentioned child entities and another company, Apollo Food and Beverages Private Limited, which is owned by the promoters.

However, considering the risk to the interests of public shareholders in such transactions, public shareholders have defeated these resolutions every time.

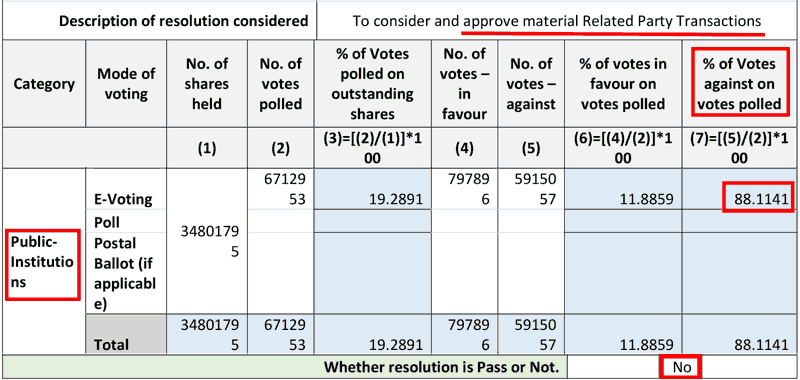

For example, in the 2025 AGM, Apollo Micro Systems Ltd proposed to enter into material related-party transactions with these entities totalling about ₹1,200 cr.

FY2025 annual report, page 67:

However, in the AGM on September 16, 2025, public-institutional shareholders voted against it and defeated this resolution (Source).

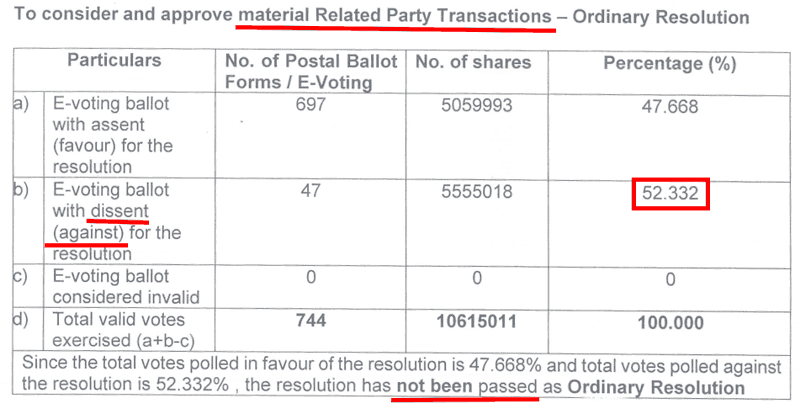

Thereafter, once again, in the postal ballot notice dated Nov. 7, 2025 (Source), Apollo Micro Systems Ltd attempted to get an approval for entering into related party transactions of about ₹1,500 cr. with its partly-owned child entities.

However, again, public-institutional shareholders voted against it and defeated this resolution a second time (Source).

By looking at this continuous tussle of the promoters attempting to get related party transactions approved and public shareholders rejecting the same again and again, an investor should understand its seriousness.

Regardless of the exact ownership structure, repeated attempts by promoters to push through large related-party transactions that public shareholders consistently reject should be viewed as a governance warning. Such persistent divergence between promoter intent and minority shareholder interests warrants heightened caution from long-term investors.

Investors looking to build a systematic approach to evaluating related-party transactions may refer to: How to Analyse Related Party Transactions of a Company.

Conclusion: What This Analysis Reinforces for Long-Term Investors

The analysis of Apollo Micro Systems Ltd reinforces the importance of looking beyond reported growth and profits when evaluating mid-sized companies. Strong growth narratives can hide structural and incentive-related risks that are easy to overlook during favourable market conditions. Over the long term, the sustainability of shareholder returns depends not only on revenues and profits, but also on how growth is funded, how cash flows behave, and how promoter incentives evolve under financial pressure.

This case also highlights how promoter incentives can gradually shift when businesses operate under sustained financial stress, especially when personal leverage and share pledging become significant. In such situations, decisions related to capital allocation, remuneration, dividends, and related-party transactions are often interconnected and therefore need to be analysed together.

For long-term investors, the key takeaway from this analysis is not limited to this company alone. It lies in consistently checking whether a business can fund its own growth, whether promoter incentives remain aligned across cycles, and whether governance structures protect minority shareholders during periods of rapid expansion. Developing this discipline helps investors avoid businesses where growth appears attractive on the surface but ultimately weakens long-term compounding.

In our premium services, this kind of analysis is used primarily as a filtering tool to eliminate businesses where long-term risks outweigh the benefits of growth. Only companies that demonstrate sustainable cash flows, prudent capital allocation, and aligned promoter incentives eventually qualify for inclusion in my long-term portfolio.

Regards,

Dr Vijay Malik

P.S.

- Subscribe to Dr Vijay Malik’s Recommended Stocks: Click here

- Chennai “Peaceful Investing” Workshop | 26 July 2026: Register Here

- To learn stock investing through videos, you may subscribe to the Peaceful Investing – Workshop Videos

- 25% savings on buying our Stock Analysis Excel Template and all ebooks together: Analysis Package: Excel Template + All eBooks (25% savings)

- To download our customized Stock Analysis Excel Template for analysing companies: Stock Analysis Excel

- Learn about our stock analysis approach in the e-book: “Peaceful Investing – A Simple Guide to Hassle-free Stock Investing”

- To learn how to do business analysis of companies: e-book: Business Analysis Guide

- To pre-register/express interest in a “Peaceful Investing” workshop in your city: Click here

Disclaimer

I, Vijay Malik, am a SEBI-registered Research Analyst (Regn. No. INH100008364). This article is for educational purposes only and does not constitute investment advice or a recommendation to buy or sell any securities. Investors should do their own research before making any investment decisions.

I, or my immediate relatives, do not have any financial interest in the companies discussed as on the date of publication of this article, nor do we hold one per cent or more of the securities of such companies at the end of the month immediately preceding it. I do not have any material conflict of interest and have not received any compensation or other benefits from the companies or any third party in relation to this article during the 12 months preceding its publication. I have not served as an officer, director, or employee of the subject companies, nor have I been engaged in market making activity for them.

8 thoughts on “Apollo Micro Systems Ltd: Key Aspects Long-Term Investors Should Not Miss”

Sir,

I appreciate your long-term research and guidance to the long-term investing community.

Who are long-term/short-term investors?

Analytical share price moments in the exchanges will also guide the gullible small investors.

Dear S A A Prasad,

Thank you for your kind words.

Broadly speaking, long-term investors focus on business quality, sustainability of cash flows, governance, and capital allocation, while short-term investors focus more on price movements, momentum, and near-term targets. Both types of investors exist at the same time in the markets, but they invest based on very different parameters.

My work is primarily focused on long-term investors who want to reduce the risk of permanent loss of capital by understanding businesses instead of relying on share price movements. While for short-term investors, market prices may provide a lot of signals, they can distract long-term investors from the underlying fundamentals.

All the best for your investing journey!

Regards,

Dr Vijay Malik

Research Analyst

I read with interest the analysis of Apollo Micro Systems Ltd. I am surprised that banks have sanctioned working capital limits when turnover ratios are far from benchmark levels.

The borrowing account would have thrown enough signals of incipient sickness. Credit appraisal systems of banks for assessing limits running into ₹100 plus crores are not up to the standard. Certainly, such high-value WC limits fall under the board’s sanctioning powers, and much due diligence must have been done.

Dear Sri Krishna,

Thank you for reading the analysis and for sharing your thoughtful observations.

You have raised an important point. In theory, large working capital limits would definitely involve rigorous appraisal, especially when exposures cross ₹100 crore and fall under the authority of higher-level sanctioning forums.

However, in practice, credit decisions are often influenced by a combination of factors beyond pure operating efficiency and current financial metrics. Future growth expectations, order book visibility, sectoral outlook, collateral/security structures, and historical relationships also play a role in sanctioning decisions.

My intent in highlighting weakness in turnover ratios and persistent working capital stress was not to suggest that banks had overlooked risks at the time of sanctioning working capital loans, but to point out that such weaknesses can prove risky for equity shareholders if sales/profit growth does not translate into internally generated cash flows.

From a long-term investor’s perspective, the key takeaway is that bank funding availability does not automatically validate company’s business quality or its capital efficiency. It simply indicates that lenders are willing to fund the operating model under their assumptions, which may or may not hold good for equity investors.

I appreciate you taking the time and add a different perspective to the discussion.

Warm regards,

Dr Vijay Malik

Research Analyst

Classic case of bashing a good company when the share price is going up. Sir, no company is 100% perfect. Stock markets are there to pick overall winners and assess the risk-to-reward ratio. Your article is not for an ordinary layman investor.

Going by your analysis, please advise at least one company that ticks all your points and whether the company’s stock price is reflecting that.

Thank you.

Dear Piyush,

Thank you for taking the time to read the article and share your perspective.

I agree with you that no company is 100% perfect, and that stock market investing ultimately involves assessing risk versus reward. My objective with such analyses is not to label companies as “good” or “bad”, nor to comment on near-term share price movements. Instead, the focus is on identifying business and governance risks that often get overlooked during strong growth phases, so that investors can make more informed decisions based on their own risk tolerance and investment horizon.

These articles are intentionally detailed and framework-driven. They are meant to help investors think more deeply about aspects such as cash flow quality, capital allocation, and promoter incentives, rather than serve as ready buy or sell calls. Different investors may arrive at different conclusions from the same information, and that is perfectly reasonable.

As for naming a company that meets all filters, in my experience, discussing specific stock recommendations in public comments is not very useful without context, portfolio construction, and risk management considerations. Each investor’s situation is different, and stock selection makes sense only when viewed as part of a broader, long-term investment approach.

I appreciate your engagement with the analysis and wish you well in your investing journey.

Regards,

Dr Vijay Malik

Research Analyst

Great analysis, sir.

What I learnt from your article:

– Business model: Cash-guzzling manufacturing for a monopsony buyer.

– Moat: Weak (L1 bidding, no pricing power).

– Economic reality: Growth is funded by dilution, not profits.

This company is a “Funding Trap.” It operates as a “pass-through” entity that takes money from shareholders to fund the Indian Government’s defence procurement delays.

Incentives: Misaligned. Management is desperate to keep its pledged shares from being sold.

Governance: Shareholders are actively blocking management proposals (a very bad sign).

Avoid any new buying.

Dear Vamshi,

Thank you for reading the article so carefully and for sharing a structured summary of your takeaways.

It is good to see that the analysis helped you connect multiple aspects, such as the business model, cash flow behaviour, funding pattern, incentives, and governance, rather than viewing each of them in isolation. This ability to link operating dynamics with capital allocation and promoter behaviour is a great advantage for long-term investors.

As highlighted in the article, the intent is not to arrive at a simple buy or avoid conclusion, but to encourage investors to identify situations where reported growth is supported more by external funding and balance sheet stress than by internally generated cash flows. In such cases, promoters’ incentives and governance decisions often become increasingly important to monitor.

I am glad the article helped reinforce these analytical frameworks. Applying the same questions consistently across different companies is what ultimately helps investors avoid unpleasant surprises over a long investment horizon.

Thank you once again for contributing to the discussion.

Regards,

Dr Vijay Malik

Research Analyst